Stagwell SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Unpack Stagwell’s competitive edge and vulnerabilities with our concise SWOT snapshot—then purchase the full analysis to access research-backed insights, actionable recommendations, and editable Word/Excel deliverables that support investment, strategy, and pitch-ready presentations.

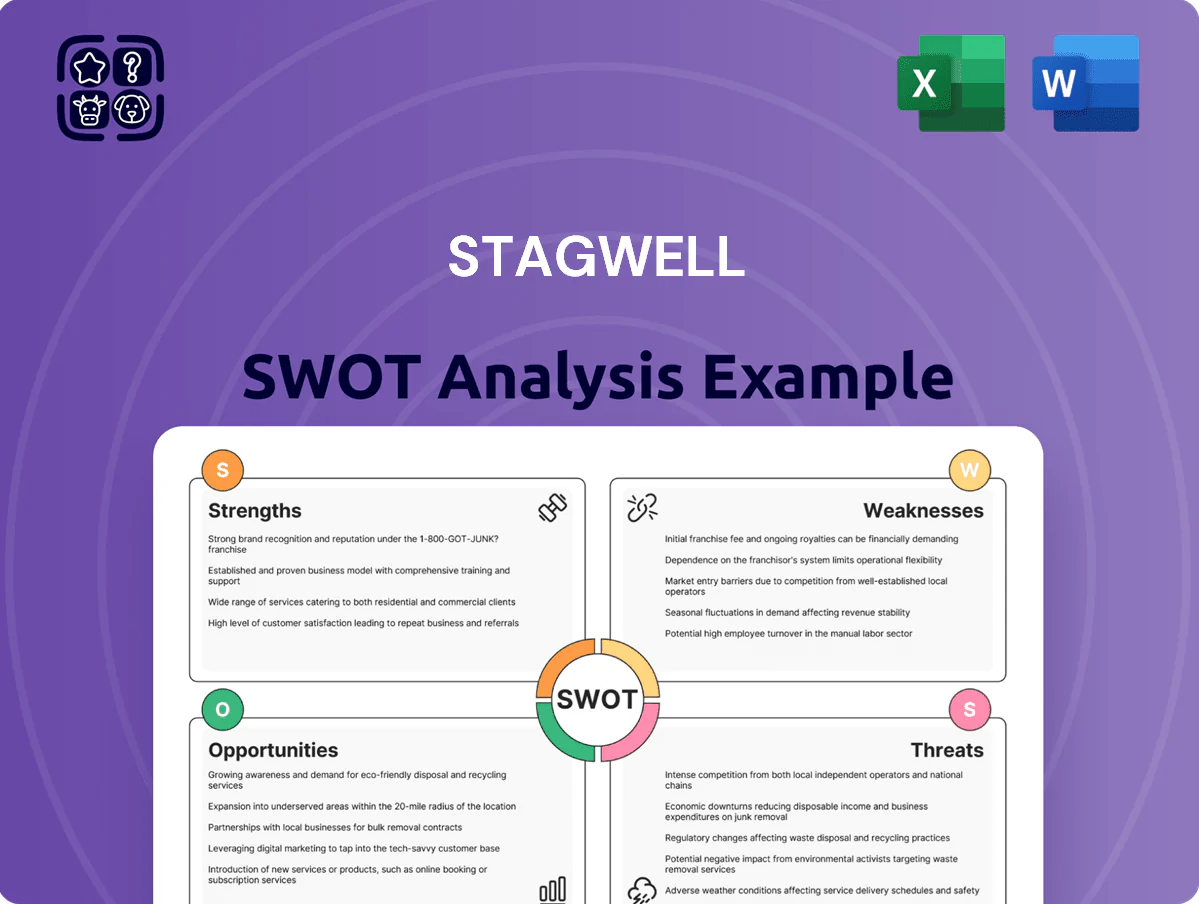

Strengths

Advanced Digital and AI Integration

Stagwell shifted to a digital-first model, shedding legacy holding-company layers to scale faster and cut overhead; revenue from digital services rose 24% year-over-year to $1.32bn in FY 2024. By late 2025, heavy investment in proprietary AI within Stagwell Marketing Cloud powered a 35% drop in content production time and a 20% lift in campaign ROI for global clients. This tech focus drives data-led decisions across 40+ markets, creating a clear competitive edge.

Agile Collaborative Network Structure

Stagwell’s decentralized network lets 130+ specialist agencies form bespoke teams fast, cutting approval layers and delivering median project ramp-up in under 10 days versus industry 25 days; that speed drove 2024 revenue growth of 19% to $1.08B, showing CMOs pay a 12–18% premium for rapid, integrated digital transformation and PR bundles.

Dominance in Political and Advocacy Marketing

Stagwell, via agencies like 160/2020 and SKDK, leads US political and advocacy marketing, capturing an estimated $220m+ in campaign-related fees in 2024, per company disclosures; this niche gives counter-cyclical revenue that surged ~35% in 2024 election spending vs 2023, cushioning downturns. Their high-stakes messaging skills also drive corporate crisis mandates, contributing roughly 8–12% of client advisory revenue.

Strong Performance-Based Culture

Stagwell’s leadership, led by CEO Mark Penn, drives a results-first culture tying agency pay to client KPIs, which helped revenue grow 12% to $1.06B in 2024 as clients demand measurable ROI.

Their emphasis on performance marketing and analytics has captured share from traditional firms—digital services now represent ~68% of billings—while data-led creativity lifted average campaign ROAS to 4.2x in 2024.

- CEO Mark Penn: performance-first incentives

- 2024 revenue: $1.06B (+12%)

- Digital billings ~68% of total

- Average ROAS 4.2x in 2024

Strategic Global Footprint Expansion

By end-2025, Stagwell expanded into 12 new EMEA and 7 APAC markets via acquisitions and partnerships, lifting international revenue share to 46% of FY2025 total and supporting 220 multinational clients.

The global footprint lets Stagwell deliver uniform campaigns across 35 languages while keeping local teams; scalable delivery cut time-to-market by 18% for cross-border briefs.

Stagwell: AI-led growth—$1.32B digital, 4.2x ROAS, 35% faster content, 46% intl

Stagwell’s digital-first, AI-powered platform drove FY2024 digital revenue to $1.32bn (+24%) and cut content time 35% by late 2025; decentralized network of 130+ agencies speeds ramp-up to <10 days, supporting 220 multinationals and 46% FY2025 international revenue. Performance focus lifted average ROAS to 4.2x in 2024 and political/advocacy fees ~ $220m, providing counter-cyclical revenue.

| Metric | Value |

|---|---|

| FY2024 digital revenue | $1.32bn (+24%) |

| Average ROAS 2024 | 4.2x |

| Content time reduction | 35% (by late 2025) |

| Agencies | 130+ |

| Intl revenue share FY2025 | 46% |

| Political fees 2024 | ~$220m |

What is included in the product

Provides a concise SWOT analysis of Stagwell, outlining its core strengths and weaknesses while mapping key opportunities and external threats shaping the company’s strategic position.

Provides a concise SWOT matrix tailored to Stagwell for fast, visual strategy alignment and executive-ready summaries.

Weaknesses

Heavy Reliance on North American Revenue

Despite international moves, 2024 SEC filings show roughly 78% of Stagwell’s $3.1B revenue came from the U.S., leaving the business exposed to domestic ad spend swings and US GDP cycles.

That concentration means a 5% US ad-market decline could cut group revenue by ~3.9% (here’s the quick math: 78% × 5%), so diversifying geographically remains a critical strategic challenge.

Brand Awareness vs Legacy Holding Companies

Stagwell often faces legacy giants—WPP, Omnicom, Publicis—with combined 2024 revenue exceeding $70B, giving them far stronger historical brand recognition than Stagwell’s $2.0B 2024 revenue.

Despite a reputation for innovation, Stagwell can lose conservative enterprise deals to legacy firms seen as the safer choice; enterprise RFPs still favor incumbent relationships.

Closing this gap needs sustained marketing of Stagwell’s integrated value proposition and case studies showing its 15–25% ROI gains on recent client pilots.

Complexity of Managing Diverse Agency Brands

The network’s many distinct agency brands can cause internal competition and brand dilution; Stagwell owned about 130 agency brands as of Dec 31, 2024, complicating cross-selling and raising overlap risk. Ensuring a unified culture and consistent service quality across this fragmented portfolio increases overhead and HR costs—SG&A was $1.1B in FY2024—while individual agency identities may clash with the corporate strategy, harming integration and client retention.

Debt Levels from M&A Activity

Stagwell’s acquisition-led growth has pushed net debt to about $1.6bn as of FY2024, raising interest costs that squeezed adjusted EBITDA margins by ~120bps in 2024 versus 2022.

In a 5%+ rate backdrop, higher debt service reduces cash for R&D and slows investment in the Stagwell Marketing Cloud, forcing trade-offs between deleveraging and product build.

Maintaining a leverage target near 3.0x net debt/EBITDA while funding cloud expansion is a narrow path that increases refinancing and execution risk.

- Net debt ≈ $1.6bn (FY2024)

- Margin bite ~120bps (2022–24)

- Leverage target ~3.0x ND/EBITDA

- Higher rates → less R&D cash

Integration Risks of Proprietary Tech

The Stagwell Marketing Cloud drives recurring revenue but carries high upkeep: Stagwell reported $265 million in technology and development spend in FY2024, pressuring margins if adoption lags.

If clients prefer third-party AI platforms or tools age quickly, the firm risks sunk capital and lower ROI; global generative AI churn can render models obsolete within 12–18 months.

Balancing product development with agency services strains talent and increases fixed costs, turning Stagwell into a de facto software vendor alongside marketing services.

- Tech/dev spend $265M in FY2024

- AI model obsolescence ~12–18 months

- Risk: lower ROI if adoption < target

Stagwell: US-heavy, debt-laden ad group faces margin pressure vs $70B rivals

High US revenue concentration (78% of $3.1B in 2024) exposes Stagwell to domestic ad cycles; a 5% US ad drop ≈ 3.9% revenue hit. Competes with giants (WPP/Omnicom/Publicis combined >$70B vs Stagwell $2.0B), faces brand dilution across ~130 agencies, elevated net debt ~$1.6B and tech spend $265M (FY2024) that pressure margins and raise execution risk.

| Metric | Value (FY2024) |

|---|---|

| Revenue | $3.1B |

| US share | 78% |

| Net debt | $1.6B |

| Tech/dev spend | $265M |

Preview Before You Purchase

Stagwell SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Unpack Stagwell’s competitive edge and vulnerabilities with our concise SWOT snapshot—then purchase the full analysis to access research-backed insights, actionable recommendations, and editable Word/Excel deliverables that support investment, strategy, and pitch-ready presentations.

Strengths

Advanced Digital and AI Integration

Stagwell shifted to a digital-first model, shedding legacy holding-company layers to scale faster and cut overhead; revenue from digital services rose 24% year-over-year to $1.32bn in FY 2024. By late 2025, heavy investment in proprietary AI within Stagwell Marketing Cloud powered a 35% drop in content production time and a 20% lift in campaign ROI for global clients. This tech focus drives data-led decisions across 40+ markets, creating a clear competitive edge.

Agile Collaborative Network Structure

Stagwell’s decentralized network lets 130+ specialist agencies form bespoke teams fast, cutting approval layers and delivering median project ramp-up in under 10 days versus industry 25 days; that speed drove 2024 revenue growth of 19% to $1.08B, showing CMOs pay a 12–18% premium for rapid, integrated digital transformation and PR bundles.

Dominance in Political and Advocacy Marketing

Stagwell, via agencies like 160/2020 and SKDK, leads US political and advocacy marketing, capturing an estimated $220m+ in campaign-related fees in 2024, per company disclosures; this niche gives counter-cyclical revenue that surged ~35% in 2024 election spending vs 2023, cushioning downturns. Their high-stakes messaging skills also drive corporate crisis mandates, contributing roughly 8–12% of client advisory revenue.

Strong Performance-Based Culture

Stagwell’s leadership, led by CEO Mark Penn, drives a results-first culture tying agency pay to client KPIs, which helped revenue grow 12% to $1.06B in 2024 as clients demand measurable ROI.

Their emphasis on performance marketing and analytics has captured share from traditional firms—digital services now represent ~68% of billings—while data-led creativity lifted average campaign ROAS to 4.2x in 2024.

- CEO Mark Penn: performance-first incentives

- 2024 revenue: $1.06B (+12%)

- Digital billings ~68% of total

- Average ROAS 4.2x in 2024

Strategic Global Footprint Expansion

By end-2025, Stagwell expanded into 12 new EMEA and 7 APAC markets via acquisitions and partnerships, lifting international revenue share to 46% of FY2025 total and supporting 220 multinational clients.

The global footprint lets Stagwell deliver uniform campaigns across 35 languages while keeping local teams; scalable delivery cut time-to-market by 18% for cross-border briefs.

Stagwell: AI-led growth—$1.32B digital, 4.2x ROAS, 35% faster content, 46% intl

Stagwell’s digital-first, AI-powered platform drove FY2024 digital revenue to $1.32bn (+24%) and cut content time 35% by late 2025; decentralized network of 130+ agencies speeds ramp-up to <10 days, supporting 220 multinationals and 46% FY2025 international revenue. Performance focus lifted average ROAS to 4.2x in 2024 and political/advocacy fees ~ $220m, providing counter-cyclical revenue.

| Metric | Value |

|---|---|

| FY2024 digital revenue | $1.32bn (+24%) |

| Average ROAS 2024 | 4.2x |

| Content time reduction | 35% (by late 2025) |

| Agencies | 130+ |

| Intl revenue share FY2025 | 46% |

| Political fees 2024 | ~$220m |

What is included in the product

Provides a concise SWOT analysis of Stagwell, outlining its core strengths and weaknesses while mapping key opportunities and external threats shaping the company’s strategic position.

Provides a concise SWOT matrix tailored to Stagwell for fast, visual strategy alignment and executive-ready summaries.

Weaknesses

Heavy Reliance on North American Revenue

Despite international moves, 2024 SEC filings show roughly 78% of Stagwell’s $3.1B revenue came from the U.S., leaving the business exposed to domestic ad spend swings and US GDP cycles.

That concentration means a 5% US ad-market decline could cut group revenue by ~3.9% (here’s the quick math: 78% × 5%), so diversifying geographically remains a critical strategic challenge.

Brand Awareness vs Legacy Holding Companies

Stagwell often faces legacy giants—WPP, Omnicom, Publicis—with combined 2024 revenue exceeding $70B, giving them far stronger historical brand recognition than Stagwell’s $2.0B 2024 revenue.

Despite a reputation for innovation, Stagwell can lose conservative enterprise deals to legacy firms seen as the safer choice; enterprise RFPs still favor incumbent relationships.

Closing this gap needs sustained marketing of Stagwell’s integrated value proposition and case studies showing its 15–25% ROI gains on recent client pilots.

Complexity of Managing Diverse Agency Brands

The network’s many distinct agency brands can cause internal competition and brand dilution; Stagwell owned about 130 agency brands as of Dec 31, 2024, complicating cross-selling and raising overlap risk. Ensuring a unified culture and consistent service quality across this fragmented portfolio increases overhead and HR costs—SG&A was $1.1B in FY2024—while individual agency identities may clash with the corporate strategy, harming integration and client retention.

Debt Levels from M&A Activity

Stagwell’s acquisition-led growth has pushed net debt to about $1.6bn as of FY2024, raising interest costs that squeezed adjusted EBITDA margins by ~120bps in 2024 versus 2022.

In a 5%+ rate backdrop, higher debt service reduces cash for R&D and slows investment in the Stagwell Marketing Cloud, forcing trade-offs between deleveraging and product build.

Maintaining a leverage target near 3.0x net debt/EBITDA while funding cloud expansion is a narrow path that increases refinancing and execution risk.

- Net debt ≈ $1.6bn (FY2024)

- Margin bite ~120bps (2022–24)

- Leverage target ~3.0x ND/EBITDA

- Higher rates → less R&D cash

Integration Risks of Proprietary Tech

The Stagwell Marketing Cloud drives recurring revenue but carries high upkeep: Stagwell reported $265 million in technology and development spend in FY2024, pressuring margins if adoption lags.

If clients prefer third-party AI platforms or tools age quickly, the firm risks sunk capital and lower ROI; global generative AI churn can render models obsolete within 12–18 months.

Balancing product development with agency services strains talent and increases fixed costs, turning Stagwell into a de facto software vendor alongside marketing services.

- Tech/dev spend $265M in FY2024

- AI model obsolescence ~12–18 months

- Risk: lower ROI if adoption < target

Stagwell: US-heavy, debt-laden ad group faces margin pressure vs $70B rivals

High US revenue concentration (78% of $3.1B in 2024) exposes Stagwell to domestic ad cycles; a 5% US ad drop ≈ 3.9% revenue hit. Competes with giants (WPP/Omnicom/Publicis combined >$70B vs Stagwell $2.0B), faces brand dilution across ~130 agencies, elevated net debt ~$1.6B and tech spend $265M (FY2024) that pressure margins and raise execution risk.

| Metric | Value (FY2024) |

|---|---|

| Revenue | $3.1B |

| US share | 78% |

| Net debt | $1.6B |

| Tech/dev spend | $265M |

Preview Before You Purchase

Stagwell SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.