Stagwell Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

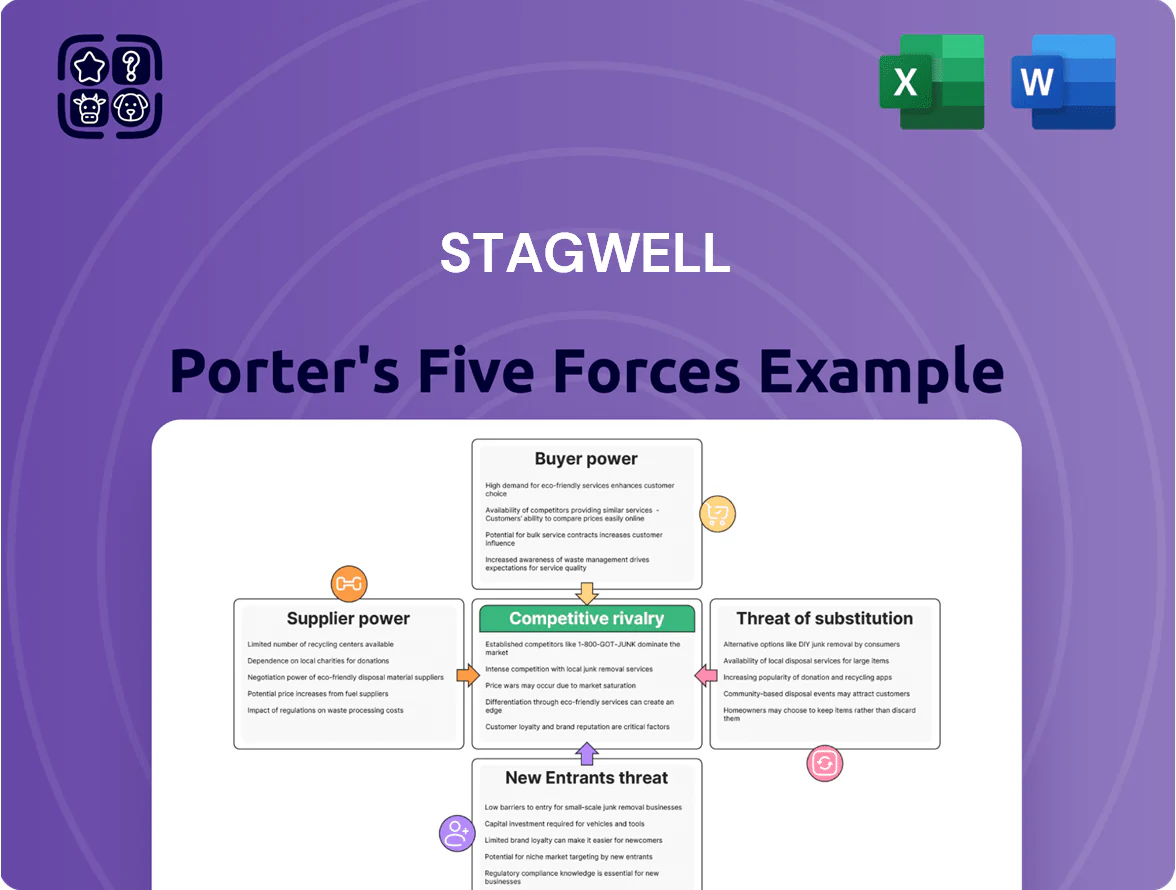

Stagwell faces a mix of strong buyer bargaining, digital disruption from substitutes, and moderate supplier leverage that together shape its competitive landscape; threat of new entrants hinges on scale and tech capabilities, while rivalry is intensified by consolidation among marketing services firms.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Stagwell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Talent and Creative Labor

Primary suppliers for Stagwell are skilled professionals—creatives, strategists, and data scientists—who delivered ~62% of agency revenue-driving work in 2024; their scarcity gave them wage leverage during the tight 2025 labor market for AI/digital skills, with US tech median pay for ML engineers up ~11% year-over-year to about $155k in 2025.

Top-tier talent now negotiates pay, hybrid setups, and equity; Stagwell faces poaching from FAANG and boutiques that raised total-comp pace by 8–15% in 2025, so it must keep investing in culture, career paths, and incentives to lower attrition below its 2024 industry peer median of ~14% annually.

Technology and Software Providers

Stagwell depends on third-party platforms—Salesforce, Adobe, Google—for cloud, CRM, and marketing automation, giving these suppliers high bargaining power because switching costs are large and integrations are deep. In 2024 Stagwell reported 17% digital revenue growth, so a 5% price hike from these vendors would erode margins materially; for example a $10m platform spend rising 5% cuts $500k from operating margins. Vendors’ essential infrastructure makes pass-through limited, forcing cost absorption or price increases to clients.

Media Platforms and Ad Exchanges

Large media owners—Meta (Facebook/Instagram), Alphabet (Google/YouTube), and Amazon—control most ad inventory where Stagwell buys placements, and they set pricing and opaque algorithm rules, leaving little room to negotiate; in 2024 Meta and Alphabet together accounted for ~60% of US digital ad spend ($190B of $315B, IAB estimate). Stagwell’s networked buying gives volume leverage, but platform owners remain the dominant force.

Freelance and Gig Economy Networks

Stagwell relies on a large freelance network for agility, with freelancers holding low individual bargaining power but platforms like Upwork and Fiverr shaping rates; Upwork reported a 17% rise in specialized talent demand in 2024.

High-end niche freelance costs in emerging markets rose ~12–20% in 2023–24, creating moderate supplier pressure on margins for specialized campaigns.

- Low individual supplier power

- Platforms set price floors, influence supply

- 17% demand rise on major platforms (2024)

- 12–20% cost increase for niche talent (2023–24)

AI and Data Content Creators

As generative AI embeds in marketing, suppliers of proprietary datasets and LLM licenses gain leverage; top model providers account for ~70% of market share in 2025, raising license and data costs for Stagwell.

Stagwell needs high-quality, ethically sourced data to train Stagwell Marketing Cloud; paying premium for vetted datasets and compliance adds to operating expense and slows rollout.

Dependence on a few major AI vendors creates supply-chain risk—single-vendor outages or price hikes could cut model access and impact client deliverables.

- Top AI vendors ~70% market share (2025)

- Data licensing and compliance raise OPEX by mid-single digits %

- Single-vendor outages risk campaign delays and revenue loss

Supplier power bites: talent pay, ad duopoly, AI vendors dominate, rising platform costs

Suppliers (talent, platforms, media owners, AI/data vendors) exert moderate-to-high power: talent scarcity lifted ML pay ~11% to $155k in 2025; Meta+Alphabet held ~60% US ad spend in 2024; top AI vendors ~70% market share (2025); platform spend sensitivity: 5% vendor price rise cuts $500k on a $10m spend; freelancer niche costs rose 12–20% (2023–24).

| Metric | Value |

|---|---|

| ML median pay (2025) | $155k (+11%) |

| Meta+Alphabet ad share (2024) | ~60% |

| Top AI vendors (2025) | ~70% |

| Freelance niche cost rise | 12–20% (2023–24) |

| Platform price sensitivity | 5% → $500k on $10m |

What is included in the product

Tailored exclusively for Stagwell, this Porter’s Five Forces analysis uncovers key drivers of competition, buyer/supplier power, barriers to entry, substitutes, and emerging disruptors that influence its pricing, profitability, and strategic positioning.

Condenses Stagwell's Porter’s Five Forces into a single-sheet strategic snapshot—ideal for swiftly assessing competitive pressure and guiding marketing or M&A decisions.

Customers Bargaining Power

Concentration of Large Enterprise Clients

Stagwell serves major global brands that often account for single-digit to mid-teens percentages of agency revenue; in 2024 several top clients represented roughly 5–12% each of consolidated revenue, giving them strong price and payment leverage.

These enterprise customers can demand lower fees, extended net-60+ terms, and bespoke service models, pressuring margins—Stagwell reported adjusted EBITDA margin pressure in client-concentrated agencies in 2023–24.

Loss of one anchor client can cut an agency’s revenue by double digits and force rapid cost adjustments; historically client exits across the ad sector have caused 10–30% quarterly revenue drops for affected units, a material risk for Stagwell.

Low Switching Costs for Marketing Services

Clients can shift accounts to rivals like WPP or Publicis with low structural barriers after contracts end, and Stagwell faced client churn pressure in 2024 when net client adds slowed despite 12% organic revenue growth.

This portability forces Stagwell to prove superior ROI and creative edge continually; its 2024 gross margin of ~28% and 2024 free cash flow of $120m suggest limited room for costly retention incentives.

The rise of project-based work—industry reports showed ~45% of agency revenue in 2024 came from short-term projects—gives buyers more scope to shop and reduces stickiness.

Transparency and Procurement-Led Decisons

Modern procurement teams audit agency fees and benchmark costs rigorously; 62% of Fortune 500 firms report using centralized procurement platforms in 2024, driving 8–12% fee compression for agencies year-over-year. This cost-first lens squeezes margins for integrated marketing networks, so Stagwell must lean on its data-driven challenger positioning—showing measurable ROI, cutting media inefficiencies by up to 15%, and passing procurement filters with transparent pricing and performance SLAs.

In-Housing of Marketing Capabilities

- 45% of marketers in 2024 moved work in-house

- Stagwell must pivot to strategic, complex offerings

- Outsourcing driven by unique IP, scale, or ROI

- Routine work decline compresses TAM and recurring fees

Demand for Performance-Based Pricing

Buyers increasingly demand performance-based pricing, tying agency pay to outcomes like sales or leads; by 2025 about 42% of U.S. marketers report using outcome-linked fees, shifting risk to Stagwell and increasing buyer control over economic value.

Agencies that can't prove direct attribution face weaker bargaining power; Stagwell must demonstrate ROI—e.g., last‑click or multi‑touch models showing >15% incremental sales—to defend fees.

- ~42% of U.S. marketers use outcome fees (2025)

- Performance models shift risk to agency

- Direct attribution >15% incremental sales strengthens negotiating position

Top-client leverage, in‑sourcing & performance fees squeeze agencies—prove >15% ROI

Large clients (5–12% each in 2024) wield strong fee and payment leverage, driving net-60+ terms and margin pressure; single-client loss can cut agency revenue by 10–30% quarterly. Project-based work (~45% of agency revenue in 2024) and 45% of marketers bringing work in-house reduce stickiness. Performance pricing adoption (~42% of U.S. marketers by 2025) shifts risk to agencies unless they prove >15% incremental sales ROI.

| Metric | Value |

|---|---|

| Top-client share (2024) | 5–12% |

| Project-based revenue (2024) | ~45% |

| Marketers in‑house (2024 ANA) | 45% |

| Performance fees (US, 2025) | ~42% |

| Required ROI to defend fees | >15% incremental sales |

Preview the Actual Deliverable

Stagwell Porter's Five Forces Analysis

This preview shows the exact Stagwell Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the full document is fully formatted and ready for use.

The analysis includes supplier and buyer power, competitive rivalry, threat of new entrants, and threat of substitutes tailored to Stagwell, and what you see here is the same file you'll download after payment.

No mockups or samples—this is the final, professionally written deliverable available instantly upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Stagwell faces a mix of strong buyer bargaining, digital disruption from substitutes, and moderate supplier leverage that together shape its competitive landscape; threat of new entrants hinges on scale and tech capabilities, while rivalry is intensified by consolidation among marketing services firms.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Stagwell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Talent and Creative Labor

Primary suppliers for Stagwell are skilled professionals—creatives, strategists, and data scientists—who delivered ~62% of agency revenue-driving work in 2024; their scarcity gave them wage leverage during the tight 2025 labor market for AI/digital skills, with US tech median pay for ML engineers up ~11% year-over-year to about $155k in 2025.

Top-tier talent now negotiates pay, hybrid setups, and equity; Stagwell faces poaching from FAANG and boutiques that raised total-comp pace by 8–15% in 2025, so it must keep investing in culture, career paths, and incentives to lower attrition below its 2024 industry peer median of ~14% annually.

Technology and Software Providers

Stagwell depends on third-party platforms—Salesforce, Adobe, Google—for cloud, CRM, and marketing automation, giving these suppliers high bargaining power because switching costs are large and integrations are deep. In 2024 Stagwell reported 17% digital revenue growth, so a 5% price hike from these vendors would erode margins materially; for example a $10m platform spend rising 5% cuts $500k from operating margins. Vendors’ essential infrastructure makes pass-through limited, forcing cost absorption or price increases to clients.

Media Platforms and Ad Exchanges

Large media owners—Meta (Facebook/Instagram), Alphabet (Google/YouTube), and Amazon—control most ad inventory where Stagwell buys placements, and they set pricing and opaque algorithm rules, leaving little room to negotiate; in 2024 Meta and Alphabet together accounted for ~60% of US digital ad spend ($190B of $315B, IAB estimate). Stagwell’s networked buying gives volume leverage, but platform owners remain the dominant force.

Freelance and Gig Economy Networks

Stagwell relies on a large freelance network for agility, with freelancers holding low individual bargaining power but platforms like Upwork and Fiverr shaping rates; Upwork reported a 17% rise in specialized talent demand in 2024.

High-end niche freelance costs in emerging markets rose ~12–20% in 2023–24, creating moderate supplier pressure on margins for specialized campaigns.

- Low individual supplier power

- Platforms set price floors, influence supply

- 17% demand rise on major platforms (2024)

- 12–20% cost increase for niche talent (2023–24)

AI and Data Content Creators

As generative AI embeds in marketing, suppliers of proprietary datasets and LLM licenses gain leverage; top model providers account for ~70% of market share in 2025, raising license and data costs for Stagwell.

Stagwell needs high-quality, ethically sourced data to train Stagwell Marketing Cloud; paying premium for vetted datasets and compliance adds to operating expense and slows rollout.

Dependence on a few major AI vendors creates supply-chain risk—single-vendor outages or price hikes could cut model access and impact client deliverables.

- Top AI vendors ~70% market share (2025)

- Data licensing and compliance raise OPEX by mid-single digits %

- Single-vendor outages risk campaign delays and revenue loss

Supplier power bites: talent pay, ad duopoly, AI vendors dominate, rising platform costs

Suppliers (talent, platforms, media owners, AI/data vendors) exert moderate-to-high power: talent scarcity lifted ML pay ~11% to $155k in 2025; Meta+Alphabet held ~60% US ad spend in 2024; top AI vendors ~70% market share (2025); platform spend sensitivity: 5% vendor price rise cuts $500k on a $10m spend; freelancer niche costs rose 12–20% (2023–24).

| Metric | Value |

|---|---|

| ML median pay (2025) | $155k (+11%) |

| Meta+Alphabet ad share (2024) | ~60% |

| Top AI vendors (2025) | ~70% |

| Freelance niche cost rise | 12–20% (2023–24) |

| Platform price sensitivity | 5% → $500k on $10m |

What is included in the product

Tailored exclusively for Stagwell, this Porter’s Five Forces analysis uncovers key drivers of competition, buyer/supplier power, barriers to entry, substitutes, and emerging disruptors that influence its pricing, profitability, and strategic positioning.

Condenses Stagwell's Porter’s Five Forces into a single-sheet strategic snapshot—ideal for swiftly assessing competitive pressure and guiding marketing or M&A decisions.

Customers Bargaining Power

Concentration of Large Enterprise Clients

Stagwell serves major global brands that often account for single-digit to mid-teens percentages of agency revenue; in 2024 several top clients represented roughly 5–12% each of consolidated revenue, giving them strong price and payment leverage.

These enterprise customers can demand lower fees, extended net-60+ terms, and bespoke service models, pressuring margins—Stagwell reported adjusted EBITDA margin pressure in client-concentrated agencies in 2023–24.

Loss of one anchor client can cut an agency’s revenue by double digits and force rapid cost adjustments; historically client exits across the ad sector have caused 10–30% quarterly revenue drops for affected units, a material risk for Stagwell.

Low Switching Costs for Marketing Services

Clients can shift accounts to rivals like WPP or Publicis with low structural barriers after contracts end, and Stagwell faced client churn pressure in 2024 when net client adds slowed despite 12% organic revenue growth.

This portability forces Stagwell to prove superior ROI and creative edge continually; its 2024 gross margin of ~28% and 2024 free cash flow of $120m suggest limited room for costly retention incentives.

The rise of project-based work—industry reports showed ~45% of agency revenue in 2024 came from short-term projects—gives buyers more scope to shop and reduces stickiness.

Transparency and Procurement-Led Decisons

Modern procurement teams audit agency fees and benchmark costs rigorously; 62% of Fortune 500 firms report using centralized procurement platforms in 2024, driving 8–12% fee compression for agencies year-over-year. This cost-first lens squeezes margins for integrated marketing networks, so Stagwell must lean on its data-driven challenger positioning—showing measurable ROI, cutting media inefficiencies by up to 15%, and passing procurement filters with transparent pricing and performance SLAs.

In-Housing of Marketing Capabilities

- 45% of marketers in 2024 moved work in-house

- Stagwell must pivot to strategic, complex offerings

- Outsourcing driven by unique IP, scale, or ROI

- Routine work decline compresses TAM and recurring fees

Demand for Performance-Based Pricing

Buyers increasingly demand performance-based pricing, tying agency pay to outcomes like sales or leads; by 2025 about 42% of U.S. marketers report using outcome-linked fees, shifting risk to Stagwell and increasing buyer control over economic value.

Agencies that can't prove direct attribution face weaker bargaining power; Stagwell must demonstrate ROI—e.g., last‑click or multi‑touch models showing >15% incremental sales—to defend fees.

- ~42% of U.S. marketers use outcome fees (2025)

- Performance models shift risk to agency

- Direct attribution >15% incremental sales strengthens negotiating position

Top-client leverage, in‑sourcing & performance fees squeeze agencies—prove >15% ROI

Large clients (5–12% each in 2024) wield strong fee and payment leverage, driving net-60+ terms and margin pressure; single-client loss can cut agency revenue by 10–30% quarterly. Project-based work (~45% of agency revenue in 2024) and 45% of marketers bringing work in-house reduce stickiness. Performance pricing adoption (~42% of U.S. marketers by 2025) shifts risk to agencies unless they prove >15% incremental sales ROI.

| Metric | Value |

|---|---|

| Top-client share (2024) | 5–12% |

| Project-based revenue (2024) | ~45% |

| Marketers in‑house (2024 ANA) | 45% |

| Performance fees (US, 2025) | ~42% |

| Required ROI to defend fees | >15% incremental sales |

Preview the Actual Deliverable

Stagwell Porter's Five Forces Analysis

This preview shows the exact Stagwell Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the full document is fully formatted and ready for use.

The analysis includes supplier and buyer power, competitive rivalry, threat of new entrants, and threat of substitutes tailored to Stagwell, and what you see here is the same file you'll download after payment.

No mockups or samples—this is the final, professionally written deliverable available instantly upon purchase.