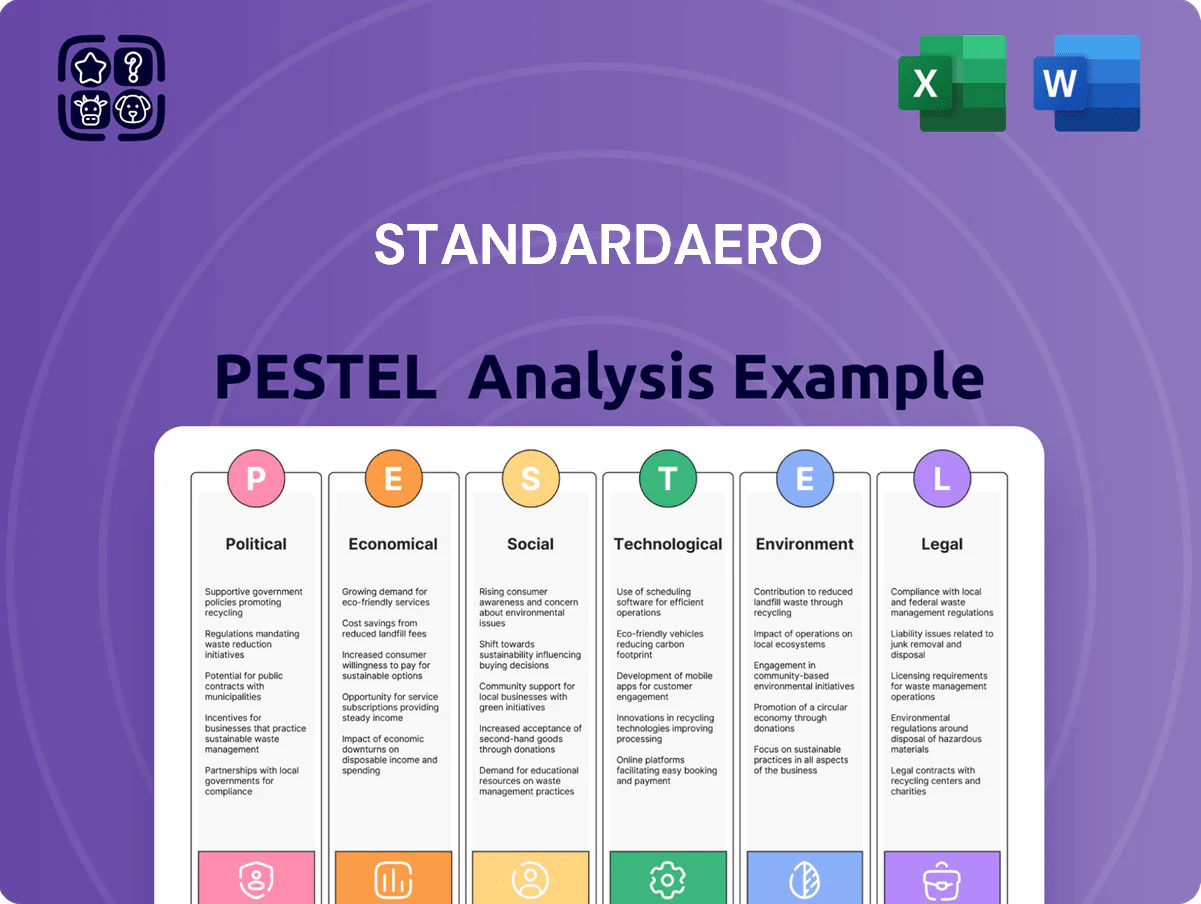

StandardAero PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces are shaping StandardAero’s trajectory—our PESTLE highlights risks and opportunities that matter to investors and strategists. This concise, expertly researched snapshot helps you make faster, smarter decisions; purchase the full analysis for the complete, editable report and deep-dive insights ready for boardrooms and investment cases.

Political factors

Defense Budget Allocations

StandardAero holds substantial exposure to military contracts, making revenue sensitive to national defense budgets; US defense spending reached roughly $858 billion in FY2025, supporting aftermarket engine services. Sustained tensions in Eastern Europe and the Indo-Pacific through late 2025 increased demand for military engine maintenance, with global defense spending up ~3.5% year-over-year. Long-term government service agreements, representing an estimated 30–40% of defense-related backlog, hedge commercial volatility.

Trade Policy and Tariffs

Global operations require seamless movement of high-value components across borders; in 2024 StandardAero moved parts valued at an estimated $1.2bn, exposing it to tariff risk across the US, EU and China trade lanes.

Changes in trade agreements or new tariffs on aerospace alloys and parts—recently averaging 5–15% in disputed sectors—can disrupt lead times and add millions in input costs.

By end-2025 protectionist measures in key markets forced localization of certain MRO capabilities, reducing cross-border shipments by ~18% and preserving ~$45m in annualized tariff exposure.

Government Outsourcing Trends

There is a clear shift: since 2020, over 25% of NATO air forces have expanded outsourcing of non-core MRO, boosting market demand for independent providers; global defense MRO outsourcing projected CAGR is ~6.1% through 2028, creating sizable opportunities for StandardAero.

StandardAero, with defense services revenue near US$600m in 2024 and established military MRO contracts, is well-positioned to capture government demand for cost-effective alternatives to OEM-managed programs, improving fleet readiness.

The political trend toward privatization of defense maintenance — reflected in rising government procurement of third-party sustainment services and budget pressures across major militaries — remains a primary growth driver for StandardAero.

Export Control Regulations

StandardAero must comply with ITAR and EAR across its global operations; US export control violations can incur fines up to $1.2 million per violation and criminal penalties including $1 million and 20 years imprisonment per willful violation (BIS/State Dept data through 2024).

Shifts in diplomatic relations have led to license revocations for aerospace engines to specific regions, disrupting revenue streams—US aerospace export licenses dropped 7% in 2023 vs 2022, raising enforcement risk for suppliers like StandardAero.

Robust compliance frameworks, training, and automated screening are essential to preserve government contracts and avoid reputational damage; companies with strong programs saw 40% fewer investigations in 2022–2024 enforcement data.

- Mandatory ITAR/EAR adherence; penalties up to $1.2M/violation and severe criminal exposure.

- Diplomatic shifts can revoke licenses; US aerospace export licenses fell 7% in 2023.

- Strong compliance reduces investigation risk by ~40% per 2022–2024 enforcement trends.

Geopolitical Stability

- Regional conflicts → fewer flight hours → fewer shop visits

- Airspace closures in Middle East/Asia cut corridor MRO demand

- Continuous geographic mix assessment reduces localized shock risk

Defense budgets, export rules & MRO outsourcing reshape $600M players—$45M tariff wins

Political exposure: defense budgets (US FY2025 ~$858B) drive ~30–40% of defense backlog; export controls (ITAR/EAR) carry fines up to $1.2M/violation; 2024–25 protectionism cut cross-border shipments ~18%, saving ~$45M tariff exposure; defense MRO outsourcing CAGR ~6.1% to 2028 creates growth opportunity.

| Metric | Value |

|---|---|

| US defense spend FY2025 | $858B |

| Defense revenue (StdAero 2024) | $600M |

| Cross-border shipment drop | 18% |

| Tariff exposure saved | $45M |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal factors uniquely impact StandardAero, with each section supported by data and trends to identify threats and opportunities.

Condenses the full StandardAero PESTLE into a crisp, shareable brief that’s visually segmented by factor for quick interpretation in meetings, easily dropped into slides, and editable with notes to align teams across regions and business lines.

Economic factors

Interest Rate Volatility

As a capital-intensive firm now public, StandardAero’s sensitivity to debt costs is acute: US corporate BAA yields rose from 4.1% in Jan 2024 to about 5.0% by Dec 2025, raising borrowing costs for expansions and MRO CAPEX.

By end-2025, sustained Fed funds around 5.25%–5.50% constrains feasibility of large-scale facility builds and turbine-tooling upgrades unless financed at higher rates or via equity.

Higher rates tighten leasing markets and working capital, with 2025 global airline CAPEX cuts of ~8% reported, increasing likelihood operators delay noncritical engine overhauls.

Global Fleet Expansion

Resurgent global air travel—projected at 4–5% annual RPK growth through 2025 with IATA estimating 2024 passenger numbers at ~95% of 2019 levels—has increased flight hours and engine cycles, boosting MRO demand; global commercial fleet hours rose ~8% year-over-year in 2023–24. This fleet expansion drives higher component shop visits and engine overhauls, directly lifting StandardAero’s service volumes. Given the firm’s exposure to commercial OEM and aftermarket segments, revenue growth closely tracks airline utilization trends and spare-part spend. StandardAero’s 2024 segment results showed aftermarket services growth consistent with industry utilization upticks.

Inflationary Pressure on Parts

Rising costs for specialty alloys and skilled labor have pushed engine-part prices up roughly 8–12% in 2024, increasing shop-visit spend per engine by an estimated $20k–$40k; StandardAero faces margin pressure as it weighs passing costs to customers while staying price-competitive with independent MROs.

Effective inventory turns and multiyear supplier agreements—StandardAero reported inventory up 6% in 2024—are key levers to hedge persistent inflation and stabilize input costs.

Currency Exchange Risk

With customers across North America, Europe and APAC, StandardAero faces material USD exposure: roughly 30–40% of 2024 service revenues originated in non-USD currencies, requiring active hedging to protect margins from sudden devaluations.

Revenue in EUR, CAD and AUD must be hedged; a 10% EUR depreciation versus USD could cut euro-denominated margin by ~3–5 percentage points for affected contracts.

Slower air travel recovery in emerging markets (2024 passenger traffic still 10–15% below 2019 in parts of LATAM/AFR) reduces local carriers’ purchasing power, pressuring aftermarket demand.

- 30–40% of 2024 service revenue non-USD

- 10% EUR move can reduce margins ~3–5ppt

- LATAM/AFR traffic 10–15% below 2019 in 2024

Labor Market Dynamics

StandardAero faces industry-wide shortages of skilled technicians and engineers, pushing average technician wages up about 8–12% between 2023–2025 and specialty engineer salaries up to mid-six figures in 2025.

To meet SLAs, StandardAero must offer competitive pay, benefits, and training; failure risks higher turnaround times and contract penalties.

Rising labor costs accounted for an increasing share of operating expenses, estimated at roughly 35–40% of total OPEX by late 2025.

- Technician wages +8–12% (2023–2025)

- Specialty engineers earning mid-six figures (2025)

- Labor ≈35–40% of OPEX by late 2025

- Competitive packages and training required to meet SLAs

Higher rates squeeze airline CAPEX; MRO demand up as RPKs recover, hedges essential

Higher interest rates (Fed 5.25–5.50% end‑2025; US BAA ~5.0%) raise borrowing costs, constraining CAPEX; airline CAPEX cut ~8% in 2025 shifts MRO timing. Strong RPK growth 4–5% and ~95% of 2019 passengers (2024) lift MRO demand, offsetting margin pressure from 8–12% input and labor cost inflation. FX exposure (30–40% non‑USD revenue) and inventory up 6% (2024) require active hedging and supplier contracts.

| Metric | 2024–25 |

|---|---|

| Fed funds | 5.25–5.50% |

| US BAA | ~5.0% |

| Airline CAPEX change | −8% (2025) |

| RPK growth | 4–5% pa |

| Input/labor inflation | +8–12% |

| Non‑USD revenue | 30–40% |

| Inventory change | +6% (2024) |

What You See Is What You Get

StandardAero PESTLE Analysis

The preview shown here is the exact StandardAero PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and detail visible in this preview are the same file you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces are shaping StandardAero’s trajectory—our PESTLE highlights risks and opportunities that matter to investors and strategists. This concise, expertly researched snapshot helps you make faster, smarter decisions; purchase the full analysis for the complete, editable report and deep-dive insights ready for boardrooms and investment cases.

Political factors

Defense Budget Allocations

StandardAero holds substantial exposure to military contracts, making revenue sensitive to national defense budgets; US defense spending reached roughly $858 billion in FY2025, supporting aftermarket engine services. Sustained tensions in Eastern Europe and the Indo-Pacific through late 2025 increased demand for military engine maintenance, with global defense spending up ~3.5% year-over-year. Long-term government service agreements, representing an estimated 30–40% of defense-related backlog, hedge commercial volatility.

Trade Policy and Tariffs

Global operations require seamless movement of high-value components across borders; in 2024 StandardAero moved parts valued at an estimated $1.2bn, exposing it to tariff risk across the US, EU and China trade lanes.

Changes in trade agreements or new tariffs on aerospace alloys and parts—recently averaging 5–15% in disputed sectors—can disrupt lead times and add millions in input costs.

By end-2025 protectionist measures in key markets forced localization of certain MRO capabilities, reducing cross-border shipments by ~18% and preserving ~$45m in annualized tariff exposure.

Government Outsourcing Trends

There is a clear shift: since 2020, over 25% of NATO air forces have expanded outsourcing of non-core MRO, boosting market demand for independent providers; global defense MRO outsourcing projected CAGR is ~6.1% through 2028, creating sizable opportunities for StandardAero.

StandardAero, with defense services revenue near US$600m in 2024 and established military MRO contracts, is well-positioned to capture government demand for cost-effective alternatives to OEM-managed programs, improving fleet readiness.

The political trend toward privatization of defense maintenance — reflected in rising government procurement of third-party sustainment services and budget pressures across major militaries — remains a primary growth driver for StandardAero.

Export Control Regulations

StandardAero must comply with ITAR and EAR across its global operations; US export control violations can incur fines up to $1.2 million per violation and criminal penalties including $1 million and 20 years imprisonment per willful violation (BIS/State Dept data through 2024).

Shifts in diplomatic relations have led to license revocations for aerospace engines to specific regions, disrupting revenue streams—US aerospace export licenses dropped 7% in 2023 vs 2022, raising enforcement risk for suppliers like StandardAero.

Robust compliance frameworks, training, and automated screening are essential to preserve government contracts and avoid reputational damage; companies with strong programs saw 40% fewer investigations in 2022–2024 enforcement data.

- Mandatory ITAR/EAR adherence; penalties up to $1.2M/violation and severe criminal exposure.

- Diplomatic shifts can revoke licenses; US aerospace export licenses fell 7% in 2023.

- Strong compliance reduces investigation risk by ~40% per 2022–2024 enforcement trends.

Geopolitical Stability

- Regional conflicts → fewer flight hours → fewer shop visits

- Airspace closures in Middle East/Asia cut corridor MRO demand

- Continuous geographic mix assessment reduces localized shock risk

Defense budgets, export rules & MRO outsourcing reshape $600M players—$45M tariff wins

Political exposure: defense budgets (US FY2025 ~$858B) drive ~30–40% of defense backlog; export controls (ITAR/EAR) carry fines up to $1.2M/violation; 2024–25 protectionism cut cross-border shipments ~18%, saving ~$45M tariff exposure; defense MRO outsourcing CAGR ~6.1% to 2028 creates growth opportunity.

| Metric | Value |

|---|---|

| US defense spend FY2025 | $858B |

| Defense revenue (StdAero 2024) | $600M |

| Cross-border shipment drop | 18% |

| Tariff exposure saved | $45M |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal factors uniquely impact StandardAero, with each section supported by data and trends to identify threats and opportunities.

Condenses the full StandardAero PESTLE into a crisp, shareable brief that’s visually segmented by factor for quick interpretation in meetings, easily dropped into slides, and editable with notes to align teams across regions and business lines.

Economic factors

Interest Rate Volatility

As a capital-intensive firm now public, StandardAero’s sensitivity to debt costs is acute: US corporate BAA yields rose from 4.1% in Jan 2024 to about 5.0% by Dec 2025, raising borrowing costs for expansions and MRO CAPEX.

By end-2025, sustained Fed funds around 5.25%–5.50% constrains feasibility of large-scale facility builds and turbine-tooling upgrades unless financed at higher rates or via equity.

Higher rates tighten leasing markets and working capital, with 2025 global airline CAPEX cuts of ~8% reported, increasing likelihood operators delay noncritical engine overhauls.

Global Fleet Expansion

Resurgent global air travel—projected at 4–5% annual RPK growth through 2025 with IATA estimating 2024 passenger numbers at ~95% of 2019 levels—has increased flight hours and engine cycles, boosting MRO demand; global commercial fleet hours rose ~8% year-over-year in 2023–24. This fleet expansion drives higher component shop visits and engine overhauls, directly lifting StandardAero’s service volumes. Given the firm’s exposure to commercial OEM and aftermarket segments, revenue growth closely tracks airline utilization trends and spare-part spend. StandardAero’s 2024 segment results showed aftermarket services growth consistent with industry utilization upticks.

Inflationary Pressure on Parts

Rising costs for specialty alloys and skilled labor have pushed engine-part prices up roughly 8–12% in 2024, increasing shop-visit spend per engine by an estimated $20k–$40k; StandardAero faces margin pressure as it weighs passing costs to customers while staying price-competitive with independent MROs.

Effective inventory turns and multiyear supplier agreements—StandardAero reported inventory up 6% in 2024—are key levers to hedge persistent inflation and stabilize input costs.

Currency Exchange Risk

With customers across North America, Europe and APAC, StandardAero faces material USD exposure: roughly 30–40% of 2024 service revenues originated in non-USD currencies, requiring active hedging to protect margins from sudden devaluations.

Revenue in EUR, CAD and AUD must be hedged; a 10% EUR depreciation versus USD could cut euro-denominated margin by ~3–5 percentage points for affected contracts.

Slower air travel recovery in emerging markets (2024 passenger traffic still 10–15% below 2019 in parts of LATAM/AFR) reduces local carriers’ purchasing power, pressuring aftermarket demand.

- 30–40% of 2024 service revenue non-USD

- 10% EUR move can reduce margins ~3–5ppt

- LATAM/AFR traffic 10–15% below 2019 in 2024

Labor Market Dynamics

StandardAero faces industry-wide shortages of skilled technicians and engineers, pushing average technician wages up about 8–12% between 2023–2025 and specialty engineer salaries up to mid-six figures in 2025.

To meet SLAs, StandardAero must offer competitive pay, benefits, and training; failure risks higher turnaround times and contract penalties.

Rising labor costs accounted for an increasing share of operating expenses, estimated at roughly 35–40% of total OPEX by late 2025.

- Technician wages +8–12% (2023–2025)

- Specialty engineers earning mid-six figures (2025)

- Labor ≈35–40% of OPEX by late 2025

- Competitive packages and training required to meet SLAs

Higher rates squeeze airline CAPEX; MRO demand up as RPKs recover, hedges essential

Higher interest rates (Fed 5.25–5.50% end‑2025; US BAA ~5.0%) raise borrowing costs, constraining CAPEX; airline CAPEX cut ~8% in 2025 shifts MRO timing. Strong RPK growth 4–5% and ~95% of 2019 passengers (2024) lift MRO demand, offsetting margin pressure from 8–12% input and labor cost inflation. FX exposure (30–40% non‑USD revenue) and inventory up 6% (2024) require active hedging and supplier contracts.

| Metric | 2024–25 |

|---|---|

| Fed funds | 5.25–5.50% |

| US BAA | ~5.0% |

| Airline CAPEX change | −8% (2025) |

| RPK growth | 4–5% pa |

| Input/labor inflation | +8–12% |

| Non‑USD revenue | 30–40% |

| Inventory change | +6% (2024) |

What You See Is What You Get

StandardAero PESTLE Analysis

The preview shown here is the exact StandardAero PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and detail visible in this preview are the same file you’ll download immediately after payment.