Shanghai Pudong Development Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Shanghai Pudong Development faces intense competitive pressures from established port operators, rising substitute logistics channels, and concentrated buyer negotiation—while regulatory shifts and capital-intensive barriers temper new entrants; this snapshot highlights strategic vulnerabilities and growth levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shanghai Pudong Development’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Central Bank and Regulatory Liquidity Control

The People’s Bank of China (PBOC) is SPD Bank’s main liquidity supplier, steering cost of capital via the medium-term lending facility (MLF) and reserve requirement ratio (RRR); the MLF rate stood at 2.75% and RRR averaging 8.5% in Q4 2025. The PBOC’s moves directly change SPD Bank’s funding costs and net interest margin, so the bank must align loan and deposit pricing to those benchmarks. That leaves SPD Bank little room to negotiate the fundamental cost of its primary input—liquidity—since regulatory tools, not market suppliers, set rates. As a result, liquidity supply is a strong supplier-side force in the bank’s Five Forces profile.

Retail and Institutional Depositors

Individual and corporate depositors supply SPD Bank's core funding but are fragmented, so individual bargaining power is low; retail deposits made up about 58% of total deposits in 2024, forcing competitive retail rates as savers shift into wealth management.

Institutional depositors hold greater sway—large corporate and government deposits (roughly 22% of deposits in 2024) negotiate bespoke rates and services, pressuring SPD to tailor pricing and liquidity terms.

Technology and Digital Infrastructure Providers

As SPD Bank accelerates digital transformation, reliance on cloud, AI, and cybersecurity vendors raises supplier power to moderate: core banking switch costs exceed $100m and integration can take 18–36 months, per industry benchmarks in 2024. The bank reduces risk by adding 7+ regional vendors and spending RMB 2.1bn on proprietary fintech R&D in 2024, lowering dependence on global tech giants.

Interbank Market Participants

The interbank market is a key short-term funding source for SPD Bank to manage daily liquidity and meet regulatory LCR/NSFR ratios; in 2025 China’s interbank repo outstanding averaged about CNY 30 trillion daily, so access matters.

Lenders gain bargaining power during tight liquidity or volatility spikes—e.g., the 2024 repo rate VIX-equivalent rose 60%—so SPD Bank must keep high credit standing and strong ties with big banks and policy banks to secure favorable rates.

- Interbank repo avg ~CNY 30 trillion/day (2025)

- Repo-rate volatility indicator +60% prior spike

- High credit rating reduces funding spread

- Strong correspondent ties cut access risk

Specialized Financial Talent

The supply of senior talent in risk, quants, and digital banking is a critical input for SPD Bank's performance; in 2024 China had a 28% shortfall in fintech-skilled roles, raising supplier leverage.

By 2025, expertise in green finance and AI wealth management remains scarce, giving specialists high bargaining power and driving moves to fintechs and foreign banks.

SPD Bank must offer premium pay, equity-like incentives, and structured career paths—market data shows top quant hires command 30–50% salary premiums—to retain staff.

- 28% fintech skills gap (2024)

- Top quant pay premium 30–50%

- Retention needs: pay, equity, career paths

China banking: tight funding, volatile repos and rising supplier leverage

Suppliers wield strong power: PBOC liquidity (MLF 2.75%, RRR ~8.5% in Q4 2025) sets base funding cost; interbank repo ≈ CNY30tn/day (2025) and repo-rate volatility spiked ~+60% amplify lender leverage. Retail deposits 58% (2024) are fragmented; institutional deposits 22% (2024) and scarce fintech/quant talent (28% skills gap, top quant pay +30–50%) raise bargaining pressure.

| Item | Key figure |

|---|---|

| MLF rate (Q4 2025) | 2.75% |

| RRR (avg Q4 2025) | ≈8.5% |

| Interbank repo (2025) | CNY30tn/day |

| Retail deposits (2024) | 58% |

| Institutional deposits (2024) | 22% |

| Fintech skills gap (2024) | 28% |

What is included in the product

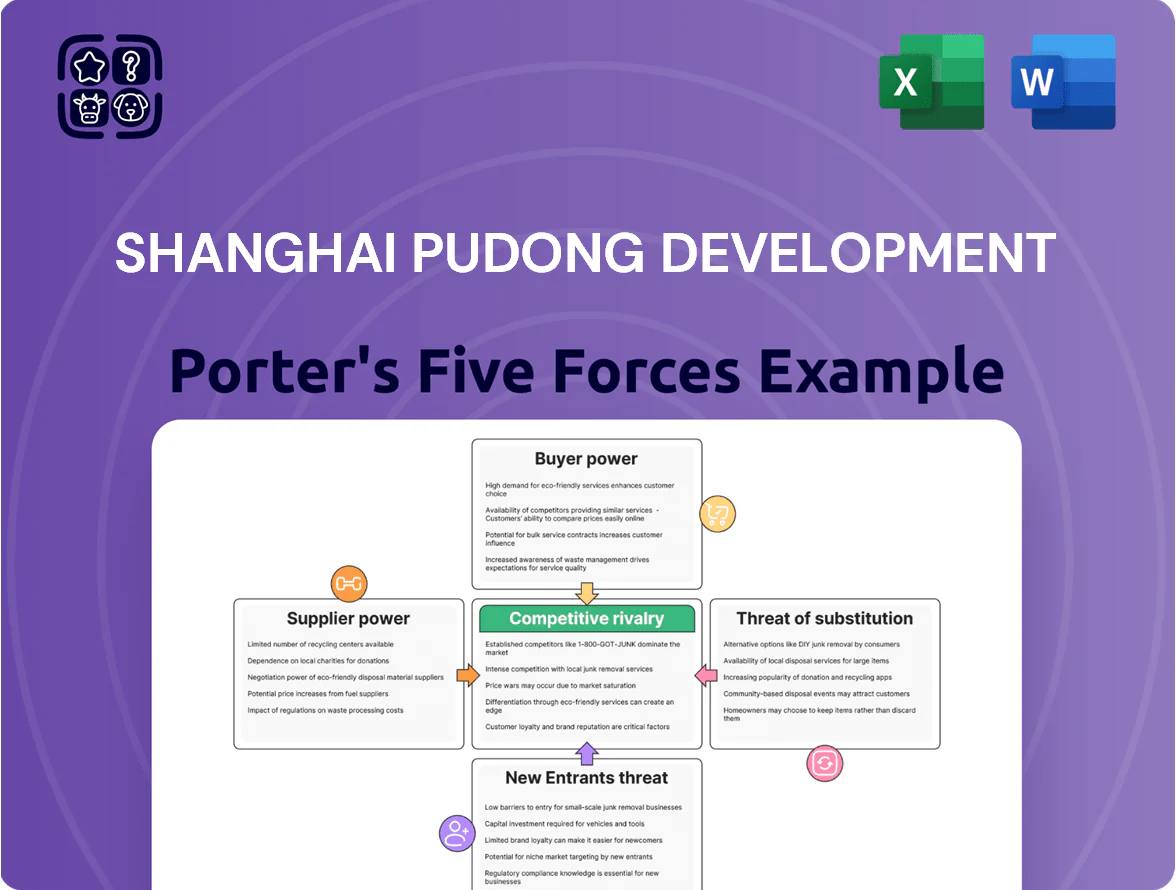

Tailored exclusively for Shanghai Pudong Development, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its port and logistics competitiveness.

Concise Porter’s Five Forces summary for Shanghai Pudong—clearly highlights competitive pressures and regulatory risks to speed strategic decisions.

Customers Bargaining Power

Large Corporate and State-Owned Enterprises

Major corporate and state-owned clients wield strong bargaining power due to huge borrowing and transaction volumes—SPD Bank lost 2024 large-account share pressure as top 50 clients accounted for ~28% of corporate loan balances, enabling discounts on interest and bespoke fee waivers.

Retail Banking and Consumer Credit Users

Retail customers’ bargaining power rose as mobile apps made interest rates and fees transparent; 2024 PBOC data shows 72% of Chinese adults compare bank rates via apps. Low switching costs let users move deposits or credit balances for small APR improvements (0.5–1.0pp). SPD Bank counters with ecosystem ties—cross-sell in wealth, payments, and e-commerce—and personalized digital offers; its 2024 retention rose to 84% in priority segments.

Small and Medium-Sized Enterprises

SMEs wield moderate bargaining power: regulators in China mandated banks raise inclusive finance lending to 30% of new SME credit by 2024, so even tiny firms gain better terms.

Individual SMEs lack leverage, but collective regulatory priority forces SPD Bank to simplify applications and cut rates by ~50–150 bps versus commercial loans in 2025.

SPD Bank uses big-data risk models—reducing NPLs by 0.6 percentage points in 2024—to price SME risk while meeting competitive 2025 lending pressures.

High Net Worth Wealth Management Clients

- HNW share: >70% of investable assets (2024)

- Key demand: personalized service, superior asset allocation, competitive returns

- Critical metric: >200 bps underperformance triggers asset migration

- Threat: global PE access and digital platforms lower switching costs

Digital Savvy Borrowers and Fintech Users

- 62% of borrowers prefer app-based lending (2024)

- Sub-24-hour approvals drive choice

- SPD Bank tech spend +15% in 2023–24

- Risk: customer migration to agile fintechs

Customers Dictate Terms: Concentrated Loans, Price-Shopping & Digital Preference

Customers hold strong bargaining power: top 50 corporates = ~28% corporate loans (2024), retail price-shopping = 72% compare rates (PBOC 2024), fintech borrowers 62% prefer app lending (2024), HNW hold >70% investable assets (MSCI/Capgemini 2024). SPD Bank cut SME rates 50–150bps (2025), retention 84% in priority segments (2024), tech spend +15% (2023–24).

| Metric | Value |

|---|---|

| Top-50 loan share | ~28% (2024) |

| Retail rate comparison | 72% (2024) |

| Fintech pref | 62% (2024) |

| HNW assets | >70% (2024) |

Preview the Actual Deliverable

Shanghai Pudong Development Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Shanghai Pudong you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use. The document covers supplier and buyer power, competitive rivalry, threat of new entrants and substitutes, and strategic implications tailored to Pudong’s port operations. Once you buy, you’ll get instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Shanghai Pudong Development faces intense competitive pressures from established port operators, rising substitute logistics channels, and concentrated buyer negotiation—while regulatory shifts and capital-intensive barriers temper new entrants; this snapshot highlights strategic vulnerabilities and growth levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Shanghai Pudong Development’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Central Bank and Regulatory Liquidity Control

The People’s Bank of China (PBOC) is SPD Bank’s main liquidity supplier, steering cost of capital via the medium-term lending facility (MLF) and reserve requirement ratio (RRR); the MLF rate stood at 2.75% and RRR averaging 8.5% in Q4 2025. The PBOC’s moves directly change SPD Bank’s funding costs and net interest margin, so the bank must align loan and deposit pricing to those benchmarks. That leaves SPD Bank little room to negotiate the fundamental cost of its primary input—liquidity—since regulatory tools, not market suppliers, set rates. As a result, liquidity supply is a strong supplier-side force in the bank’s Five Forces profile.

Retail and Institutional Depositors

Individual and corporate depositors supply SPD Bank's core funding but are fragmented, so individual bargaining power is low; retail deposits made up about 58% of total deposits in 2024, forcing competitive retail rates as savers shift into wealth management.

Institutional depositors hold greater sway—large corporate and government deposits (roughly 22% of deposits in 2024) negotiate bespoke rates and services, pressuring SPD to tailor pricing and liquidity terms.

Technology and Digital Infrastructure Providers

As SPD Bank accelerates digital transformation, reliance on cloud, AI, and cybersecurity vendors raises supplier power to moderate: core banking switch costs exceed $100m and integration can take 18–36 months, per industry benchmarks in 2024. The bank reduces risk by adding 7+ regional vendors and spending RMB 2.1bn on proprietary fintech R&D in 2024, lowering dependence on global tech giants.

Interbank Market Participants

The interbank market is a key short-term funding source for SPD Bank to manage daily liquidity and meet regulatory LCR/NSFR ratios; in 2025 China’s interbank repo outstanding averaged about CNY 30 trillion daily, so access matters.

Lenders gain bargaining power during tight liquidity or volatility spikes—e.g., the 2024 repo rate VIX-equivalent rose 60%—so SPD Bank must keep high credit standing and strong ties with big banks and policy banks to secure favorable rates.

- Interbank repo avg ~CNY 30 trillion/day (2025)

- Repo-rate volatility indicator +60% prior spike

- High credit rating reduces funding spread

- Strong correspondent ties cut access risk

Specialized Financial Talent

The supply of senior talent in risk, quants, and digital banking is a critical input for SPD Bank's performance; in 2024 China had a 28% shortfall in fintech-skilled roles, raising supplier leverage.

By 2025, expertise in green finance and AI wealth management remains scarce, giving specialists high bargaining power and driving moves to fintechs and foreign banks.

SPD Bank must offer premium pay, equity-like incentives, and structured career paths—market data shows top quant hires command 30–50% salary premiums—to retain staff.

- 28% fintech skills gap (2024)

- Top quant pay premium 30–50%

- Retention needs: pay, equity, career paths

China banking: tight funding, volatile repos and rising supplier leverage

Suppliers wield strong power: PBOC liquidity (MLF 2.75%, RRR ~8.5% in Q4 2025) sets base funding cost; interbank repo ≈ CNY30tn/day (2025) and repo-rate volatility spiked ~+60% amplify lender leverage. Retail deposits 58% (2024) are fragmented; institutional deposits 22% (2024) and scarce fintech/quant talent (28% skills gap, top quant pay +30–50%) raise bargaining pressure.

| Item | Key figure |

|---|---|

| MLF rate (Q4 2025) | 2.75% |

| RRR (avg Q4 2025) | ≈8.5% |

| Interbank repo (2025) | CNY30tn/day |

| Retail deposits (2024) | 58% |

| Institutional deposits (2024) | 22% |

| Fintech skills gap (2024) | 28% |

What is included in the product

Tailored exclusively for Shanghai Pudong Development, this Porter’s Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats shaping its port and logistics competitiveness.

Concise Porter’s Five Forces summary for Shanghai Pudong—clearly highlights competitive pressures and regulatory risks to speed strategic decisions.

Customers Bargaining Power

Large Corporate and State-Owned Enterprises

Major corporate and state-owned clients wield strong bargaining power due to huge borrowing and transaction volumes—SPD Bank lost 2024 large-account share pressure as top 50 clients accounted for ~28% of corporate loan balances, enabling discounts on interest and bespoke fee waivers.

Retail Banking and Consumer Credit Users

Retail customers’ bargaining power rose as mobile apps made interest rates and fees transparent; 2024 PBOC data shows 72% of Chinese adults compare bank rates via apps. Low switching costs let users move deposits or credit balances for small APR improvements (0.5–1.0pp). SPD Bank counters with ecosystem ties—cross-sell in wealth, payments, and e-commerce—and personalized digital offers; its 2024 retention rose to 84% in priority segments.

Small and Medium-Sized Enterprises

SMEs wield moderate bargaining power: regulators in China mandated banks raise inclusive finance lending to 30% of new SME credit by 2024, so even tiny firms gain better terms.

Individual SMEs lack leverage, but collective regulatory priority forces SPD Bank to simplify applications and cut rates by ~50–150 bps versus commercial loans in 2025.

SPD Bank uses big-data risk models—reducing NPLs by 0.6 percentage points in 2024—to price SME risk while meeting competitive 2025 lending pressures.

High Net Worth Wealth Management Clients

- HNW share: >70% of investable assets (2024)

- Key demand: personalized service, superior asset allocation, competitive returns

- Critical metric: >200 bps underperformance triggers asset migration

- Threat: global PE access and digital platforms lower switching costs

Digital Savvy Borrowers and Fintech Users

- 62% of borrowers prefer app-based lending (2024)

- Sub-24-hour approvals drive choice

- SPD Bank tech spend +15% in 2023–24

- Risk: customer migration to agile fintechs

Customers Dictate Terms: Concentrated Loans, Price-Shopping & Digital Preference

Customers hold strong bargaining power: top 50 corporates = ~28% corporate loans (2024), retail price-shopping = 72% compare rates (PBOC 2024), fintech borrowers 62% prefer app lending (2024), HNW hold >70% investable assets (MSCI/Capgemini 2024). SPD Bank cut SME rates 50–150bps (2025), retention 84% in priority segments (2024), tech spend +15% (2023–24).

| Metric | Value |

|---|---|

| Top-50 loan share | ~28% (2024) |

| Retail rate comparison | 72% (2024) |

| Fintech pref | 62% (2024) |

| HNW assets | >70% (2024) |

Preview the Actual Deliverable

Shanghai Pudong Development Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Shanghai Pudong you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use. The document covers supplier and buyer power, competitive rivalry, threat of new entrants and substitutes, and strategic implications tailored to Pudong’s port operations. Once you buy, you’ll get instant access to this same file.