Steel Partners PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and technological change are shaping Steel Partners' strategic options—our concise PESTLE snapshot highlights the key external forces you need to know; purchase the full PESTLE to access a detailed, actionable report that investors and strategists rely on.

Political factors

Geopolitical Trade Volatility

The diversified nature of Steel Partners leaves its industrial subsidiaries exposed to shifting trade alliances and tariff regimes; in 2025 global protectionist measures rose, with G20 average applied tariff equivalents climbing ~0.8 percentage points, prompting the firm to re-evaluate cross-border sourcing to avoid punitive duties.

Defense Spending and Government Contracts

With aerospace and defense exposures, Steel Partners is sensitive to US national security priorities and the FY2025 proposed defense budget of about $858 billion; shifts in political leadership or strategy can materially alter procurement volumes for its industrial units. Ongoing defense modernization programs underpin recurring revenue, yet congressional gridlock and continuing resolutions—occurring multiple times in 2023–2025—pose persistent contract-timing and funding risks.

Financial Services Regulatory Environment

Steel Partners' financial arm WebBank operates under FDIC and state scrutiny; in 2024 the FDIC issued guidance tightening supervision of industrial banks after several high-profile fintech failures, increasing compliance costs industry-wide by an estimated 10-15%. Political momentum for stricter fintech oversight and proposed bills in 2024–25 could impose capital or lending limits, potentially reducing WebBank-originated loans (which accounted for a meaningful share of WebBank’s $3.2bn assets in 2023) and pressuring profitability. Navigating these rules is critical to sustain the segment’s operational viability.

Corporate Tax Policy Shifts

- 2024 EBITDA ~ $420m; 2024 capex ~$320m

- Federal corporate rate 21%; 5ppt rise → ~6–8% after-tax income decline

- 10% cut in investment incentives → $30–50m lower annual capex

- Maintain 9–11% target ROIC via tax optimization

Labor Relations and Union Influence

Political movements pushing higher minimum wages and stronger labor protections raise operating costs for Steel Partners’ manufacturing and energy subsidiaries; a $15 federal minimum wage proposal in the US would add roughly 3–6% to hourly labor costs in low-wage facilities.

Pro-union political climates—e.g., recent union wins in US manufacturing sectors where union density rose marginally to ~10% in 2024—can strengthen collective bargaining, increasing wage and benefits commitments.

Steel Partners must weigh these pressures against efficiency targets and margin preservation, balancing potential 1–3% EBITDA impact from wage inflation with productivity investments.

- Higher minimum wage proposals: +3–6% labor cost impact

Rising tariffs, defense shifts & tighter oversight squeeze profits, financing and capex

Political risks: rising protectionism (G20 applied tariffs +0.8ppt in 2025) and US defense budget shifts (FY2025 ~$858bn) affect sourcing and aerospace contracts; tighter bank/fintech oversight raised compliance costs ~10–15% post-2024, threatening WebBank loan volumes (WebBank assets $3.2bn in 2023); tax or incentive cuts (5ppt rate hike → ≈6–8% after-tax income loss; 10% incentive cut → $30–50m capex reduction)

| Metric | Value |

|---|---|

| G20 tariff change (2025) | +0.8 ppt |

| FY2025 defense budget | $858bn |

| WebBank assets (2023) | $3.2bn |

| 2024 EBITDA | $420m |

| 2024 capex | $320m |

What is included in the product

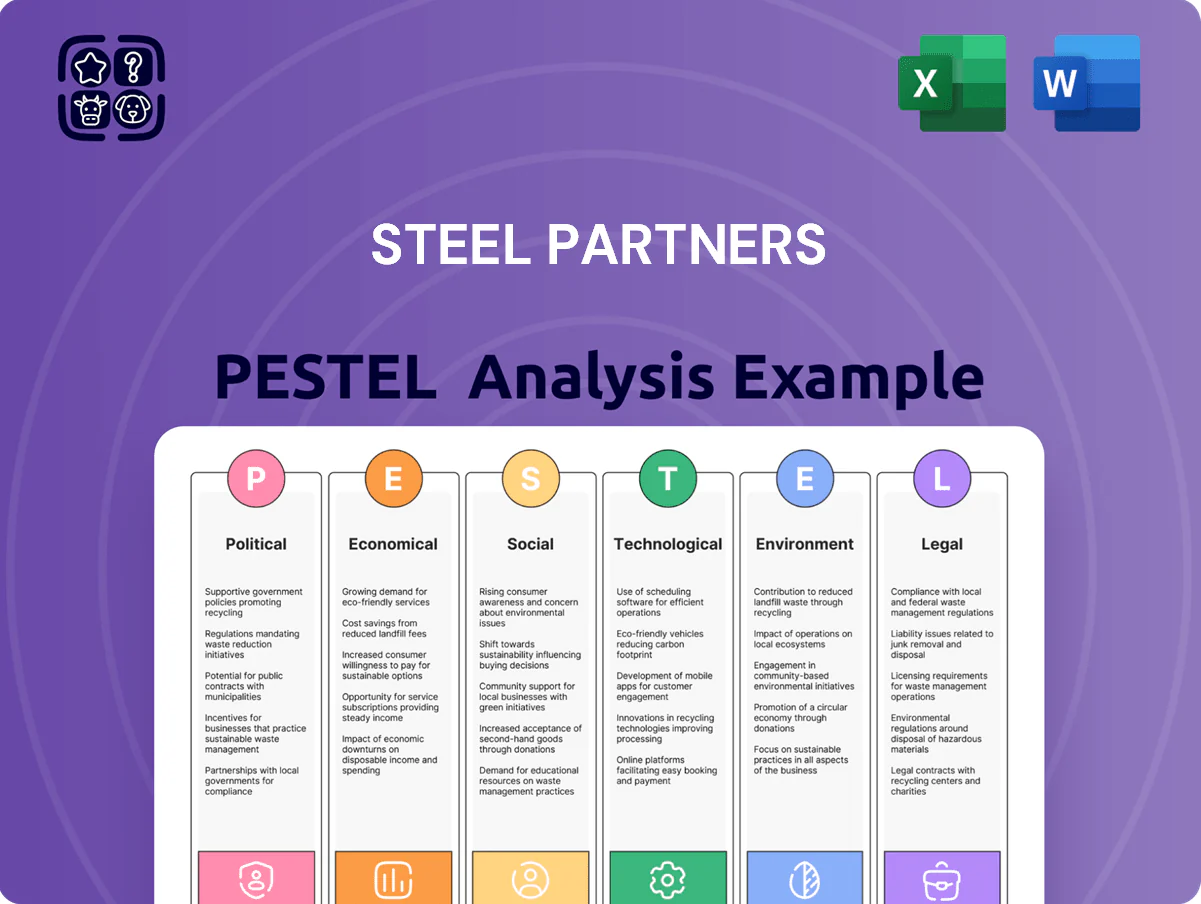

Explores how macro-environmental forces uniquely affect Steel Partners across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE summary of Steel Partners that’s easy to drop into presentations or share across teams, helping stakeholders quickly align on external risks and market positioning during planning sessions.

Economic factors

Interest Rate and Cost of Debt

At end-2025 the US effective federal funds rate near 5.25–5.50% and average corporate A-rated yields around 5.8%–6.2% raise borrowing costs for Steel Partners, constraining leveraged acquisitions and reducing IRR on distressed targets.

Higher interest expense increases servicing costs across its debt book—Steel Partners reported consolidated net debt/EBITDA ratios near 3.0x in 2024—so margin compression risk is tangible.

Management must optimize capital structure via refinancing, extend maturities, or shift to lower-cost fixed-rate instruments to prevent interest burdens from eroding subsidiary cash flows and deal capacity.

Inflationary Pressures on Industrial Inputs

Fluctuations in energy, steel and chemical prices directly raise COGS for Steel Partners’ industrial units; crude oil fell from $85/bbl in 2022 to ~$75/bbl average in 2024 while HRC steel rallied 18% in 2024 to ~$900/ton, increasing input costs materially.

Although headline U.S. CPI eased to 3.4% in 2024 from 6.5% in 2022, commodity price volatility persists, necessitating sophisticated hedging and dynamic pricing.

The firm’s ability to pass higher costs through contract escalators and surcharges is pivotal to preserving operating margins, with EBITDA sensitivity to a 10% input shock estimated at several hundred basis points.

Energy Market Demand and Pricing

Steel Energy Services' performance ties closely to oil and gas sector health; global oil demand reached about 101.6 million bpd in 2023 and IEA projects ~103–104 million bpd in 2024–25, driving utilization of energy assets and service rates.

As energy mix diversifies, capital spending for traditional E&P fell; global upstream CAPEX was roughly $410 billion in 2023, down from peaks, causing volatility in contract pricing and dayrates.

Price benchmarks matter: Brent averaged $86/bbl in 2024 YTD to Jan 2026 signals improved economics but remains sensitive to OPEC+ cuts and recession risks in China and EU that could curb drilling and lower utilization.

Consumer Spending and Credit Trends

The financial services segment's performance hinges on consumer creditworthiness and macroeconomic health; US household debt reached about 17.5 trillion USD in Q3 2025, pressuring default risk and loan demand during downturns.

Economic contractions typically raise delinquencies—e.g., serious consumer loan delinquencies rose to 2.0% in 2024—reducing volumes of loans facilitated through WebBank.

Conversely, strong consumer confidence (index near 110 in late 2024) boosts loan originations and uplifts interest income tied to Steel Partners' financial holdings.

- Higher household debt and rising delinquencies increase credit losses and compress lending volumes

- WebBank originations correlate positively with consumer confidence and GDP growth

- Loan volume growth in 2024–25 supported profitability when consumer sentiment remained elevated

Capital Market Liquidity

Steel Partners depends on liquid capital markets to buy, manage, and sell undervalued businesses; Q4 2025 US equity market turnover averaged about 0.9% daily of market cap, and marked declines in liquidity—like the 2022 volatility spike where S&P 500 ADV fell ~22%—can compress exit valuations and delay divestitures.

Access to secondary markets and private equity funding (global PE dry powder ~US$2.4 trillion in 2024) is critical for portfolio rotation and opportunistic acquisitions.

- Heavy reliance on public market liquidity for exits

- Market volatility can reduce achievable valuations

- Secondary market depth and ~US$2.4T PE dry powder support deal flow

Rising Rates, Commodity Costs & Leverage Squeeze Deals as PE Dry Powder Fuels Exits

Higher rates (Fed funds ~5.25–5.50% end-2025) and A-rated yields ~5.8–6.2% raise borrowing costs, stressing leveraged deals; consolidated net debt/EBITDA ~3.0x (2024) heightens margin risk. Commodity volatility (HRC ~900/ton 2024; Brent ~$86/bbl 2024) lifts COGS, requiring hedges/contract escalators. Household debt ~17.5T (Q3 2025) and delinquencies up raise credit risk; PE dry powder ~US$2.4T (2024) supports exits.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (end-2025) |

| A-rated yields | 5.8–6.2% |

| Net debt/EBITDA | ~3.0x (2024) |

| HRC steel | ~$900/ton (2024) |

| Brent | ~$86/bbl (2024) |

| Household debt | ~$17.5T (Q3 2025) |

| PE dry powder | ~$2.4T (2024) |

Preview Before You Purchase

Steel Partners PESTLE Analysis

The preview shown here is the exact Steel Partners PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and technological change are shaping Steel Partners' strategic options—our concise PESTLE snapshot highlights the key external forces you need to know; purchase the full PESTLE to access a detailed, actionable report that investors and strategists rely on.

Political factors

Geopolitical Trade Volatility

The diversified nature of Steel Partners leaves its industrial subsidiaries exposed to shifting trade alliances and tariff regimes; in 2025 global protectionist measures rose, with G20 average applied tariff equivalents climbing ~0.8 percentage points, prompting the firm to re-evaluate cross-border sourcing to avoid punitive duties.

Defense Spending and Government Contracts

With aerospace and defense exposures, Steel Partners is sensitive to US national security priorities and the FY2025 proposed defense budget of about $858 billion; shifts in political leadership or strategy can materially alter procurement volumes for its industrial units. Ongoing defense modernization programs underpin recurring revenue, yet congressional gridlock and continuing resolutions—occurring multiple times in 2023–2025—pose persistent contract-timing and funding risks.

Financial Services Regulatory Environment

Steel Partners' financial arm WebBank operates under FDIC and state scrutiny; in 2024 the FDIC issued guidance tightening supervision of industrial banks after several high-profile fintech failures, increasing compliance costs industry-wide by an estimated 10-15%. Political momentum for stricter fintech oversight and proposed bills in 2024–25 could impose capital or lending limits, potentially reducing WebBank-originated loans (which accounted for a meaningful share of WebBank’s $3.2bn assets in 2023) and pressuring profitability. Navigating these rules is critical to sustain the segment’s operational viability.

Corporate Tax Policy Shifts

- 2024 EBITDA ~ $420m; 2024 capex ~$320m

- Federal corporate rate 21%; 5ppt rise → ~6–8% after-tax income decline

- 10% cut in investment incentives → $30–50m lower annual capex

- Maintain 9–11% target ROIC via tax optimization

Labor Relations and Union Influence

Political movements pushing higher minimum wages and stronger labor protections raise operating costs for Steel Partners’ manufacturing and energy subsidiaries; a $15 federal minimum wage proposal in the US would add roughly 3–6% to hourly labor costs in low-wage facilities.

Pro-union political climates—e.g., recent union wins in US manufacturing sectors where union density rose marginally to ~10% in 2024—can strengthen collective bargaining, increasing wage and benefits commitments.

Steel Partners must weigh these pressures against efficiency targets and margin preservation, balancing potential 1–3% EBITDA impact from wage inflation with productivity investments.

- Higher minimum wage proposals: +3–6% labor cost impact

Rising tariffs, defense shifts & tighter oversight squeeze profits, financing and capex

Political risks: rising protectionism (G20 applied tariffs +0.8ppt in 2025) and US defense budget shifts (FY2025 ~$858bn) affect sourcing and aerospace contracts; tighter bank/fintech oversight raised compliance costs ~10–15% post-2024, threatening WebBank loan volumes (WebBank assets $3.2bn in 2023); tax or incentive cuts (5ppt rate hike → ≈6–8% after-tax income loss; 10% incentive cut → $30–50m capex reduction)

| Metric | Value |

|---|---|

| G20 tariff change (2025) | +0.8 ppt |

| FY2025 defense budget | $858bn |

| WebBank assets (2023) | $3.2bn |

| 2024 EBITDA | $420m |

| 2024 capex | $320m |

What is included in the product

Explores how macro-environmental forces uniquely affect Steel Partners across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE summary of Steel Partners that’s easy to drop into presentations or share across teams, helping stakeholders quickly align on external risks and market positioning during planning sessions.

Economic factors

Interest Rate and Cost of Debt

At end-2025 the US effective federal funds rate near 5.25–5.50% and average corporate A-rated yields around 5.8%–6.2% raise borrowing costs for Steel Partners, constraining leveraged acquisitions and reducing IRR on distressed targets.

Higher interest expense increases servicing costs across its debt book—Steel Partners reported consolidated net debt/EBITDA ratios near 3.0x in 2024—so margin compression risk is tangible.

Management must optimize capital structure via refinancing, extend maturities, or shift to lower-cost fixed-rate instruments to prevent interest burdens from eroding subsidiary cash flows and deal capacity.

Inflationary Pressures on Industrial Inputs

Fluctuations in energy, steel and chemical prices directly raise COGS for Steel Partners’ industrial units; crude oil fell from $85/bbl in 2022 to ~$75/bbl average in 2024 while HRC steel rallied 18% in 2024 to ~$900/ton, increasing input costs materially.

Although headline U.S. CPI eased to 3.4% in 2024 from 6.5% in 2022, commodity price volatility persists, necessitating sophisticated hedging and dynamic pricing.

The firm’s ability to pass higher costs through contract escalators and surcharges is pivotal to preserving operating margins, with EBITDA sensitivity to a 10% input shock estimated at several hundred basis points.

Energy Market Demand and Pricing

Steel Energy Services' performance ties closely to oil and gas sector health; global oil demand reached about 101.6 million bpd in 2023 and IEA projects ~103–104 million bpd in 2024–25, driving utilization of energy assets and service rates.

As energy mix diversifies, capital spending for traditional E&P fell; global upstream CAPEX was roughly $410 billion in 2023, down from peaks, causing volatility in contract pricing and dayrates.

Price benchmarks matter: Brent averaged $86/bbl in 2024 YTD to Jan 2026 signals improved economics but remains sensitive to OPEC+ cuts and recession risks in China and EU that could curb drilling and lower utilization.

Consumer Spending and Credit Trends

The financial services segment's performance hinges on consumer creditworthiness and macroeconomic health; US household debt reached about 17.5 trillion USD in Q3 2025, pressuring default risk and loan demand during downturns.

Economic contractions typically raise delinquencies—e.g., serious consumer loan delinquencies rose to 2.0% in 2024—reducing volumes of loans facilitated through WebBank.

Conversely, strong consumer confidence (index near 110 in late 2024) boosts loan originations and uplifts interest income tied to Steel Partners' financial holdings.

- Higher household debt and rising delinquencies increase credit losses and compress lending volumes

- WebBank originations correlate positively with consumer confidence and GDP growth

- Loan volume growth in 2024–25 supported profitability when consumer sentiment remained elevated

Capital Market Liquidity

Steel Partners depends on liquid capital markets to buy, manage, and sell undervalued businesses; Q4 2025 US equity market turnover averaged about 0.9% daily of market cap, and marked declines in liquidity—like the 2022 volatility spike where S&P 500 ADV fell ~22%—can compress exit valuations and delay divestitures.

Access to secondary markets and private equity funding (global PE dry powder ~US$2.4 trillion in 2024) is critical for portfolio rotation and opportunistic acquisitions.

- Heavy reliance on public market liquidity for exits

- Market volatility can reduce achievable valuations

- Secondary market depth and ~US$2.4T PE dry powder support deal flow

Rising Rates, Commodity Costs & Leverage Squeeze Deals as PE Dry Powder Fuels Exits

Higher rates (Fed funds ~5.25–5.50% end-2025) and A-rated yields ~5.8–6.2% raise borrowing costs, stressing leveraged deals; consolidated net debt/EBITDA ~3.0x (2024) heightens margin risk. Commodity volatility (HRC ~900/ton 2024; Brent ~$86/bbl 2024) lifts COGS, requiring hedges/contract escalators. Household debt ~17.5T (Q3 2025) and delinquencies up raise credit risk; PE dry powder ~US$2.4T (2024) supports exits.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (end-2025) |

| A-rated yields | 5.8–6.2% |

| Net debt/EBITDA | ~3.0x (2024) |

| HRC steel | ~$900/ton (2024) |

| Brent | ~$86/bbl (2024) |

| Household debt | ~$17.5T (Q3 2025) |

| PE dry powder | ~$2.4T (2024) |

Preview Before You Purchase

Steel Partners PESTLE Analysis

The preview shown here is the exact Steel Partners PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.