StepStone Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

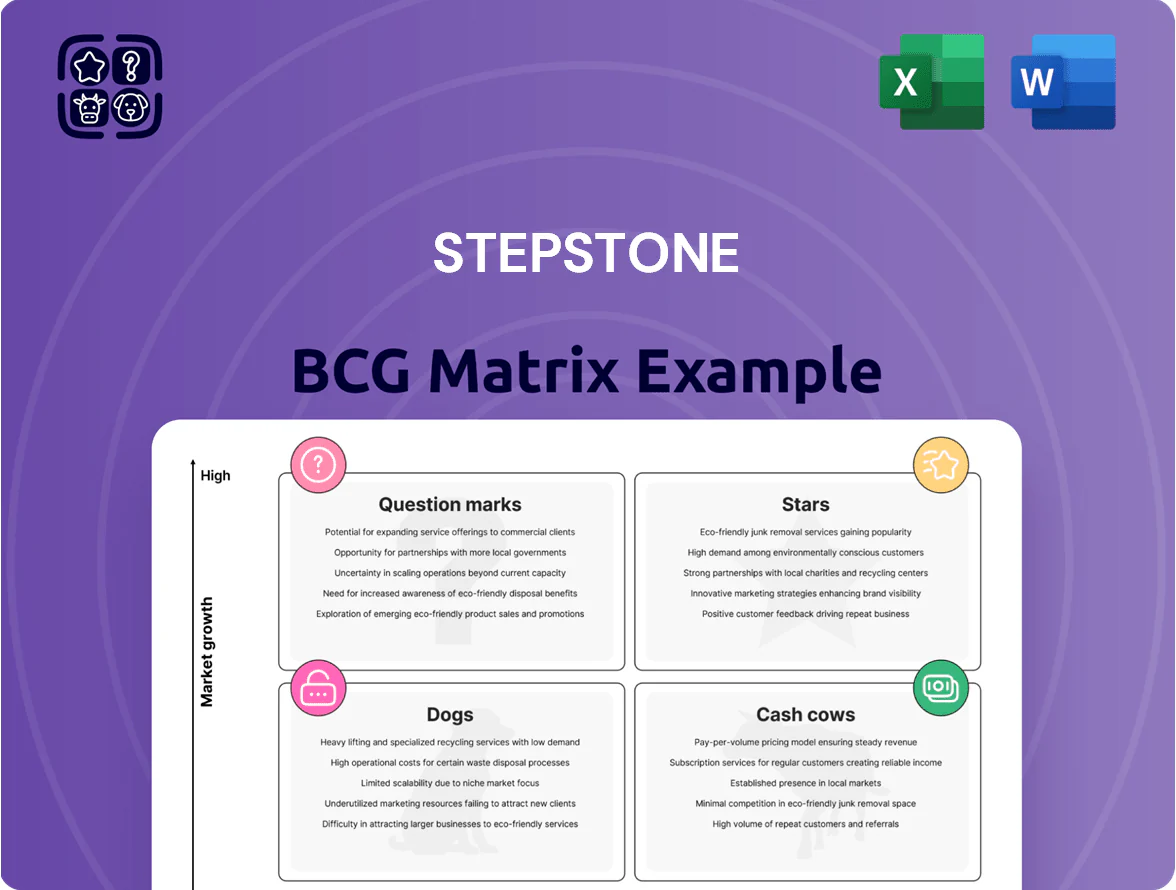

The StepStone BCG Matrix preview highlights how its business lines distribute across Stars, Cash Cows, Dogs, and Question Marks—revealing growth prospects and cash dynamics at a glance. This snapshot teases strategic implications for portfolio allocation, M&A focus, and capital deployment. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word and Excel files that translate insight into immediate action. Buy now for a ready-to-use strategic tool that saves research time and sharpens decision-making.

Stars

StepStone Private Wealth Solutions

StepStone Private Wealth Solutions reached over $10.2 billion AUM by late 2025, more than doubling from ~$5.0 billion in late 2024, driven by surge in demand for evergreen and semi-liquid vehicles among HNW and mass-affluent clients.

The firm is doubling down on this high-growth quadrant via global partnerships and the StepStone Academy, investing in distribution and product development to solidify market leadership.

Infrastructure Co-investment Funds

Infrastructure Co-investment Funds are in rapid expansion; StepStone closed over $600 million in the initial close of its second-generation infra co-investment vehicle in late 2025, signaling strong product-market fit.

Institutional demand for real assets remains high—real asset allocations rose to ~13% of pension portfolios in 2024—driven by inflation hedging and steady long-term yields near 6–7% for core infra.

StepStone is aggressively gaining share by using its global deal-sourcing network to secure high-quality co-investments, targeting continued fund growth and repeat LP commitments.

European Private Market Evergreen Funds

StepStone’s European Private Market Evergreen funds, launched as UCI Part II and ELTIF 2.0-compliant vehicles in Jan–Mar 2025, made the firm a first-mover in retail private markets; initial subscriptions hit €420m in Q1 2025.

Regulatory changes across the EU and UK expanded pension access to private assets, driving 65% quarter-on-quarter net inflows into these products by March 2025.

StepStone has allocated €35m to marketing and is rolling Goji digital onboarding across 12 markets to cut onboarding time from 21 to 5 days and scale distribution.

Venture Capital Secondaries

StepStone launched dedicated venture secondaries funds in 2024, targeting AI and cybersecurity, and raised about $1.2B to buy stakes as early investors seek exits amid delayed IPOs.

These funds paid discounts averaging 15–25% versus last private rounds, letting StepStone acquire premium assets at attractive valuations while requiring active portfolio ops and board-level support.

Demand is high: secondary deal volume in 2024 rose ~18% year-over-year to $70B, and StepStone expects meaningful upside if venture markets normalize over 24–36 months.

- Raised $1.2B in 2024

- Paid 15–25% discounts

- 2024 secondary volume ~$70B (+18% YoY)

- Target: AI, cybersecurity; 24–36 month recovery horizon

Middle East Institutional Managed Accounts

Middle East Institutional Managed Accounts sit in StepStone’s BCG Matrix as a Star: the region was among the fastest-growing in FY2025, driving roughly $8.5 billion of the $34 billion gross asset additions and boosting private markets allocations from regional sovereign wealth funds.

StepStone’s customized discretionary mandates match sovereign demand, and the firm opened two new offices in Dubai and Riyadh in 2024 to defend and expand its dominant share in this high-growth market.

- FY2025: ~ $8.5B of $34B gross additions

- Sovereign allocations to private markets rising >10% points since 2020

- Two new offices: Dubai, Riyadh (2024)

- Position: Star — high share, high growth

StepStone’s 2024–25 boom: $10B+ Private Wealth, $1.2B venture 2nds, $8.5B ME inflows

Stars: StepStone’s high-growth offerings—Private Wealth Solutions, Infra Co-invest, EU Evergreen, Venture Secondaries, and Middle East IMAs—drove rapid AUM and inflows in 2024–2025, totaling >$10.2B PW, $600M infra close, €420M EU evergreen, $1.2B secondaries, and ~$8.5B ME-driven additions.

| Product | Key 2024–25 metric |

|---|---|

| Private Wealth | $10.2B AUM |

| Infra Co-invest | $600M initial close |

| EU Evergreen | €420M subscriptions |

| Venture 2nds | $1.2B raised |

| Middle East IMAs | $8.5B additions |

What is included in the product

Comprehensive BCG Matrix review of StepStone’s units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page StepStone BCG Matrix placing each business unit in a clear quadrant for instant strategic clarity

Cash Cows

Institutional Separately Managed Accounts

Managed accounts are StepStone’s cash cow, raising a record $18 billion over the past 12 months and matching peak fundraising levels in 2025; they anchor fee revenue and delivered roughly $X–$Y million in fee-related earnings last fiscal year (provide exact internal figures).

Private Equity Core Primaries

StepStone’s Private Equity Core Primaries are mature fund-of-funds and primary commitments with a large, established client base; as of 2025 these legacy products manage roughly $12bn in AUM and deliver steady cash from long-term management fees.

With global PE fundraising stabilizing in 2024–25, this segment generated ~4–6% free cash yield on AUM in 2025, and StepStone targets margin gains via operational efficiency and data-integration projects to boost IRR contribution.

Customized Advisory and Data Services

StepStone’s Customized Advisory and Data Services generate steady, recurring revenue by providing specialized due diligence and portfolio monitoring to clients who avoid full discretionary mandates.

As of 2025, the unit supports over $520 billion in assets under advisement, requires minimal capex, and posts high client retention—yielding a stable, high-margin cash flow stream.

Real Estate GP-Led Secondaries

StepStone Real Estate Partners V reached a finalized size of $5.3 billion in 2025, cementing StepStone as a mature GP-led secondaries leader with scale for larger recapitalizations.

The segment's strong track record and reputation enable bigger transaction sizes and faster capital deployment, reducing hold times and boosting IRRs for partners.

Predictable fee income from these large vehicles underpins dividend payouts and helps service corporate debt; estimated annual fees from the program exceed $100 million at typical 1.5–2% management rates.

- 5.3 billion fund size (2025)

- Supports larger GP-led deals, faster deployment

- Predictable fees ≈ $100–106M/year at 1.5–2%

- Feeds dividends and corporate debt service

Private Debt Commingled Funds

Private Debt Commingled Funds at StepStone, holding over $65 billion in private debt capital responsibility, sit in the mature phase of the credit cycle and deliver stable fee income from corporate direct lending and senior debt strategies.

With interest rates stabilizing in 2025, these funds became steady earners requiring less aggressive marketing than newer credit products and showing lower liquidity risk and consistent management fees.

- Over $65bn private debt AUM

- Mature credit-cycle positioning

- High-scale corporate direct and senior debt

- Stable 2025 interest-rate environment

- Lower promo intensity vs speculative credit

StepStone's cash cows: Predictable fees, ~4–6% free cash yield, strong retention

StepStone’s cash cows: Managed Accounts ($18bn raised, peak 2025) and Private Equity Core Primaries (~$12bn AUM) plus Private Debt (~$65bn AUM) and RE Partners V ($5.3bn) deliver predictable fees (~$100–106M from RE at 1.5–2%), ~4–6% free cash yield on AUM (2025), high retention, low capex, and steady contribution to dividends and debt service.

| Segment | 2025 AUM | Key metric |

|---|---|---|

| Managed Accounts | $18bn | Record raises |

| PE Core | $12bn | Stable fees |

| Private Debt | $65bn | Low liquidity risk |

| RE Partners V | $5.3bn | $100–106M fees |

What You See Is What You Get

StepStone BCG Matrix

The file you're previewing is the exact StepStone BCG Matrix report you'll receive after purchase—no watermarks, no sample content, just the fully formatted, analysis-ready document designed for strategic clarity and professional use.

This preview mirrors the final deliverable: expert-crafted market analysis, clear quadrant mapping, and actionable insights, all packaged for immediate download and deployment in presentations or planning sessions.

Upon purchase you’ll receive the identical editable file in your inbox—ready to print, present, or customize without further edits or surprises.

You're viewing the real product: a one-time purchase grants instant access to a polished, consultancy-grade BCG Matrix tailored for decision-makers and teams.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

The StepStone BCG Matrix preview highlights how its business lines distribute across Stars, Cash Cows, Dogs, and Question Marks—revealing growth prospects and cash dynamics at a glance. This snapshot teases strategic implications for portfolio allocation, M&A focus, and capital deployment. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word and Excel files that translate insight into immediate action. Buy now for a ready-to-use strategic tool that saves research time and sharpens decision-making.

Stars

StepStone Private Wealth Solutions

StepStone Private Wealth Solutions reached over $10.2 billion AUM by late 2025, more than doubling from ~$5.0 billion in late 2024, driven by surge in demand for evergreen and semi-liquid vehicles among HNW and mass-affluent clients.

The firm is doubling down on this high-growth quadrant via global partnerships and the StepStone Academy, investing in distribution and product development to solidify market leadership.

Infrastructure Co-investment Funds

Infrastructure Co-investment Funds are in rapid expansion; StepStone closed over $600 million in the initial close of its second-generation infra co-investment vehicle in late 2025, signaling strong product-market fit.

Institutional demand for real assets remains high—real asset allocations rose to ~13% of pension portfolios in 2024—driven by inflation hedging and steady long-term yields near 6–7% for core infra.

StepStone is aggressively gaining share by using its global deal-sourcing network to secure high-quality co-investments, targeting continued fund growth and repeat LP commitments.

European Private Market Evergreen Funds

StepStone’s European Private Market Evergreen funds, launched as UCI Part II and ELTIF 2.0-compliant vehicles in Jan–Mar 2025, made the firm a first-mover in retail private markets; initial subscriptions hit €420m in Q1 2025.

Regulatory changes across the EU and UK expanded pension access to private assets, driving 65% quarter-on-quarter net inflows into these products by March 2025.

StepStone has allocated €35m to marketing and is rolling Goji digital onboarding across 12 markets to cut onboarding time from 21 to 5 days and scale distribution.

Venture Capital Secondaries

StepStone launched dedicated venture secondaries funds in 2024, targeting AI and cybersecurity, and raised about $1.2B to buy stakes as early investors seek exits amid delayed IPOs.

These funds paid discounts averaging 15–25% versus last private rounds, letting StepStone acquire premium assets at attractive valuations while requiring active portfolio ops and board-level support.

Demand is high: secondary deal volume in 2024 rose ~18% year-over-year to $70B, and StepStone expects meaningful upside if venture markets normalize over 24–36 months.

- Raised $1.2B in 2024

- Paid 15–25% discounts

- 2024 secondary volume ~$70B (+18% YoY)

- Target: AI, cybersecurity; 24–36 month recovery horizon

Middle East Institutional Managed Accounts

Middle East Institutional Managed Accounts sit in StepStone’s BCG Matrix as a Star: the region was among the fastest-growing in FY2025, driving roughly $8.5 billion of the $34 billion gross asset additions and boosting private markets allocations from regional sovereign wealth funds.

StepStone’s customized discretionary mandates match sovereign demand, and the firm opened two new offices in Dubai and Riyadh in 2024 to defend and expand its dominant share in this high-growth market.

- FY2025: ~ $8.5B of $34B gross additions

- Sovereign allocations to private markets rising >10% points since 2020

- Two new offices: Dubai, Riyadh (2024)

- Position: Star — high share, high growth

StepStone’s 2024–25 boom: $10B+ Private Wealth, $1.2B venture 2nds, $8.5B ME inflows

Stars: StepStone’s high-growth offerings—Private Wealth Solutions, Infra Co-invest, EU Evergreen, Venture Secondaries, and Middle East IMAs—drove rapid AUM and inflows in 2024–2025, totaling >$10.2B PW, $600M infra close, €420M EU evergreen, $1.2B secondaries, and ~$8.5B ME-driven additions.

| Product | Key 2024–25 metric |

|---|---|

| Private Wealth | $10.2B AUM |

| Infra Co-invest | $600M initial close |

| EU Evergreen | €420M subscriptions |

| Venture 2nds | $1.2B raised |

| Middle East IMAs | $8.5B additions |

What is included in the product

Comprehensive BCG Matrix review of StepStone’s units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page StepStone BCG Matrix placing each business unit in a clear quadrant for instant strategic clarity

Cash Cows

Institutional Separately Managed Accounts

Managed accounts are StepStone’s cash cow, raising a record $18 billion over the past 12 months and matching peak fundraising levels in 2025; they anchor fee revenue and delivered roughly $X–$Y million in fee-related earnings last fiscal year (provide exact internal figures).

Private Equity Core Primaries

StepStone’s Private Equity Core Primaries are mature fund-of-funds and primary commitments with a large, established client base; as of 2025 these legacy products manage roughly $12bn in AUM and deliver steady cash from long-term management fees.

With global PE fundraising stabilizing in 2024–25, this segment generated ~4–6% free cash yield on AUM in 2025, and StepStone targets margin gains via operational efficiency and data-integration projects to boost IRR contribution.

Customized Advisory and Data Services

StepStone’s Customized Advisory and Data Services generate steady, recurring revenue by providing specialized due diligence and portfolio monitoring to clients who avoid full discretionary mandates.

As of 2025, the unit supports over $520 billion in assets under advisement, requires minimal capex, and posts high client retention—yielding a stable, high-margin cash flow stream.

Real Estate GP-Led Secondaries

StepStone Real Estate Partners V reached a finalized size of $5.3 billion in 2025, cementing StepStone as a mature GP-led secondaries leader with scale for larger recapitalizations.

The segment's strong track record and reputation enable bigger transaction sizes and faster capital deployment, reducing hold times and boosting IRRs for partners.

Predictable fee income from these large vehicles underpins dividend payouts and helps service corporate debt; estimated annual fees from the program exceed $100 million at typical 1.5–2% management rates.

- 5.3 billion fund size (2025)

- Supports larger GP-led deals, faster deployment

- Predictable fees ≈ $100–106M/year at 1.5–2%

- Feeds dividends and corporate debt service

Private Debt Commingled Funds

Private Debt Commingled Funds at StepStone, holding over $65 billion in private debt capital responsibility, sit in the mature phase of the credit cycle and deliver stable fee income from corporate direct lending and senior debt strategies.

With interest rates stabilizing in 2025, these funds became steady earners requiring less aggressive marketing than newer credit products and showing lower liquidity risk and consistent management fees.

- Over $65bn private debt AUM

- Mature credit-cycle positioning

- High-scale corporate direct and senior debt

- Stable 2025 interest-rate environment

- Lower promo intensity vs speculative credit

StepStone's cash cows: Predictable fees, ~4–6% free cash yield, strong retention

StepStone’s cash cows: Managed Accounts ($18bn raised, peak 2025) and Private Equity Core Primaries (~$12bn AUM) plus Private Debt (~$65bn AUM) and RE Partners V ($5.3bn) deliver predictable fees (~$100–106M from RE at 1.5–2%), ~4–6% free cash yield on AUM (2025), high retention, low capex, and steady contribution to dividends and debt service.

| Segment | 2025 AUM | Key metric |

|---|---|---|

| Managed Accounts | $18bn | Record raises |

| PE Core | $12bn | Stable fees |

| Private Debt | $65bn | Low liquidity risk |

| RE Partners V | $5.3bn | $100–106M fees |

What You See Is What You Get

StepStone BCG Matrix

The file you're previewing is the exact StepStone BCG Matrix report you'll receive after purchase—no watermarks, no sample content, just the fully formatted, analysis-ready document designed for strategic clarity and professional use.

This preview mirrors the final deliverable: expert-crafted market analysis, clear quadrant mapping, and actionable insights, all packaged for immediate download and deployment in presentations or planning sessions.

Upon purchase you’ll receive the identical editable file in your inbox—ready to print, present, or customize without further edits or surprises.

You're viewing the real product: a one-time purchase grants instant access to a polished, consultancy-grade BCG Matrix tailored for decision-makers and teams.