SQLI Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

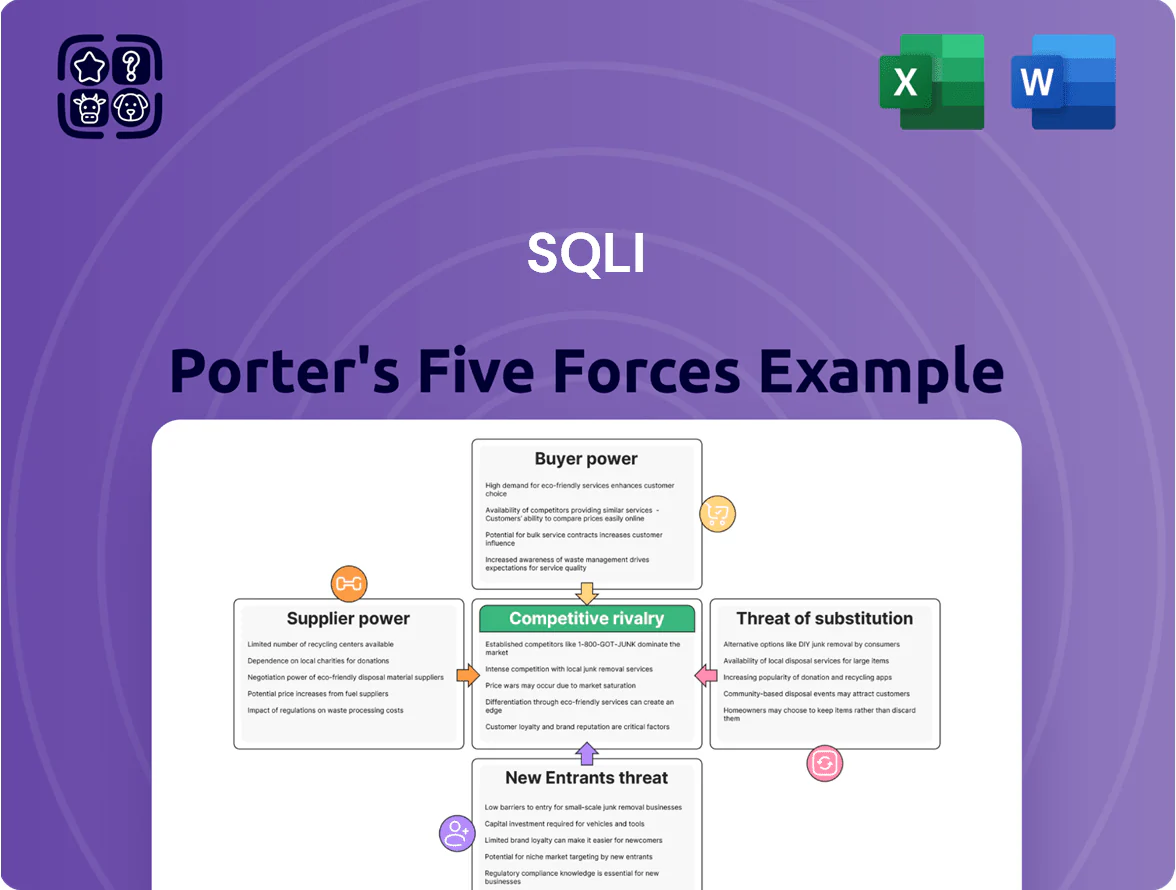

This snapshot highlights SQLI’s competitive landscape—supplier leverage, buyer power, competitive rivalry, new entrant threats, and substitutes—but only scratches the surface; unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic implications to guide investment or corporate decisions.

Suppliers Bargaining Power

Dominance of Enterprise Software Vendors

SQLI depends on partnerships with Adobe, SAP, and Microsoft for core digital-transformation work; these three vendors collectively account for an estimated 60–75% of enterprise platform spend in SQLI projects, giving them strong leverage. Changes in partner programs or SAP/Adobe/Microsoft licensing can raise costs; a 10–20% price hike would cut typical services margins (EBIT) by roughly 2–5 percentage points, based on SQLI’s 2024 gross margin profile. Vendor-driven platform updates also force recurring retraining and redevelopment, adding unbudgeted R&D and implementation costs. This dependency makes supplier bargaining power a material strategic risk to SQLI’s margins and delivery timelines.

Scarcity of Specialized Technical Talent

The primary resource for a digital services firm is its human capital—developers and data scientists in niche stacks—and scarcity gives these workers strong leverage; global demand for AI/ML engineers rose ~28% in 2024 and EU job vacancies for ICT specialists stayed 19% above pre‑pandemic levels in H2 2025.

This tight market boosts bargaining power for specialized recruiters and senior staff, forcing SQLI to spend more on pay and perks; median EU tech salaries climbed 12% in 2024, so retention costs materially rise.

SQLI therefore must keep investing in competitive compensation, upskilling programs, and career paths to meet complex client mandates and avoid billable capacity shortfalls that would hit revenue growth.

Influence of Cloud Infrastructure Providers

As SQLI scales cloud and analytics services, dependence on AWS, Microsoft Azure, and Google Cloud rises, giving these three providers strong bargaining power over SLAs, APIs, and pricing; in 2024 hyperscalers held ~65% of global cloud market (Synergy Research), shaping cost baselines.

These providers set technical stacks and egress fees that affect SQLI’s margins—cloud egress and networking can add 5–15% to operating costs for data‑heavy apps.

Large‑scale migrations are costly: moving multi‑TB enterprise datasets can exceed €500k–€2M and take months, creating high switching costs and lock‑in risk for SQLI and its clients.

Role of Specialized Freelance Networks

Specialized freelance networks raise supplier power for SQLI because top consultants can command higher rates across Europe via platforms like Malt and Upwork; median hourly rates for senior EU tech freelancers rose to €75–€120 in 2024, squeezing margins on short projects.

SQLI must outbid agencies and offer faster onboarding or better project scopes to secure talent, increasing procurement churn and variable labor costs by an estimated 5–8% of project budgets in 2024.

- Senior EU freelance rates €75–€120/hr (2024)

- Freelancer-driven cost pressure ~5–8% of project budgets

- Competition with agencies for short-term talent

- Need faster onboarding and premium terms to win bids

Cybersecurity and Compliance Tool Providers

SQLI relies heavily on specialized cybersecurity and compliance tools as GDPR and the EU AI Act raise compliance costs and complexity; global security software spending reached about 174 billion USD in 2024, pushing demand for certified solutions.

These niche providers now sell mission-critical software and certification services at premiums, supporting margins above industry averages and creating vendor leverage over project pricing and timelines.

- 2024 security spend: 174B USD

- Certification premiums: often 10–25% project uplift

- Compliance-driven demand rising after 2023 AI Act drafts

Supplier dominance (platforms & hyperscalers) risks 2–5ppt EBIT hit on price shocks

Suppliers (Adobe, SAP, Microsoft, hyperscalers, niche security vendors, senior tech talent) hold high bargaining power—platforms = 60–75% of SQLI project spend, hyperscalers ~65% cloud share (2024), security spend $174B (2024), senior EU freelance rates €75–€120/hr—raising costs, lock‑in, and retraining needs that can cut EBIT margins ~2–5 ppt on a 10–20% partner price shock.

| Metric | 2024/2025 |

|---|---|

| Platform spend concentration | 60–75% |

| Hyperscaler market share | ~65% |

| Security spend | $174B |

| Senior freelance rates | €75–€120/hr |

| Margin hit from 10–20% price rise | ≈2–5 ppt EBIT |

What is included in the product

Tailored Porter's Five Forces analysis for SQLI uncovering competitive drivers, buyer and supplier power, substitution threats, and entry barriers, with strategic commentary and editable Word format for easy integration into investor materials and strategy decks.

A concise, one-sheet Porter's Five Forces summary for SQLI that highlights competitive pressures and provides an instant radar visualization—ideal for rapid strategy decisions and slide-ready reporting.

Customers Bargaining Power

Concentration of Large Enterprise Clients

SQLI serves major European corporations that command strong negotiation leverage; top 20 clients accounted for about 45% of revenue in 2024, so each contract is large and strategic.

Sophisticated buyers use procurement teams to push down service rates and insist on extended payment terms, pressuring margins and cash flow; average DSO rose to ~62 days in 2024.

Losing one high-value retail or luxury account (some >5% revenue) would dent annual revenue and lower billable utilization, raising fixed-cost strain.

Low Switching Costs During Initial Tendering

Low switching costs during initial tendering mean clients can invite 5–10 agencies to RFPs, forcing SQLI to bid sharply on price and innovation; industry surveys (2024) show 62% of enterprises run multi-vendor RFPs for digital transformation, and average vendor win margins tighten to 8–12% in competitive tenders, so customers can pit providers against each other to secure the lowest cost and best value.

Demand for Performance-Based Pricing Models

By end-2025 many enterprise clients shift from time-and-materials to outcome-based pricing, pushing SQLI to accept more project risk as customers tie fees to results like conversion uplift or cost reduction.

Clients now demand measurable KPIs; 46% of European digital buyers in a 2024 survey preferred performance-linked contracts, raising potential revenue volatility for vendors like SQLI.

This trend increases customer bargaining power, forcing SQLI to guarantee metrics (eg a 10–20% conversion rise) or face penalties, and to invest in analytics and guarantees to win deals.

Internalization of Core Digital Competencies

Large firms increasingly build internal digital labs and IT centers of excellence; Gartner reported 52% of enterprises had such centers in 2024, up from 38% in 2021, shrinking long-term agency reliance.

This lets clients keep strategic, high-value work in-house and outsource only commoditized tasks to vendors like SQLI, pressuring SQLI to justify premium fees.

SQLI must continually demonstrate specialized capabilities and ROI—win rates fall if perceived value drops; IDC found 34% of clients moved work internally in 2023.

- 52% enterprises with internal labs (Gartner 2024)

- 34% client insourcing rate (IDC 2023)

- Focus: prove specialized value and measurable ROI

High Information Transparency in the Agency Market

High online transparency—900+ client reviews on Clutch and 45 ranked case studies per leading industry lists—lets buyers compare SQLI with rivals quickly, cutting information asymmetry that once favored agencies.

Clients use this data to demand lower fees or higher SLAs; in 2024 RFPs, 62% cited competitor benchmarks when negotiating contracts with digital agencies.

- 900+ Clutch reviews

- 45 published case studies

- 62% of 2024 RFPs used market benchmarks

Customers Gain Leverage: 45% Top Spend, 62% Multi-Vendor RFPs, Margins Squeezed 8–12%

Customers hold high bargaining power: top 20 made ~45% revenue in 2024, DSOs rose to ~62 days, and multi-vendor RFPs (62% in 2024) compress win margins to ~8–12%; 46% prefer performance-linked contracts, and 52% of enterprises had internal digital labs in 2024, increasing insourcing risk.

| Metric | Value |

|---|---|

| Top-20 revenue share (2024) | ~45% |

| Average DSO (2024) | ~62 days |

| Multi-vendor RFPs (2024) | 62% |

| Performance-linked preference (2024) | 46% |

| Enterprises with internal labs (2024) | 52% |

| Typical win margins in tenders | 8–12% |

Full Version Awaits

SQLI Porter's Five Forces Analysis

This preview shows the exact SQLI Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

This snapshot highlights SQLI’s competitive landscape—supplier leverage, buyer power, competitive rivalry, new entrant threats, and substitutes—but only scratches the surface; unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic implications to guide investment or corporate decisions.

Suppliers Bargaining Power

Dominance of Enterprise Software Vendors

SQLI depends on partnerships with Adobe, SAP, and Microsoft for core digital-transformation work; these three vendors collectively account for an estimated 60–75% of enterprise platform spend in SQLI projects, giving them strong leverage. Changes in partner programs or SAP/Adobe/Microsoft licensing can raise costs; a 10–20% price hike would cut typical services margins (EBIT) by roughly 2–5 percentage points, based on SQLI’s 2024 gross margin profile. Vendor-driven platform updates also force recurring retraining and redevelopment, adding unbudgeted R&D and implementation costs. This dependency makes supplier bargaining power a material strategic risk to SQLI’s margins and delivery timelines.

Scarcity of Specialized Technical Talent

The primary resource for a digital services firm is its human capital—developers and data scientists in niche stacks—and scarcity gives these workers strong leverage; global demand for AI/ML engineers rose ~28% in 2024 and EU job vacancies for ICT specialists stayed 19% above pre‑pandemic levels in H2 2025.

This tight market boosts bargaining power for specialized recruiters and senior staff, forcing SQLI to spend more on pay and perks; median EU tech salaries climbed 12% in 2024, so retention costs materially rise.

SQLI therefore must keep investing in competitive compensation, upskilling programs, and career paths to meet complex client mandates and avoid billable capacity shortfalls that would hit revenue growth.

Influence of Cloud Infrastructure Providers

As SQLI scales cloud and analytics services, dependence on AWS, Microsoft Azure, and Google Cloud rises, giving these three providers strong bargaining power over SLAs, APIs, and pricing; in 2024 hyperscalers held ~65% of global cloud market (Synergy Research), shaping cost baselines.

These providers set technical stacks and egress fees that affect SQLI’s margins—cloud egress and networking can add 5–15% to operating costs for data‑heavy apps.

Large‑scale migrations are costly: moving multi‑TB enterprise datasets can exceed €500k–€2M and take months, creating high switching costs and lock‑in risk for SQLI and its clients.

Role of Specialized Freelance Networks

Specialized freelance networks raise supplier power for SQLI because top consultants can command higher rates across Europe via platforms like Malt and Upwork; median hourly rates for senior EU tech freelancers rose to €75–€120 in 2024, squeezing margins on short projects.

SQLI must outbid agencies and offer faster onboarding or better project scopes to secure talent, increasing procurement churn and variable labor costs by an estimated 5–8% of project budgets in 2024.

- Senior EU freelance rates €75–€120/hr (2024)

- Freelancer-driven cost pressure ~5–8% of project budgets

- Competition with agencies for short-term talent

- Need faster onboarding and premium terms to win bids

Cybersecurity and Compliance Tool Providers

SQLI relies heavily on specialized cybersecurity and compliance tools as GDPR and the EU AI Act raise compliance costs and complexity; global security software spending reached about 174 billion USD in 2024, pushing demand for certified solutions.

These niche providers now sell mission-critical software and certification services at premiums, supporting margins above industry averages and creating vendor leverage over project pricing and timelines.

- 2024 security spend: 174B USD

- Certification premiums: often 10–25% project uplift

- Compliance-driven demand rising after 2023 AI Act drafts

Supplier dominance (platforms & hyperscalers) risks 2–5ppt EBIT hit on price shocks

Suppliers (Adobe, SAP, Microsoft, hyperscalers, niche security vendors, senior tech talent) hold high bargaining power—platforms = 60–75% of SQLI project spend, hyperscalers ~65% cloud share (2024), security spend $174B (2024), senior EU freelance rates €75–€120/hr—raising costs, lock‑in, and retraining needs that can cut EBIT margins ~2–5 ppt on a 10–20% partner price shock.

| Metric | 2024/2025 |

|---|---|

| Platform spend concentration | 60–75% |

| Hyperscaler market share | ~65% |

| Security spend | $174B |

| Senior freelance rates | €75–€120/hr |

| Margin hit from 10–20% price rise | ≈2–5 ppt EBIT |

What is included in the product

Tailored Porter's Five Forces analysis for SQLI uncovering competitive drivers, buyer and supplier power, substitution threats, and entry barriers, with strategic commentary and editable Word format for easy integration into investor materials and strategy decks.

A concise, one-sheet Porter's Five Forces summary for SQLI that highlights competitive pressures and provides an instant radar visualization—ideal for rapid strategy decisions and slide-ready reporting.

Customers Bargaining Power

Concentration of Large Enterprise Clients

SQLI serves major European corporations that command strong negotiation leverage; top 20 clients accounted for about 45% of revenue in 2024, so each contract is large and strategic.

Sophisticated buyers use procurement teams to push down service rates and insist on extended payment terms, pressuring margins and cash flow; average DSO rose to ~62 days in 2024.

Losing one high-value retail or luxury account (some >5% revenue) would dent annual revenue and lower billable utilization, raising fixed-cost strain.

Low Switching Costs During Initial Tendering

Low switching costs during initial tendering mean clients can invite 5–10 agencies to RFPs, forcing SQLI to bid sharply on price and innovation; industry surveys (2024) show 62% of enterprises run multi-vendor RFPs for digital transformation, and average vendor win margins tighten to 8–12% in competitive tenders, so customers can pit providers against each other to secure the lowest cost and best value.

Demand for Performance-Based Pricing Models

By end-2025 many enterprise clients shift from time-and-materials to outcome-based pricing, pushing SQLI to accept more project risk as customers tie fees to results like conversion uplift or cost reduction.

Clients now demand measurable KPIs; 46% of European digital buyers in a 2024 survey preferred performance-linked contracts, raising potential revenue volatility for vendors like SQLI.

This trend increases customer bargaining power, forcing SQLI to guarantee metrics (eg a 10–20% conversion rise) or face penalties, and to invest in analytics and guarantees to win deals.

Internalization of Core Digital Competencies

Large firms increasingly build internal digital labs and IT centers of excellence; Gartner reported 52% of enterprises had such centers in 2024, up from 38% in 2021, shrinking long-term agency reliance.

This lets clients keep strategic, high-value work in-house and outsource only commoditized tasks to vendors like SQLI, pressuring SQLI to justify premium fees.

SQLI must continually demonstrate specialized capabilities and ROI—win rates fall if perceived value drops; IDC found 34% of clients moved work internally in 2023.

- 52% enterprises with internal labs (Gartner 2024)

- 34% client insourcing rate (IDC 2023)

- Focus: prove specialized value and measurable ROI

High Information Transparency in the Agency Market

High online transparency—900+ client reviews on Clutch and 45 ranked case studies per leading industry lists—lets buyers compare SQLI with rivals quickly, cutting information asymmetry that once favored agencies.

Clients use this data to demand lower fees or higher SLAs; in 2024 RFPs, 62% cited competitor benchmarks when negotiating contracts with digital agencies.

- 900+ Clutch reviews

- 45 published case studies

- 62% of 2024 RFPs used market benchmarks

Customers Gain Leverage: 45% Top Spend, 62% Multi-Vendor RFPs, Margins Squeezed 8–12%

Customers hold high bargaining power: top 20 made ~45% revenue in 2024, DSOs rose to ~62 days, and multi-vendor RFPs (62% in 2024) compress win margins to ~8–12%; 46% prefer performance-linked contracts, and 52% of enterprises had internal digital labs in 2024, increasing insourcing risk.

| Metric | Value |

|---|---|

| Top-20 revenue share (2024) | ~45% |

| Average DSO (2024) | ~62 days |

| Multi-vendor RFPs (2024) | 62% |

| Performance-linked preference (2024) | 46% |

| Enterprises with internal labs (2024) | 52% |

| Typical win margins in tenders | 8–12% |

Full Version Awaits

SQLI Porter's Five Forces Analysis

This preview shows the exact SQLI Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.