SSAB PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and sustainability trends are reshaping SSAB’s strategic outlook—our concise PESTLE snapshot highlights the external forces that matter most to investors and strategists; purchase the full PESTLE for a complete, actionable briefing you can use today.

Political factors

Geopolitical Trade Policies

Geopolitical trade policies shape SSAB’s margins as tariffs and quotas alter flows of iron ore and finished steel; 2024 US Section 232 and EU safeguard reviews risk raising costs after EU steel imports fell 12% YoY in 2023.

Government Subsidies for Green Transition

Sweden and Finland have allocated over SEK 20 billion (≈EUR 1.8bn) combined since 2020 for industrial decarbonization and pilot projects; SSAB depends on these subsidies to underwrite the ~SEK 40–50 billion investments projected for fossil-free HYBRIT facilities. Continued political backing—including Sweden’s 2024 extension of hydrogen and CCS incentives and Finland’s €200m green steel grants—remains critical to SSAB’s cost-competitiveness and scale-up timing.

Energy Sovereignty and Infrastructure

Political decisions on national grids and renewable expansion directly affect SSAB, which announced a target to reach fossil-free steel by 2045 and needs roughly 6–8 TWh/year of renewable power for planned electric arc furnace rollouts; state energy policies determine grid access and tariffs. Delays in permits or instability in Sweden, Finland, or the US risk pushing project timelines and capital deployment, with infrastructure bottlenecks potentially increasing costs beyond SSAB’s reported 2024 capex guidance of ~SEK 6–8 billion.

Defense Spending and Procurement

Rising defense budgets—EU planned defense spending up ~8% in 2024 and US defense budget at $858B for FY2024—boost demand for SSABs high-strength steels for armoured vehicles and infrastructure.

SSAB, with specialty grades and ~SEK 77.8bn revenue in 2023, gains from geopolitical tensions that increase state procurement.

Alignment with NATO and allies secures recurring high-value contracts and supports order visibility for SSABs advanced steel offerings.

- EU defense +8% (2024), US $858B (FY2024)

- SSAB revenue SEK 77.8bn (2023)

- NATO alignment → steady gov contracts

Regulatory Stability in the US Market

SSAB's large US footprint—roughly 28% of 2024 group sales—makes it highly exposed to shifts in American industrial policy and federal politics, where changes in administrations can alter emissions rules or infrastructure funding such as IRA allocations that directed $369bn nationwide by 2024.

Maintaining robust government relations is critical to keep US scrap-metal and minimill operations compliant and profitable amid potential regulatory tightening and subsidy shifts.

- 28% of 2024 sales from US

- IRA and related programs allocated $369bn by 2024

- Regulatory shifts risk operational and compliance cost volatility

SSAB margins hinge on trade, subsidies & HYBRIT funding as US exposure rises

Trade measures, subsidies and energy policy drive SSAB’s margins and project timing: 2024 EU/US steel reviews, SEK 20bn+ Sweden/Finland decarbonization support vs SEK 40–50bn HYBRIT need, ~6–8 TWh/yr renewable demand, SEK 77.8bn revenue (2023), 28% sales US exposure, EU defense +8% (2024), US $858bn FY2024.

| Metric | Value |

|---|---|

| Revenue (2023) | SEK 77.8bn |

| US share (2024) | 28% |

| HYBRIT capex need | SEK 40–50bn |

| Sweden/Finland support | SEK 20bn+ |

What is included in the product

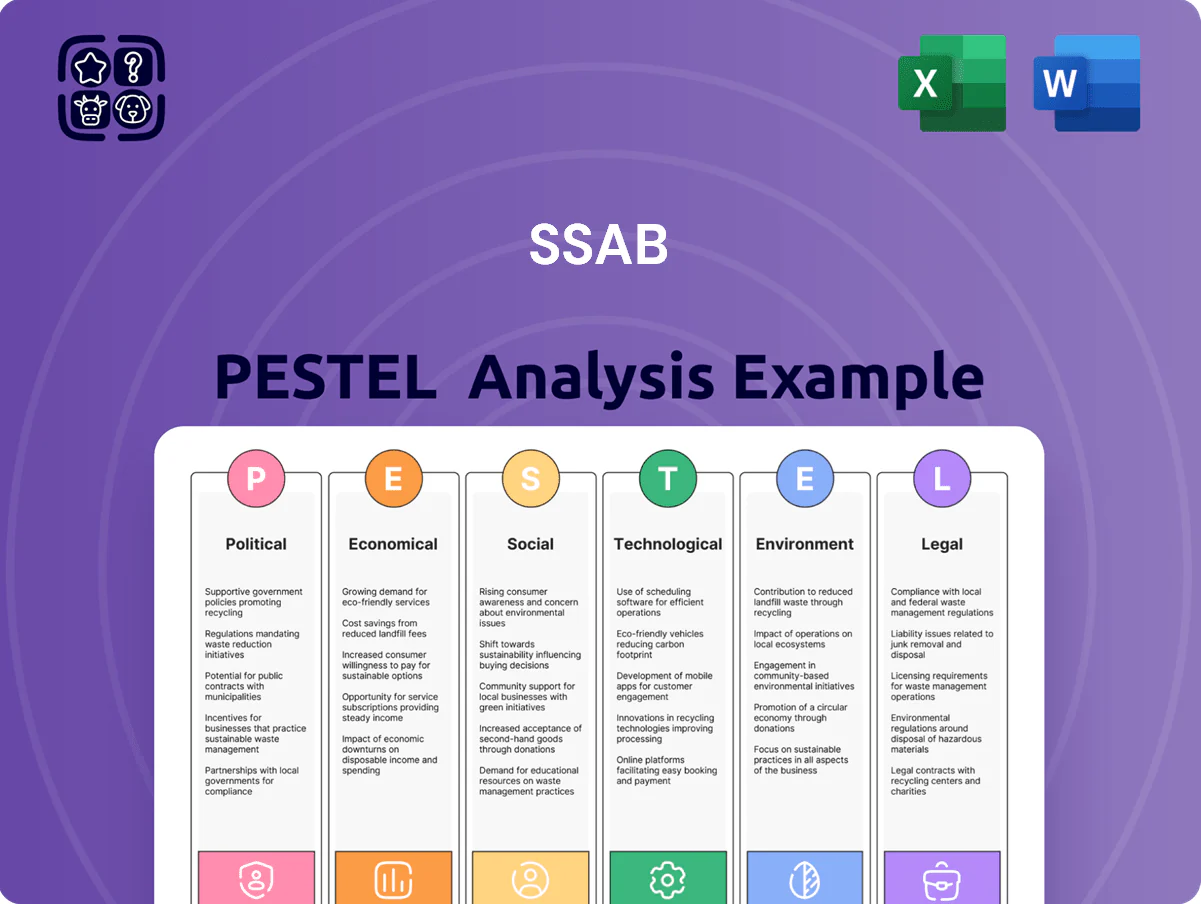

Explores how external macro-environmental factors uniquely affect SSAB across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, visually segmented PESTLE summary for SSAB that simplifies external risk assessment and market positioning, ready to drop into presentations or share across teams for fast alignment.

Economic factors

Global Steel Demand Cycles

The demand for SSAB’s steels is highly cyclical and tied to construction, automotive and heavy transport; global steel consumption fell 2.3% in 2023 but recovered with a 1.8% rise in 2024, while world GDP grew 3.1% in 2024—slower growth or higher interest rates can cut infrastructure spending and auto production, hitting volumes and ASPs. Monitoring OECD industrial production and IMF GDP forecasts is essential for near‑term revenue visibility.

Raw Material and Energy Costs

Fluctuations in iron ore, coking coal and electricity drive SSABs COGS; iron ore spot rose ~18% YoY in 2024 while EU industrial electricity prices averaged ~€120/MWh in 2024, amplifying cost pressure. SSAB’s HYBRIT shift to fossil-free steel reduces long-term exposure, but in 2024 ~70% of steelmaking still tied to traditional inputs, leaving margins vulnerable. The company uses hedges and passed through some costs, yet sustained high input prices risk compressing EBITDA if not fully recovered from customers.

Currency Exchange Rate Volatility

As SSAB reports in SEK while earning significant revenues in USD and EUR, 2024 FX moves mattered: the SEK weakened ~6% vs USD and ~4% vs EUR, amplifying translation gains but squeezing export competitiveness; a 10% USD/SEK swing can alter reported operating profit by several hundred million SEK given 2023 revenue mix (~40% Americas, ~30% Europe). Financial analysts must hedge and model FX impacts on consolidated statements and asset valuations.

Inflationary Pressures on Capital Expenditure

- Estimated investment need: SEK 100–150bn

- Input/wage inflation 2023–24: ~6–9% y/y

- Real rates ~1.5% (Sweden, 2024) raising financing costs

Scrap Metal Market Dynamics

SSAB’s US EAF operations depend on high-quality scrap; US scrap prices averaged about $380–$420/ton in 2024, driven by strong domestic demand and tighter global flows after Indonesia and Turkey tightened exports.

Global recycling growth and export restrictions reduced available scrap exports by an estimated 8–12% in 2023–24, raising procurement costs; rising EAF adoption pushed feeder competition, with steelmakers increasing scrap purchases ~6–9% YoY.

- US scrap price range 2024: $380–$420/ton

- Export supply reduction 2023–24: ~8–12%

- Increased scrap demand YoY: ~6–9%

- Higher procurement risk for SSAB’s margins

SSAB Outlook: Rising costs, weak SEK and modest demand lift margins pressure in 2024

Economic cycles, input-price swings and FX materially affect SSAB: 2024 steel demand +1.8%, world GDP +3.1%; iron ore +18% YoY; EU industrial power ~€120/MWh; SEK -6% vs USD, -4% vs EUR; estimated transition capex SEK 100–150bn; Swedish real rate ~1.5%; US scrap $380–420/t; scrap export reduction ~8–12%.

| Metric | 2024 / 2023–24 |

|---|---|

| World GDP growth | 3.1% (2024) |

| Steel demand | +1.8% (2024) |

| Iron ore | +18% YoY (2024) |

| EU power price | ~€120/MWh (2024) |

| SEK vs USD / EUR | -6% / -4% (2024) |

| Transition capex | SEK 100–150bn (2030 target) |

| Swedish real rate | ~1.5% (2024) |

| US scrap | $380–420/ton (2024) |

| Scrap export cut | ~8–12% (2023–24) |

Preview Before You Purchase

SSAB PESTLE Analysis

The preview shown here is the exact SSAB PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and sustainability trends are reshaping SSAB’s strategic outlook—our concise PESTLE snapshot highlights the external forces that matter most to investors and strategists; purchase the full PESTLE for a complete, actionable briefing you can use today.

Political factors

Geopolitical Trade Policies

Geopolitical trade policies shape SSAB’s margins as tariffs and quotas alter flows of iron ore and finished steel; 2024 US Section 232 and EU safeguard reviews risk raising costs after EU steel imports fell 12% YoY in 2023.

Government Subsidies for Green Transition

Sweden and Finland have allocated over SEK 20 billion (≈EUR 1.8bn) combined since 2020 for industrial decarbonization and pilot projects; SSAB depends on these subsidies to underwrite the ~SEK 40–50 billion investments projected for fossil-free HYBRIT facilities. Continued political backing—including Sweden’s 2024 extension of hydrogen and CCS incentives and Finland’s €200m green steel grants—remains critical to SSAB’s cost-competitiveness and scale-up timing.

Energy Sovereignty and Infrastructure

Political decisions on national grids and renewable expansion directly affect SSAB, which announced a target to reach fossil-free steel by 2045 and needs roughly 6–8 TWh/year of renewable power for planned electric arc furnace rollouts; state energy policies determine grid access and tariffs. Delays in permits or instability in Sweden, Finland, or the US risk pushing project timelines and capital deployment, with infrastructure bottlenecks potentially increasing costs beyond SSAB’s reported 2024 capex guidance of ~SEK 6–8 billion.

Defense Spending and Procurement

Rising defense budgets—EU planned defense spending up ~8% in 2024 and US defense budget at $858B for FY2024—boost demand for SSABs high-strength steels for armoured vehicles and infrastructure.

SSAB, with specialty grades and ~SEK 77.8bn revenue in 2023, gains from geopolitical tensions that increase state procurement.

Alignment with NATO and allies secures recurring high-value contracts and supports order visibility for SSABs advanced steel offerings.

- EU defense +8% (2024), US $858B (FY2024)

- SSAB revenue SEK 77.8bn (2023)

- NATO alignment → steady gov contracts

Regulatory Stability in the US Market

SSAB's large US footprint—roughly 28% of 2024 group sales—makes it highly exposed to shifts in American industrial policy and federal politics, where changes in administrations can alter emissions rules or infrastructure funding such as IRA allocations that directed $369bn nationwide by 2024.

Maintaining robust government relations is critical to keep US scrap-metal and minimill operations compliant and profitable amid potential regulatory tightening and subsidy shifts.

- 28% of 2024 sales from US

- IRA and related programs allocated $369bn by 2024

- Regulatory shifts risk operational and compliance cost volatility

SSAB margins hinge on trade, subsidies & HYBRIT funding as US exposure rises

Trade measures, subsidies and energy policy drive SSAB’s margins and project timing: 2024 EU/US steel reviews, SEK 20bn+ Sweden/Finland decarbonization support vs SEK 40–50bn HYBRIT need, ~6–8 TWh/yr renewable demand, SEK 77.8bn revenue (2023), 28% sales US exposure, EU defense +8% (2024), US $858bn FY2024.

| Metric | Value |

|---|---|

| Revenue (2023) | SEK 77.8bn |

| US share (2024) | 28% |

| HYBRIT capex need | SEK 40–50bn |

| Sweden/Finland support | SEK 20bn+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect SSAB across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities.

A concise, visually segmented PESTLE summary for SSAB that simplifies external risk assessment and market positioning, ready to drop into presentations or share across teams for fast alignment.

Economic factors

Global Steel Demand Cycles

The demand for SSAB’s steels is highly cyclical and tied to construction, automotive and heavy transport; global steel consumption fell 2.3% in 2023 but recovered with a 1.8% rise in 2024, while world GDP grew 3.1% in 2024—slower growth or higher interest rates can cut infrastructure spending and auto production, hitting volumes and ASPs. Monitoring OECD industrial production and IMF GDP forecasts is essential for near‑term revenue visibility.

Raw Material and Energy Costs

Fluctuations in iron ore, coking coal and electricity drive SSABs COGS; iron ore spot rose ~18% YoY in 2024 while EU industrial electricity prices averaged ~€120/MWh in 2024, amplifying cost pressure. SSAB’s HYBRIT shift to fossil-free steel reduces long-term exposure, but in 2024 ~70% of steelmaking still tied to traditional inputs, leaving margins vulnerable. The company uses hedges and passed through some costs, yet sustained high input prices risk compressing EBITDA if not fully recovered from customers.

Currency Exchange Rate Volatility

As SSAB reports in SEK while earning significant revenues in USD and EUR, 2024 FX moves mattered: the SEK weakened ~6% vs USD and ~4% vs EUR, amplifying translation gains but squeezing export competitiveness; a 10% USD/SEK swing can alter reported operating profit by several hundred million SEK given 2023 revenue mix (~40% Americas, ~30% Europe). Financial analysts must hedge and model FX impacts on consolidated statements and asset valuations.

Inflationary Pressures on Capital Expenditure

- Estimated investment need: SEK 100–150bn

- Input/wage inflation 2023–24: ~6–9% y/y

- Real rates ~1.5% (Sweden, 2024) raising financing costs

Scrap Metal Market Dynamics

SSAB’s US EAF operations depend on high-quality scrap; US scrap prices averaged about $380–$420/ton in 2024, driven by strong domestic demand and tighter global flows after Indonesia and Turkey tightened exports.

Global recycling growth and export restrictions reduced available scrap exports by an estimated 8–12% in 2023–24, raising procurement costs; rising EAF adoption pushed feeder competition, with steelmakers increasing scrap purchases ~6–9% YoY.

- US scrap price range 2024: $380–$420/ton

- Export supply reduction 2023–24: ~8–12%

- Increased scrap demand YoY: ~6–9%

- Higher procurement risk for SSAB’s margins

SSAB Outlook: Rising costs, weak SEK and modest demand lift margins pressure in 2024

Economic cycles, input-price swings and FX materially affect SSAB: 2024 steel demand +1.8%, world GDP +3.1%; iron ore +18% YoY; EU industrial power ~€120/MWh; SEK -6% vs USD, -4% vs EUR; estimated transition capex SEK 100–150bn; Swedish real rate ~1.5%; US scrap $380–420/t; scrap export reduction ~8–12%.

| Metric | 2024 / 2023–24 |

|---|---|

| World GDP growth | 3.1% (2024) |

| Steel demand | +1.8% (2024) |

| Iron ore | +18% YoY (2024) |

| EU power price | ~€120/MWh (2024) |

| SEK vs USD / EUR | -6% / -4% (2024) |

| Transition capex | SEK 100–150bn (2030 target) |

| Swedish real rate | ~1.5% (2024) |

| US scrap | $380–420/ton (2024) |

| Scrap export cut | ~8–12% (2023–24) |

Preview Before You Purchase

SSAB PESTLE Analysis

The preview shown here is the exact SSAB PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.