Sportsman's Warehouse Holdings Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Sportsman's Warehouse faces moderate buyer power and high threat from online and specialty rivals, while supplier influence and capital intensity temper margin expansion—this snapshot hints at strategic pressure points and growth levers.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Sportsman's Warehouse Holdings to inform smarter investment and strategy decisions.

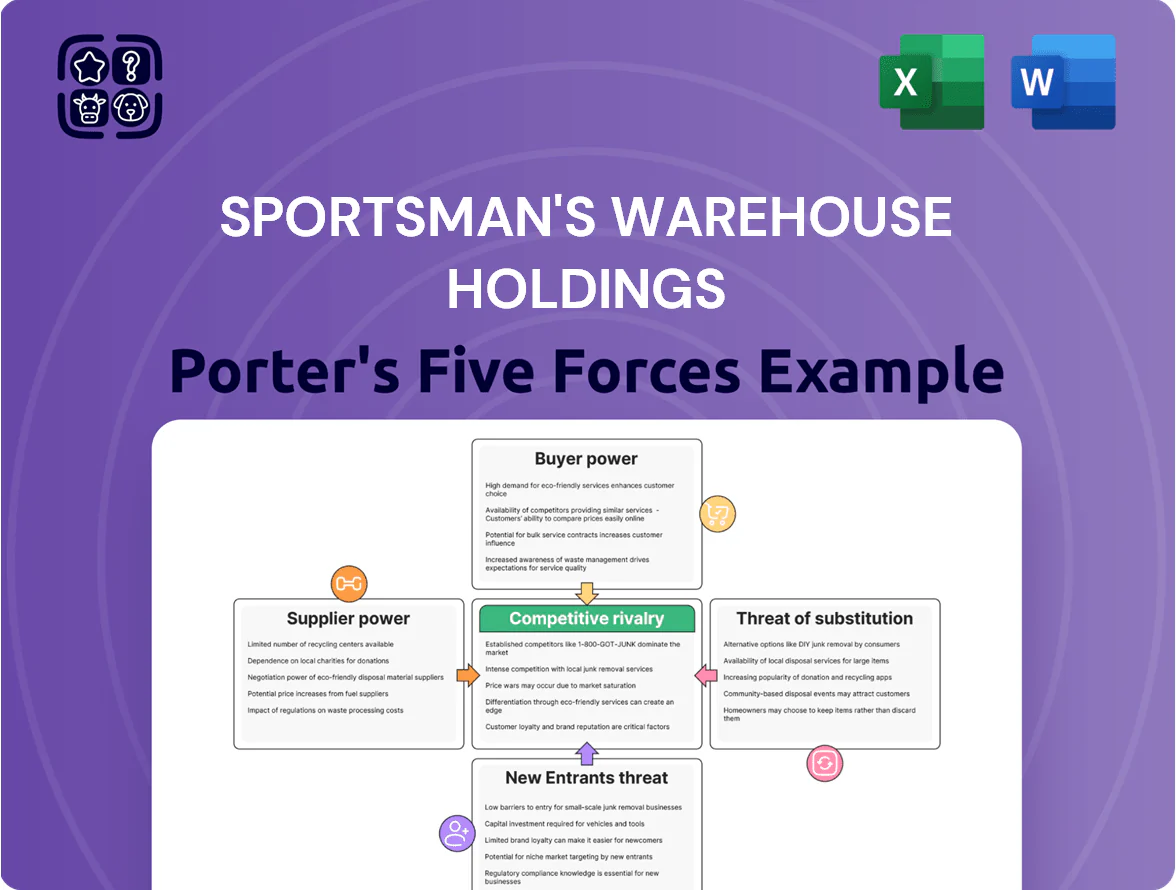

Suppliers Bargaining Power

Concentration of Key Brand Manufacturers

The outdoor market is concentrated: in firearms, ammo, and premium technical apparel three-to-five brands (eg, Vista Outdoors, Smith & Wesson Brands, Gore-Tex licensees) account for roughly 60–75% of category sales, giving suppliers strong leverage over retailers like Sportsman's Warehouse. Their products drive store traffic, so suppliers can demand higher wholesale prices and tighter allocation; by late 2025 consolidation raised supplier gross margin setting power by an estimated 5–10 percentage points.

Supply Chain Resilience and Inventory Access

Suppliers with strong logistics gained leverage as retailers chase in-stock rates; in 2024 retailers targeted 98% availability, boosting supplier power. Sportsman’s Warehouse depends on seasonal hunting and fishing peaks—Q4 2023 accounted for ~32% of annual outdoor-gear sales—so on-time deliveries matter. High-performing vendors can demand net-60 terms or MOQ hikes; in 2024 top suppliers negotiated average price premiums of 3–5% for guaranteed fill rates.

Direct-to-Consumer (DTC) Shift

As suppliers like Vista Outdoor and Smith & Wesson expand DTC channels—US sporting goods DTC sales rose ~18% in 2024 to $6.5B—suppliers depend less on wholesale, eroding Sportsman's Warehouse’s leverage and pressuring margins.

To stay a preferred partner, Sportsman's Warehouse must deliver superior localized services—inventory availability, in-store expertise, local marketing—that DTC can't match, or face higher supplier pricing and reduced SKU access.

Regulatory Compliance and Specialized Production

Suppliers of firearms and ammunition face tight federal and state rules (ATF, FFL licensing), raising entry barriers and limiting alternative sources for Sportsman's Warehouse; only ~100 major ammo manufacturers and a few dozen large firearm makers dominate the U.S. market as of 2025.

Specialized production needs high capex and licensed facilities, keeping supplier pool small; this scarcity lets suppliers hold prices—ammo wholesale index rose ~12% in 2023–24—even when retail demand swings.

- High regulatory cost: FFL/ATF compliance

- Small supplier pool: ~100 major ammo makers

- High capex/licensing limits entry

- Pricing power: wholesale ammo +12% (2023–24)

Input Cost Pass-Through

Suppliers have passed higher raw-material costs—lead, brass, synthetic fabrics—directly to Sportsman's Warehouse, and by 2025 inflation in manufacturing drove the company to accept price hikes to preserve assortment and margins.

Industry-wide cost increases limit Sportsman's Warehouse’s bargaining leverage versus major competitors; passthrough was visible in 2024–2025 COGS upticks and thinner gross margin episodes.

- 2025: manufacturing inflation forced retailer price acceptance

- Key inputs: lead, brass, synthetic fabrics

- Industry-wide hikes reduce pushback power

Concentrated Ammo Suppliers Force Retailers to Pay Premiums as DTC Sales Surge

Suppliers (eg, Vista Outdoors, Smith & Wesson) hold strong leverage: 60–75% category share, ~100 major ammo makers, wholesale ammo +12% (2023–24), DTC sales up 18% to $6.5B (2024), top vendors got 3–5% price premiums for fill rates; regulatory/CapEx barriers keep supplier pool small, forcing Sportsman's Warehouse to accept higher prices to maintain assortment.

| Metric | Value |

|---|---|

| Category concentration | 60–75% |

| Major ammo makers | ~100 |

| Ammo wholesale change | +12% (2023–24) |

| DTC sporting goods | $6.5B, +18% (2024) |

What is included in the product

Tailored exclusively for Sportsman's Warehouse Holdings, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier leverage, entry barriers, substitutes, and emerging threats that shape its pricing power and profitability.

A concise Porter's Five Forces one-sheet for Sportsman's Warehouse—quickly spot supplier, buyer, and competitive pressures to guide merchandising, pricing, and store expansion decisions.

Customers Bargaining Power

Low Switching Costs for Enthusiasts

Customers can compare prices and inventory across Amazon, Cabela’s, Bass Pro and Walmart in seconds, and 64% of outdoor shoppers reported using online price comparison in 2024, so switching is easy.

Many SKUs—ammo, apparel, optics—are commoditized, making brand loyalty secondary to price and convenience; repeat buyers often chase deals.

That dynamic pushed Sportsman’s Warehouse to run discount-heavy promos in 2024, contributing to a 7% same-store sales decline in Q3 2024 and higher promo-driven margin pressure.

Access to Real-Time Price Transparency

The prevalence of mobile shopping apps lets customers check competitor prices while in a Sportsman's Warehouse store, prompting immediate price matching demands or on-the-spot online orders from cheaper retailers.

By end-2025, price transparency helped cut Sportsman's Warehouse gross margins on commodity items by about 160 basis points versus 2021, per industry pricing studies, capping markup flexibility.

Price Sensitivity in Discretionary Spending

Outdoor gear is largely discretionary, so demand at Sportsman's Warehouse Holdings (SPWH) falls with income shocks; US personal consumption on recreation goods dropped 3.1% in Q4 2023 year-over-year, showing sensitivity.

In recessions shoppers prioritize value over premium features, and in 2024 SPWH reported higher promotional activity with gross margin compression of ~120 basis points.

This price sensitivity gives buyers leverage to force heavy discounting cycles to clear inventory, as seen in SPWH’s inventory-to-sales ratio rising to 1.28 in FY2024.

Demand for Integrated Omni-Channel Experiences

Modern consumers expect seamless BOPIS (buy-online-pickup-in-store); 2024 data show 58% of US shoppers used BOPIS at least once and retailers with robust omni-channel saw 20% higher basket size.

If Sportsman's Warehouse lags, shoppers shift to Bass Pro Shops, Cabela’s, or Amazon—Amazon Prime members spend 2.5x more annually.

The bargaining power rests with customers to set service and tech standards; meeting BOPIS and real-time inventory is essential to retain market share and revenue.

- 58% US shoppers used BOPIS (2024)

- Omni-channel retailers +20% basket size

- Amazon Prime shoppers spend 2.5x more

- Real-time inventory and BOPIS are must-haves

Influence of Online Reviews and Community Forums

Peer reviews and outdoor forums drive buying: 63% of outdoor shoppers say user reviews heavily influence purchases (2024 Nielsen study), so negative service or quality trends can erode Sportsman’s Warehouse’s share quickly.

A viral complaint cascades: e.g., a 2023 product recall in the sector cut one retailer’s same-store sales 4–6% in Q2, showing rapid impact on revenue and margin.

This social power forces Sportsman’s Warehouse to keep high standards in engagement, response time, and community programs to protect its ~$1.1B FY2024 revenue base.

- 63% of buyers influenced by reviews (2024 Nielsen)

- Sector recall linked to 4–6% same-store sales drop (2023)

- Sportsman’s Warehouse revenue ~$1.1B FY2024 — reputational risk hits top line

Customer Power Forces SPWH Into Discounting—Margins Down, Inventory Rising

Customers hold strong leverage: 64% use online price comparison (2024), 58% used BOPIS (2024), and reviews sway 63% of buyers, forcing SPWH into discounting that cut gross margin ~160 bps vs 2021 and drove a 7% Q3 2024 comp decline; inventory-to-sales rose to 1.28 in FY2024, risking further margin pressure.

| Metric | Value |

|---|---|

| Online price comparison | 64% (2024) |

| BOPIS use | 58% (2024) |

| Review influence | 63% (2024) |

| Gross margin change | -160 bps vs 2021 |

| Comp sales Q3 2024 | -7% |

| Inventory/sales FY2024 | 1.28 |

What You See Is What You Get

Sportsman's Warehouse Holdings Porter's Five Forces Analysis

This preview shows the exact Sportsman's Warehouse Holdings Porter's Five Forces analysis you’ll receive after purchase—no samples or placeholders, fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Sportsman's Warehouse faces moderate buyer power and high threat from online and specialty rivals, while supplier influence and capital intensity temper margin expansion—this snapshot hints at strategic pressure points and growth levers.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Sportsman's Warehouse Holdings to inform smarter investment and strategy decisions.

Suppliers Bargaining Power

Concentration of Key Brand Manufacturers

The outdoor market is concentrated: in firearms, ammo, and premium technical apparel three-to-five brands (eg, Vista Outdoors, Smith & Wesson Brands, Gore-Tex licensees) account for roughly 60–75% of category sales, giving suppliers strong leverage over retailers like Sportsman's Warehouse. Their products drive store traffic, so suppliers can demand higher wholesale prices and tighter allocation; by late 2025 consolidation raised supplier gross margin setting power by an estimated 5–10 percentage points.

Supply Chain Resilience and Inventory Access

Suppliers with strong logistics gained leverage as retailers chase in-stock rates; in 2024 retailers targeted 98% availability, boosting supplier power. Sportsman’s Warehouse depends on seasonal hunting and fishing peaks—Q4 2023 accounted for ~32% of annual outdoor-gear sales—so on-time deliveries matter. High-performing vendors can demand net-60 terms or MOQ hikes; in 2024 top suppliers negotiated average price premiums of 3–5% for guaranteed fill rates.

Direct-to-Consumer (DTC) Shift

As suppliers like Vista Outdoor and Smith & Wesson expand DTC channels—US sporting goods DTC sales rose ~18% in 2024 to $6.5B—suppliers depend less on wholesale, eroding Sportsman's Warehouse’s leverage and pressuring margins.

To stay a preferred partner, Sportsman's Warehouse must deliver superior localized services—inventory availability, in-store expertise, local marketing—that DTC can't match, or face higher supplier pricing and reduced SKU access.

Regulatory Compliance and Specialized Production

Suppliers of firearms and ammunition face tight federal and state rules (ATF, FFL licensing), raising entry barriers and limiting alternative sources for Sportsman's Warehouse; only ~100 major ammo manufacturers and a few dozen large firearm makers dominate the U.S. market as of 2025.

Specialized production needs high capex and licensed facilities, keeping supplier pool small; this scarcity lets suppliers hold prices—ammo wholesale index rose ~12% in 2023–24—even when retail demand swings.

- High regulatory cost: FFL/ATF compliance

- Small supplier pool: ~100 major ammo makers

- High capex/licensing limits entry

- Pricing power: wholesale ammo +12% (2023–24)

Input Cost Pass-Through

Suppliers have passed higher raw-material costs—lead, brass, synthetic fabrics—directly to Sportsman's Warehouse, and by 2025 inflation in manufacturing drove the company to accept price hikes to preserve assortment and margins.

Industry-wide cost increases limit Sportsman's Warehouse’s bargaining leverage versus major competitors; passthrough was visible in 2024–2025 COGS upticks and thinner gross margin episodes.

- 2025: manufacturing inflation forced retailer price acceptance

- Key inputs: lead, brass, synthetic fabrics

- Industry-wide hikes reduce pushback power

Concentrated Ammo Suppliers Force Retailers to Pay Premiums as DTC Sales Surge

Suppliers (eg, Vista Outdoors, Smith & Wesson) hold strong leverage: 60–75% category share, ~100 major ammo makers, wholesale ammo +12% (2023–24), DTC sales up 18% to $6.5B (2024), top vendors got 3–5% price premiums for fill rates; regulatory/CapEx barriers keep supplier pool small, forcing Sportsman's Warehouse to accept higher prices to maintain assortment.

| Metric | Value |

|---|---|

| Category concentration | 60–75% |

| Major ammo makers | ~100 |

| Ammo wholesale change | +12% (2023–24) |

| DTC sporting goods | $6.5B, +18% (2024) |

What is included in the product

Tailored exclusively for Sportsman's Warehouse Holdings, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier leverage, entry barriers, substitutes, and emerging threats that shape its pricing power and profitability.

A concise Porter's Five Forces one-sheet for Sportsman's Warehouse—quickly spot supplier, buyer, and competitive pressures to guide merchandising, pricing, and store expansion decisions.

Customers Bargaining Power

Low Switching Costs for Enthusiasts

Customers can compare prices and inventory across Amazon, Cabela’s, Bass Pro and Walmart in seconds, and 64% of outdoor shoppers reported using online price comparison in 2024, so switching is easy.

Many SKUs—ammo, apparel, optics—are commoditized, making brand loyalty secondary to price and convenience; repeat buyers often chase deals.

That dynamic pushed Sportsman’s Warehouse to run discount-heavy promos in 2024, contributing to a 7% same-store sales decline in Q3 2024 and higher promo-driven margin pressure.

Access to Real-Time Price Transparency

The prevalence of mobile shopping apps lets customers check competitor prices while in a Sportsman's Warehouse store, prompting immediate price matching demands or on-the-spot online orders from cheaper retailers.

By end-2025, price transparency helped cut Sportsman's Warehouse gross margins on commodity items by about 160 basis points versus 2021, per industry pricing studies, capping markup flexibility.

Price Sensitivity in Discretionary Spending

Outdoor gear is largely discretionary, so demand at Sportsman's Warehouse Holdings (SPWH) falls with income shocks; US personal consumption on recreation goods dropped 3.1% in Q4 2023 year-over-year, showing sensitivity.

In recessions shoppers prioritize value over premium features, and in 2024 SPWH reported higher promotional activity with gross margin compression of ~120 basis points.

This price sensitivity gives buyers leverage to force heavy discounting cycles to clear inventory, as seen in SPWH’s inventory-to-sales ratio rising to 1.28 in FY2024.

Demand for Integrated Omni-Channel Experiences

Modern consumers expect seamless BOPIS (buy-online-pickup-in-store); 2024 data show 58% of US shoppers used BOPIS at least once and retailers with robust omni-channel saw 20% higher basket size.

If Sportsman's Warehouse lags, shoppers shift to Bass Pro Shops, Cabela’s, or Amazon—Amazon Prime members spend 2.5x more annually.

The bargaining power rests with customers to set service and tech standards; meeting BOPIS and real-time inventory is essential to retain market share and revenue.

- 58% US shoppers used BOPIS (2024)

- Omni-channel retailers +20% basket size

- Amazon Prime shoppers spend 2.5x more

- Real-time inventory and BOPIS are must-haves

Influence of Online Reviews and Community Forums

Peer reviews and outdoor forums drive buying: 63% of outdoor shoppers say user reviews heavily influence purchases (2024 Nielsen study), so negative service or quality trends can erode Sportsman’s Warehouse’s share quickly.

A viral complaint cascades: e.g., a 2023 product recall in the sector cut one retailer’s same-store sales 4–6% in Q2, showing rapid impact on revenue and margin.

This social power forces Sportsman’s Warehouse to keep high standards in engagement, response time, and community programs to protect its ~$1.1B FY2024 revenue base.

- 63% of buyers influenced by reviews (2024 Nielsen)

- Sector recall linked to 4–6% same-store sales drop (2023)

- Sportsman’s Warehouse revenue ~$1.1B FY2024 — reputational risk hits top line

Customer Power Forces SPWH Into Discounting—Margins Down, Inventory Rising

Customers hold strong leverage: 64% use online price comparison (2024), 58% used BOPIS (2024), and reviews sway 63% of buyers, forcing SPWH into discounting that cut gross margin ~160 bps vs 2021 and drove a 7% Q3 2024 comp decline; inventory-to-sales rose to 1.28 in FY2024, risking further margin pressure.

| Metric | Value |

|---|---|

| Online price comparison | 64% (2024) |

| BOPIS use | 58% (2024) |

| Review influence | 63% (2024) |

| Gross margin change | -160 bps vs 2021 |

| Comp sales Q3 2024 | -7% |

| Inventory/sales FY2024 | 1.28 |

What You See Is What You Get

Sportsman's Warehouse Holdings Porter's Five Forces Analysis

This preview shows the exact Sportsman's Warehouse Holdings Porter's Five Forces analysis you’ll receive after purchase—no samples or placeholders, fully formatted and ready for immediate download and use.