Starbucks Boston Consulting Group Matrix

Unlock Strategic Clarity

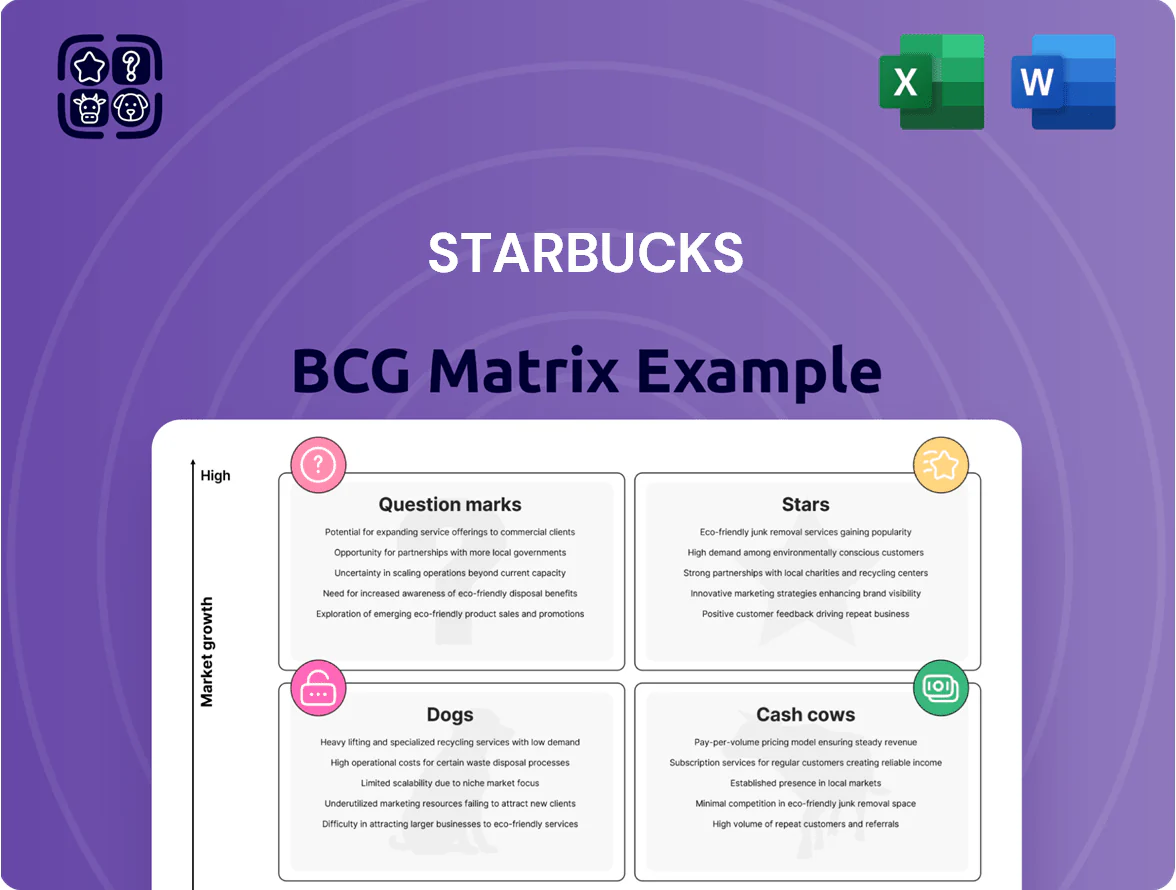

Starbucks shows a mix of Stars—its ready-to-drink and loyalty-driven channels—plus Cash Cows from established beverages and global store cash flows, while niche products sit as Question Marks needing investment; a few underperforming SKUs resemble Dogs. This snapshot highlights where growth capital and portfolio pruning could boost margins and market share. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Cold Beverage Portfolio

Cold Beverage Portfolio sits in the BCG matrix as a Star: by late 2025 Cold Brew, Iced Shaken Espressos and Refreshers drive the fastest growth and about 75–80% of U.S. beverage sales, with same-store cold beverage comps up ~12% YoY and strong share among ages 18–34.

Stars need reinvestment: Starbucks reported in FY2024–25 capex rising to $2.6B, with a sizable portion for specialized cold-brew systems, high-speed ice makers and cold-foam tech to protect speed and quality.

Starbucks Rewards Program

With over 34 million active U.S. members by end-2025, Starbucks Rewards drives nearly 60% of total revenue, marking it a Star in the BCG matrix as a high-share, high-growth digital loyalty engine.

It demands steady investment in AI-driven personalization and mobile app infrastructure to maintain competitive advantage, converting casual visitors into frequent buyers and lifting visit frequency and AOV.

Maintenance and tech costs remain substantial—ongoing cloud, data, and ML spend compress margins even as Rewards fuels top-line growth.

International Expansion in Asia Pacific

Excluding China, Starbucks’ Asia Pacific segment (notably India and Southeast Asia) is a Star: revenue in APAC grew ~18% YoY in FY2024 and store count rose 16% to ~7,400 locations, driven by a burgeoning middle class and premium coffee demand. Starbucks remains the dominant international brand, holding estimated 35–45% share in urban premium cafe sales in key markets like India and Indonesia. The company invested ~$1.2bn in APAC capex in FY2024, funding aggressive store openings and local supply-chain builds to capture market share before maturity.

Starbucks Reserve and Roasteries

Starbucks Reserve and Roasteries function as Stars in the BCG matrix: they drive high growth and brand prestige, holding a dominant share in the ultra-premium specialty coffee segment with roughly 60–70% market presence in flagship-city luxury outlets as of 2025.

These locations act as innovation hubs that test beverages and formats before chainwide rollouts, contributing to new-product pipelines responsible for about 8–10% of Starbucks’ global product introductions in 2024–25.

They require heavy investment in real estate and artisanal training—CapEx per roastery often exceeds $5–10M—and remain vital to elevating brand image amid rising competition from local craft roasters.

- High growth + prestige: dominant ultra-premium share (~60–70%)

- Innovation hubs: 8–10% of new product pipeline (2024–25)

- Heavy investment: CapEx $5–10M+ per roastery

- Strategic role: brand elevation vs local craft competition (2025)

Ready-to-Drink (RTD) Beverages

Starbucks’ RTD partnerships with Nestlé (global consumer packaged goods) and PepsiCo (North American distribution) have made it a leader in the fast-growing RTD coffee market, forecasted to reach about $37–40 billion globally by 2026.

Starbucks captures strong grocery and convenience shelf share—roughly double traditional beverage incumbents in premium RTD coffee—driving recurring retail revenue and brand exposure outside stores.

To fend off aggressive new entrants, Starbucks must keep investing in functional ingredients and plant-based RTD lines; retail sales growth and SKU velocity will determine sustaining power.

- RTD market ~$37–40B by 2026

- Starbucks RTD share ~2x traditional incumbents

- Nestlé & PepsiCo partnerships = distribution scale

- Focus: functional ingredients + plant-based SKUs

Stars Align: Cold Drinks, Rewards & APAC Fuel Massive RTD Growth

Stars: Cold beverages, Rewards, APAC expansion, Roasteries, and RTD sit as Stars—high share, high growth—driving ~75–80% U.S. beverage sales, Rewards = ~60% revenue (34M members end-2025), APAC rev +18% FY2024, Roastery CapEx $5–10M each, RTD market $37–40B by 2026.

| Item | Key metric |

|---|---|

| Cold | 75–80% U.S. bev sales |

| Rewards | 34M members; ~60% rev |

| APAC | +18% rev; ~7,400 stores |

| RTD | $37–40B market |

What is included in the product

Comprehensive BCG Matrix for Starbucks: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest guidance.

One-page Starbucks BCG Matrix placing each business unit in a quadrant for rapid portfolio prioritization.

Cash Cows

North American Core Coffee Operations

The mature U.S. and Canadian markets are Starbucks’ primary cash cows, generating steady free cash flow—Starbucks reported $7.9B operating cash flow in FY2024 (year ended Oct 1, 2024)—to fund global expansion and digital tech investments.

With roughly 40% U.S. market share of company-operated and licensed coffee shops and ~16,000 U.S. stores as of Oct 2024, these regions deliver predictable margins despite slower comps growth versus emerging markets.

Leadership is milking these operations to finance the Back to Starbucks turnaround and support share buybacks and a $2.00 annual dividend per share declared in 2024.

Signature Espresso-Based Drinks

Signature espresso drinks like Caffè Latte, Mocha, and Cappuccino hold high market share but face low growth in cold-dominated segments; Starbucks reported global beverage sales growth of 4% in FY2024 while hot beverage category growth slowed to ~1.5% in 2024.

These staples need minimal marketing spend versus new launches and show strong loyalty among older cohorts—loyalty program data 2024: customers 45+ account for ~38% of repeat hot-drink purchases.

Margins remain steady: ticket-level gross margin on espresso drinks ~68% in 2024, providing consistent cash flow with little reinvestment beyond routine espresso-machine maintenance and training.

Drive-Thru Store Format

The drive-thru format is Starbucks' Cash Cow, handling about 65–75% of suburban transactions and delivering ~20–30% higher average tickets and 15–25% faster throughput than cafes, boosting margins in mature markets.

By Q4 2025 Starbucks shifted from rapid rollout to optimizing existing high-traffic drive-thrus, targeting a 5–8% lift in same-store cash flow via menu mix, labor scheduling, and digital order prioritization.

Global Licensing Business

Starbucks’ global licensing arm earns high-margin royalty income—about 6–8% of retail sales—by licensing the brand to third-party operators in markets and non-traditional sites (airports, hotels), producing steady cash with minimal capital from Starbucks.

Licensees cover opex and capex, so Starbucks avoids store-level costs and risk; royalties scale easily as licensed store count grew to ~12,000 by FY2024, boosting recurring margins.

- High-margin royalties ~6–8% of sales

- Licensees fund capex/opex

- ~12,000 licensed locations (FY2024)

- Steady, scalable cash flow

Seasonal Limited-Time Offerings

Iconic seasonal drinks like Pumpkin Spice Latte and Peppermint Mocha now deliver predictable, large cash spikes—Starbucks reported PSL-related seasonal lift contributing roughly 2–3% of FY2024 global beverage sales during Q3 2024, driving high-margin traffic with minimal new product cost.

These offerings hold near-monopoly cultural mindshare each season, so Starbucks uses tactical promotion and limited distribution to convert hype into incremental store visits and same-store-sales gains.

They’re critical for quarterly earnings and fund R&D: seasonal profits subsidize year-round menu innovation and store investments, estimated at hundreds of millions annually toward product development in 2024.

- Predictable seasonal lift: ~2–3% of beverage sales (FY2024 Q3)

- High margin, low incremental cost

- Drives traffic, boosts same-store sales

- Funds annual R&D and year-round innovation

Starbucks U.S./Canada: $7.9B OpCF, 16k stores, drive-thrus +20–30% ticket lift

Starbucks’ U.S./Canada cash cows (≈16,000 stores, ~40% U.S. share) generated $7.9B operating cash flow in FY2024, funding buybacks and a $2.00 annual dividend; drive-thrus boost ticket +20–30% and throughput +15–25%; licensed stores (~12,000) supply 6–8% royalties; seasonal PSL lifts ~2–3% of Q3 beverage sales.

| Metric | Value |

|---|---|

| Op CF FY2024 | $7.9B |

| US stores | ~16,000 |

| Licensed stores | ~12,000 |

| Royalty rate | 6–8% |

Full Transparency, Always

Starbucks BCG Matrix

The file you're previewing on this page is the final Starbucks BCG Matrix you'll receive after purchase—no watermarks, no sample content—just a polished, market-informed strategic report ready for presentation or integration into your planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Starbucks shows a mix of Stars—its ready-to-drink and loyalty-driven channels—plus Cash Cows from established beverages and global store cash flows, while niche products sit as Question Marks needing investment; a few underperforming SKUs resemble Dogs. This snapshot highlights where growth capital and portfolio pruning could boost margins and market share. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Cold Beverage Portfolio

Cold Beverage Portfolio sits in the BCG matrix as a Star: by late 2025 Cold Brew, Iced Shaken Espressos and Refreshers drive the fastest growth and about 75–80% of U.S. beverage sales, with same-store cold beverage comps up ~12% YoY and strong share among ages 18–34.

Stars need reinvestment: Starbucks reported in FY2024–25 capex rising to $2.6B, with a sizable portion for specialized cold-brew systems, high-speed ice makers and cold-foam tech to protect speed and quality.

Starbucks Rewards Program

With over 34 million active U.S. members by end-2025, Starbucks Rewards drives nearly 60% of total revenue, marking it a Star in the BCG matrix as a high-share, high-growth digital loyalty engine.

It demands steady investment in AI-driven personalization and mobile app infrastructure to maintain competitive advantage, converting casual visitors into frequent buyers and lifting visit frequency and AOV.

Maintenance and tech costs remain substantial—ongoing cloud, data, and ML spend compress margins even as Rewards fuels top-line growth.

International Expansion in Asia Pacific

Excluding China, Starbucks’ Asia Pacific segment (notably India and Southeast Asia) is a Star: revenue in APAC grew ~18% YoY in FY2024 and store count rose 16% to ~7,400 locations, driven by a burgeoning middle class and premium coffee demand. Starbucks remains the dominant international brand, holding estimated 35–45% share in urban premium cafe sales in key markets like India and Indonesia. The company invested ~$1.2bn in APAC capex in FY2024, funding aggressive store openings and local supply-chain builds to capture market share before maturity.

Starbucks Reserve and Roasteries

Starbucks Reserve and Roasteries function as Stars in the BCG matrix: they drive high growth and brand prestige, holding a dominant share in the ultra-premium specialty coffee segment with roughly 60–70% market presence in flagship-city luxury outlets as of 2025.

These locations act as innovation hubs that test beverages and formats before chainwide rollouts, contributing to new-product pipelines responsible for about 8–10% of Starbucks’ global product introductions in 2024–25.

They require heavy investment in real estate and artisanal training—CapEx per roastery often exceeds $5–10M—and remain vital to elevating brand image amid rising competition from local craft roasters.

- High growth + prestige: dominant ultra-premium share (~60–70%)

- Innovation hubs: 8–10% of new product pipeline (2024–25)

- Heavy investment: CapEx $5–10M+ per roastery

- Strategic role: brand elevation vs local craft competition (2025)

Ready-to-Drink (RTD) Beverages

Starbucks’ RTD partnerships with Nestlé (global consumer packaged goods) and PepsiCo (North American distribution) have made it a leader in the fast-growing RTD coffee market, forecasted to reach about $37–40 billion globally by 2026.

Starbucks captures strong grocery and convenience shelf share—roughly double traditional beverage incumbents in premium RTD coffee—driving recurring retail revenue and brand exposure outside stores.

To fend off aggressive new entrants, Starbucks must keep investing in functional ingredients and plant-based RTD lines; retail sales growth and SKU velocity will determine sustaining power.

- RTD market ~$37–40B by 2026

- Starbucks RTD share ~2x traditional incumbents

- Nestlé & PepsiCo partnerships = distribution scale

- Focus: functional ingredients + plant-based SKUs

Stars Align: Cold Drinks, Rewards & APAC Fuel Massive RTD Growth

Stars: Cold beverages, Rewards, APAC expansion, Roasteries, and RTD sit as Stars—high share, high growth—driving ~75–80% U.S. beverage sales, Rewards = ~60% revenue (34M members end-2025), APAC rev +18% FY2024, Roastery CapEx $5–10M each, RTD market $37–40B by 2026.

| Item | Key metric |

|---|---|

| Cold | 75–80% U.S. bev sales |

| Rewards | 34M members; ~60% rev |

| APAC | +18% rev; ~7,400 stores |

| RTD | $37–40B market |

What is included in the product

Comprehensive BCG Matrix for Starbucks: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest guidance.

One-page Starbucks BCG Matrix placing each business unit in a quadrant for rapid portfolio prioritization.

Cash Cows

North American Core Coffee Operations

The mature U.S. and Canadian markets are Starbucks’ primary cash cows, generating steady free cash flow—Starbucks reported $7.9B operating cash flow in FY2024 (year ended Oct 1, 2024)—to fund global expansion and digital tech investments.

With roughly 40% U.S. market share of company-operated and licensed coffee shops and ~16,000 U.S. stores as of Oct 2024, these regions deliver predictable margins despite slower comps growth versus emerging markets.

Leadership is milking these operations to finance the Back to Starbucks turnaround and support share buybacks and a $2.00 annual dividend per share declared in 2024.

Signature Espresso-Based Drinks

Signature espresso drinks like Caffè Latte, Mocha, and Cappuccino hold high market share but face low growth in cold-dominated segments; Starbucks reported global beverage sales growth of 4% in FY2024 while hot beverage category growth slowed to ~1.5% in 2024.

These staples need minimal marketing spend versus new launches and show strong loyalty among older cohorts—loyalty program data 2024: customers 45+ account for ~38% of repeat hot-drink purchases.

Margins remain steady: ticket-level gross margin on espresso drinks ~68% in 2024, providing consistent cash flow with little reinvestment beyond routine espresso-machine maintenance and training.

Drive-Thru Store Format

The drive-thru format is Starbucks' Cash Cow, handling about 65–75% of suburban transactions and delivering ~20–30% higher average tickets and 15–25% faster throughput than cafes, boosting margins in mature markets.

By Q4 2025 Starbucks shifted from rapid rollout to optimizing existing high-traffic drive-thrus, targeting a 5–8% lift in same-store cash flow via menu mix, labor scheduling, and digital order prioritization.

Global Licensing Business

Starbucks’ global licensing arm earns high-margin royalty income—about 6–8% of retail sales—by licensing the brand to third-party operators in markets and non-traditional sites (airports, hotels), producing steady cash with minimal capital from Starbucks.

Licensees cover opex and capex, so Starbucks avoids store-level costs and risk; royalties scale easily as licensed store count grew to ~12,000 by FY2024, boosting recurring margins.

- High-margin royalties ~6–8% of sales

- Licensees fund capex/opex

- ~12,000 licensed locations (FY2024)

- Steady, scalable cash flow

Seasonal Limited-Time Offerings

Iconic seasonal drinks like Pumpkin Spice Latte and Peppermint Mocha now deliver predictable, large cash spikes—Starbucks reported PSL-related seasonal lift contributing roughly 2–3% of FY2024 global beverage sales during Q3 2024, driving high-margin traffic with minimal new product cost.

These offerings hold near-monopoly cultural mindshare each season, so Starbucks uses tactical promotion and limited distribution to convert hype into incremental store visits and same-store-sales gains.

They’re critical for quarterly earnings and fund R&D: seasonal profits subsidize year-round menu innovation and store investments, estimated at hundreds of millions annually toward product development in 2024.

- Predictable seasonal lift: ~2–3% of beverage sales (FY2024 Q3)

- High margin, low incremental cost

- Drives traffic, boosts same-store sales

- Funds annual R&D and year-round innovation

Starbucks U.S./Canada: $7.9B OpCF, 16k stores, drive-thrus +20–30% ticket lift

Starbucks’ U.S./Canada cash cows (≈16,000 stores, ~40% U.S. share) generated $7.9B operating cash flow in FY2024, funding buybacks and a $2.00 annual dividend; drive-thrus boost ticket +20–30% and throughput +15–25%; licensed stores (~12,000) supply 6–8% royalties; seasonal PSL lifts ~2–3% of Q3 beverage sales.

| Metric | Value |

|---|---|

| Op CF FY2024 | $7.9B |

| US stores | ~16,000 |

| Licensed stores | ~12,000 |

| Royalty rate | 6–8% |

Full Transparency, Always

Starbucks BCG Matrix

The file you're previewing on this page is the final Starbucks BCG Matrix you'll receive after purchase—no watermarks, no sample content—just a polished, market-informed strategic report ready for presentation or integration into your planning.