SPH SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

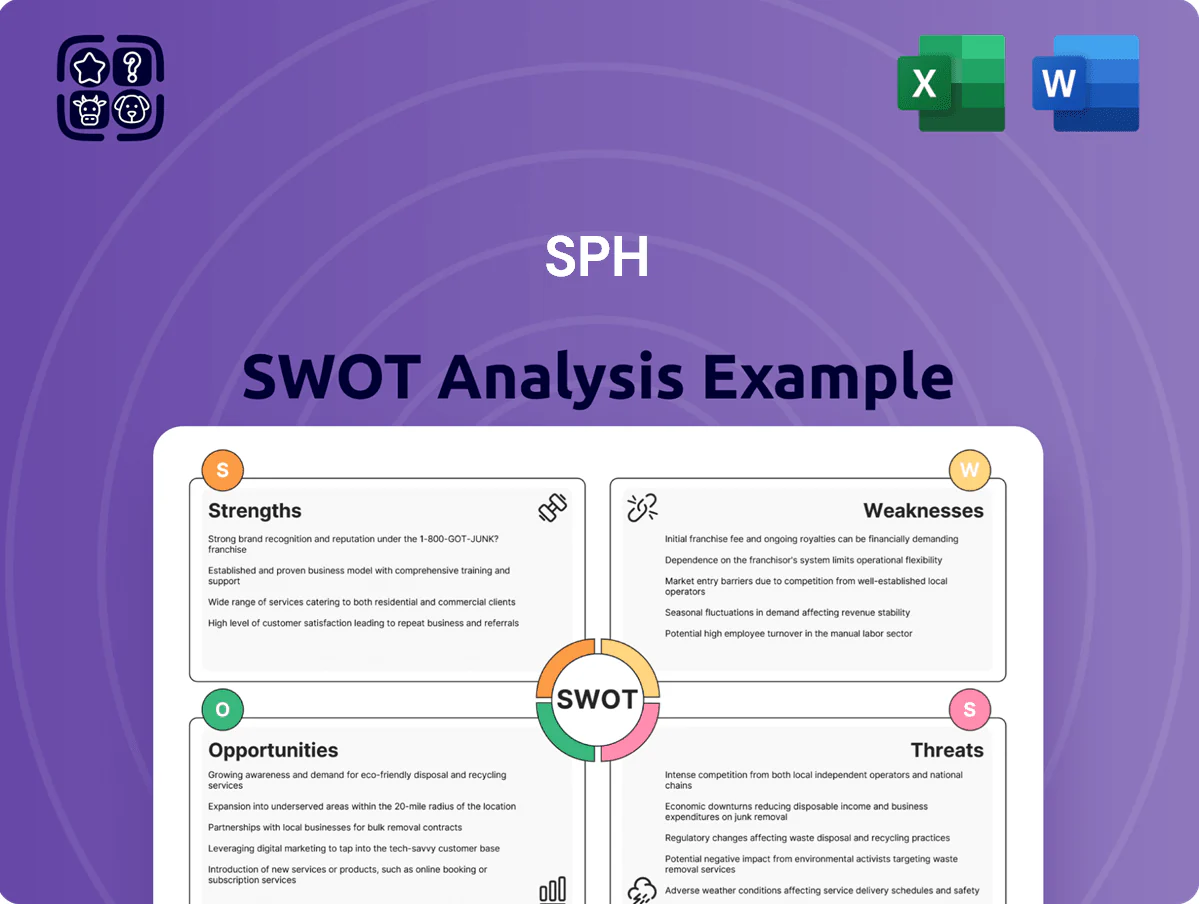

SPH’s resilient brand portfolio and digital push position it well against regional peers, yet legacy print exposure and revenue cyclicality pose material risks to short-term margins and valuation upside.

Strengths

Dominant Market Position in Singapore Media

As of late 2025, SPH Media remains Singapore’s primary news source with over 60% weekly reach across print, digital and radio, securing roughly S$220m in advertising revenue for FY2024–25; this legacy brand equity produces a loyal audience hard for new entrants to match. SPH leverages that dominance to win high-value national advertisers and sustain strong social influence on public discourse.

Significant Government Financial Support

The 2024 restructuring into a not-for-profit let SPH Media secure up to S$900 million (≈US$660M) in government funding across five years, giving a rare cash buffer for legacy-to-digital shifts.

That funding removes quarterly profit pressure, so SPH can pace investments in paywalls, data platforms, and AI-driven personalization aimed at restoring digital ad and subscription growth.

High Quality Core Real Estate Assets

The legacy portfolio includes Paragon (Orchard Road) and The Woodleigh Mall (Bidadari), which posted rental reversion of +8% and +6% respectively in FY2024 and maintained >95% occupancy, underpinning resilient cash flows during 2023–24 volatility.

Strategic Diversification into Student Accommodation

- UK/Australia PBSA: occupancy >95%

- Valuation gains ~£120m (30% since 2020)

- Counter-cyclical revenue stream, stable yields

- Pivots away from traditional media to real estate

Advanced Digital Infrastructure and AI Integration

- Production time −40%

- Session duration +22%

- Paid users 320,000 (+18% YoY)

- Ad revenue +12% FY2024

- Users 18–34 = 48%

SPH: 60% reach, S$900M funding, digital & real estate surging—paid users +18%

SPH’s strengths: dominant national reach (60% weekly), S$900m five-year funding secured in 2024, diversified high-occupancy real estate (Paragon/Woodleigh >95% occupancy; PBSA valuation +£120m since 2020, occupancy >95%), digital progress (320,000 paid users +18% YoY; ad rev +12%; production time −40%; mobile session +22%).

| Metric | Value |

|---|---|

| Weekly reach | 60% |

| Government funding (5y) | S$900m |

| Paid users | 320,000 (+18% YoY) |

| Ad revenue FY2024 | +12% |

| PBSA valuation gain | +£120m (since 2020) |

| Occupancy (retail/PBSA) | >95% |

| Production time | −40% |

| Mobile session duration | +22% |

What is included in the product

Provides a concise SWOT overview of SPH, outlining its core strengths and weaknesses alongside market opportunities and external threats to inform strategic decisions.

Provides a concise SWOT matrix tailored to SPH for rapid strategy alignment and quick integration into reports, slides, and stakeholder reviews.

Weaknesses

Structural Decline in Print Revenue

Despite digital growth, SPH (Singapore Press Holdings) faces a secular decline in print circulation and advertising, which historically delivered higher margins; print revenue fell about 18% y/y in 2024, keeping EBITDA under pressure.

The shift to digital-first hasn’t matched print dollar-for-dollar: digital ad revenue grew ~12% in 2024 but remained roughly 40% below legacy print revenue levels, widening the revenue gap.

This ongoing erosion of a core legacy stream continues to drag overall financial performance, contributing to a 7% decline in total group revenue in FY2024 and compressing operating margins.

Heavy Reliance on External Subsidies

SPH’s media arm relies heavily on government grants and corporate sponsorships—about 35% of FY2024 media revenue came from subsidies and sponsored content, per company disclosures—making operations vulnerable to shifts in public policy or budget cuts.

If grants drop, EBITDA could fall sharply: a 10% subsidy reduction would trim FY2024 group EBITDA by ~3.5 percentage points, exposing weak commercial ad and subscription growth.

Limited Geographic Diversification in Media

SPH’s media arm is still almost wholly Singapore-focused, while its real-estate division has assets in Australia and the UK; this concentration caps addressable digital-subscription growth given Singapore’s 5.9 million population (2025 est.) and limits global ad revenue potential.

Global platforms like Google and Meta—which together took ~62% of APAC digital ad spend in 2024—outcompete SPH’s reach, squeezing CPMs and hindering scale economics for content investment.

Historical Data Integrity and Public Trust Issues

Past circulation overstatement scandals—most notably the 2019 disclosure reducing reported print reach by ~18%—have dented SPH’s transparency image and advertiser confidence.

Rebuilding trust is slow; SPH now uses quarterly third-party audits (Kantar, Nielsen) and must sustain them to reassure clients; lapses would magnify reputational and revenue risk.

- 2019 reach cut ~18%

- Quarterly third-party audits in place

- Any new lapse could sharply hit ad spend and credibility

High Operating Costs in a Tight Labor Market

- Tech salary growth: +8.5% (2024)

- Electricity tariffs: +12% YoY (2024)

- Industry churn: ~9% (2024)

- Higher capex for property maintenance

SPH margin squeeze: print collapse, subsidy reliance and rising costs threaten EBITDA

SPH suffers falling print revenue (−18% y/y in 2024) and slower digital monetisation (digital ads +12% in 2024 but ~40% below legacy print), heavy reliance on subsidies (~35% of media revenue FY2024), Singapore market concentration (pop. 5.9M est. 2025), and rising costs (tech wages +8.5% and electricity +12% in 2024) that compress EBITDA and heighten reputational risk after the 2019 reach cut (−18%).

| Metric | 2024/2025 |

|---|---|

| Print revenue change | −18% y/y (2024) |

| Digital ad growth | +12% (2024) |

| Subsidies of media rev | ~35% (FY2024) |

| Singapore pop. | 5.9M (2025 est.) |

| Tech wage growth | +8.5% (2024) |

| Electricity | +12% YoY (2024) |

Same Document Delivered

SPH SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

SPH’s resilient brand portfolio and digital push position it well against regional peers, yet legacy print exposure and revenue cyclicality pose material risks to short-term margins and valuation upside.

Strengths

Dominant Market Position in Singapore Media

As of late 2025, SPH Media remains Singapore’s primary news source with over 60% weekly reach across print, digital and radio, securing roughly S$220m in advertising revenue for FY2024–25; this legacy brand equity produces a loyal audience hard for new entrants to match. SPH leverages that dominance to win high-value national advertisers and sustain strong social influence on public discourse.

Significant Government Financial Support

The 2024 restructuring into a not-for-profit let SPH Media secure up to S$900 million (≈US$660M) in government funding across five years, giving a rare cash buffer for legacy-to-digital shifts.

That funding removes quarterly profit pressure, so SPH can pace investments in paywalls, data platforms, and AI-driven personalization aimed at restoring digital ad and subscription growth.

High Quality Core Real Estate Assets

The legacy portfolio includes Paragon (Orchard Road) and The Woodleigh Mall (Bidadari), which posted rental reversion of +8% and +6% respectively in FY2024 and maintained >95% occupancy, underpinning resilient cash flows during 2023–24 volatility.

Strategic Diversification into Student Accommodation

- UK/Australia PBSA: occupancy >95%

- Valuation gains ~£120m (30% since 2020)

- Counter-cyclical revenue stream, stable yields

- Pivots away from traditional media to real estate

Advanced Digital Infrastructure and AI Integration

- Production time −40%

- Session duration +22%

- Paid users 320,000 (+18% YoY)

- Ad revenue +12% FY2024

- Users 18–34 = 48%

SPH: 60% reach, S$900M funding, digital & real estate surging—paid users +18%

SPH’s strengths: dominant national reach (60% weekly), S$900m five-year funding secured in 2024, diversified high-occupancy real estate (Paragon/Woodleigh >95% occupancy; PBSA valuation +£120m since 2020, occupancy >95%), digital progress (320,000 paid users +18% YoY; ad rev +12%; production time −40%; mobile session +22%).

| Metric | Value |

|---|---|

| Weekly reach | 60% |

| Government funding (5y) | S$900m |

| Paid users | 320,000 (+18% YoY) |

| Ad revenue FY2024 | +12% |

| PBSA valuation gain | +£120m (since 2020) |

| Occupancy (retail/PBSA) | >95% |

| Production time | −40% |

| Mobile session duration | +22% |

What is included in the product

Provides a concise SWOT overview of SPH, outlining its core strengths and weaknesses alongside market opportunities and external threats to inform strategic decisions.

Provides a concise SWOT matrix tailored to SPH for rapid strategy alignment and quick integration into reports, slides, and stakeholder reviews.

Weaknesses

Structural Decline in Print Revenue

Despite digital growth, SPH (Singapore Press Holdings) faces a secular decline in print circulation and advertising, which historically delivered higher margins; print revenue fell about 18% y/y in 2024, keeping EBITDA under pressure.

The shift to digital-first hasn’t matched print dollar-for-dollar: digital ad revenue grew ~12% in 2024 but remained roughly 40% below legacy print revenue levels, widening the revenue gap.

This ongoing erosion of a core legacy stream continues to drag overall financial performance, contributing to a 7% decline in total group revenue in FY2024 and compressing operating margins.

Heavy Reliance on External Subsidies

SPH’s media arm relies heavily on government grants and corporate sponsorships—about 35% of FY2024 media revenue came from subsidies and sponsored content, per company disclosures—making operations vulnerable to shifts in public policy or budget cuts.

If grants drop, EBITDA could fall sharply: a 10% subsidy reduction would trim FY2024 group EBITDA by ~3.5 percentage points, exposing weak commercial ad and subscription growth.

Limited Geographic Diversification in Media

SPH’s media arm is still almost wholly Singapore-focused, while its real-estate division has assets in Australia and the UK; this concentration caps addressable digital-subscription growth given Singapore’s 5.9 million population (2025 est.) and limits global ad revenue potential.

Global platforms like Google and Meta—which together took ~62% of APAC digital ad spend in 2024—outcompete SPH’s reach, squeezing CPMs and hindering scale economics for content investment.

Historical Data Integrity and Public Trust Issues

Past circulation overstatement scandals—most notably the 2019 disclosure reducing reported print reach by ~18%—have dented SPH’s transparency image and advertiser confidence.

Rebuilding trust is slow; SPH now uses quarterly third-party audits (Kantar, Nielsen) and must sustain them to reassure clients; lapses would magnify reputational and revenue risk.

- 2019 reach cut ~18%

- Quarterly third-party audits in place

- Any new lapse could sharply hit ad spend and credibility

High Operating Costs in a Tight Labor Market

- Tech salary growth: +8.5% (2024)

- Electricity tariffs: +12% YoY (2024)

- Industry churn: ~9% (2024)

- Higher capex for property maintenance

SPH margin squeeze: print collapse, subsidy reliance and rising costs threaten EBITDA

SPH suffers falling print revenue (−18% y/y in 2024) and slower digital monetisation (digital ads +12% in 2024 but ~40% below legacy print), heavy reliance on subsidies (~35% of media revenue FY2024), Singapore market concentration (pop. 5.9M est. 2025), and rising costs (tech wages +8.5% and electricity +12% in 2024) that compress EBITDA and heighten reputational risk after the 2019 reach cut (−18%).

| Metric | 2024/2025 |

|---|---|

| Print revenue change | −18% y/y (2024) |

| Digital ad growth | +12% (2024) |

| Subsidies of media rev | ~35% (FY2024) |

| Singapore pop. | 5.9M (2025 est.) |

| Tech wage growth | +8.5% (2024) |

| Electricity | +12% YoY (2024) |

Same Document Delivered

SPH SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy now to unlock the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.