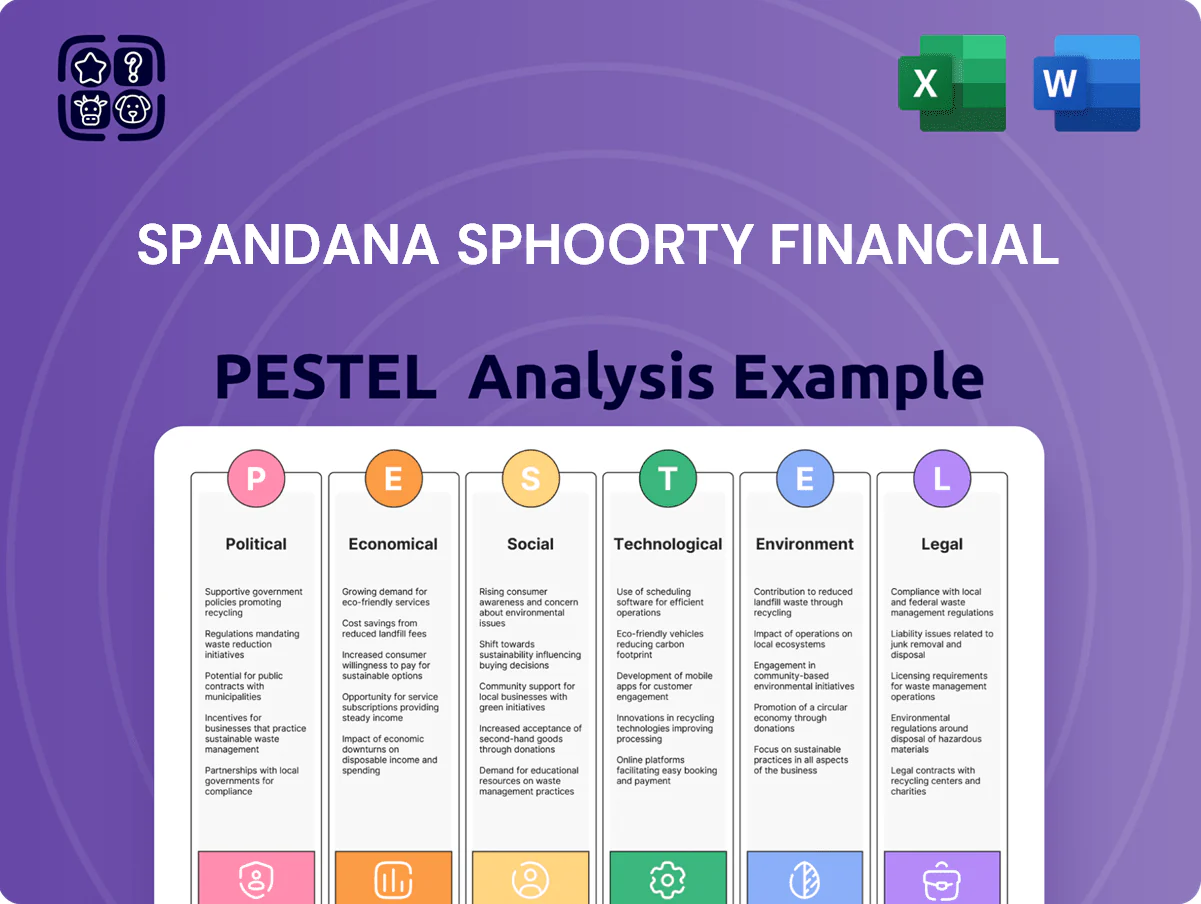

Spandana Sphoorty Financial PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Navigate the external forces shaping Spandana Sphoorty Financial with our concise PESTLE snapshot—identify regulatory, economic, and technological risks and opportunities fast; purchase the full analysis to unlock detailed, actionable insights and ready-to-use charts for investment or strategy decisions.

Political factors

Government focus on financial inclusion

The Indian government’s continued push for financial inclusion—PMJDY reaching over 480 million accounts by 2024—creates a policy tailwind for Spandana Sphoorty Financial to expand microcredit in under-penetrated rural areas; this supportive environment, coupled with government poverty-alleviation missions (e.g., 2024 rural employment and livelihoods programs), increases reliance on MFIs’ distribution networks to deliver credit, boosting addressable market and portfolio growth potential.

Geopolitical stability and rural policy

Political stability at federal and state levels affects Spandana Sphoorty Financial's microfinance operations across 18 states; state election cycles in 2024–25 saw five major agrarian-focused governments introduce or promise loan relief, raising regional operational risk. Changes in state leadership can shift rural development spending—India’s rural credit growth slowed to 6.2% YoY in FY2024 in some states—altering demand for MFI loans. Populist measures like farm loan waivers can weaken credit discipline; areas with recent waivers recorded up to a 7–10 percentage-point rise in NPA incidence among small borrowers, affecting Spandana’s core portfolio performance.

Regulatory oversight by the RBI

The Reserve Bank of India is the primary regulator for NBFC-MFIs, and recent 2024 guidance revising interest rate caps to 24% and tightening qualifying assets to 50% high‑priority microloans affects Spandana Sphoorty; household income thresholds (now ₹1.25 lakh rural/₹2.5 lakh urban) are periodically reviewed, and Spandana must adapt underwriting, pricing, and portfolio mix to remain compliant while protecting margins—net interest margin was 11.2% in FY2024.

Direct Benefit Transfer (DBT) integration

Government DBT rollout has raised financial literacy and digital footprints among rural women; as of 2024 over 280 million DBT beneficiaries receive payments via Aadhaar-linked accounts, expanding Spandana Sphoorty Financial’s target base.

DBT integration streamlines loan disbursement and collections by using Aadhaar-linked transfers, lowering transaction costs and reducing defaults tied to cash handling.

Greater digital payments reduce cash dependence and boost transaction transparency—India’s digital payments volume reached 111 billion in FY2024, supporting scalable microfinance operations.

- ~280M DBT beneficiaries (2024)

- 111B digital payments FY2024

- Lower cash handling costs and higher collection transparency

State-level microfinance legislation

Individual state governments in India have enacted local MFI rules; Maharashtra and Andhra Pradesh recently reviewed recovery guidelines after high-profile incidents; Andhra’s interventions in 2024 affected ~8% of regional MFI collections.

RBI remains the central regulator, but state political pressure on aggressive recovery practices creates localized operational risk and occasional moratoria or enhanced oversight.

Spandana engages proactively with state authorities and reports a 2024 compliance-related expense increase of ~0.4% of AUM to mitigate regional political interference.

- State-level rules can alter collections and operations (e.g., Andhra 2024 impact ~8% of collections)

- Central RBI authority limits but does not eliminate local enforcement risk

- Spandana’s active state engagement and 0.4% AUM compliance cost rise in 2024 reduce regulatory disruption

Spandana: Policy tailwinds expand market but RBI caps, state actions compress margins

Political support for financial inclusion (PMJDY >480M accounts, 2024) and DBT scale (~280M beneficiaries) expands Spandana’s market, while RBI rules (24% interest cap, 50% qualifying assets) and state interventions (Andhra 2024 impact ~8% collections) raise compliance and pricing pressures; Spandana reported NIM 11.2% and compliance costs +0.4% AUM in 2024.

| Metric | 2024 |

|---|---|

| PMJDY accounts | 480M+ |

| DBT beneficiaries | ~280M |

| Digital payments | 111B |

| Interest cap | 24% |

| NIM (Spandana) | 11.2% |

| State impact (Andhra) | ~8% collections |

| Compliance cost rise | +0.4% AUM |

What is included in the product

Explores how external macro-environmental factors uniquely affect Spandana Sphoorty Financial across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify risks and opportunities for executives, investors, and strategists.

Compact PESTLE insight tailored to Spandana Sphoorty that distills external risks and opportunities into a shareable, presentation-ready format—ideal for quick alignment in meetings and supporting strategic decision-making across teams.

Economic factors

Interest rate environment and cost of funds

Fluctuations in the RBI repo rate—raised from 6.5% in May 2022 to 6.5–6.75% through 2023–24 and held around 6.5% in 2024–25—directly affect Spandana Sphoorty’s borrowing costs, increasing cost of funds for NBFCs. As a mid-sized NBFC with reported FY24 borrowings of ~INR 15,000 crore, its NIM depends on securing low-cost bank and market debt; higher policy rates compressed industry NIMs by ~40–60 bps in 2023–24. Economic cycles that push rates higher risk further margin compression if increased costs cannot be passed fully to microloan borrowers.

Rural GDP growth and agricultural performance

Rural GDP growth and monsoon-linked agriculture drive Spandana Sphoorty Financial’s client incomes; India’s rural GDP rose about 3.5% in FY2024 while kharif foodgrains production hit a record 153.4 million tonnes in 2023–24, supporting loan uptake for livelihoods and microenterprises.

Weak monsoons or a 2024 contraction in farm incomes could raise localized credit stress; MFI GNPA ratios climbed to ~4.2% in FY2024 in drought-affected states, signaling vulnerability to primary-sector shocks.

Inflationary pressures on low-income households

High inflation—India's CPI at 6.4% in 2024 with food inflation near 8% and petrol/diesel up ~12% YoY—hits Spandana Sphoorty's low-income clients hardest, as higher food and fuel costs eat into already thin household margins.

Rising living costs reduce repayment capacity for microentrepreneurs; Spandana's 2024 GNPA sensitivity could rise if marginal borrowers face 10–15% income shocks.

The firm must closely track CPI, rural inflation and fuel prices and recalibrate credit scoring, provisioning and tenor policies in near-real time.

Capital market liquidity and funding access

Spandana Sphoorty’s growth hinges on access to equity and debt from domestic and international investors; in FY2024 it reported consolidated AUM of ~INR 20,500 crore, underscoring capital needs for portfolio expansion.

Economic stability and improving sentiment toward Indian microfinance—industry GNPA for MFIs at ~0.9% in 2024—support steady liquidity inflows.

However, market volatility can depress valuations and delay fundraising; Spandana’s ability to complete rounds depends on interest-rate environment and investor risk appetite.

- FY2024 AUM ~INR 20,500 crore

- Industry MFI GNPA ~0.9% (2024)

- Funding sensitivity to rates and volatility

Employment trends in the informal sector

- Informal sector dominance: ~81% of non-agri workers (2023)

- Microloan demand: +12% YoY disbursements FY2024

- Formalization impact: improved KYC/GST data strengthens credit scoring, lowering default risk

Rising RBI rates squeeze NBFC margins as rural demand and inflation test asset quality

Rising RBI rates (~6.5% in 2024–25) raised NBFC funding costs, compressing NIMs by ~40–60 bps in 2023–24; FY24 AUM ~INR 20,500 crore and borrowings ~INR 15,000 crore heighten rate sensitivity. Rural GDP ~3.5% (FY2024) and record kharif output (153.4 mt) supported demand, but CPI 6.4%/food ~8% and informal-sector exposure (81% non-agri workers) elevate repayment risk.

| Metric | Value |

|---|---|

| AUM FY24 | INR 20,500 cr |

| Borrowings FY24 | ~INR 15,000 cr |

| RBI rate | ~6.5% |

| CPI 2024 | 6.4% |

What You See Is What You Get

Spandana Sphoorty Financial PESTLE Analysis

The preview shown here is the exact Spandana Sphoorty Financial PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Navigate the external forces shaping Spandana Sphoorty Financial with our concise PESTLE snapshot—identify regulatory, economic, and technological risks and opportunities fast; purchase the full analysis to unlock detailed, actionable insights and ready-to-use charts for investment or strategy decisions.

Political factors

Government focus on financial inclusion

The Indian government’s continued push for financial inclusion—PMJDY reaching over 480 million accounts by 2024—creates a policy tailwind for Spandana Sphoorty Financial to expand microcredit in under-penetrated rural areas; this supportive environment, coupled with government poverty-alleviation missions (e.g., 2024 rural employment and livelihoods programs), increases reliance on MFIs’ distribution networks to deliver credit, boosting addressable market and portfolio growth potential.

Geopolitical stability and rural policy

Political stability at federal and state levels affects Spandana Sphoorty Financial's microfinance operations across 18 states; state election cycles in 2024–25 saw five major agrarian-focused governments introduce or promise loan relief, raising regional operational risk. Changes in state leadership can shift rural development spending—India’s rural credit growth slowed to 6.2% YoY in FY2024 in some states—altering demand for MFI loans. Populist measures like farm loan waivers can weaken credit discipline; areas with recent waivers recorded up to a 7–10 percentage-point rise in NPA incidence among small borrowers, affecting Spandana’s core portfolio performance.

Regulatory oversight by the RBI

The Reserve Bank of India is the primary regulator for NBFC-MFIs, and recent 2024 guidance revising interest rate caps to 24% and tightening qualifying assets to 50% high‑priority microloans affects Spandana Sphoorty; household income thresholds (now ₹1.25 lakh rural/₹2.5 lakh urban) are periodically reviewed, and Spandana must adapt underwriting, pricing, and portfolio mix to remain compliant while protecting margins—net interest margin was 11.2% in FY2024.

Direct Benefit Transfer (DBT) integration

Government DBT rollout has raised financial literacy and digital footprints among rural women; as of 2024 over 280 million DBT beneficiaries receive payments via Aadhaar-linked accounts, expanding Spandana Sphoorty Financial’s target base.

DBT integration streamlines loan disbursement and collections by using Aadhaar-linked transfers, lowering transaction costs and reducing defaults tied to cash handling.

Greater digital payments reduce cash dependence and boost transaction transparency—India’s digital payments volume reached 111 billion in FY2024, supporting scalable microfinance operations.

- ~280M DBT beneficiaries (2024)

- 111B digital payments FY2024

- Lower cash handling costs and higher collection transparency

State-level microfinance legislation

Individual state governments in India have enacted local MFI rules; Maharashtra and Andhra Pradesh recently reviewed recovery guidelines after high-profile incidents; Andhra’s interventions in 2024 affected ~8% of regional MFI collections.

RBI remains the central regulator, but state political pressure on aggressive recovery practices creates localized operational risk and occasional moratoria or enhanced oversight.

Spandana engages proactively with state authorities and reports a 2024 compliance-related expense increase of ~0.4% of AUM to mitigate regional political interference.

- State-level rules can alter collections and operations (e.g., Andhra 2024 impact ~8% of collections)

- Central RBI authority limits but does not eliminate local enforcement risk

- Spandana’s active state engagement and 0.4% AUM compliance cost rise in 2024 reduce regulatory disruption

Spandana: Policy tailwinds expand market but RBI caps, state actions compress margins

Political support for financial inclusion (PMJDY >480M accounts, 2024) and DBT scale (~280M beneficiaries) expands Spandana’s market, while RBI rules (24% interest cap, 50% qualifying assets) and state interventions (Andhra 2024 impact ~8% collections) raise compliance and pricing pressures; Spandana reported NIM 11.2% and compliance costs +0.4% AUM in 2024.

| Metric | 2024 |

|---|---|

| PMJDY accounts | 480M+ |

| DBT beneficiaries | ~280M |

| Digital payments | 111B |

| Interest cap | 24% |

| NIM (Spandana) | 11.2% |

| State impact (Andhra) | ~8% collections |

| Compliance cost rise | +0.4% AUM |

What is included in the product

Explores how external macro-environmental factors uniquely affect Spandana Sphoorty Financial across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify risks and opportunities for executives, investors, and strategists.

Compact PESTLE insight tailored to Spandana Sphoorty that distills external risks and opportunities into a shareable, presentation-ready format—ideal for quick alignment in meetings and supporting strategic decision-making across teams.

Economic factors

Interest rate environment and cost of funds

Fluctuations in the RBI repo rate—raised from 6.5% in May 2022 to 6.5–6.75% through 2023–24 and held around 6.5% in 2024–25—directly affect Spandana Sphoorty’s borrowing costs, increasing cost of funds for NBFCs. As a mid-sized NBFC with reported FY24 borrowings of ~INR 15,000 crore, its NIM depends on securing low-cost bank and market debt; higher policy rates compressed industry NIMs by ~40–60 bps in 2023–24. Economic cycles that push rates higher risk further margin compression if increased costs cannot be passed fully to microloan borrowers.

Rural GDP growth and agricultural performance

Rural GDP growth and monsoon-linked agriculture drive Spandana Sphoorty Financial’s client incomes; India’s rural GDP rose about 3.5% in FY2024 while kharif foodgrains production hit a record 153.4 million tonnes in 2023–24, supporting loan uptake for livelihoods and microenterprises.

Weak monsoons or a 2024 contraction in farm incomes could raise localized credit stress; MFI GNPA ratios climbed to ~4.2% in FY2024 in drought-affected states, signaling vulnerability to primary-sector shocks.

Inflationary pressures on low-income households

High inflation—India's CPI at 6.4% in 2024 with food inflation near 8% and petrol/diesel up ~12% YoY—hits Spandana Sphoorty's low-income clients hardest, as higher food and fuel costs eat into already thin household margins.

Rising living costs reduce repayment capacity for microentrepreneurs; Spandana's 2024 GNPA sensitivity could rise if marginal borrowers face 10–15% income shocks.

The firm must closely track CPI, rural inflation and fuel prices and recalibrate credit scoring, provisioning and tenor policies in near-real time.

Capital market liquidity and funding access

Spandana Sphoorty’s growth hinges on access to equity and debt from domestic and international investors; in FY2024 it reported consolidated AUM of ~INR 20,500 crore, underscoring capital needs for portfolio expansion.

Economic stability and improving sentiment toward Indian microfinance—industry GNPA for MFIs at ~0.9% in 2024—support steady liquidity inflows.

However, market volatility can depress valuations and delay fundraising; Spandana’s ability to complete rounds depends on interest-rate environment and investor risk appetite.

- FY2024 AUM ~INR 20,500 crore

- Industry MFI GNPA ~0.9% (2024)

- Funding sensitivity to rates and volatility

Employment trends in the informal sector

- Informal sector dominance: ~81% of non-agri workers (2023)

- Microloan demand: +12% YoY disbursements FY2024

- Formalization impact: improved KYC/GST data strengthens credit scoring, lowering default risk

Rising RBI rates squeeze NBFC margins as rural demand and inflation test asset quality

Rising RBI rates (~6.5% in 2024–25) raised NBFC funding costs, compressing NIMs by ~40–60 bps in 2023–24; FY24 AUM ~INR 20,500 crore and borrowings ~INR 15,000 crore heighten rate sensitivity. Rural GDP ~3.5% (FY2024) and record kharif output (153.4 mt) supported demand, but CPI 6.4%/food ~8% and informal-sector exposure (81% non-agri workers) elevate repayment risk.

| Metric | Value |

|---|---|

| AUM FY24 | INR 20,500 cr |

| Borrowings FY24 | ~INR 15,000 cr |

| RBI rate | ~6.5% |

| CPI 2024 | 6.4% |

What You See Is What You Get

Spandana Sphoorty Financial PESTLE Analysis

The preview shown here is the exact Spandana Sphoorty Financial PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.