Spirax-Sarco Engineering Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

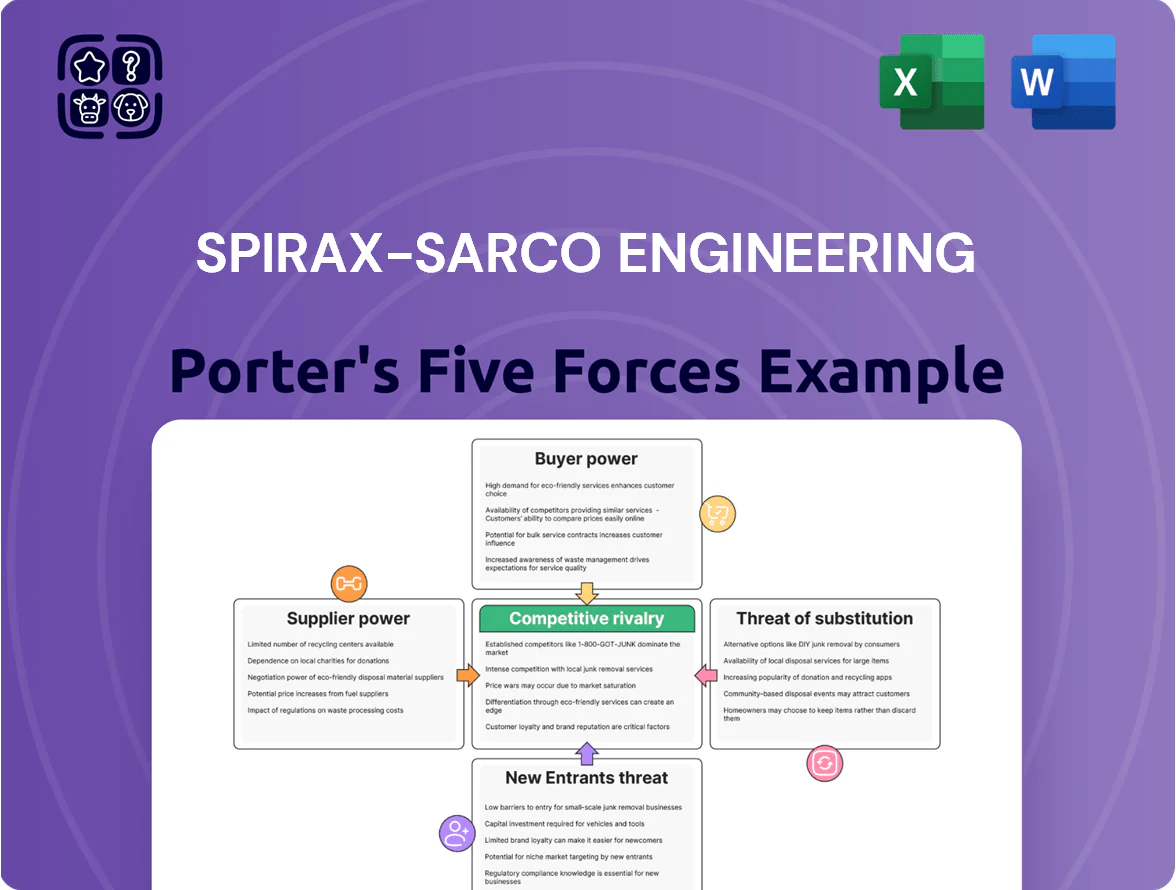

Spirax-Sarco Engineering operates in a niche industrial steam and thermal management market with moderate supplier power, differentiated products that limit buyer leverage, and relatively high barriers deterring new entrants.

Competitive rivalry is steady but innovation and service breadth are key differentiators, while substitutes pose limited immediate threat.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Spirax-Sarco Engineering’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse raw material sourcing

Spirax-Sarco sources stainless steel, copper and specialized electronics across a global network of 200+ approved suppliers, lowering supplier price power; in FY2024 materials accounted for about 34% of COGS, so diversified sourcing cut single-supplier risk and helped contain input-cost inflation to a 3.2% increase versus industry average 5.8%.

Specialized component dependency

Certain high-precision components for Watson-Marlow pumps and Chromalox heating elements come from niche suppliers with unique capabilities, giving them higher bargaining power because these parts affect product quality and compliance; industry data shows single-supplier risk raises procurement premium by ~8–12% and can delay production by 6–10 weeks.

Spirax-Sarco reduces this leverage via multi-year partnership contracts and joint R&D; in 2024 the company reported supplier contract coverage at ~72% of critical parts and a 15% reduction in lead-time variance versus 2019.

Rising importance of electronic subsystems

As Spirax-Sarco adds IoT and digital monitoring to steam and pumping systems, its dependence on semiconductors and sensors—markets where top 5 suppliers hold >60% share—has risen, raising risk of supply constraints and price swings (chip shortages cut global industrial IC availability by ~15% in 2021–23). Spirax-Sarco hedges via forward inventory buys and modular hardware designs that allow component substitution, trimming potential downtime and margin shock.

Labor and energy costs

Suppliers of energy-intensive materials like cast iron and specialized alloys try to pass higher energy costs—which rose ~15% globally in 2024—onto engineering firms, squeezing margins for heat-transfer equipment makers.

Tightening skilled-labor supply in precision manufacturing pushed UK/Europe wage growth for machinists ~6–8% in 2023–24, raising sub-assembly costs.

Spirax-Sarco offsets this by leveraging annual volumes (2024 revenue £1.97bn) to secure discounts and longer-term supply contracts.

- Energy prices +15% (2024)

- Machinist pay +6–8% (2023–24)

- Spirax-Sarco 2024 revenue £1.97bn

Vertical integration initiatives

Spirax-Sarco has selectively vertically integrated and acquired tech partners, cutting supplier hold-up risk by securing critical IP and production stages; in 2024 internal manufacturing accounted for about 36% of core component spend, boosting control versus smaller rivals.

By making many core parts in-house the group raises self-sufficiency, supports gross margin resilience (FY2024 adjusted gross margin ~53.8%), and shortens lead times during supply shocks.

- 36% internal component spend (2024)

- FY2024 adjusted gross margin 53.8%

- Acquisitions target critical IP and production

- Lower holdup risk, shorter lead times

Spirax-Sarco: Strong margins and supply diversity but niche suppliers, rising costs bite

Spirax-Sarco faces moderate supplier power: diversified 200+ suppliers and 36% in-house production limit price pressure, yet niche pump/sensor suppliers and energy/wage inflation (energy +15% 2024; machinist pay +6–8% 2023–24) keep vulnerability. FY2024 revenue £1.97bn and adjusted gross margin 53.8% support bargaining leverage and longer-term contracts (72% critical parts covered).

| Metric | 2024 |

|---|---|

| Suppliers | 200+ |

| In-house component spend | 36% |

| Revenue | £1.97bn |

| Adj. gross margin | 53.8% |

| Energy change | +15% |

| Machinist pay | +6–8% |

What is included in the product

Tailored exclusively for Spirax-Sarco Engineering, this Porter's Five Forces analysis uncovers key drivers of competition, evaluates supplier and buyer power, identifies substitutes and new entrant risks, and highlights disruptive threats to the company’s market share and profitability.

A concise Porter's Five Forces one-sheet for Spirax-Sarco—quickly highlights supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions.

Customers Bargaining Power

High cost of failure for end users

In pharmaceuticals and food production a Spirax-Sarco valve failure can cost millions in lost product and shutdowns, so buyers pay for reliability and service over lowest price; surveys show 72% of process plants prioritize uptime over cost, weakening customer bargaining on price.

Fragmented global customer base

Spirax-Sarco serves over 100,000 customers across industries and 70+ countries, so no single client can dictate pricing or terms.

Large multinationals may secure global framework agreements, but SME clients—which make up the majority—provide a steady revenue floor, reducing concentration risk.

This customer fragmentation helped Spirax-Sarco report 2024 gross margins near 46%, keeping negotiating leverage and protecting margins from a few big buyers.

Switching costs and system integration

Once a Spirax-Sarco steam system or Watson-Marlow fluid path is embedded, estimated re‑engineering and downtime costs often exceed 15–25% of annual plant operating expenses, making switches costly and slow.

Customers follow strict maintenance cycles and buy proprietary spare parts; Spirax‑Sarco reported 2024 aftermarket revenue of £413m, underlining lock‑in via parts and service.

This deep integration drives long tenure: renewal rates in industrial OEM aftermarket contracts commonly exceed 80%, reducing price‑only churn.

Demand for energy efficiency and decarbonization

Industrial customers face rising ESG mandates; 78% of global manufacturers report decarbonization targets for 2030, pushing demand for Spirax-Sarco’s thermal-efficiency solutions that cut steam system losses up to 20%.

Spirax-Sarco’s energy audits and retrofit services position it as a strategic partner, shifting buyer focus from upfront price to total cost of ownership and avoided CO2—clients report paybacks often under 3 years.

- 78% manufacturers with 2030 ESG targets

- Steam efficiency gains ~20%

- Typical retrofit payback <3 years

- Focus: TCO and CO2 reduction

Information transparency and procurement sophistication

Modern industrial buyers use advanced e-procurement and benchmarking tools and access market databases to compare specs and pricing, raising pressure on Spirax-Sarco (FTSE 250, 2024 revenue £1.3bn) to defend its premium margins.

Spirax-Sarco counters by stressing bespoke engineering, claiming higher uptime and lifecycle savings; its service-led contracts grew 9% in 2024, helping justify price premiums.

- Buyers: greater price/spec transparency

- Impact: margin pressure vs premium pricing

- Company response: bespoke solutions, service contracts +9% (2024)

- Key metric: £1.3bn revenue (2024)

Strong aftermarket lock‑in: £413m revenue, ~46% margin, >80% renewals fuel pricing power

Customers have limited price leverage: 100,000+ clients across 70+ countries dilute concentration, aftermarket revenue £413m (2024) and gross margin ~46% protect pricing, and high switching costs (reworks >15–25% of OPEX) plus >80% aftermarket renewal rates drive lock‑in; e‑procurement raises transparency, but service contracts (+9% in 2024) and TCO focus sustain premiums.

| Metric | Value (2024) |

|---|---|

| Customers | 100,000+ |

| Countries | 70+ |

| Aftermarket rev | £413m |

| Gross margin | ~46% |

| Service growth | +9% |

| Renewal rate | >80% |

Full Version Awaits

Spirax-Sarco Engineering Porter's Five Forces Analysis

This preview shows the exact Spirax-Sarco Engineering Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You're looking at the actual analysis file; once payment is complete, you’ll get instant access to this same ready-to-use document.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Spirax-Sarco Engineering operates in a niche industrial steam and thermal management market with moderate supplier power, differentiated products that limit buyer leverage, and relatively high barriers deterring new entrants.

Competitive rivalry is steady but innovation and service breadth are key differentiators, while substitutes pose limited immediate threat.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Spirax-Sarco Engineering’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse raw material sourcing

Spirax-Sarco sources stainless steel, copper and specialized electronics across a global network of 200+ approved suppliers, lowering supplier price power; in FY2024 materials accounted for about 34% of COGS, so diversified sourcing cut single-supplier risk and helped contain input-cost inflation to a 3.2% increase versus industry average 5.8%.

Specialized component dependency

Certain high-precision components for Watson-Marlow pumps and Chromalox heating elements come from niche suppliers with unique capabilities, giving them higher bargaining power because these parts affect product quality and compliance; industry data shows single-supplier risk raises procurement premium by ~8–12% and can delay production by 6–10 weeks.

Spirax-Sarco reduces this leverage via multi-year partnership contracts and joint R&D; in 2024 the company reported supplier contract coverage at ~72% of critical parts and a 15% reduction in lead-time variance versus 2019.

Rising importance of electronic subsystems

As Spirax-Sarco adds IoT and digital monitoring to steam and pumping systems, its dependence on semiconductors and sensors—markets where top 5 suppliers hold >60% share—has risen, raising risk of supply constraints and price swings (chip shortages cut global industrial IC availability by ~15% in 2021–23). Spirax-Sarco hedges via forward inventory buys and modular hardware designs that allow component substitution, trimming potential downtime and margin shock.

Labor and energy costs

Suppliers of energy-intensive materials like cast iron and specialized alloys try to pass higher energy costs—which rose ~15% globally in 2024—onto engineering firms, squeezing margins for heat-transfer equipment makers.

Tightening skilled-labor supply in precision manufacturing pushed UK/Europe wage growth for machinists ~6–8% in 2023–24, raising sub-assembly costs.

Spirax-Sarco offsets this by leveraging annual volumes (2024 revenue £1.97bn) to secure discounts and longer-term supply contracts.

- Energy prices +15% (2024)

- Machinist pay +6–8% (2023–24)

- Spirax-Sarco 2024 revenue £1.97bn

Vertical integration initiatives

Spirax-Sarco has selectively vertically integrated and acquired tech partners, cutting supplier hold-up risk by securing critical IP and production stages; in 2024 internal manufacturing accounted for about 36% of core component spend, boosting control versus smaller rivals.

By making many core parts in-house the group raises self-sufficiency, supports gross margin resilience (FY2024 adjusted gross margin ~53.8%), and shortens lead times during supply shocks.

- 36% internal component spend (2024)

- FY2024 adjusted gross margin 53.8%

- Acquisitions target critical IP and production

- Lower holdup risk, shorter lead times

Spirax-Sarco: Strong margins and supply diversity but niche suppliers, rising costs bite

Spirax-Sarco faces moderate supplier power: diversified 200+ suppliers and 36% in-house production limit price pressure, yet niche pump/sensor suppliers and energy/wage inflation (energy +15% 2024; machinist pay +6–8% 2023–24) keep vulnerability. FY2024 revenue £1.97bn and adjusted gross margin 53.8% support bargaining leverage and longer-term contracts (72% critical parts covered).

| Metric | 2024 |

|---|---|

| Suppliers | 200+ |

| In-house component spend | 36% |

| Revenue | £1.97bn |

| Adj. gross margin | 53.8% |

| Energy change | +15% |

| Machinist pay | +6–8% |

What is included in the product

Tailored exclusively for Spirax-Sarco Engineering, this Porter's Five Forces analysis uncovers key drivers of competition, evaluates supplier and buyer power, identifies substitutes and new entrant risks, and highlights disruptive threats to the company’s market share and profitability.

A concise Porter's Five Forces one-sheet for Spirax-Sarco—quickly highlights supplier, buyer, rivalry, entrant, and substitute pressures to speed strategic decisions.

Customers Bargaining Power

High cost of failure for end users

In pharmaceuticals and food production a Spirax-Sarco valve failure can cost millions in lost product and shutdowns, so buyers pay for reliability and service over lowest price; surveys show 72% of process plants prioritize uptime over cost, weakening customer bargaining on price.

Fragmented global customer base

Spirax-Sarco serves over 100,000 customers across industries and 70+ countries, so no single client can dictate pricing or terms.

Large multinationals may secure global framework agreements, but SME clients—which make up the majority—provide a steady revenue floor, reducing concentration risk.

This customer fragmentation helped Spirax-Sarco report 2024 gross margins near 46%, keeping negotiating leverage and protecting margins from a few big buyers.

Switching costs and system integration

Once a Spirax-Sarco steam system or Watson-Marlow fluid path is embedded, estimated re‑engineering and downtime costs often exceed 15–25% of annual plant operating expenses, making switches costly and slow.

Customers follow strict maintenance cycles and buy proprietary spare parts; Spirax‑Sarco reported 2024 aftermarket revenue of £413m, underlining lock‑in via parts and service.

This deep integration drives long tenure: renewal rates in industrial OEM aftermarket contracts commonly exceed 80%, reducing price‑only churn.

Demand for energy efficiency and decarbonization

Industrial customers face rising ESG mandates; 78% of global manufacturers report decarbonization targets for 2030, pushing demand for Spirax-Sarco’s thermal-efficiency solutions that cut steam system losses up to 20%.

Spirax-Sarco’s energy audits and retrofit services position it as a strategic partner, shifting buyer focus from upfront price to total cost of ownership and avoided CO2—clients report paybacks often under 3 years.

- 78% manufacturers with 2030 ESG targets

- Steam efficiency gains ~20%

- Typical retrofit payback <3 years

- Focus: TCO and CO2 reduction

Information transparency and procurement sophistication

Modern industrial buyers use advanced e-procurement and benchmarking tools and access market databases to compare specs and pricing, raising pressure on Spirax-Sarco (FTSE 250, 2024 revenue £1.3bn) to defend its premium margins.

Spirax-Sarco counters by stressing bespoke engineering, claiming higher uptime and lifecycle savings; its service-led contracts grew 9% in 2024, helping justify price premiums.

- Buyers: greater price/spec transparency

- Impact: margin pressure vs premium pricing

- Company response: bespoke solutions, service contracts +9% (2024)

- Key metric: £1.3bn revenue (2024)

Strong aftermarket lock‑in: £413m revenue, ~46% margin, >80% renewals fuel pricing power

Customers have limited price leverage: 100,000+ clients across 70+ countries dilute concentration, aftermarket revenue £413m (2024) and gross margin ~46% protect pricing, and high switching costs (reworks >15–25% of OPEX) plus >80% aftermarket renewal rates drive lock‑in; e‑procurement raises transparency, but service contracts (+9% in 2024) and TCO focus sustain premiums.

| Metric | Value (2024) |

|---|---|

| Customers | 100,000+ |

| Countries | 70+ |

| Aftermarket rev | £413m |

| Gross margin | ~46% |

| Service growth | +9% |

| Renewal rate | >80% |

Full Version Awaits

Spirax-Sarco Engineering Porter's Five Forces Analysis

This preview shows the exact Spirax-Sarco Engineering Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted report you’ll be able to download and use the moment you buy.

You're looking at the actual analysis file; once payment is complete, you’ll get instant access to this same ready-to-use document.