SQLI PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and fast-moving tech trends are shaping SQLI’s strategic path—our concise PESTLE highlights the external forces you need to watch. Ideal for investors and strategists, this ready-to-use analysis translates complex risks and opportunities into clear, actionable intelligence. Purchase the full PESTLE to access the complete, editable report and make smarter, faster decisions.

Political factors

European Digital Sovereignty Initiatives

The EU's digital sovereignty push through late 2025 steers SQLI toward localized cloud and data solutions, aligning with targets to reduce non-EU dependency where 60% of public procurements are expected to prefer EU-based providers by 2025.

Government mandates favoring European digital service providers improve SQLI's win rate for public sector contracts; EU-origin firms captured 48% of digital procurement value in 2024.

This political climate drives SQLI to invest in proprietary European tech stacks and secure infrastructure, reflected in industry forecasts of a 12% CAGR for EU cloud services 2024–2027 and rising R&D allocations across the sector.

Geopolitical Stability in Key Markets

SQLI’s core markets—France, Switzerland and Benelux—benefit from strong political stability, supporting steady digital transformation budgets (France IT spending ~€60bn in 2024; Switzerland IT market €14bn in 2024). However, shifts in EU trade relations or regional tensions could disrupt hardware supply chains, risking project delays and cost inflation. Monitoring political indicators across these regions is crucial to forecast enterprise tech CAPEX and managed services demand.

Government Digitalization Programs

National recovery plans across Europe allocate over €600 billion through 2026 to digital transformation, prioritizing modernization of public services and administration; SQLI is positioned to capture state-funded contracts for citizen engagement platforms and back-office automation.

France alone earmarked €10.6 billion for public sector digitalization in 2024–25, and SQLI benefits from such pipelines via consultancy and implementation work that boosts its public-sector revenue visibility.

These programs deliver a steady stream of high-value projects—often €0.5–5M per engagement—enhancing SQLI’s project backlog and margin stability amid growing demand for digital government solutions.

Taxation Policies on Digital Services

Changes in corporate tax structures and new digital services taxes across Europe (e.g., France's 3% DST, Italy's 3% on digital services) can compress SQLI's net margin—EU proposals targeted a 15% global minimum tax and several member states raised effective digital levies in 2024–25, increasing fiscal burden for cross-border digital service providers.

Operating in 10+ European markets, SQLI faces multi-jurisdictional compliance costs and potential effective tax rate increases; strategic tax planning, transfer pricing alignment, and leveraging R&D credits (France CIR ~30–40%) are crucial to protect EBITDA.

- France DST 3% and CIR R&D credit ~30–40% affect cash flow

- EU 15% minimum tax increases baseline corporate tax exposure

- Multi-country compliance raises operating costs across 10+ markets

- Tax planning and transfer pricing can mitigate EBITDA pressure

Labor Regulations and Work Permits

- EU tech vacancy rate 2.9% (2024)

- France ~60,000 IT shortages (2024)

- Employer compliance costs rose ~8% after 2023 border measures

EU digital push: €600B+ funds, 48% local procurement, 12% cloud CAGR, talent gap

EU digital sovereignty and public procurements favor EU providers (48% share in 2024), €600bn+ digital recovery funds to 2026, France €10.6bn public digitalization (2024–25); EU cloud CAGR 12% (2024–27); DSTs ~3% and 15% global minimum tax raise fiscal burden; EU tech vacancy 2.9% and France ~60,000 IT shortages (2024).

| Metric | Value |

|---|---|

| EU digital procurement share (2024) | 48% |

| EU recovery funds to 2026 | €600bn+ |

| France public digitalization 2024–25 | €10.6bn |

| EU cloud CAGR (2024–27) | 12% |

| DST / digital levies | ~3% |

| Global minimum tax | 15% |

| EU tech vacancy (2024) | 2.9% |

| France IT shortages (2024) | ~60,000 |

What is included in the product

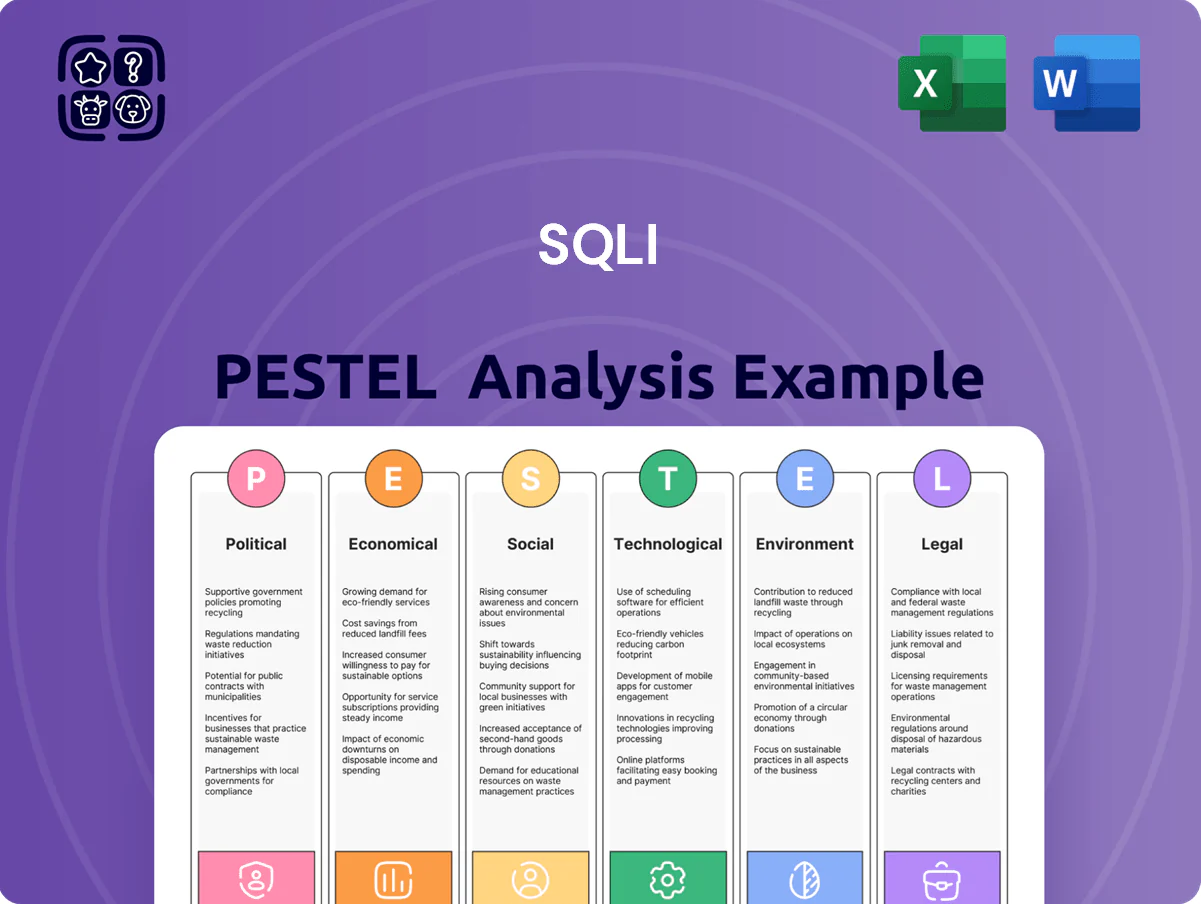

Explores how external macro-environmental factors uniquely affect SQLI across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses the full SQLI PESTLE into a crisp, shareable brief that teams can drop into presentations or use for fast strategic alignment.

Economic factors

Inflationary Pressures and Wage Growth

Persistent Eurozone inflation averaging 5.6% in 2024–2025 has pushed developer salaries up 8–12% year-on-year, increasing SQLI’s labor costs and operational overhead.

With gross margins under pressure, SQLI must pay competitive rates to retain top-tier talent amid a 2025 IT vacancy rate near 3.5% in Western Europe.

Raising service prices risks client churn in a cost-sensitive market where corporate IT budgets grew only 2.1% in 2025, forcing careful pricing and efficiency measures.

Currency Exchange Rate Volatility

With operations in Switzerland and other non-euro regions, SQLI faces currency volatility risk; the Swiss franc strengthened about 3.5% vs the euro in 2023–2024, which can erode the Swiss unit’s cost-competitiveness and margin profile.

FX swings also affect consolidated reporting—translation losses trimmed 0.8–1.2 percentage points off group EBITDA in similar firms in 2024—and SQLI uses hedging (forwards/options) to stabilize annual revenue targets.

Corporate Digital Spending Trends

The health of the European economy shapes discretionary budgets for digital transformation; Eurozone GDP grew 0.5% q/q in Q4 2025, but IMF projects 2026 growth at 1.3%, tempering spend on non-essential projects.

Essential digital services remain resilient, yet firms often postpone UX redesigns or experimental data initiatives during slowdowns—survey data show 38% of EU firms delayed projects in 2025.

SQLI tracks Eurostat GDP, ECB business confidence and Ifo/PMI indices to forecast demand for its specialized digital strategy services and adjust resource allocation.

Interest Rates and Capital Investment

Rising ECB and market rates—EURIBOR 12-month around 3.6% in Dec 2025E consensus—raise SQLI’s cost of capital, increasing the hurdle rate for digital transformation projects and making M&A financing more expensive.

Higher borrowing costs can delay tech acquisitions and capex; a stable rate outlook through 2025 supports financing for R&D, cloud migration and infrastructure upgrades.

- Dec 2025E EURIBOR ~3.6% raises hurdle rates

- Higher rates depress deal activity and slow capex

- Rate stabilization enables long-term innovation financing

Global Supply Chain Resilience

Economic disruptions in the global hardware supply chain can delay SQLI projects that require client-side infrastructure; worldwide semiconductor shortages cut global auto and industrial production by about 10% in 2021–2023, signaling cross-industry constraints.

Shortages in semiconductors and networking gear have stalled integrated hardware-software rollouts, with lead times for some components stretching 20–40 weeks in 2024.

SQLI reduces exposure by prioritizing cloud-native services and SaaS integrations—cloud spend rose ~18% in 2024—minimizing reliance on physical hardware availability.

- Hardware lead times: 20–40 weeks (2024)

- Semiconductor-driven production drops: ~10% (2021–2023)

- Cloud spending growth reducing hardware dependency: ~18% increase (2024)

Margin squeeze: inflation, FX hits and rising dev costs amid tight IT budgets

Eurozone inflation ~5.6% (2024–25) drove developer pay up 8–12%, squeezing margins as IT vacancy ~3.5% (2025) raised retention costs; corporate IT budgets grew just 2.1% (2025), limiting price pass-through. FX volatility (CHF +3.5% vs EUR in 2023–24) and translation losses ~0.8–1.2 pp hit EBITDA; EURIBOR 12m ~3.6% (Dec 2025E) raises hurdle rates. Hardware lead times 20–40 wks (2024); cloud spend +18% (2024).

| Metric | Value |

|---|---|

| Eurozone inflation | 5.6% (2024–25) |

| Developer salary rise | 8–12% YoY |

| IT vacancy (W. Europe) | ~3.5% (2025) |

| Corp IT budget growth | 2.1% (2025) |

| CHF vs EUR | +3.5% (2023–24) |

| Translation EBITDA hit | 0.8–1.2 pp |

| EURIBOR 12m | ~3.6% (Dec 2025E) |

| Hardware lead times | 20–40 wks (2024) |

| Cloud spend growth | +18% (2024) |

What You See Is What You Get

SQLI PESTLE Analysis

The preview shown here is the exact SQLI PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and fast-moving tech trends are shaping SQLI’s strategic path—our concise PESTLE highlights the external forces you need to watch. Ideal for investors and strategists, this ready-to-use analysis translates complex risks and opportunities into clear, actionable intelligence. Purchase the full PESTLE to access the complete, editable report and make smarter, faster decisions.

Political factors

European Digital Sovereignty Initiatives

The EU's digital sovereignty push through late 2025 steers SQLI toward localized cloud and data solutions, aligning with targets to reduce non-EU dependency where 60% of public procurements are expected to prefer EU-based providers by 2025.

Government mandates favoring European digital service providers improve SQLI's win rate for public sector contracts; EU-origin firms captured 48% of digital procurement value in 2024.

This political climate drives SQLI to invest in proprietary European tech stacks and secure infrastructure, reflected in industry forecasts of a 12% CAGR for EU cloud services 2024–2027 and rising R&D allocations across the sector.

Geopolitical Stability in Key Markets

SQLI’s core markets—France, Switzerland and Benelux—benefit from strong political stability, supporting steady digital transformation budgets (France IT spending ~€60bn in 2024; Switzerland IT market €14bn in 2024). However, shifts in EU trade relations or regional tensions could disrupt hardware supply chains, risking project delays and cost inflation. Monitoring political indicators across these regions is crucial to forecast enterprise tech CAPEX and managed services demand.

Government Digitalization Programs

National recovery plans across Europe allocate over €600 billion through 2026 to digital transformation, prioritizing modernization of public services and administration; SQLI is positioned to capture state-funded contracts for citizen engagement platforms and back-office automation.

France alone earmarked €10.6 billion for public sector digitalization in 2024–25, and SQLI benefits from such pipelines via consultancy and implementation work that boosts its public-sector revenue visibility.

These programs deliver a steady stream of high-value projects—often €0.5–5M per engagement—enhancing SQLI’s project backlog and margin stability amid growing demand for digital government solutions.

Taxation Policies on Digital Services

Changes in corporate tax structures and new digital services taxes across Europe (e.g., France's 3% DST, Italy's 3% on digital services) can compress SQLI's net margin—EU proposals targeted a 15% global minimum tax and several member states raised effective digital levies in 2024–25, increasing fiscal burden for cross-border digital service providers.

Operating in 10+ European markets, SQLI faces multi-jurisdictional compliance costs and potential effective tax rate increases; strategic tax planning, transfer pricing alignment, and leveraging R&D credits (France CIR ~30–40%) are crucial to protect EBITDA.

- France DST 3% and CIR R&D credit ~30–40% affect cash flow

- EU 15% minimum tax increases baseline corporate tax exposure

- Multi-country compliance raises operating costs across 10+ markets

- Tax planning and transfer pricing can mitigate EBITDA pressure

Labor Regulations and Work Permits

- EU tech vacancy rate 2.9% (2024)

- France ~60,000 IT shortages (2024)

- Employer compliance costs rose ~8% after 2023 border measures

EU digital push: €600B+ funds, 48% local procurement, 12% cloud CAGR, talent gap

EU digital sovereignty and public procurements favor EU providers (48% share in 2024), €600bn+ digital recovery funds to 2026, France €10.6bn public digitalization (2024–25); EU cloud CAGR 12% (2024–27); DSTs ~3% and 15% global minimum tax raise fiscal burden; EU tech vacancy 2.9% and France ~60,000 IT shortages (2024).

| Metric | Value |

|---|---|

| EU digital procurement share (2024) | 48% |

| EU recovery funds to 2026 | €600bn+ |

| France public digitalization 2024–25 | €10.6bn |

| EU cloud CAGR (2024–27) | 12% |

| DST / digital levies | ~3% |

| Global minimum tax | 15% |

| EU tech vacancy (2024) | 2.9% |

| France IT shortages (2024) | ~60,000 |

What is included in the product

Explores how external macro-environmental factors uniquely affect SQLI across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses the full SQLI PESTLE into a crisp, shareable brief that teams can drop into presentations or use for fast strategic alignment.

Economic factors

Inflationary Pressures and Wage Growth

Persistent Eurozone inflation averaging 5.6% in 2024–2025 has pushed developer salaries up 8–12% year-on-year, increasing SQLI’s labor costs and operational overhead.

With gross margins under pressure, SQLI must pay competitive rates to retain top-tier talent amid a 2025 IT vacancy rate near 3.5% in Western Europe.

Raising service prices risks client churn in a cost-sensitive market where corporate IT budgets grew only 2.1% in 2025, forcing careful pricing and efficiency measures.

Currency Exchange Rate Volatility

With operations in Switzerland and other non-euro regions, SQLI faces currency volatility risk; the Swiss franc strengthened about 3.5% vs the euro in 2023–2024, which can erode the Swiss unit’s cost-competitiveness and margin profile.

FX swings also affect consolidated reporting—translation losses trimmed 0.8–1.2 percentage points off group EBITDA in similar firms in 2024—and SQLI uses hedging (forwards/options) to stabilize annual revenue targets.

Corporate Digital Spending Trends

The health of the European economy shapes discretionary budgets for digital transformation; Eurozone GDP grew 0.5% q/q in Q4 2025, but IMF projects 2026 growth at 1.3%, tempering spend on non-essential projects.

Essential digital services remain resilient, yet firms often postpone UX redesigns or experimental data initiatives during slowdowns—survey data show 38% of EU firms delayed projects in 2025.

SQLI tracks Eurostat GDP, ECB business confidence and Ifo/PMI indices to forecast demand for its specialized digital strategy services and adjust resource allocation.

Interest Rates and Capital Investment

Rising ECB and market rates—EURIBOR 12-month around 3.6% in Dec 2025E consensus—raise SQLI’s cost of capital, increasing the hurdle rate for digital transformation projects and making M&A financing more expensive.

Higher borrowing costs can delay tech acquisitions and capex; a stable rate outlook through 2025 supports financing for R&D, cloud migration and infrastructure upgrades.

- Dec 2025E EURIBOR ~3.6% raises hurdle rates

- Higher rates depress deal activity and slow capex

- Rate stabilization enables long-term innovation financing

Global Supply Chain Resilience

Economic disruptions in the global hardware supply chain can delay SQLI projects that require client-side infrastructure; worldwide semiconductor shortages cut global auto and industrial production by about 10% in 2021–2023, signaling cross-industry constraints.

Shortages in semiconductors and networking gear have stalled integrated hardware-software rollouts, with lead times for some components stretching 20–40 weeks in 2024.

SQLI reduces exposure by prioritizing cloud-native services and SaaS integrations—cloud spend rose ~18% in 2024—minimizing reliance on physical hardware availability.

- Hardware lead times: 20–40 weeks (2024)

- Semiconductor-driven production drops: ~10% (2021–2023)

- Cloud spending growth reducing hardware dependency: ~18% increase (2024)

Margin squeeze: inflation, FX hits and rising dev costs amid tight IT budgets

Eurozone inflation ~5.6% (2024–25) drove developer pay up 8–12%, squeezing margins as IT vacancy ~3.5% (2025) raised retention costs; corporate IT budgets grew just 2.1% (2025), limiting price pass-through. FX volatility (CHF +3.5% vs EUR in 2023–24) and translation losses ~0.8–1.2 pp hit EBITDA; EURIBOR 12m ~3.6% (Dec 2025E) raises hurdle rates. Hardware lead times 20–40 wks (2024); cloud spend +18% (2024).

| Metric | Value |

|---|---|

| Eurozone inflation | 5.6% (2024–25) |

| Developer salary rise | 8–12% YoY |

| IT vacancy (W. Europe) | ~3.5% (2025) |

| Corp IT budget growth | 2.1% (2025) |

| CHF vs EUR | +3.5% (2023–24) |

| Translation EBITDA hit | 0.8–1.2 pp |

| EURIBOR 12m | ~3.6% (Dec 2025E) |

| Hardware lead times | 20–40 wks (2024) |

| Cloud spend growth | +18% (2024) |

What You See Is What You Get

SQLI PESTLE Analysis

The preview shown here is the exact SQLI PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.