Spanco Porter's Five Forces Analysis

Don't Miss the Bigger Picture

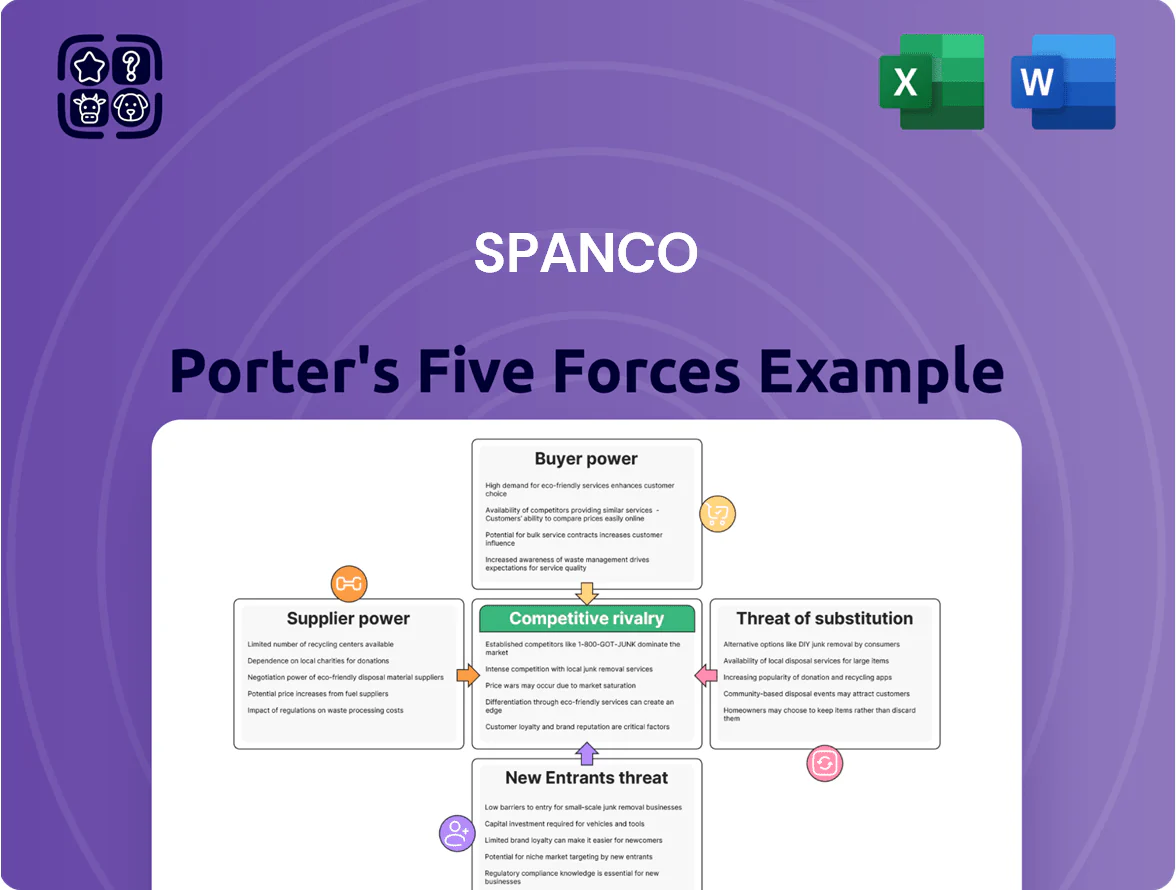

Spanco faces moderate buyer power, constrained supplier leverage, and niche-specific barriers to entry that shape its competitive landscape; competitive rivalry centers on service quality and pricing among regional players. Threats from substitutes are limited but evolving with technological logistics solutions, while regulatory and capital-intensity factors influence strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Spanco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Hardware and Software OEMs

Scarcity of Specialized Technical Talent

The Indian IT sector still loses talent in cybersecurity, cloud architecture, and system integration, with attrition in specialist roles at ~22% in 2025 vs 15% company average; demand for high-end skills pushed median cloud architect pay up 18% YoY to ₹3.6M in 2025, giving suppliers of talent leverage.

Spanco must match market benchmarks—total comp packages near ₹4M–₹5M for senior cloud/cyber roles—and offer training, equity, and hybrid work to prevent hires by Tier-1 firms like TCS and Infosys, which hired 40% of campus and lateral senior talent in 2024–25.

Dependence on Third-Party Infrastructure Providers

For large-scale e-governance projects Spanco relies on niche third-party infrastructure partners for local support; in 2025 about 32% of its project costs tied to subcontractors in regional deployments. When a sub-contractor is the sole provider in a region or tech niche, they can push prices or timelines, risking margin erosion on multi-year government contracts. Tight vendor management and dual-sourcing cut supplier leverage and helped Spanco reduce subcontractor cost inflation from 6.4% (2023) to 2.1% in 2024.

Impact of Global Supply Chain Fluctuations

As an integrator, Spanco faces price swings in semiconductors and networking gear—global chip prices rose ~15% in 2021–24 while lead times for key components averaged 22 weeks in 2023, pressuring margins.

Supply shocks through 2025 increased leverage for suppliers who can promise on-time delivery, forcing Spanco to hold strategic inventory buffers or incur SLA penalties and project delay costs.

- Semiconductor price rise ~15% (2021–24)

- Avg component lead time 22 weeks (2023)

- Buffer inventory raises working capital needs

- SLA delay penalties hit margins

Standardization of Technology Platforms

The shift to open-source stacks in 2024 reduced proprietary vendors' leverage, with 38% of government IT tenders favoring open platforms per UK Cabinet Office data, easing licensing costs for Spanco.

Still, certification and authorized-maintenance rules force Spanco to use approved service partners, keeping supplier influence on uptime and upgrade timing at a steady 15–20% impact on operational flexibility.

- 38% government tenders use open-source (2024)

- Authorized support requirement remains

- 15–20% operational flexibility impact

Supplier concentration, rising costs & talent churn squeeze cloud margins

Suppliers hold high leverage: top five OEMs = 68% market share (2025); vendor price moves cut project gross margins 3–6pp; component lead times averaged 22 weeks (2023) and supply shocks raised inventory and SLA costs; talent attrition ~22% (2025) pushed senior cloud pay to ₹3.6M; open-source adoption 38% (2024) eased licensing.

| Metric | Value |

|---|---|

| Top-5 OEM share | 68% (2025) |

| Margin sensitivity | 3–6pp |

| Lead time | 22 weeks (2023) |

| Talent attrition | 22% (2025) |

| Senior cloud pay | ₹3.6M (2025) |

| Open-source tenders | 38% (2024) |

What is included in the product

Concise Porter's Five Forces assessment for Spanco that pinpoints competitive intensity, supplier and buyer power, substitution risks, and barriers to entry, with strategic insights and editable format for reports and presentations.

Spanco Porter's Five Forces delivers a concise one-sheet assessment of competitive pressures—ideal for fast strategic decisions and slide-ready summaries.

Customers Bargaining Power

Domination of Government and Public Sector Clients

A significant share of Spanco’s FY2024 revenue—about 58% per company filings—comes from government contracts and e‑governance projects, concentrating customer power. Centralized procurement bodies like India’s eProcurement platforms enforce strict RFP terms and long payment cycles, shifting risk to vendors. Large contract sizes (single awards often >INR 50 million) let public clients set price and service standards, making them de facto price-makers.

Tender-Based Competitive Bidding Processes

The reliance on transparent, tender-based bidding raises customer bargaining power: public infrastructure tenders saw 6.8 bidders on average in 2024, so buyers can quickly price-compare Spanco against rivals and push margins down to industry lows (average EPC margin ~4–6% in 2024). That forces Spanco to drive operational excellence, trim OPEX, and protect profitability under tight budget caps.

High Service Level Agreement Expectations

Enterprise and government clients in 2025 demand >99.95% uptime and sub-15 minute incident response for IT infrastructure; surveys show 68% of large buyers require these SLAs. These customers can impose penalties up to 10% of contract value or liquidated damages, shifting negotiation leverage to clients. The accountability and penalty clauses move power toward buyers across the multi-year contract lifecycle.

Low Switching Costs for Standardized Services

Low switching costs make routine IT maintenance commoditized; global surveys show 62% of SMBs switch providers within 12 months for price or speed, so Spanco risks churn on basic contracts.

System integration is stickier but domestic market depth—over 2,300 registered Indian IT services firms in 2024—lets clients find alternatives, raising price pressure.

Spanco must add value-added services (security, analytics, SLAs) to create stickiness; firms with bundled services report 18% lower churn.

- 62% SMB switch rate within 12 months

- 2,300+ domestic IT firms (2024)

- 18% lower churn with bundled services

Information Symmetry and Market Transparency

Modern procurement teams track market rates and tech trends closely; 2024 surveys show 78% of buyers use benchmarking tools, cutting information gaps that once favored providers.

Customers leverage pricing data and vendor scorecards to demand newer tech at lower costs, pushing average contract discounts to 12–18% in mid‑market IT deals in 2024.

This transparency caps Spanco’s ability to charge premiums for standard IT solutions, forcing differentiation via managed services or niche offerings.

- 78% of buyers use benchmarking tools (2024)

- Average IT contract discounts: 12–18% (2024)

- Premium pricing limited for standard solutions

Buyers dominate: 58% govt revenue, fierce bids, slim EPC margins, high SLAs & churn

Buyers hold strong power: 58% FY2024 revenue from government tenders, average 6.8 bidders (2024), EPC margins 4–6%, buyers demand >99.95% uptime (68% require), penalties up to 10% contract value, 62% SMB switch rate, 2,300+ domestic firms (2024), bundled services cut churn 18%, benchmarking use 78%, average contract discounts 12–18% (2024).

| Metric | Value |

|---|---|

| Govt revenue share (FY2024) | 58% |

| Avg bidders (2024) | 6.8 |

| EPC margins (2024) | 4–6% |

| Uptime SLA demand (2025) | >99.95% (68%) |

| SMB switch rate | 62% |

| Domestic IT firms (2024) | 2,300+ |

| Bundled services churn reduction | 18% |

| Buyer benchmarking (2024) | 78% |

| Avg discounts (2024) | 12–18% |

Preview Before You Purchase

Spanco Porter's Five Forces Analysis

This preview shows the exact Spanco Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy.

No mockups: once you complete payment you’ll get instant access to this identical file, fully prepared for your needs.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Spanco faces moderate buyer power, constrained supplier leverage, and niche-specific barriers to entry that shape its competitive landscape; competitive rivalry centers on service quality and pricing among regional players. Threats from substitutes are limited but evolving with technological logistics solutions, while regulatory and capital-intensity factors influence strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Spanco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Hardware and Software OEMs

Scarcity of Specialized Technical Talent

The Indian IT sector still loses talent in cybersecurity, cloud architecture, and system integration, with attrition in specialist roles at ~22% in 2025 vs 15% company average; demand for high-end skills pushed median cloud architect pay up 18% YoY to ₹3.6M in 2025, giving suppliers of talent leverage.

Spanco must match market benchmarks—total comp packages near ₹4M–₹5M for senior cloud/cyber roles—and offer training, equity, and hybrid work to prevent hires by Tier-1 firms like TCS and Infosys, which hired 40% of campus and lateral senior talent in 2024–25.

Dependence on Third-Party Infrastructure Providers

For large-scale e-governance projects Spanco relies on niche third-party infrastructure partners for local support; in 2025 about 32% of its project costs tied to subcontractors in regional deployments. When a sub-contractor is the sole provider in a region or tech niche, they can push prices or timelines, risking margin erosion on multi-year government contracts. Tight vendor management and dual-sourcing cut supplier leverage and helped Spanco reduce subcontractor cost inflation from 6.4% (2023) to 2.1% in 2024.

Impact of Global Supply Chain Fluctuations

As an integrator, Spanco faces price swings in semiconductors and networking gear—global chip prices rose ~15% in 2021–24 while lead times for key components averaged 22 weeks in 2023, pressuring margins.

Supply shocks through 2025 increased leverage for suppliers who can promise on-time delivery, forcing Spanco to hold strategic inventory buffers or incur SLA penalties and project delay costs.

- Semiconductor price rise ~15% (2021–24)

- Avg component lead time 22 weeks (2023)

- Buffer inventory raises working capital needs

- SLA delay penalties hit margins

Standardization of Technology Platforms

The shift to open-source stacks in 2024 reduced proprietary vendors' leverage, with 38% of government IT tenders favoring open platforms per UK Cabinet Office data, easing licensing costs for Spanco.

Still, certification and authorized-maintenance rules force Spanco to use approved service partners, keeping supplier influence on uptime and upgrade timing at a steady 15–20% impact on operational flexibility.

- 38% government tenders use open-source (2024)

- Authorized support requirement remains

- 15–20% operational flexibility impact

Supplier concentration, rising costs & talent churn squeeze cloud margins

Suppliers hold high leverage: top five OEMs = 68% market share (2025); vendor price moves cut project gross margins 3–6pp; component lead times averaged 22 weeks (2023) and supply shocks raised inventory and SLA costs; talent attrition ~22% (2025) pushed senior cloud pay to ₹3.6M; open-source adoption 38% (2024) eased licensing.

| Metric | Value |

|---|---|

| Top-5 OEM share | 68% (2025) |

| Margin sensitivity | 3–6pp |

| Lead time | 22 weeks (2023) |

| Talent attrition | 22% (2025) |

| Senior cloud pay | ₹3.6M (2025) |

| Open-source tenders | 38% (2024) |

What is included in the product

Concise Porter's Five Forces assessment for Spanco that pinpoints competitive intensity, supplier and buyer power, substitution risks, and barriers to entry, with strategic insights and editable format for reports and presentations.

Spanco Porter's Five Forces delivers a concise one-sheet assessment of competitive pressures—ideal for fast strategic decisions and slide-ready summaries.

Customers Bargaining Power

Domination of Government and Public Sector Clients

A significant share of Spanco’s FY2024 revenue—about 58% per company filings—comes from government contracts and e‑governance projects, concentrating customer power. Centralized procurement bodies like India’s eProcurement platforms enforce strict RFP terms and long payment cycles, shifting risk to vendors. Large contract sizes (single awards often >INR 50 million) let public clients set price and service standards, making them de facto price-makers.

Tender-Based Competitive Bidding Processes

The reliance on transparent, tender-based bidding raises customer bargaining power: public infrastructure tenders saw 6.8 bidders on average in 2024, so buyers can quickly price-compare Spanco against rivals and push margins down to industry lows (average EPC margin ~4–6% in 2024). That forces Spanco to drive operational excellence, trim OPEX, and protect profitability under tight budget caps.

High Service Level Agreement Expectations

Enterprise and government clients in 2025 demand >99.95% uptime and sub-15 minute incident response for IT infrastructure; surveys show 68% of large buyers require these SLAs. These customers can impose penalties up to 10% of contract value or liquidated damages, shifting negotiation leverage to clients. The accountability and penalty clauses move power toward buyers across the multi-year contract lifecycle.

Low Switching Costs for Standardized Services

Low switching costs make routine IT maintenance commoditized; global surveys show 62% of SMBs switch providers within 12 months for price or speed, so Spanco risks churn on basic contracts.

System integration is stickier but domestic market depth—over 2,300 registered Indian IT services firms in 2024—lets clients find alternatives, raising price pressure.

Spanco must add value-added services (security, analytics, SLAs) to create stickiness; firms with bundled services report 18% lower churn.

- 62% SMB switch rate within 12 months

- 2,300+ domestic IT firms (2024)

- 18% lower churn with bundled services

Information Symmetry and Market Transparency

Modern procurement teams track market rates and tech trends closely; 2024 surveys show 78% of buyers use benchmarking tools, cutting information gaps that once favored providers.

Customers leverage pricing data and vendor scorecards to demand newer tech at lower costs, pushing average contract discounts to 12–18% in mid‑market IT deals in 2024.

This transparency caps Spanco’s ability to charge premiums for standard IT solutions, forcing differentiation via managed services or niche offerings.

- 78% of buyers use benchmarking tools (2024)

- Average IT contract discounts: 12–18% (2024)

- Premium pricing limited for standard solutions

Buyers dominate: 58% govt revenue, fierce bids, slim EPC margins, high SLAs & churn

Buyers hold strong power: 58% FY2024 revenue from government tenders, average 6.8 bidders (2024), EPC margins 4–6%, buyers demand >99.95% uptime (68% require), penalties up to 10% contract value, 62% SMB switch rate, 2,300+ domestic firms (2024), bundled services cut churn 18%, benchmarking use 78%, average contract discounts 12–18% (2024).

| Metric | Value |

|---|---|

| Govt revenue share (FY2024) | 58% |

| Avg bidders (2024) | 6.8 |

| EPC margins (2024) | 4–6% |

| Uptime SLA demand (2025) | >99.95% (68%) |

| SMB switch rate | 62% |

| Domestic IT firms (2024) | 2,300+ |

| Bundled services churn reduction | 18% |

| Buyer benchmarking (2024) | 78% |

| Avg discounts (2024) | 12–18% |

Preview Before You Purchase

Spanco Porter's Five Forces Analysis

This preview shows the exact Spanco Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy.

No mockups: once you complete payment you’ll get instant access to this identical file, fully prepared for your needs.