Stifel Financial Porter's Five Forces Analysis

Don't Miss the Bigger Picture

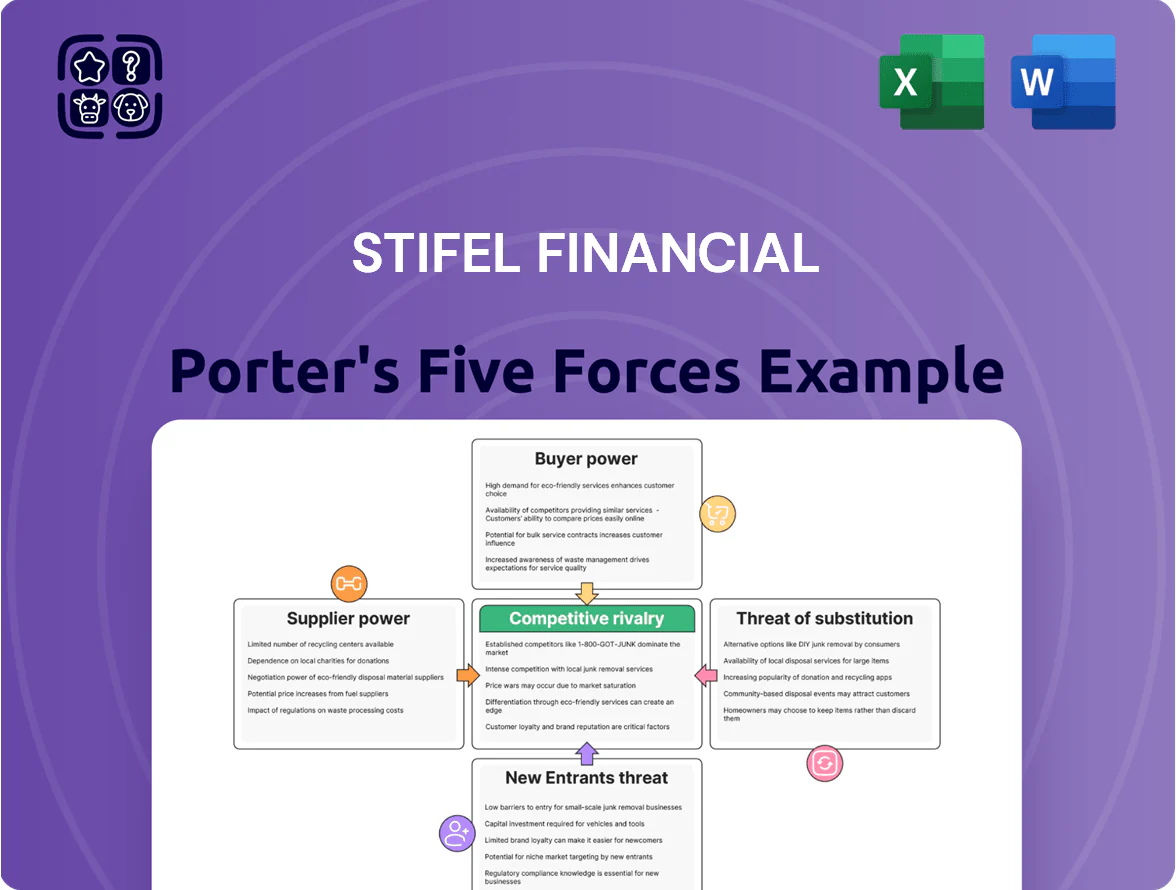

Stifel Financial faces moderate buyer power, intense rivalry, and regulatory pressures that shape its advisory and wealth-management margins, while supplier and entrant threats remain manageable for now.

Suppliers Bargaining Power

Retention of Elite Human Capital

The primary suppliers for Stifel are its financial advisors, investment bankers, and research analysts whose intellectual capital drives revenue; by end-2025 competition for top talent rose sharply, with industry attrition for senior advisors hitting ~12% and top-producer pay packages increasing 8–12% year-over-year, giving suppliers leverage to demand higher compensation and payout splits. Stifel must keep an entrepreneurial culture and competitive commission splits (often 60–80% for rainmakers) to prevent defections to independents or boutiques.

Dominance of Market Data Providers

Stifel relies on a small set of market-data and infrastructure vendors—Bloomberg, Refinitiv (LSEG), and major exchanges—for real-time pricing and analytics, creating high supplier power because feeds are embedded in trading and research stacks and costly to replace; industry reports show enterprise data costs rose ~12% in 2025, squeezing mid-tier firms where data/tech can be 8–15% of operating expenses and pressuring Stifel’s margins.

Regulatory and Compliance Authorities

Regulatory bodies like the SEC and FINRA act as non-traditional suppliers by granting licenses and the legal framework Stifel needs to operate; their power is absolute because revocation ends market access. As of Q4 2025, SEC/FINRA AI guidance raised compliance costs—Stifel reported a $12m increase in tech and compliance spend in 2025 to meet AI oversight and stay eligible for underwriting mandates.

Technology and Cybersecurity Vendors

Stifel depends on major cloud and cybersecurity vendors as it scales digital wealth products; in 2025 roughly 35% of client-facing apps run on third-party clouds, making these suppliers strategically critical.

Switching costs are high due to technical debt and compliance; industry estimates show platform migration can cost 5–15% of annual IT budget and take 9–18 months, boosting vendor leverage.

Client demand for advanced mobile UX and secure digital vaults rose 28% year-over-year in 2025, increasing Stifel’s reliance on specialized security firms and concentrating supplier power.

- 35% client apps on third-party cloud (2025)

- Migration cost 5–15% IT budget; 9–18 months

- 28% YoY rise in demand for secure digital vaults (2025)

Access to Wholesale Funding Markets

Stifel needs steady access to wholesale funding to finance its balance sheet and support institutional trading; banks and institutional lenders supply this liquidity and their bargaining power rises when rates climb or markets spike in volatility.

In late 2025, a 150–200bp widening in corporate credit spreads would raise Stifel’s unsecured funding costs materially, squeezing margins on margin lending and repo financing and forcing higher client rates or reduced capacity.

- Dependence: wholesale funding for trading and margin lending

- Supplier power: higher when Fed rates and volatility rise

- Impact: 150–200bp spread widening increases funding cost sharply

- Response: pass costs to clients or cut leverage

Rising supplier costs, talent drain & spread shock squeeze margins in 2025

Suppliers wield high power: advisors demand 8–12% higher pay (senior attrition ~12% 2025), data vendors (Bloomberg/Refinitiv) raised costs ~12% (data 8–15% of Opex), cloud use 35% of client apps, compliance/AI added $12m in 2025, migration costs 5–15% IT budget (9–18 months), funding spreads +150–200bp sharply raise unsecured costs.

| Metric | 2025 |

|---|---|

| Advisor attrition | ~12% |

| Pay rise | 8–12% |

| Data cost rise | ~12% |

| Cloud apps | 35% |

| Compliance spend | $12m |

| Migration cost | 5–15% IT |

| Spread shock | +150–200bp |

What is included in the product

Tailored Porter's Five Forces analysis for Stifel Financial that uncovers competitive drivers, buyer and supplier influence, barriers to entry, and substitutes, highlighting disruptive threats and strategic levers to protect market share.

A concise, one-sheet Porter's Five Forces for Stifel—instantly highlights competitive pressures and relieves analysis overload for quick, confident decisions.

Customers Bargaining Power

Institutional Pressure on Commission Rates

Institutional clients like hedge funds and pension managers wield high bargaining power, routing large volumes through Stifel’s institutional group and pushing for lower execution fees and bundled services that compress secondary-trading margins.

By 2025, electronic execution growth—US equity institutional electronic share increased to ~70% of volume in 2024—lets these buyers shop for sub-penny transaction costs, forcing Stifel to match fee cuts or risk loss of flow.

High Net Worth Client Sophistication

The wealth-management segment faces savvy High Net Worth Individuals (HNWs) who in 2024 held roughly 6.6 million global HNW households and compared fees via platforms showing average advisory fees of ~0.75% AUM; they can easily benchmark Stifel’s performance and fees against wirehouses (Morgan Stanley, UBS) and RIAs, pushing demand for personalized, holistic planning that includes tax-loss harvesting, trust/estate strategies, and family-office services.

Low Switching Costs for Retail Investors

Individual retail investors face low switching costs: 2024 data show ACATS (Automated Customer Account Transfer Service) transfers rose 8% to 28.7 million moves, making account migration fast and cheap, so price and platform matter more.

Personal advisor ties add stickiness—Stifel offsets easy exits by offering deeper, relationship-driven wealth management and fee-based advice that discount brokers (average advisory fees ~0.50% vs Stifel’s higher mix) find hard to copy.

Corporate Client Leverage in M and A

Corporate clients often run competitive pitch processes for M&A and capital raises, letting 3–7 banks bid; this drove average negotiated success-fee cuts of 15–30% in 2024–2025 for $500m+ deals, boosting buyer leverage.

Stifel’s mid-market strength (median deal size ~ $250m in 2025) reduces client bargaining power via sector expertise and repeat relationships, though megadeals remain buyer-centric.

- 3–7 banks per pitch

- 15–30% average fee reduction on $500m+ deals

- Stifel median deal ~$250m (2025)

- Large deals remain buyer-favorable

Demand for ESG and Values Based Investing

By end-2025, an estimated $40 trillion in global AUM is tied to ESG mandates, pushing retail and institutional clients to demand ESG-aligned products; Stifel must broaden offerings and deepen ESG research to retain flows.

Clients can move capital quickly to firms with clearer ESG metrics and stewardship; in 2024, 56% of institutional allocators cited ESG integration as a top selection factor, increasing Stifel's customer bargaining power.

- ~$40T global ESG AUM by 2025

- 56% institutional priority on ESG (2024)

- Transparency and integration drive flows

Clients’ Bargaining Power Surges: Fees Cut, Electronic Execution & ESG Shift Leverage

Clients hold high bargaining power: institutional electronic execution (≈70% US equity volume in 2024) pressures fees, HNWs compare advisory rates (~0.75% avg) and ACATS transfers rose 8% to 28.7M in 2024 easing exits; corporate pitches (3–7 banks) cut $500M+ deal fees 15–30% (2024–25). ESG flows (~$40T AUM by 2025; 56% allocators cite ESG importance in 2024) further shift leverage to buyers.

| Metric | Value |

|---|---|

| US equity electronic share (2024) | ~70% |

| ACATS transfers (2024) | 28.7M (+8%) |

| Avg HNW advisory fee | ~0.75% AUM |

| Pitch banks per deal | 3–7 |

| Fee cut on $500M+ deals (2024–25) | 15–30% |

| Global ESG AUM (2025 est.) | ~$40T |

| Institutional priority on ESG (2024) | 56% |

Preview Before You Purchase

Stifel Financial Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Stifel Financial you'll receive immediately after purchase—no placeholders, no previews.

The document displayed here is the full, professionally formatted analysis—ready to download and use the moment you buy.

No mockups or samples: the file you see is the deliverable you’ll get instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Stifel Financial faces moderate buyer power, intense rivalry, and regulatory pressures that shape its advisory and wealth-management margins, while supplier and entrant threats remain manageable for now.

Suppliers Bargaining Power

Retention of Elite Human Capital

The primary suppliers for Stifel are its financial advisors, investment bankers, and research analysts whose intellectual capital drives revenue; by end-2025 competition for top talent rose sharply, with industry attrition for senior advisors hitting ~12% and top-producer pay packages increasing 8–12% year-over-year, giving suppliers leverage to demand higher compensation and payout splits. Stifel must keep an entrepreneurial culture and competitive commission splits (often 60–80% for rainmakers) to prevent defections to independents or boutiques.

Dominance of Market Data Providers

Stifel relies on a small set of market-data and infrastructure vendors—Bloomberg, Refinitiv (LSEG), and major exchanges—for real-time pricing and analytics, creating high supplier power because feeds are embedded in trading and research stacks and costly to replace; industry reports show enterprise data costs rose ~12% in 2025, squeezing mid-tier firms where data/tech can be 8–15% of operating expenses and pressuring Stifel’s margins.

Regulatory and Compliance Authorities

Regulatory bodies like the SEC and FINRA act as non-traditional suppliers by granting licenses and the legal framework Stifel needs to operate; their power is absolute because revocation ends market access. As of Q4 2025, SEC/FINRA AI guidance raised compliance costs—Stifel reported a $12m increase in tech and compliance spend in 2025 to meet AI oversight and stay eligible for underwriting mandates.

Technology and Cybersecurity Vendors

Stifel depends on major cloud and cybersecurity vendors as it scales digital wealth products; in 2025 roughly 35% of client-facing apps run on third-party clouds, making these suppliers strategically critical.

Switching costs are high due to technical debt and compliance; industry estimates show platform migration can cost 5–15% of annual IT budget and take 9–18 months, boosting vendor leverage.

Client demand for advanced mobile UX and secure digital vaults rose 28% year-over-year in 2025, increasing Stifel’s reliance on specialized security firms and concentrating supplier power.

- 35% client apps on third-party cloud (2025)

- Migration cost 5–15% IT budget; 9–18 months

- 28% YoY rise in demand for secure digital vaults (2025)

Access to Wholesale Funding Markets

Stifel needs steady access to wholesale funding to finance its balance sheet and support institutional trading; banks and institutional lenders supply this liquidity and their bargaining power rises when rates climb or markets spike in volatility.

In late 2025, a 150–200bp widening in corporate credit spreads would raise Stifel’s unsecured funding costs materially, squeezing margins on margin lending and repo financing and forcing higher client rates or reduced capacity.

- Dependence: wholesale funding for trading and margin lending

- Supplier power: higher when Fed rates and volatility rise

- Impact: 150–200bp spread widening increases funding cost sharply

- Response: pass costs to clients or cut leverage

Rising supplier costs, talent drain & spread shock squeeze margins in 2025

Suppliers wield high power: advisors demand 8–12% higher pay (senior attrition ~12% 2025), data vendors (Bloomberg/Refinitiv) raised costs ~12% (data 8–15% of Opex), cloud use 35% of client apps, compliance/AI added $12m in 2025, migration costs 5–15% IT budget (9–18 months), funding spreads +150–200bp sharply raise unsecured costs.

| Metric | 2025 |

|---|---|

| Advisor attrition | ~12% |

| Pay rise | 8–12% |

| Data cost rise | ~12% |

| Cloud apps | 35% |

| Compliance spend | $12m |

| Migration cost | 5–15% IT |

| Spread shock | +150–200bp |

What is included in the product

Tailored Porter's Five Forces analysis for Stifel Financial that uncovers competitive drivers, buyer and supplier influence, barriers to entry, and substitutes, highlighting disruptive threats and strategic levers to protect market share.

A concise, one-sheet Porter's Five Forces for Stifel—instantly highlights competitive pressures and relieves analysis overload for quick, confident decisions.

Customers Bargaining Power

Institutional Pressure on Commission Rates

Institutional clients like hedge funds and pension managers wield high bargaining power, routing large volumes through Stifel’s institutional group and pushing for lower execution fees and bundled services that compress secondary-trading margins.

By 2025, electronic execution growth—US equity institutional electronic share increased to ~70% of volume in 2024—lets these buyers shop for sub-penny transaction costs, forcing Stifel to match fee cuts or risk loss of flow.

High Net Worth Client Sophistication

The wealth-management segment faces savvy High Net Worth Individuals (HNWs) who in 2024 held roughly 6.6 million global HNW households and compared fees via platforms showing average advisory fees of ~0.75% AUM; they can easily benchmark Stifel’s performance and fees against wirehouses (Morgan Stanley, UBS) and RIAs, pushing demand for personalized, holistic planning that includes tax-loss harvesting, trust/estate strategies, and family-office services.

Low Switching Costs for Retail Investors

Individual retail investors face low switching costs: 2024 data show ACATS (Automated Customer Account Transfer Service) transfers rose 8% to 28.7 million moves, making account migration fast and cheap, so price and platform matter more.

Personal advisor ties add stickiness—Stifel offsets easy exits by offering deeper, relationship-driven wealth management and fee-based advice that discount brokers (average advisory fees ~0.50% vs Stifel’s higher mix) find hard to copy.

Corporate Client Leverage in M and A

Corporate clients often run competitive pitch processes for M&A and capital raises, letting 3–7 banks bid; this drove average negotiated success-fee cuts of 15–30% in 2024–2025 for $500m+ deals, boosting buyer leverage.

Stifel’s mid-market strength (median deal size ~ $250m in 2025) reduces client bargaining power via sector expertise and repeat relationships, though megadeals remain buyer-centric.

- 3–7 banks per pitch

- 15–30% average fee reduction on $500m+ deals

- Stifel median deal ~$250m (2025)

- Large deals remain buyer-favorable

Demand for ESG and Values Based Investing

By end-2025, an estimated $40 trillion in global AUM is tied to ESG mandates, pushing retail and institutional clients to demand ESG-aligned products; Stifel must broaden offerings and deepen ESG research to retain flows.

Clients can move capital quickly to firms with clearer ESG metrics and stewardship; in 2024, 56% of institutional allocators cited ESG integration as a top selection factor, increasing Stifel's customer bargaining power.

- ~$40T global ESG AUM by 2025

- 56% institutional priority on ESG (2024)

- Transparency and integration drive flows

Clients’ Bargaining Power Surges: Fees Cut, Electronic Execution & ESG Shift Leverage

Clients hold high bargaining power: institutional electronic execution (≈70% US equity volume in 2024) pressures fees, HNWs compare advisory rates (~0.75% avg) and ACATS transfers rose 8% to 28.7M in 2024 easing exits; corporate pitches (3–7 banks) cut $500M+ deal fees 15–30% (2024–25). ESG flows (~$40T AUM by 2025; 56% allocators cite ESG importance in 2024) further shift leverage to buyers.

| Metric | Value |

|---|---|

| US equity electronic share (2024) | ~70% |

| ACATS transfers (2024) | 28.7M (+8%) |

| Avg HNW advisory fee | ~0.75% AUM |

| Pitch banks per deal | 3–7 |

| Fee cut on $500M+ deals (2024–25) | 15–30% |

| Global ESG AUM (2025 est.) | ~$40T |

| Institutional priority on ESG (2024) | 56% |

Preview Before You Purchase

Stifel Financial Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Stifel Financial you'll receive immediately after purchase—no placeholders, no previews.

The document displayed here is the full, professionally formatted analysis—ready to download and use the moment you buy.

No mockups or samples: the file you see is the deliverable you’ll get instantly after payment.