Star Health and Allied Insurance Boston Consulting Group Matrix

Unlock Strategic Clarity

Star Health and Allied Insurance shows strong growth potential in retail health products but faces margin pressure from high claims and competition, placing select offerings between Stars and Question Marks; legacy group plans resemble Cash Cows with steady premiums yet limited upside. Purchase the full BCG Matrix for a complete quadrant mapping, data-backed prioritization, and actionable strategies to optimize capital allocation and product focus—delivered in Word + Excel for immediate use.

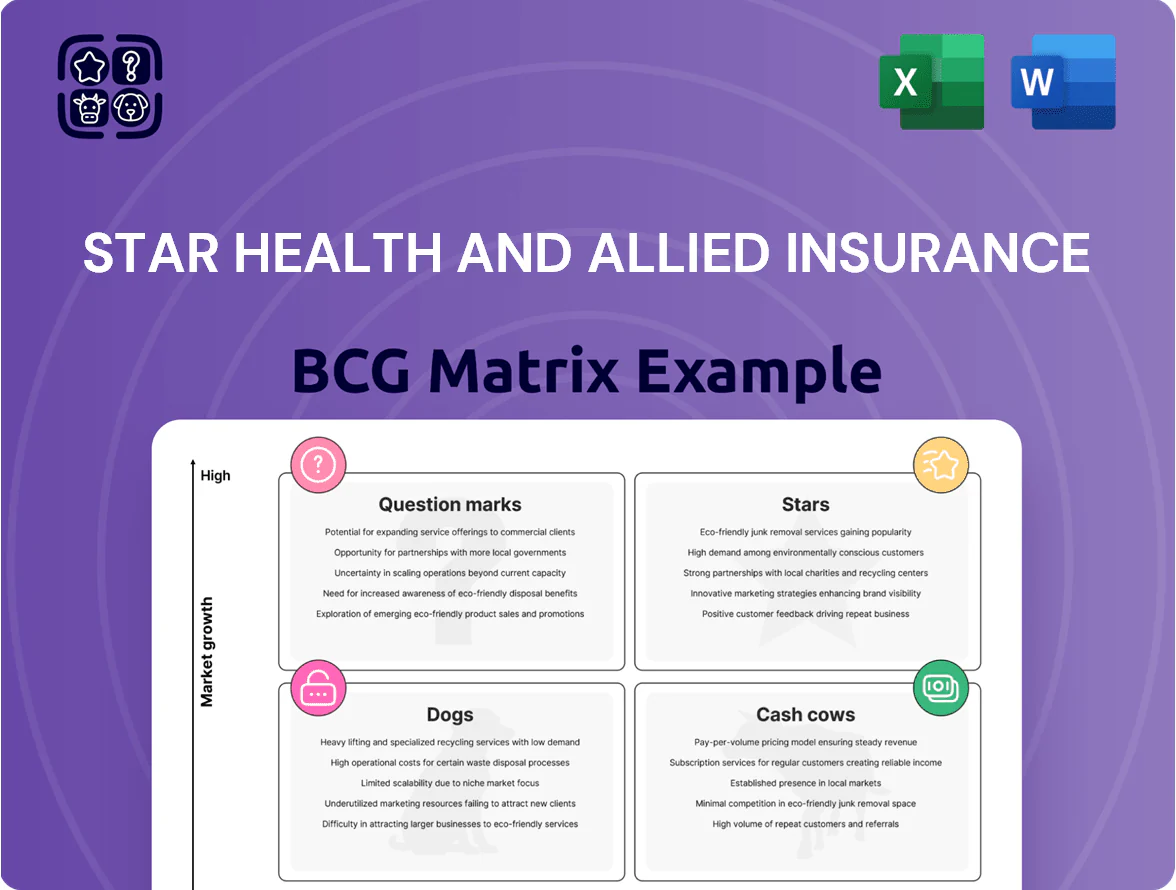

Stars

Retail Health Insurance Segment

As of late 2025, Star Health and Allied Insurance’s retail health segment drives growth, holding roughly 18–20% market share in India’s individual and family floater market and contributing about 55% of company GWP (gross written premium) in FY2024–25.

Rising medical inflation near 9–11% and higher health awareness push retail premium growth of ~14–16% YoY, forcing sustained spend: marketing rose to ~9% of retail premiums and hospital empanelment costs climbed 22% in 2025.

The segment delivers most revenue but ties up capital—combined acquisition and network investment absorbed an estimated 28–30% of operating cash flow in 2025—while private rivals (Bajaj, HDFC Ergo) intensify price and service competition.

Specialized Disease Specific Plans

Star Health and Allied Insurance pioneered disease-specific plans for diabetes and cardiac care, tapping a rising need as India’s 60+ population grew to 8.6% in 2023 and diabetes prevalence hit 8.9% in 2024 (IDA). These niche plans hold a leading share in specialty retail health segments and show double-digit premium growth—Star’s chronic-care line reported ~18% YoY premium growth in FY2024. With unit economics improving, these products are high-growth candidates moving toward future cash cows. Continued investment in specialized underwriting and tie-ups with 2,100+ empanelled hospitals is essential to sustain margins.

Senior Citizen Red Carpet Policy

Star Health and Allied Insurance’s Senior Citizen Red Carpet policy is a star in the BCG matrix: with India’s 60+ population hitting 152 million in 2025 (UN DESA) and life expectancy at 70.8 years (WHO 2024), demand is rising and Star Health gained first-mover advantage in the segment.

The Red Carpet product commands higher average premiums—reported blended premium per policy ~INR 18,000 in FY2024—and attracts seniors who prioritize comprehensive cover over price.

To retain star status, Star Health must sustain >90% customer satisfaction and process claims within target TATs; FY2024 claims ratio for senior products rose ~8 percentage points vs. general book, so efficient claims handling is critical.

Comprehensive Health Insurance Products

Comprehensive plans with maternity, dental, and ophthalmic cover have become stars for Star Health and Allied Insurance, driven by a 28% CAGR in premium income for these products from FY2020–FY2024 and 18% market share in urban retail health by 2024.

Consumers accept 15–25% higher premiums for all‑inclusive protection, pushing claims-adjusted revenue up 32% YoY in FY2024 and prompting the firm to expand product bundles and distribution in metros.

Star Health is investing in marketing and tech for these premium lines to win wallet share among the rising middle class and affluent urban households, which grew 22% in number from 2019–2024.

- 28% CAGR premium income (FY2020–FY2024)

- 18% urban retail health market share (2024)

- 15–25% premium uplift for all‑inclusive plans

- 32% claims‑adjusted revenue growth YoY (FY2024)

Digital and App Based Distribution

Star Health's proprietary digital platforms and mobile apps became a star by end-2025, driving 28% of new policy issuance (up from 9% in 2022) and cutting reliance on physical agents by 35%.

The firm committed ₹450 crore in 2024–25 to UX upgrades and AI-driven claim/chat automation, boosting conversion rates to 6.8% and lowering CAC by 22%.

- 28% new policies via digital (2025)

- Agent reliance down 35%

- ₹450 crore capex on digital (2024–25)

- Conversion 6.8%; CAC −22%

Star Health: Retail & Senior 'BCG Stars'—55% GWP, 18–20% share; digital 28%, ₹450cr capex

Star Health’s retail and senior products are BCG Stars: retail ~55% GWP, 18–20% indy market share (2025); Senior Red Carpet premium ~INR 18,000 (FY2024); chronic-care +18% YoY (FY2024); digital sales 28% (2025), ₹450 crore capex (2024–25). Efficient claims and continued investment required to convert to cash cows.

| Metric | Value |

|---|---|

| Retail GWP% | ~55% |

| Indy market share | 18–20% |

| Senior avg premium | INR 18,000 |

| Chronic YoY | ~18% |

| Digital new sales | 28% |

| Digital capex | ₹450 cr |

What is included in the product

BCG Matrix analysis of Star Health and Allied Insurance: strategic guidance on Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest moves.

One-page overview placing each Star Health business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Group Health Insurance Portfolio

Group health insurance is a mature segment where Star Health and Allied Insurance holds a high market share—about 18% of India’s corporate health premiums in FY2024—despite intense price competition.

Growth here lags retail (corporate CAGR ~4% vs retail ~12% 2021–24), but large corporate contracts deliver steady cash flows with minimal incremental marketing costs.

Liquidity from these accounts funded ~₹120 crore in R&D and pilot products in FY2024, supporting innovation in the company’s question-mark lines.

Personal Accident Insurance

Personal accident covers at Star Health and Allied Insurance are a mature product line with high market share and low growth, fitting the BCG cash cow profile; industry premium growth for personal accident was ~3% in 2024 while Star Health reported ~15% share in retail accident lines in FY2024 (source: IR and IRDAI reports).

This segment yields high margins due to low claim frequency—industry claim ratios for personal accident averaged ~28% in 2024—plus established underwriting and pricing models that keep loss ratios favorable for Star Health.

Star Health prioritizes harvesting cash flows from personal accident products to fund operations and dividends, with net earned premium from miscellaneous retail lines contributing an estimated 8–10% of group GPW in FY2024, bolstering liquidity and dividend capacity.

Standard Indemnity Plans

Standard indemnity plans, like the regulated Arogya Sanjeevani (mandatory since 2020), act as cash cows—covering ~55–60% of Star Health and Allied Insurance’s retail book in 2024 and delivering steady combined ratios near 95%, thanks to scale and price regulation.

Renewal Premium Book

Renewal Premium Book: Star Health's large existing policyholder base generated about INR 7,200 crore in renewal premiums in FY2024–25, making it a strong cash cow with low acquisition cost and high margins.

Renewals cut acquisition spend by ~60% versus new business, delivering steady cash inflows that support servicing ~INR 1,500 crore corporate debt and fund R&D in health tech initiatives.

- INR 7,200 crore renewal premiums FY2024–25

- ~60% lower acquisition cost vs new business

- ~INR 1,500 crore debt service supported

- Funds allocated to health tech R&D from cash flows

Agency Network Distribution

Star Health's agency network is a mature, dominant distribution channel delivering steady premiums—agents contributed about 52% of gross written premium (GWP) in FY2024, making it a primary cash cow with high market share and reliable returns.

Growth in agency-sourced business has slowed as digital channels rose (digital accounted for ~18% of GWP in FY2024), so management prioritizes productivity gains over expansion to sustain margins and retention.

Focus is on milking existing infrastructure: higher agent productivity, targeted training, and cross-sell drives stable cash flow and ROE support for underwriting and reserves.

- Agents = ~52% GWP (FY2024)

- Digital = ~18% GWP (FY2024)

- Strategy: optimize productivity, not expand

- Outcome: steady premium income, stable returns

Star Health: Renewal engine (₹7,200cr) & agents fund ₹1,620cr debt+R&D with low PA claims

Star Health's cash cows: renewal premiums ~INR 7,200 crore (FY2024–25), agents ~52% of GWP, agency growth flat, renewals cut acquisition cost ~60%, personal accident share ~15% (retail FY2024) with claim ratio ~28%, group health ~18% corporate premium share; these segments fund ~INR 1,500 crore debt service and ~₹120 crore R&D in FY2024.

| Metric | Value |

|---|---|

| Renewals | INR 7,200 cr |

| Agent GWP | 52% |

| Acq cost saving | ~60% |

| Personal accident share | 15% |

| PA claim ratio | 28% |

| Group health share | 18% |

| Debt service funded | INR 1,500 cr |

| R&D funded | INR 120 cr |

What You’re Viewing Is Included

Star Health and Allied Insurance BCG Matrix

The file you're previewing on this page is the final Star Health and Allied Insurance BCG Matrix you'll receive after purchase—no watermarks, no placeholder content; just a fully formatted, analysis-ready report designed for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Star Health and Allied Insurance shows strong growth potential in retail health products but faces margin pressure from high claims and competition, placing select offerings between Stars and Question Marks; legacy group plans resemble Cash Cows with steady premiums yet limited upside. Purchase the full BCG Matrix for a complete quadrant mapping, data-backed prioritization, and actionable strategies to optimize capital allocation and product focus—delivered in Word + Excel for immediate use.

Stars

Retail Health Insurance Segment

As of late 2025, Star Health and Allied Insurance’s retail health segment drives growth, holding roughly 18–20% market share in India’s individual and family floater market and contributing about 55% of company GWP (gross written premium) in FY2024–25.

Rising medical inflation near 9–11% and higher health awareness push retail premium growth of ~14–16% YoY, forcing sustained spend: marketing rose to ~9% of retail premiums and hospital empanelment costs climbed 22% in 2025.

The segment delivers most revenue but ties up capital—combined acquisition and network investment absorbed an estimated 28–30% of operating cash flow in 2025—while private rivals (Bajaj, HDFC Ergo) intensify price and service competition.

Specialized Disease Specific Plans

Star Health and Allied Insurance pioneered disease-specific plans for diabetes and cardiac care, tapping a rising need as India’s 60+ population grew to 8.6% in 2023 and diabetes prevalence hit 8.9% in 2024 (IDA). These niche plans hold a leading share in specialty retail health segments and show double-digit premium growth—Star’s chronic-care line reported ~18% YoY premium growth in FY2024. With unit economics improving, these products are high-growth candidates moving toward future cash cows. Continued investment in specialized underwriting and tie-ups with 2,100+ empanelled hospitals is essential to sustain margins.

Senior Citizen Red Carpet Policy

Star Health and Allied Insurance’s Senior Citizen Red Carpet policy is a star in the BCG matrix: with India’s 60+ population hitting 152 million in 2025 (UN DESA) and life expectancy at 70.8 years (WHO 2024), demand is rising and Star Health gained first-mover advantage in the segment.

The Red Carpet product commands higher average premiums—reported blended premium per policy ~INR 18,000 in FY2024—and attracts seniors who prioritize comprehensive cover over price.

To retain star status, Star Health must sustain >90% customer satisfaction and process claims within target TATs; FY2024 claims ratio for senior products rose ~8 percentage points vs. general book, so efficient claims handling is critical.

Comprehensive Health Insurance Products

Comprehensive plans with maternity, dental, and ophthalmic cover have become stars for Star Health and Allied Insurance, driven by a 28% CAGR in premium income for these products from FY2020–FY2024 and 18% market share in urban retail health by 2024.

Consumers accept 15–25% higher premiums for all‑inclusive protection, pushing claims-adjusted revenue up 32% YoY in FY2024 and prompting the firm to expand product bundles and distribution in metros.

Star Health is investing in marketing and tech for these premium lines to win wallet share among the rising middle class and affluent urban households, which grew 22% in number from 2019–2024.

- 28% CAGR premium income (FY2020–FY2024)

- 18% urban retail health market share (2024)

- 15–25% premium uplift for all‑inclusive plans

- 32% claims‑adjusted revenue growth YoY (FY2024)

Digital and App Based Distribution

Star Health's proprietary digital platforms and mobile apps became a star by end-2025, driving 28% of new policy issuance (up from 9% in 2022) and cutting reliance on physical agents by 35%.

The firm committed ₹450 crore in 2024–25 to UX upgrades and AI-driven claim/chat automation, boosting conversion rates to 6.8% and lowering CAC by 22%.

- 28% new policies via digital (2025)

- Agent reliance down 35%

- ₹450 crore capex on digital (2024–25)

- Conversion 6.8%; CAC −22%

Star Health: Retail & Senior 'BCG Stars'—55% GWP, 18–20% share; digital 28%, ₹450cr capex

Star Health’s retail and senior products are BCG Stars: retail ~55% GWP, 18–20% indy market share (2025); Senior Red Carpet premium ~INR 18,000 (FY2024); chronic-care +18% YoY (FY2024); digital sales 28% (2025), ₹450 crore capex (2024–25). Efficient claims and continued investment required to convert to cash cows.

| Metric | Value |

|---|---|

| Retail GWP% | ~55% |

| Indy market share | 18–20% |

| Senior avg premium | INR 18,000 |

| Chronic YoY | ~18% |

| Digital new sales | 28% |

| Digital capex | ₹450 cr |

What is included in the product

BCG Matrix analysis of Star Health and Allied Insurance: strategic guidance on Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest moves.

One-page overview placing each Star Health business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Group Health Insurance Portfolio

Group health insurance is a mature segment where Star Health and Allied Insurance holds a high market share—about 18% of India’s corporate health premiums in FY2024—despite intense price competition.

Growth here lags retail (corporate CAGR ~4% vs retail ~12% 2021–24), but large corporate contracts deliver steady cash flows with minimal incremental marketing costs.

Liquidity from these accounts funded ~₹120 crore in R&D and pilot products in FY2024, supporting innovation in the company’s question-mark lines.

Personal Accident Insurance

Personal accident covers at Star Health and Allied Insurance are a mature product line with high market share and low growth, fitting the BCG cash cow profile; industry premium growth for personal accident was ~3% in 2024 while Star Health reported ~15% share in retail accident lines in FY2024 (source: IR and IRDAI reports).

This segment yields high margins due to low claim frequency—industry claim ratios for personal accident averaged ~28% in 2024—plus established underwriting and pricing models that keep loss ratios favorable for Star Health.

Star Health prioritizes harvesting cash flows from personal accident products to fund operations and dividends, with net earned premium from miscellaneous retail lines contributing an estimated 8–10% of group GPW in FY2024, bolstering liquidity and dividend capacity.

Standard Indemnity Plans

Standard indemnity plans, like the regulated Arogya Sanjeevani (mandatory since 2020), act as cash cows—covering ~55–60% of Star Health and Allied Insurance’s retail book in 2024 and delivering steady combined ratios near 95%, thanks to scale and price regulation.

Renewal Premium Book

Renewal Premium Book: Star Health's large existing policyholder base generated about INR 7,200 crore in renewal premiums in FY2024–25, making it a strong cash cow with low acquisition cost and high margins.

Renewals cut acquisition spend by ~60% versus new business, delivering steady cash inflows that support servicing ~INR 1,500 crore corporate debt and fund R&D in health tech initiatives.

- INR 7,200 crore renewal premiums FY2024–25

- ~60% lower acquisition cost vs new business

- ~INR 1,500 crore debt service supported

- Funds allocated to health tech R&D from cash flows

Agency Network Distribution

Star Health's agency network is a mature, dominant distribution channel delivering steady premiums—agents contributed about 52% of gross written premium (GWP) in FY2024, making it a primary cash cow with high market share and reliable returns.

Growth in agency-sourced business has slowed as digital channels rose (digital accounted for ~18% of GWP in FY2024), so management prioritizes productivity gains over expansion to sustain margins and retention.

Focus is on milking existing infrastructure: higher agent productivity, targeted training, and cross-sell drives stable cash flow and ROE support for underwriting and reserves.

- Agents = ~52% GWP (FY2024)

- Digital = ~18% GWP (FY2024)

- Strategy: optimize productivity, not expand

- Outcome: steady premium income, stable returns

Star Health: Renewal engine (₹7,200cr) & agents fund ₹1,620cr debt+R&D with low PA claims

Star Health's cash cows: renewal premiums ~INR 7,200 crore (FY2024–25), agents ~52% of GWP, agency growth flat, renewals cut acquisition cost ~60%, personal accident share ~15% (retail FY2024) with claim ratio ~28%, group health ~18% corporate premium share; these segments fund ~INR 1,500 crore debt service and ~₹120 crore R&D in FY2024.

| Metric | Value |

|---|---|

| Renewals | INR 7,200 cr |

| Agent GWP | 52% |

| Acq cost saving | ~60% |

| Personal accident share | 15% |

| PA claim ratio | 28% |

| Group health share | 18% |

| Debt service funded | INR 1,500 cr |

| R&D funded | INR 120 cr |

What You’re Viewing Is Included

Star Health and Allied Insurance BCG Matrix

The file you're previewing on this page is the final Star Health and Allied Insurance BCG Matrix you'll receive after purchase—no watermarks, no placeholder content; just a fully formatted, analysis-ready report designed for strategic clarity and professional use.