Stef Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

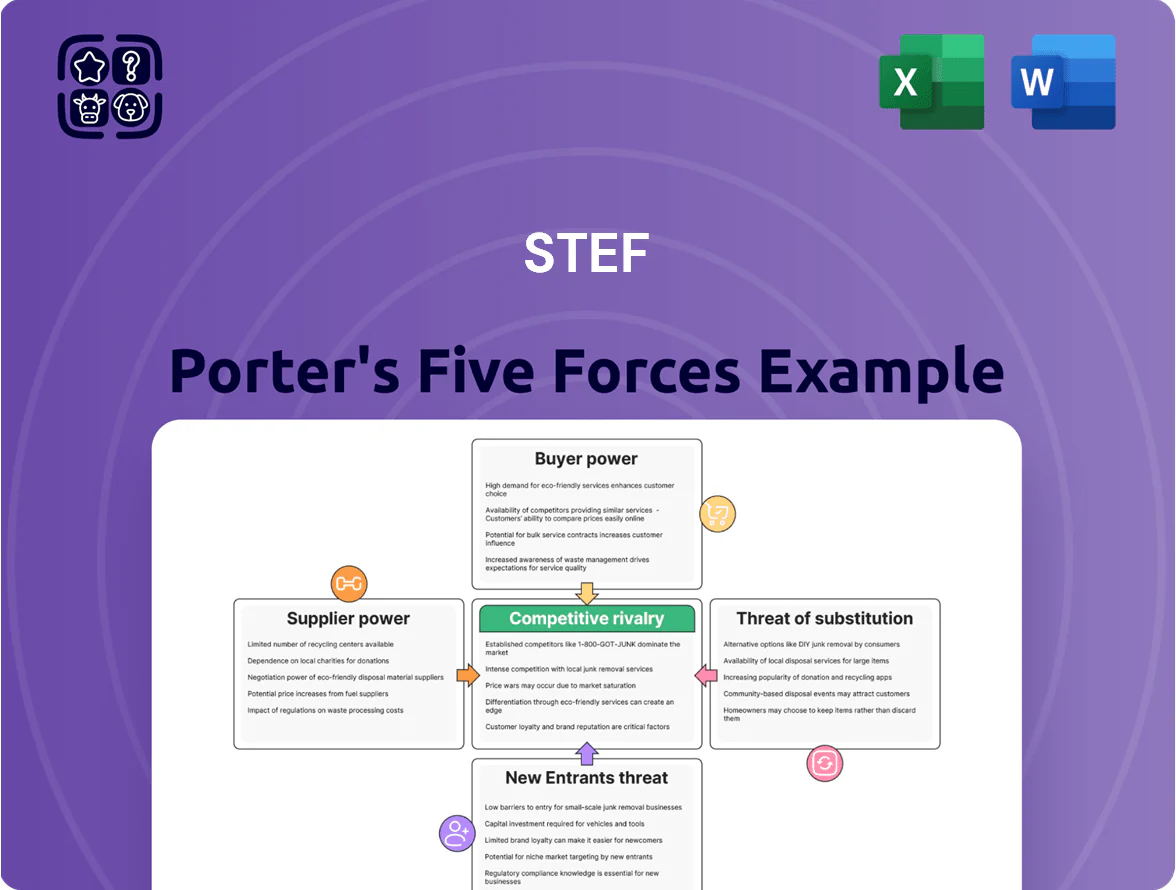

Suppliers Bargaining Power

Volatility of Energy and Fuel Costs

STEF depends on electricity for ~1,000+ cold sites and diesel/electric for ~4,000 vehicles; energy suppliers hold strong leverage as power is essential to the cold chain.

By end-2025 European wholesale electricity prices averaged ~€120/MWh (vs €70/MWh 2021); sudden spikes raise STEF’s variable costs despite hedging.

STEF’s efficiency and hedging cut exposure: reported 2024 energy savings ~8% and fuel hedges cover ~40% of volume, but supplier pricing still directly lifts operating margins when volatile.

Dependency on Specialized Vehicle Manufacturers

STEF faces rising supplier power as decarbonization forces reliance on few OEMs for heavy-duty electric or hydrogen refrigerated trucks; in 2024 only ~3 OEMs offered certified models meeting EU CO2 targets, so options are narrow.

These OEMs hold tech patents and charge premiums; typical lead times hit 12–24 months in 2024, and order backlogs grew 40% YoY, giving suppliers pricing leverage.

With EU heavy-duty CO2 rules tightening for 2025–2030, demand now exceeds supply—market shortages drove unit prices up ~15% in 2024, squeezing fleet renewal costs for STEF.

Shortage of Specialized Labor and Drivers

The EU logistics sector had a 2024 shortfall of about 300,000 HGV drivers and growing demand for cold-chain techs; scarce labor acts as a supplier, pushing wages up—EU median HGV driver pay rose ~8% in 2023–24.

For STEF (STEF SE, listed Euronext: STEF), this means higher operating costs and margin pressure; the firm must invest in training and retention—STEF reported 2023 payroll up ~6%—to counter supplier power from a shrinking skilled labor pool.

Real Estate and Strategic Infrastructure Providers

Limited land near major EU cities pushes industrial real estate rents up—prime logistics rents rose 6–10% in 2024 in Paris, Rotterdam, and Milan, giving developers leverage over Stef Porter.

Cold storage needs (R-value, backup power, HACCP systems) make relocations costly—moving a 10,000 m2 frozen facility can exceed €5–12m, locking tenants to sites.

Landlords extract favorable lease clauses and premiums; recent strategic hub sale prices hit €1,200–€2,500/m2 in 2024 for well-connected sites.

- Prime logistics rent growth 6–10% (2024)

- Relocation cost ≈ €5–12m (10,000 m2 cold site)

- Sale prices €1,200–€2,500/m2 (2024)

Digital Infrastructure and Software Vendors

- Market size ~USD 8.6bn (2024)

- Switch cost 1–3m USD, 6–18 months

- Few dominant vendors → pricing leverage

- Data integrity = compliance risk

Supplier power squeezes STEF: rising energy, OEM costs, tech and rent pressures

Suppliers (energy, OEMs, tech, real estate, labour) hold high bargaining power for STEF: 2024 EU wholesale power ~€120/MWh, OEM lead times 12–24m with prices +15% YoY, cold-tech market ~USD8.6bn, switching costs USD1–3m, prime rents +6–10% and relocation ≈€5–12m; these drive operating-cost and margin pressure.

| Supplier | Key metric (2024) |

|---|---|

| Energy | €120/MWh |

| OEMs | Lead 12–24m; +15% price |

| Tech | USD8.6bn; USD1–3m switch |

| Rents | +6–10%; relocate €5–12m |

What is included in the product

Concise Five Forces breakdown for Stef that reveals competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and industry rivalry—supported by strategic insights to inform pricing, market defense, and growth decisions.

Stef Porter’s Five Forces delivers a concise, one-sheet strategic snapshot—quickly pinpoint competitive pressures and prioritize actions for immediate decision-making.

Customers Bargaining Power

High Concentration of Retail Giants

The European food retail market is concentrated: Carrefour, Lidl, and Tesco together account for roughly 30–35% of EU grocery sales and move millions of pallets annually, giving them outsized buying power.

These chains use scale to push down logistics rates and demand tight SLAs; average pallet rates can be pressured down by 5–15% in tender cycles, squeezing carrier margins.

For STEF (STEF SE, market cap ~€4.5bn in 2025), losing one major retail contract could cut regional revenue by an estimated 8–12%, so contract retention and service differentiation are critical.

Low Switching Costs for Standard Transport

While cold storage is specialized, transport of palletized food is often a commodity; 62% of EU food shippers cite price as their top selection factor in 2024, so manufacturers can switch carriers easily for lower rates on non-specialized routes.

This low switching cost pressures STEF to show value via reliability and dense networks; STEF reported 97.6% on-time delivery in 2024 across Europe, a key metric to deter cost-only switches.

Demand for Integrated Digital Transparency

Threat of Vertical Integration by Retailers

Large retail chains explored backward integration; e.g., Carrefour and Walmart pilots cut logistics costs by up to 8% in 2023–24, keeping STEF under pricing pressure during contracts.

STEF must quantify its scale: 2024 group turnover €3.9bn, 700+ sites, and multi-client routes that lower unit costs versus single-retailer networks.

Prove value via metrics: cost per pallet, service frequency, cold-chain uptime to deter insourcing.

- Retailer pilots cut logistics 6–8% (2023–24)

- STEF 2024 revenue €3.9bn; 700+ sites

- Focus metrics: €/pallet, uptime %, route density

Increasing Sensitivity to ESG Performance

Corporate customers, pressed to cut Scope 3 emissions, increasingly demand greener logistics from STEF, pushing adoption of EVs and sustainable warehousing without price premiums; 2024 CDP data shows 70% of large buyers link procurement to supplier emissions reporting.

Buyers leverage volume to force capex shifts: EV fleet and cold-storage upgrades raise STEF’s capital needs—EVs cost ~€120k each, racking sustainable warehouses can add 10–15% to build costs—yet customers expect parity on rates.

STEF must align its investment plan with these demands to stay preferred; failing to invest risks losing major accounts—top 20 customers often represent >40% of revenue in refrigerated logistics.

- 70% buyers link procurement to emissions reporting

- EV unit cost ~€120,000

- Sustainable warehousing +10–15% capex

- Top 20 customers >40% revenue

Retailer buyers dominate: STEF faces IT capex and margin squeeze as customers threaten to switch

Buyers hold strong leverage: top EU retailers (Carrefour, Lidl, Tesco ~30–35% market share) drive pricing, SLAs, and tech specs, forcing STEF (2024 revenue €3.9bn; market cap ~€4.5bn) to invest ~€20–30m/yr in integrations and face margin pressure if rates fall 5–15% in tenders; top 20 customers likely >40% revenue, and 72% of shippers would switch over poor visibility.

| Metric | Value |

|---|---|

| EU top retailers share | 30–35% |

| STEF 2024 rev | €3.9bn |

| IT capex pressure | €20–30m/yr |

| Switch risk | 72% |

Full Version Awaits

Stef Porter's Five Forces Analysis

This preview shows the exact Stef Porter Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

The document displayed here is the same complete, ready-to-use file you'll get upon payment, containing the full competitive assessment and actionable insights for strategic decision-making.

You're viewing the final deliverable; once purchased, you'll have instant access to this identical analysis for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Suppliers Bargaining Power

Volatility of Energy and Fuel Costs

STEF depends on electricity for ~1,000+ cold sites and diesel/electric for ~4,000 vehicles; energy suppliers hold strong leverage as power is essential to the cold chain.

By end-2025 European wholesale electricity prices averaged ~€120/MWh (vs €70/MWh 2021); sudden spikes raise STEF’s variable costs despite hedging.

STEF’s efficiency and hedging cut exposure: reported 2024 energy savings ~8% and fuel hedges cover ~40% of volume, but supplier pricing still directly lifts operating margins when volatile.

Dependency on Specialized Vehicle Manufacturers

STEF faces rising supplier power as decarbonization forces reliance on few OEMs for heavy-duty electric or hydrogen refrigerated trucks; in 2024 only ~3 OEMs offered certified models meeting EU CO2 targets, so options are narrow.

These OEMs hold tech patents and charge premiums; typical lead times hit 12–24 months in 2024, and order backlogs grew 40% YoY, giving suppliers pricing leverage.

With EU heavy-duty CO2 rules tightening for 2025–2030, demand now exceeds supply—market shortages drove unit prices up ~15% in 2024, squeezing fleet renewal costs for STEF.

Shortage of Specialized Labor and Drivers

The EU logistics sector had a 2024 shortfall of about 300,000 HGV drivers and growing demand for cold-chain techs; scarce labor acts as a supplier, pushing wages up—EU median HGV driver pay rose ~8% in 2023–24.

For STEF (STEF SE, listed Euronext: STEF), this means higher operating costs and margin pressure; the firm must invest in training and retention—STEF reported 2023 payroll up ~6%—to counter supplier power from a shrinking skilled labor pool.

Real Estate and Strategic Infrastructure Providers

Limited land near major EU cities pushes industrial real estate rents up—prime logistics rents rose 6–10% in 2024 in Paris, Rotterdam, and Milan, giving developers leverage over Stef Porter.

Cold storage needs (R-value, backup power, HACCP systems) make relocations costly—moving a 10,000 m2 frozen facility can exceed €5–12m, locking tenants to sites.

Landlords extract favorable lease clauses and premiums; recent strategic hub sale prices hit €1,200–€2,500/m2 in 2024 for well-connected sites.

- Prime logistics rent growth 6–10% (2024)

- Relocation cost ≈ €5–12m (10,000 m2 cold site)

- Sale prices €1,200–€2,500/m2 (2024)

Digital Infrastructure and Software Vendors

- Market size ~USD 8.6bn (2024)

- Switch cost 1–3m USD, 6–18 months

- Few dominant vendors → pricing leverage

- Data integrity = compliance risk

Supplier power squeezes STEF: rising energy, OEM costs, tech and rent pressures

Suppliers (energy, OEMs, tech, real estate, labour) hold high bargaining power for STEF: 2024 EU wholesale power ~€120/MWh, OEM lead times 12–24m with prices +15% YoY, cold-tech market ~USD8.6bn, switching costs USD1–3m, prime rents +6–10% and relocation ≈€5–12m; these drive operating-cost and margin pressure.

| Supplier | Key metric (2024) |

|---|---|

| Energy | €120/MWh |

| OEMs | Lead 12–24m; +15% price |

| Tech | USD8.6bn; USD1–3m switch |

| Rents | +6–10%; relocate €5–12m |

What is included in the product

Concise Five Forces breakdown for Stef that reveals competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and industry rivalry—supported by strategic insights to inform pricing, market defense, and growth decisions.

Stef Porter’s Five Forces delivers a concise, one-sheet strategic snapshot—quickly pinpoint competitive pressures and prioritize actions for immediate decision-making.

Customers Bargaining Power

High Concentration of Retail Giants

The European food retail market is concentrated: Carrefour, Lidl, and Tesco together account for roughly 30–35% of EU grocery sales and move millions of pallets annually, giving them outsized buying power.

These chains use scale to push down logistics rates and demand tight SLAs; average pallet rates can be pressured down by 5–15% in tender cycles, squeezing carrier margins.

For STEF (STEF SE, market cap ~€4.5bn in 2025), losing one major retail contract could cut regional revenue by an estimated 8–12%, so contract retention and service differentiation are critical.

Low Switching Costs for Standard Transport

While cold storage is specialized, transport of palletized food is often a commodity; 62% of EU food shippers cite price as their top selection factor in 2024, so manufacturers can switch carriers easily for lower rates on non-specialized routes.

This low switching cost pressures STEF to show value via reliability and dense networks; STEF reported 97.6% on-time delivery in 2024 across Europe, a key metric to deter cost-only switches.

Demand for Integrated Digital Transparency

Threat of Vertical Integration by Retailers

Large retail chains explored backward integration; e.g., Carrefour and Walmart pilots cut logistics costs by up to 8% in 2023–24, keeping STEF under pricing pressure during contracts.

STEF must quantify its scale: 2024 group turnover €3.9bn, 700+ sites, and multi-client routes that lower unit costs versus single-retailer networks.

Prove value via metrics: cost per pallet, service frequency, cold-chain uptime to deter insourcing.

- Retailer pilots cut logistics 6–8% (2023–24)

- STEF 2024 revenue €3.9bn; 700+ sites

- Focus metrics: €/pallet, uptime %, route density

Increasing Sensitivity to ESG Performance

Corporate customers, pressed to cut Scope 3 emissions, increasingly demand greener logistics from STEF, pushing adoption of EVs and sustainable warehousing without price premiums; 2024 CDP data shows 70% of large buyers link procurement to supplier emissions reporting.

Buyers leverage volume to force capex shifts: EV fleet and cold-storage upgrades raise STEF’s capital needs—EVs cost ~€120k each, racking sustainable warehouses can add 10–15% to build costs—yet customers expect parity on rates.

STEF must align its investment plan with these demands to stay preferred; failing to invest risks losing major accounts—top 20 customers often represent >40% of revenue in refrigerated logistics.

- 70% buyers link procurement to emissions reporting

- EV unit cost ~€120,000

- Sustainable warehousing +10–15% capex

- Top 20 customers >40% revenue

Retailer buyers dominate: STEF faces IT capex and margin squeeze as customers threaten to switch

Buyers hold strong leverage: top EU retailers (Carrefour, Lidl, Tesco ~30–35% market share) drive pricing, SLAs, and tech specs, forcing STEF (2024 revenue €3.9bn; market cap ~€4.5bn) to invest ~€20–30m/yr in integrations and face margin pressure if rates fall 5–15% in tenders; top 20 customers likely >40% revenue, and 72% of shippers would switch over poor visibility.

| Metric | Value |

|---|---|

| EU top retailers share | 30–35% |

| STEF 2024 rev | €3.9bn |

| IT capex pressure | €20–30m/yr |

| Switch risk | 72% |

Full Version Awaits

Stef Porter's Five Forces Analysis

This preview shows the exact Stef Porter Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

The document displayed here is the same complete, ready-to-use file you'll get upon payment, containing the full competitive assessment and actionable insights for strategic decision-making.

You're viewing the final deliverable; once purchased, you'll have instant access to this identical analysis for immediate use.