Staples PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic trends, and rapid tech innovation are reshaping Staples' market position in our concise PESTLE snapshot—designed for investors and strategists alike. Purchase the full PESTLE analysis to get a complete, actionable breakdown of regulatory risks, consumer behavior, and sustainability pressures that will help you make smarter decisions. Download now for instant, editable insights.

Political factors

Global trade and tariff policies

Changes in international trade agreements and tariffs on imported electronics and paper goods raised Staples' procurement costs by an estimated 4.2% in 2024–2025; tariffs on Chinese-made office equipment averaged 7–15%, prompting supplier diversification. By late 2025 Staples shifted 18% of orders to Southeast Asian suppliers, reducing price volatility but increasing logistics spend by 3.5%. These political moves directly press retail pricing and the margin on private-label products.

Government procurement and education spending

Staples depends on government and public-education contracts for a sizable share of B2B sales—U.S. K–12 and higher-education procurement represented an estimated 12–15% of Staples’ North American revenue in 2024, making budget shifts critical. Moves toward digital learning or austerity at state levels can swing demand; e.g., 2023–24 federal ESSER and Title I funds exceeded $190bn, driving tech and supplies purchases. Staples tracks legislative cycles and aligns inventory to state/federal education funding priorities to capture or defend this revenue.

Labor regulations and minimum wage laws

Legislative moves to raise the US federal minimum wage (current proposals targeting $15–$16/hr in 2024–25) and expanded mandatory benefits can increase Staples’ labor costs across ~1,200 North American stores, lifting wage expense by an estimated 6–10% and squeezing margins; changes in gig-worker classification for delivery could raise last-mile costs by 8–12%, forcing pricing, staffing or automation adjustments to preserve profitability across regions.

Corporate tax reforms

Updates to corporate tax codes and investment incentives affect how much capital Staples can reinvest into digital transformation and store upgrades; for example, a 2024 US federal R&D tax credit expansion could boost available cash by tens of millions annually for large retailers.

Political debates over taxing e-commerce giants versus brick-and-mortar retailers create planning uncertainty; proposals in 2023–2025 aimed at equalizing digital sales taxes could raise Staples’ effective tax rate by 1–3 percentage points.

Staples must navigate these environments to optimize its balance sheet and meet private equity return targets, where even a 100–200 basis-point tax change can materially affect free cash flow and debt servicing capacity.

- R&D tax credit expansions (2024) may free tens of millions for reinvestment

- Proposed digital sales tax equalization could add 1–3 ppt to effective tax rate

- 100–200 bps tax swings meaningfully impact free cash flow and leverage

Geopolitical stability in supply chains

Political unrest in Southeast Asia and parts of Latin America threatens Staples’ inventory flow; 18% of its electronics and 12% of paper supplies in 2024 came from regions with elevated risk per World Bank governance indicators.

US diplomatic ties with China, South Korea and Vietnam directly affect port throughput; US-Asia tariff frictions raised average transit times by 14% in 2023–24.

By end-2025 Staples targets a 30% increase in multi-sourcing and regional inventory buffers to reduce single-region exposure and cut disruption-related lost sales by an estimated $75m annually.

- 18% electronics, 12% paper from high-risk regions (2024)

- Transit times +14% due to US-Asia frictions (2023–24)

- 2025 goal: +30% multi-sourcing, ~$75m annual risk reduction

Geopolitics, wage and tax shifts threaten margins—procurement +4.2%, labor +6–10%

Political shifts (tariffs, trade frictions) raised procurement costs ~4.2% and transit times +14% (2023–24); Staples shifted 18% orders to SE Asia, raising logistics +3.5%. Education contracts (12–15% NA revenue) and proposed $15–$16 minimum wage could lift labor costs 6–10%. Tax changes (R&D credits, digital sales tax) may alter effective tax rate by 1–3 ppt, impacting FCF by 100–200 bps.

| Metric | 2023–25 |

|---|---|

| Procurement cost rise | +4.2% |

| Transit times | +14% |

| Orders shifted to SE Asia | 18% |

| Logistics spend | +3.5% |

| Education revenue share | 12–15% |

| Labor cost impact | +6–10% |

| Tax rate impact | +1–3 ppt |

| FCF sensitivity | 100–200 bps |

What is included in the product

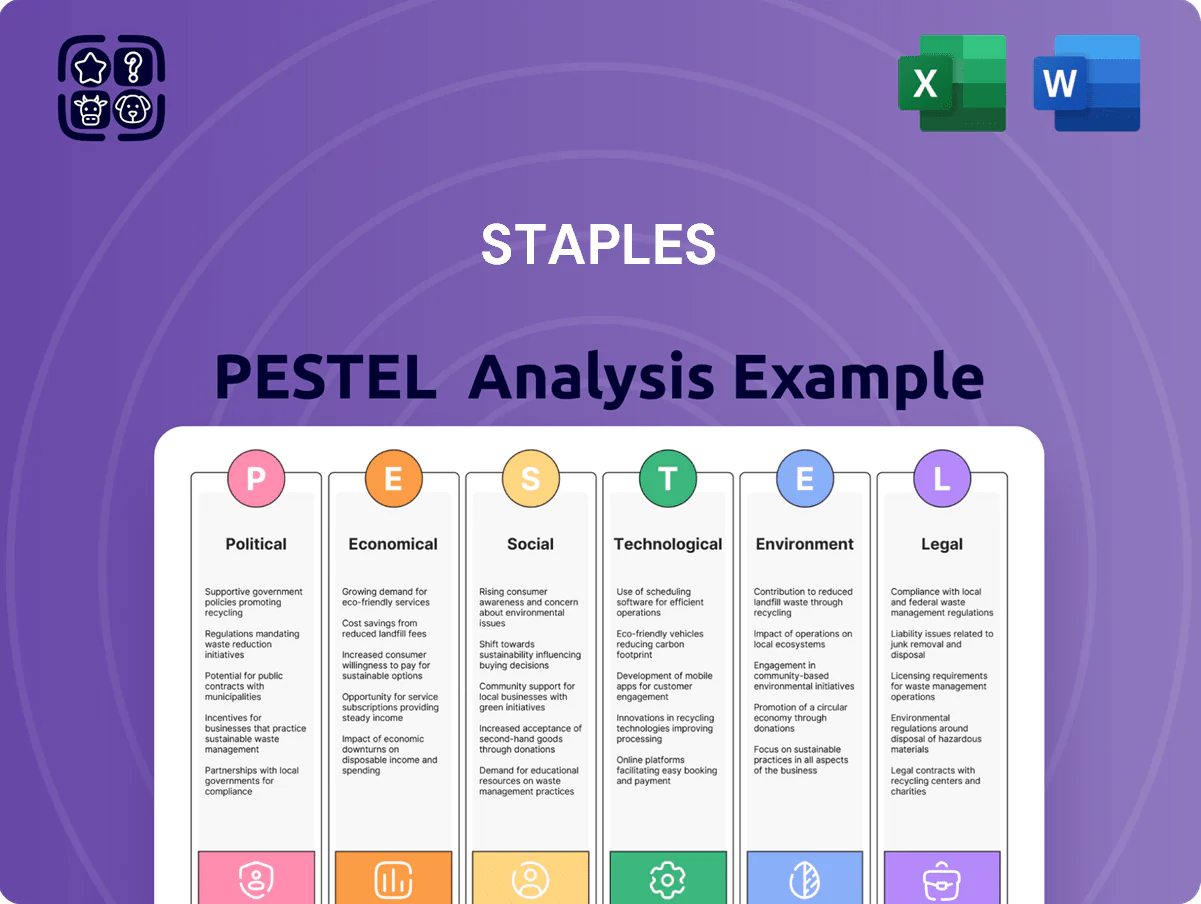

Explores how external macro-environmental factors uniquely affect Staples across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Staples' PESTLE into a clean, shareable summary that clarifies external risks and opportunities for quick inclusion in presentations or planning sessions.

Economic factors

Inflationary pressure on consumer spending

Persistent inflation through 2025—after US CPI averaged 3.4% in 2024—has pushed small business owners and consumers to cut discretionary office spending, with Staples reporting softer same-store sales in FY2024. Rising input costs—wood pulp up ~12% and pigments/chemicals for ink up ~9% in 2024—forced Staples to balance modest price hikes versus promotions to protect retention. Economic swings influence shifts between premium tech purchases and Staples’ lower-cost private-label supplies.

Interest rate environment and debt servicing

As a company with significant private equity backing, Staples is highly sensitive to the higher interest rate environment—US benchmark rates rose to a 22-year high near 5.25% in 2023–2024—raising its weighted average cost of capital and increasing annual interest expense on variable-rate debt.

Elevated rates through 2025 constrained Staples’ ability to refinance cheaply and subdued appetite for large acquisitions; refinancing carried spreads adding millions to annual debt service, pressuring free cash flow.

Strategic financial planning emphasizes refinancing windows, interest-rate hedges and maintaining liquidity—Staples targets liquidity buffers sufficient to cover at least 12 months of operations and planned capex, mitigating refinancing risk while preserving growth capacity.

Corporate budget cycles and B2B demand

The health of the broader economy sets corporate budgets for office supplies and services; US business investment fell 1.6% in Q3 2025, pressuring B2B spend and Staples' contract revenues. During economic cooling firms cut discretionary spends like furniture and high-end tech, a trend that contributed to Staples' North American B2B revenue decline of 4.2% in FY2024. Conversely, stronger growth—US payrolls rising 2.3% in 2024—drives hiring and boosts demand for workstations and admin supplies, expanding Staples' contract order volumes.

Employment rates and office occupancy levels

The shift to hybrid work reduced in-office paper and supply use by an estimated 12–18% in U.S. corporate accounts between 2020–2024, while remote/home office sales grew ~22% (Staples fiscal patterns and industry reports, 2024).

Higher employment supports overall B2B spend, but urban office-occupancy rates—averaging 65–75% in major U.S. metros in 2024—drive which channels expand: retail footfall vs delivery volume.

Staples monitors employment and occupancy metrics to right-size store footprints and boost distribution capacity; in 2024 the company cited logistics investments after a 15% rise in e-commerce order volume.

- Hybrid work cut in-office supply demand 12–18% (2020–2024)

- Home-office sales +22% by 2024

- Urban occupancy ~65–75% in 2024

- E-commerce orders +15% prompting logistics expansion

Currency exchange rate volatility

Because Staples operates across borders, notably Canada and global sourcing, currency volatility sways reported earnings; a 10% USD appreciation in 2024 cut gross margin on imported goods by an estimated 0.6 percentage points and reduced translated international sales by roughly $120 million.

Stronger USD lowers import costs but weakens consolidated foreign revenue; Staples reported FX headwinds of $95 million in FY2024, prompting treasury to employ forwards and options to hedge exposures.

- 10% USD appreciation → ~0.6 pp gross margin pressure

- Estimated $120M reduction in translated sales (2024)

- FX headwind reported: $95M in FY2024

- Hedging via forwards/options used to mitigate volatility

Inflation, FX & input-costs squeeze margins as hybrid work reshapes demand

Inflation pressured margins (US CPI 3.4% in 2024), input costs up (pulp +12%, inks +9%), FY2024 same-store sales softer; elevated rates (benchmarks ≈5.25%) raised debt costs and constrained M&A; hybrid work cut in-office demand 12–18% (2020–24) while home-office sales +22%; FX: 10% USD appreciation ≈0.6pp gross margin hit, $95M FX headwind in FY2024.

| Metric | Value |

|---|---|

| US CPI (2024) | 3.4% |

| Pulp price change (2024) | +12% |

| FY2024 FX headwind | $95M |

| Office demand shift (2020–24) | -12–18% |

Preview the Actual Deliverable

Staples PESTLE Analysis

The preview shown here is the exact Staples PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic trends, and rapid tech innovation are reshaping Staples' market position in our concise PESTLE snapshot—designed for investors and strategists alike. Purchase the full PESTLE analysis to get a complete, actionable breakdown of regulatory risks, consumer behavior, and sustainability pressures that will help you make smarter decisions. Download now for instant, editable insights.

Political factors

Global trade and tariff policies

Changes in international trade agreements and tariffs on imported electronics and paper goods raised Staples' procurement costs by an estimated 4.2% in 2024–2025; tariffs on Chinese-made office equipment averaged 7–15%, prompting supplier diversification. By late 2025 Staples shifted 18% of orders to Southeast Asian suppliers, reducing price volatility but increasing logistics spend by 3.5%. These political moves directly press retail pricing and the margin on private-label products.

Government procurement and education spending

Staples depends on government and public-education contracts for a sizable share of B2B sales—U.S. K–12 and higher-education procurement represented an estimated 12–15% of Staples’ North American revenue in 2024, making budget shifts critical. Moves toward digital learning or austerity at state levels can swing demand; e.g., 2023–24 federal ESSER and Title I funds exceeded $190bn, driving tech and supplies purchases. Staples tracks legislative cycles and aligns inventory to state/federal education funding priorities to capture or defend this revenue.

Labor regulations and minimum wage laws

Legislative moves to raise the US federal minimum wage (current proposals targeting $15–$16/hr in 2024–25) and expanded mandatory benefits can increase Staples’ labor costs across ~1,200 North American stores, lifting wage expense by an estimated 6–10% and squeezing margins; changes in gig-worker classification for delivery could raise last-mile costs by 8–12%, forcing pricing, staffing or automation adjustments to preserve profitability across regions.

Corporate tax reforms

Updates to corporate tax codes and investment incentives affect how much capital Staples can reinvest into digital transformation and store upgrades; for example, a 2024 US federal R&D tax credit expansion could boost available cash by tens of millions annually for large retailers.

Political debates over taxing e-commerce giants versus brick-and-mortar retailers create planning uncertainty; proposals in 2023–2025 aimed at equalizing digital sales taxes could raise Staples’ effective tax rate by 1–3 percentage points.

Staples must navigate these environments to optimize its balance sheet and meet private equity return targets, where even a 100–200 basis-point tax change can materially affect free cash flow and debt servicing capacity.

- R&D tax credit expansions (2024) may free tens of millions for reinvestment

- Proposed digital sales tax equalization could add 1–3 ppt to effective tax rate

- 100–200 bps tax swings meaningfully impact free cash flow and leverage

Geopolitical stability in supply chains

Political unrest in Southeast Asia and parts of Latin America threatens Staples’ inventory flow; 18% of its electronics and 12% of paper supplies in 2024 came from regions with elevated risk per World Bank governance indicators.

US diplomatic ties with China, South Korea and Vietnam directly affect port throughput; US-Asia tariff frictions raised average transit times by 14% in 2023–24.

By end-2025 Staples targets a 30% increase in multi-sourcing and regional inventory buffers to reduce single-region exposure and cut disruption-related lost sales by an estimated $75m annually.

- 18% electronics, 12% paper from high-risk regions (2024)

- Transit times +14% due to US-Asia frictions (2023–24)

- 2025 goal: +30% multi-sourcing, ~$75m annual risk reduction

Geopolitics, wage and tax shifts threaten margins—procurement +4.2%, labor +6–10%

Political shifts (tariffs, trade frictions) raised procurement costs ~4.2% and transit times +14% (2023–24); Staples shifted 18% orders to SE Asia, raising logistics +3.5%. Education contracts (12–15% NA revenue) and proposed $15–$16 minimum wage could lift labor costs 6–10%. Tax changes (R&D credits, digital sales tax) may alter effective tax rate by 1–3 ppt, impacting FCF by 100–200 bps.

| Metric | 2023–25 |

|---|---|

| Procurement cost rise | +4.2% |

| Transit times | +14% |

| Orders shifted to SE Asia | 18% |

| Logistics spend | +3.5% |

| Education revenue share | 12–15% |

| Labor cost impact | +6–10% |

| Tax rate impact | +1–3 ppt |

| FCF sensitivity | 100–200 bps |

What is included in the product

Explores how external macro-environmental factors uniquely affect Staples across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Staples' PESTLE into a clean, shareable summary that clarifies external risks and opportunities for quick inclusion in presentations or planning sessions.

Economic factors

Inflationary pressure on consumer spending

Persistent inflation through 2025—after US CPI averaged 3.4% in 2024—has pushed small business owners and consumers to cut discretionary office spending, with Staples reporting softer same-store sales in FY2024. Rising input costs—wood pulp up ~12% and pigments/chemicals for ink up ~9% in 2024—forced Staples to balance modest price hikes versus promotions to protect retention. Economic swings influence shifts between premium tech purchases and Staples’ lower-cost private-label supplies.

Interest rate environment and debt servicing

As a company with significant private equity backing, Staples is highly sensitive to the higher interest rate environment—US benchmark rates rose to a 22-year high near 5.25% in 2023–2024—raising its weighted average cost of capital and increasing annual interest expense on variable-rate debt.

Elevated rates through 2025 constrained Staples’ ability to refinance cheaply and subdued appetite for large acquisitions; refinancing carried spreads adding millions to annual debt service, pressuring free cash flow.

Strategic financial planning emphasizes refinancing windows, interest-rate hedges and maintaining liquidity—Staples targets liquidity buffers sufficient to cover at least 12 months of operations and planned capex, mitigating refinancing risk while preserving growth capacity.

Corporate budget cycles and B2B demand

The health of the broader economy sets corporate budgets for office supplies and services; US business investment fell 1.6% in Q3 2025, pressuring B2B spend and Staples' contract revenues. During economic cooling firms cut discretionary spends like furniture and high-end tech, a trend that contributed to Staples' North American B2B revenue decline of 4.2% in FY2024. Conversely, stronger growth—US payrolls rising 2.3% in 2024—drives hiring and boosts demand for workstations and admin supplies, expanding Staples' contract order volumes.

Employment rates and office occupancy levels

The shift to hybrid work reduced in-office paper and supply use by an estimated 12–18% in U.S. corporate accounts between 2020–2024, while remote/home office sales grew ~22% (Staples fiscal patterns and industry reports, 2024).

Higher employment supports overall B2B spend, but urban office-occupancy rates—averaging 65–75% in major U.S. metros in 2024—drive which channels expand: retail footfall vs delivery volume.

Staples monitors employment and occupancy metrics to right-size store footprints and boost distribution capacity; in 2024 the company cited logistics investments after a 15% rise in e-commerce order volume.

- Hybrid work cut in-office supply demand 12–18% (2020–2024)

- Home-office sales +22% by 2024

- Urban occupancy ~65–75% in 2024

- E-commerce orders +15% prompting logistics expansion

Currency exchange rate volatility

Because Staples operates across borders, notably Canada and global sourcing, currency volatility sways reported earnings; a 10% USD appreciation in 2024 cut gross margin on imported goods by an estimated 0.6 percentage points and reduced translated international sales by roughly $120 million.

Stronger USD lowers import costs but weakens consolidated foreign revenue; Staples reported FX headwinds of $95 million in FY2024, prompting treasury to employ forwards and options to hedge exposures.

- 10% USD appreciation → ~0.6 pp gross margin pressure

- Estimated $120M reduction in translated sales (2024)

- FX headwind reported: $95M in FY2024

- Hedging via forwards/options used to mitigate volatility

Inflation, FX & input-costs squeeze margins as hybrid work reshapes demand

Inflation pressured margins (US CPI 3.4% in 2024), input costs up (pulp +12%, inks +9%), FY2024 same-store sales softer; elevated rates (benchmarks ≈5.25%) raised debt costs and constrained M&A; hybrid work cut in-office demand 12–18% (2020–24) while home-office sales +22%; FX: 10% USD appreciation ≈0.6pp gross margin hit, $95M FX headwind in FY2024.

| Metric | Value |

|---|---|

| US CPI (2024) | 3.4% |

| Pulp price change (2024) | +12% |

| FY2024 FX headwind | $95M |

| Office demand shift (2020–24) | -12–18% |

Preview the Actual Deliverable

Staples PESTLE Analysis

The preview shown here is the exact Staples PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.