ST Engineering SWOT Analysis

Make Insightful Decisions Backed by Expert Research

ST Engineering’s diversified defense and aerospace portfolio, strong R&D, and global footprint position it well against cyclicality and geopolitical demand—but rising competition, regulatory pressures, and supply-chain risks merit close scrutiny. Discover the complete picture behind the company’s market position with our full SWOT analysis, offering actionable insights, financial context, and strategic takeaways to inform investment or strategic decisions.

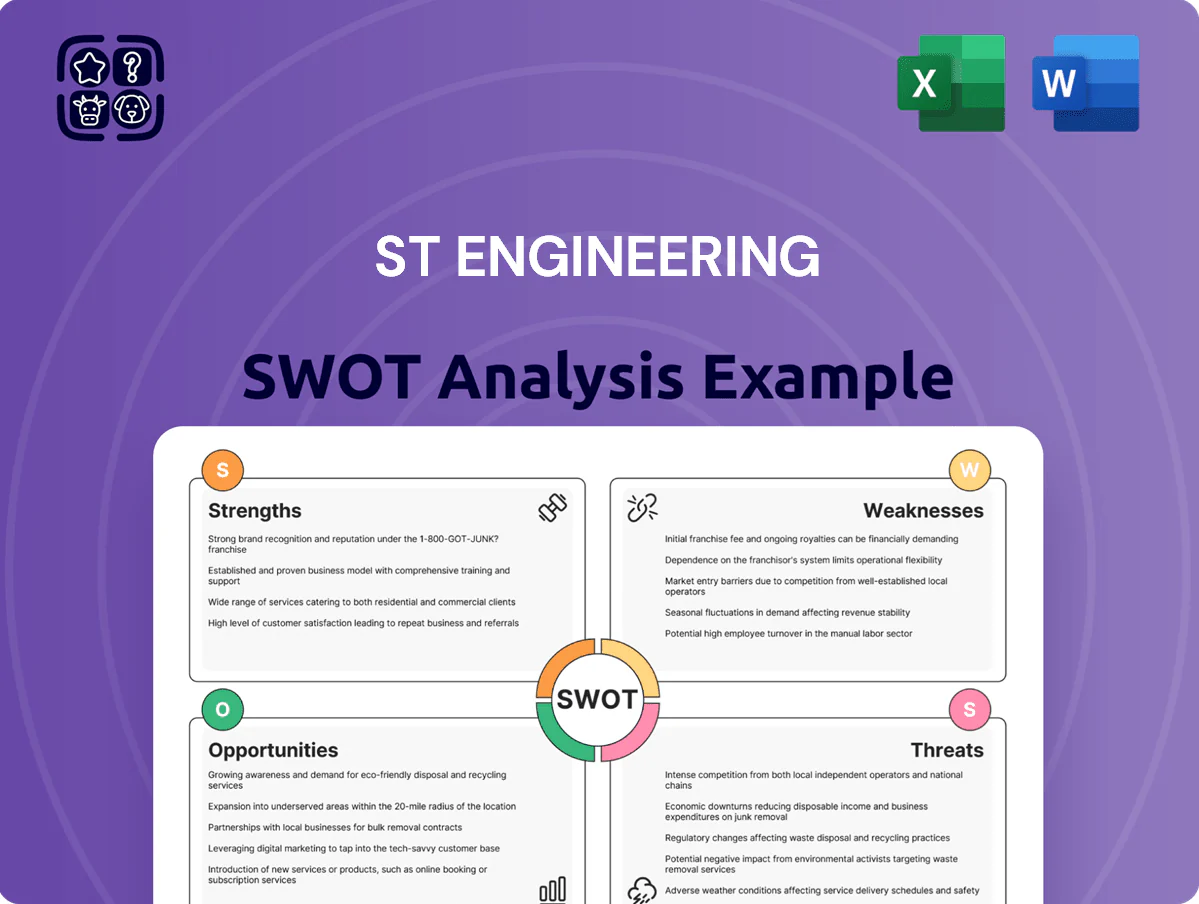

Strengths

Dominant Global MRO Position

ST Engineering remains the world’s largest commercial airframe MRO by capacity as of late 2025, servicing over 2,100 narrow- and widebody aircraft slots across Asia, Europe and the United States, which drives unit cost advantages and 18% lower cycle times vs peers. The scale supports a global footprint with 35 facilities and $2.1 billion annual MRO revenue in FY2024. Its quality and safety record—<0.02 hull-loss events per million flight hours—helps secure multi‑year contracts with major airlines and lessors, underpinning stable backlog and repeat revenue.

Diversified Multi-Sector Portfolio

ST Engineering operates across aerospace, smart city, and defense, which provided a natural hedge and helped sustain group revenue of S$10.4 billion in FY2025, down just 2% year-on-year despite sector shocks; aerospace, smart city and defense each contributed roughly 35%, 30% and 35% of revenue, respectively. Shared AI and robotics platforms cut R&D overlap by an estimated 18% and lifted segment EBITDA margin to 14.2% in 2025, showing resilience to market volatility.

Strong Sovereign Backing

As a Temasek-linked firm, ST Engineering benefits from a stable credit profile and close ties to the Singapore government, underpinning lower borrowing costs—its 2024-2025 debt facilities quoted margins ~30–50bps below peers—and reliable domestic demand for defense and public-security contracts worth S$1.2bn booked in 2024. This relationship smooths export facilitation and diplomatic channels and secures capital access for R&D, including a S$150m government-partnered tech fund launched in 2023.

Advanced Technological Integration

- AI, robotics, cybersecurity embedded across products by 2025

- Segment EBIT margin ~14% in FY2024

- 2023–2025 smart-mobility revenue CAGR ~8%

- R&D spend SG$430m (2021–2024)

Robust Record Order Book

- Multi-year backlog ~ S$6.2bn (FY2025)

- Smart-city awards ~ S$1.1bn

- Strong P2F conversion pipeline

- Improved resource planning; lower volatility

ST Engineering: Scale-driven MRO leader—S$10.4bn group, S$2.1bn MRO, <0.02 hull-loss

ST Engineering’s scale—35 facilities, 2,100+ MRO slots, S$2.1bn MRO revenue (FY2024)—drives cost and cycle-time advantages and a <0.02 hull-loss rate securing multi‑year airline contracts; group revenue S$10.4bn (FY2025) with diversified aerospace, smart city, defense mix; R&D SG$430m (2021–24) and embedded AI/cyber lift EBIT margin ~14% and smart-mobility CAGR ~8% (2023–25).

| Metric | Value |

|---|---|

| Group revenue FY2025 | S$10.4bn |

| MRO revenue FY2024 | S$2.1bn |

| Facilities / MRO slots | 35 / 2,100+ |

| EBIT margin (segment) | ~14% |

| R&D (2021–24) | SG$430m |

| Backlog FY2025 | S$6.2bn |

What is included in the product

Provides a concise SWOT analysis of ST Engineering, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and growth prospects.

Provides a concise ST Engineering SWOT snapshot for rapid strategic alignment and executive-ready presentations.

Weaknesses

Capital Intensive Operations

Maintaining ST Engineering’s global hangars and factories demands heavy capital spending; the group reported S$1.1bn in capex guidance for 2024–25 to support new aircraft types and digital manufacturing, keeping upgrade costs high into 2025. This capital intensity raises fixed costs and reduces operating leverage when utilization falls—MRO segment revenue fell 7% YoY in 2023, showing sensitivity to volume drops. High capex and a 20–30% facility fixed-cost share can compress free cash flow in downturns.

Geographic Concentration Risks

Despite global expansion, ~45% of ST Engineering’s FY2024 defense revenue came from Singapore, concentrating high-margin earnings and exposing the group to domestic budget shifts—Singapore’s 2024 defence budget rose 3.9% to SGD 16.7bn, but any future cuts would hit margins hard.

Dependence on national procurement policy makes cashflows sensitive; major contracts from DSTA and MINDEF drive profitability, so policy or timing changes can create revenue volatility.

Expanding defense sales abroad lags aerospace: international defense contracts grew only 8% YoY in 2024 for the group versus 22% for aerospace, reflecting longer sales cycles, export controls, and local offsets.

Integration of Large Acquisitions

Sensitivity to Labor Costs

ST Engineering faces a global shortfall of skilled technicians and specialized engineers in 2025, tightening hiring and raising training costs; IATA estimates a 20% shortfall in aerospace maintenance technicians by 2030, pressuring supply chains now.

Wage inflation in North America and Europe lifted labor costs ~6–8% in 2024–2025 for aerospace roles, squeezing operating margins; ST Engineering must spend to retain talent and meet contracts.

The group must invest heavily in automation and training—capital outlays and training programs can exceed 2–3% of revenue in capital-intensive units—to mitigate labor tightness and avoid service delays.

- Global technician shortfall ~20% by 2030 (IATA)

- Wage inflation 6–8% in 2024–25 in key markets

- Training/automation capex ~2–3% of revenue in units

Margin Compression in Commercial Segments

ST Engineering faces margin compression in commercial aerospace and smart-city segments as global competition drives aggressive pricing; industry-wide aero MRO margins fell toward 6–8% in 2024 versus 9–11% in 2019, pressuring providers.

Sustaining profitability needs continuous cost cuts and tech innovation—ST Engineering reported a 2024 gross margin of ~18.5%, so even small price erosion hits EPS and ROCE.

- Commercial competition: many global bidders

- Aero MRO margins down ~2–3 pp since 2019

- 2024 gross margin ~18.5% for ST Eng

- Requires lean ops + R&D to defend margins

Heavy Capex, Defense Exposure & Rising Labor Costs Squeeze Margins

Heavy capex (S$1.1bn guidance 2024–25) and ~20–30% fixed facility costs compress cash flow; ~45% FY2024 defense revenue tied to Singapore exposes margins to local budget shifts; integration of TransCore and 2023–25 tech deals delays synergies (US$120m SG&A target to 2026) while global technician shortfall (~20% by 2030) and 6–8% wage inflation lift operating costs.

| Metric | Value |

|---|---|

| Capex guidance 2024–25 | S$1.1bn |

| Defense share (FY2024) | ~45% |

| SG&A synergy target | US$120m by 2026 |

| Technician shortfall (IATA) | ~20% by 2030 |

| Wage inflation 2024–25 | 6–8% |

What You See Is What You Get

ST Engineering SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the same editable file included in your download. Buy now to unlock the complete, detailed version immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

ST Engineering’s diversified defense and aerospace portfolio, strong R&D, and global footprint position it well against cyclicality and geopolitical demand—but rising competition, regulatory pressures, and supply-chain risks merit close scrutiny. Discover the complete picture behind the company’s market position with our full SWOT analysis, offering actionable insights, financial context, and strategic takeaways to inform investment or strategic decisions.

Strengths

Dominant Global MRO Position

ST Engineering remains the world’s largest commercial airframe MRO by capacity as of late 2025, servicing over 2,100 narrow- and widebody aircraft slots across Asia, Europe and the United States, which drives unit cost advantages and 18% lower cycle times vs peers. The scale supports a global footprint with 35 facilities and $2.1 billion annual MRO revenue in FY2024. Its quality and safety record—<0.02 hull-loss events per million flight hours—helps secure multi‑year contracts with major airlines and lessors, underpinning stable backlog and repeat revenue.

Diversified Multi-Sector Portfolio

ST Engineering operates across aerospace, smart city, and defense, which provided a natural hedge and helped sustain group revenue of S$10.4 billion in FY2025, down just 2% year-on-year despite sector shocks; aerospace, smart city and defense each contributed roughly 35%, 30% and 35% of revenue, respectively. Shared AI and robotics platforms cut R&D overlap by an estimated 18% and lifted segment EBITDA margin to 14.2% in 2025, showing resilience to market volatility.

Strong Sovereign Backing

As a Temasek-linked firm, ST Engineering benefits from a stable credit profile and close ties to the Singapore government, underpinning lower borrowing costs—its 2024-2025 debt facilities quoted margins ~30–50bps below peers—and reliable domestic demand for defense and public-security contracts worth S$1.2bn booked in 2024. This relationship smooths export facilitation and diplomatic channels and secures capital access for R&D, including a S$150m government-partnered tech fund launched in 2023.

Advanced Technological Integration

- AI, robotics, cybersecurity embedded across products by 2025

- Segment EBIT margin ~14% in FY2024

- 2023–2025 smart-mobility revenue CAGR ~8%

- R&D spend SG$430m (2021–2024)

Robust Record Order Book

- Multi-year backlog ~ S$6.2bn (FY2025)

- Smart-city awards ~ S$1.1bn

- Strong P2F conversion pipeline

- Improved resource planning; lower volatility

ST Engineering: Scale-driven MRO leader—S$10.4bn group, S$2.1bn MRO, <0.02 hull-loss

ST Engineering’s scale—35 facilities, 2,100+ MRO slots, S$2.1bn MRO revenue (FY2024)—drives cost and cycle-time advantages and a <0.02 hull-loss rate securing multi‑year airline contracts; group revenue S$10.4bn (FY2025) with diversified aerospace, smart city, defense mix; R&D SG$430m (2021–24) and embedded AI/cyber lift EBIT margin ~14% and smart-mobility CAGR ~8% (2023–25).

| Metric | Value |

|---|---|

| Group revenue FY2025 | S$10.4bn |

| MRO revenue FY2024 | S$2.1bn |

| Facilities / MRO slots | 35 / 2,100+ |

| EBIT margin (segment) | ~14% |

| R&D (2021–24) | SG$430m |

| Backlog FY2025 | S$6.2bn |

What is included in the product

Provides a concise SWOT analysis of ST Engineering, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic positioning and growth prospects.

Provides a concise ST Engineering SWOT snapshot for rapid strategic alignment and executive-ready presentations.

Weaknesses

Capital Intensive Operations

Maintaining ST Engineering’s global hangars and factories demands heavy capital spending; the group reported S$1.1bn in capex guidance for 2024–25 to support new aircraft types and digital manufacturing, keeping upgrade costs high into 2025. This capital intensity raises fixed costs and reduces operating leverage when utilization falls—MRO segment revenue fell 7% YoY in 2023, showing sensitivity to volume drops. High capex and a 20–30% facility fixed-cost share can compress free cash flow in downturns.

Geographic Concentration Risks

Despite global expansion, ~45% of ST Engineering’s FY2024 defense revenue came from Singapore, concentrating high-margin earnings and exposing the group to domestic budget shifts—Singapore’s 2024 defence budget rose 3.9% to SGD 16.7bn, but any future cuts would hit margins hard.

Dependence on national procurement policy makes cashflows sensitive; major contracts from DSTA and MINDEF drive profitability, so policy or timing changes can create revenue volatility.

Expanding defense sales abroad lags aerospace: international defense contracts grew only 8% YoY in 2024 for the group versus 22% for aerospace, reflecting longer sales cycles, export controls, and local offsets.

Integration of Large Acquisitions

Sensitivity to Labor Costs

ST Engineering faces a global shortfall of skilled technicians and specialized engineers in 2025, tightening hiring and raising training costs; IATA estimates a 20% shortfall in aerospace maintenance technicians by 2030, pressuring supply chains now.

Wage inflation in North America and Europe lifted labor costs ~6–8% in 2024–2025 for aerospace roles, squeezing operating margins; ST Engineering must spend to retain talent and meet contracts.

The group must invest heavily in automation and training—capital outlays and training programs can exceed 2–3% of revenue in capital-intensive units—to mitigate labor tightness and avoid service delays.

- Global technician shortfall ~20% by 2030 (IATA)

- Wage inflation 6–8% in 2024–25 in key markets

- Training/automation capex ~2–3% of revenue in units

Margin Compression in Commercial Segments

ST Engineering faces margin compression in commercial aerospace and smart-city segments as global competition drives aggressive pricing; industry-wide aero MRO margins fell toward 6–8% in 2024 versus 9–11% in 2019, pressuring providers.

Sustaining profitability needs continuous cost cuts and tech innovation—ST Engineering reported a 2024 gross margin of ~18.5%, so even small price erosion hits EPS and ROCE.

- Commercial competition: many global bidders

- Aero MRO margins down ~2–3 pp since 2019

- 2024 gross margin ~18.5% for ST Eng

- Requires lean ops + R&D to defend margins

Heavy Capex, Defense Exposure & Rising Labor Costs Squeeze Margins

Heavy capex (S$1.1bn guidance 2024–25) and ~20–30% fixed facility costs compress cash flow; ~45% FY2024 defense revenue tied to Singapore exposes margins to local budget shifts; integration of TransCore and 2023–25 tech deals delays synergies (US$120m SG&A target to 2026) while global technician shortfall (~20% by 2030) and 6–8% wage inflation lift operating costs.

| Metric | Value |

|---|---|

| Capex guidance 2024–25 | S$1.1bn |

| Defense share (FY2024) | ~45% |

| SG&A synergy target | US$120m by 2026 |

| Technician shortfall (IATA) | ~20% by 2030 |

| Wage inflation 2024–25 | 6–8% |

What You See Is What You Get

ST Engineering SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the same editable file included in your download. Buy now to unlock the complete, detailed version immediately after payment.