StoneCo PESTLE Analysis

Your Competitive Advantage Starts with This Report

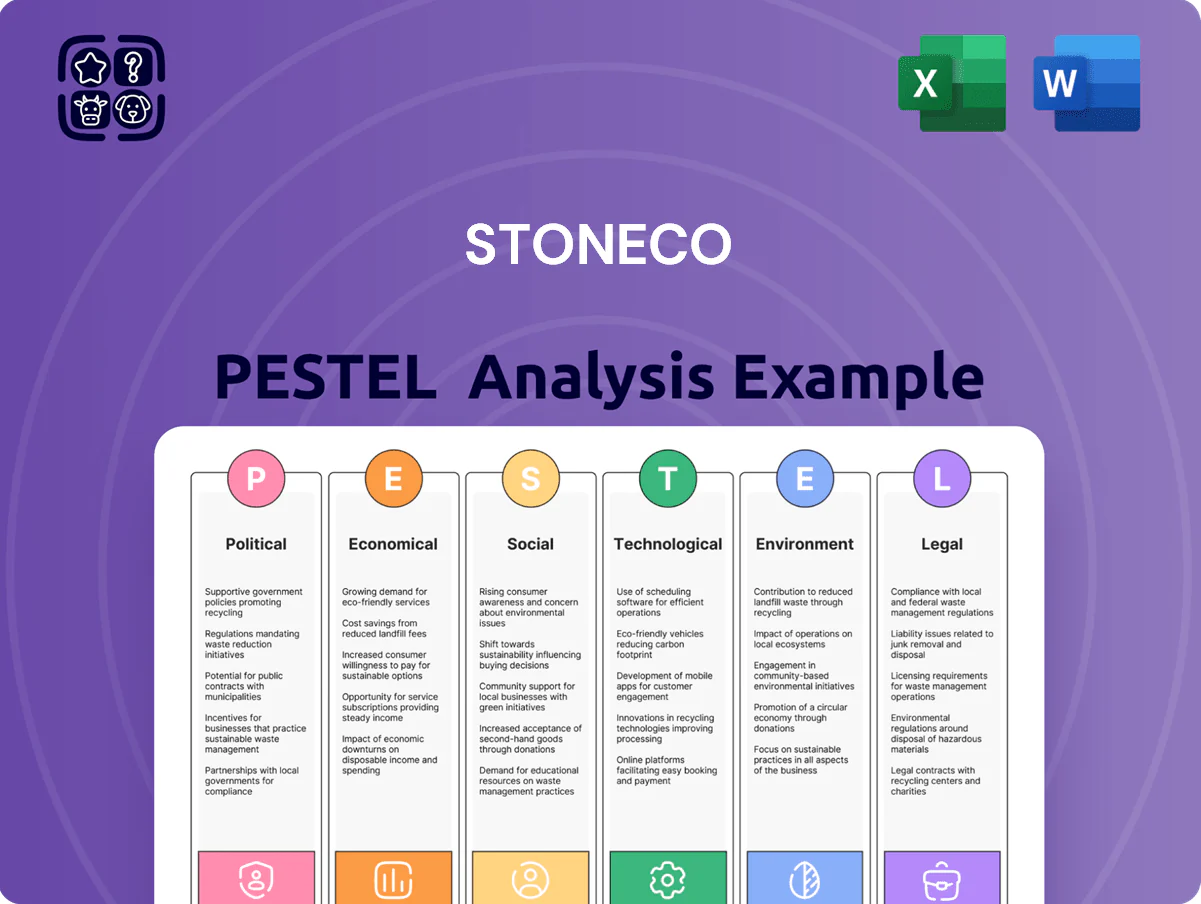

Gain a strategic advantage with our concise PESTLE Analysis of StoneCo—unpack how political shifts, economic trends, social dynamics, technological innovation, legal changes, and environmental factors will shape its trajectory; perfect for investors and strategists seeking actionable clarity. Buy the full report to access the complete, editable analysis and make smarter, faster decisions.

Political factors

Central Bank Independence and Monetary Policy

The autonomy of the Brazilian Central Bank is vital for StoneCo, providing a predictable monetary environment; Brazil's Selic rate stood at 10.75% in Dec 2025 consensus forecasts, and stable leadership through 2025 supports investor confidence in the real, which traded near 5.2 BRL/USD in 2024–2025; political interference in rate decisions could spike volatility, raising StoneCo's funding costs and compressing margins on its credit products.

Implementation of Comprehensive Tax Reforms

The shift toward a unified VAT in Brazil, targeted for phased implementation from 2024-2025, materially affects StoneCo’s payments and services segment, which processed R$78.5 billion in TPV in FY2024; simplification could reduce compliance costs but forces system overhauls.

StoneCo faces one-time IT and billing investments—industry estimates suggest 0.5–1.5% of revenues—while reviewing pricing to protect 2024 gross margins of ~36%.

Proactive merchant support and API upgrades will be critical to retain SMEs and limit churn amid regulatory rollout and potential short-term margin pressure.

Government Programs for SME Support

Federal programs like Brasil Mais Produtivo and BNDES credit lines that allocated over BRL 30 billion to SMEs in 2024 boost demand for StoneCo’s POS, gateway and banking services, expanding its addressable SME market; formalization drives digital adoption, with Brazil’s formal SME base rising 6.8% YoY to ~5.2 million in 2024, increasing potential merchant clients for StoneCo.

Regulatory Lobbying and Industry Influence

StoneCo navigates a Brazilian political arena where legacy banks resist fintech growth; in 2024 fintechs captured over 18% of payment volume, intensifying regulatory battles.

StoneCo is active in associations like Febraban and ABFintechs, lobbying for open access; such advocacy is key as proposed interchange cap changes could cut merchant acquiring revenue by an estimated 5–8%.

Legislative shifts on credit-card rules and interchange fees—where Brazil processed R$2.7 trillion in card transactions in 2024—directly affect StoneCo’s TPV-linked margins and fee income.

- Fintechs >18% payment volume share in 2024

- R$2.7 trillion card transactions in 2024

- Interchange cap risk could reduce acquiring revenue 5–8%

Geopolitical Relations and Foreign Investment

Brazil's active BRICS+ role and improving trade ties with the US affect foreign capital flows; foreign direct investment into Brazil totaled about $47.7 billion in 2023, signaling investor appetite that benefits exporters like StoneCo.

As a Nasdaq-listed firm, StoneCo remains sensitive to perceptions of Brazilian political risk—Brazil's EMBI sovereign spread averaged ~370 bps in 2024, influencing international investor demand and cost of capital.

Stable geopolitics supports long-term institutional investment critical for StoneCo's valuation and market access; foreign ownership in Brazilian equities was ~22% in 2024, underpinning liquidity for Nasdaq-listed issuers.

- 2023 FDI into Brazil: $47.7B

- EMBI spread avg 2024: ~370 bps

- Foreign ownership of Brazilian equities 2024: ~22%

StoneCo: VAT risks shave revenue but SME credit and formalization boost growth; markets watch EMBI

Political stability and Central Bank autonomy support predictable funding costs (Selic ~10.75% in 2025 consensus) while VAT reform (phased 2024–25) and potential interchange caps threaten 5–8% of acquiring revenue; BNDES/SME credit (BRL30B in 2024) and rising formal SMEs (+6.8% to ~5.2M in 2024) expand StoneCo’s market, but EMBI ~370bps and 22% foreign equity ownership keep Nasdaq sentiment sensitive.

| Metric | Value |

|---|---|

| Selic (2025 consensus) | 10.75% |

| Card volume (2024) | R$2.7T |

| SME credit via BNDES (2024) | BRL30B |

| Formal SMEs (2024) | ~5.2M (+6.8% YoY) |

| Fintech payment share (2024) | >18% |

| EMBI (avg 2024) | ~370bps |

What is included in the product

Explores how external macro-environmental factors uniquely affect StoneCo across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and forward-looking insights to inform strategy, risk management, and investor communications.

A concise, visually segmented PESTLE summary for StoneCo that removes clutter and supports quick decision-making in meetings or presentations.

Economic factors

Fluctuations in the Selic Interest Rate

The Selic rate, Brazil's benchmark, directly drives StoneCo's profitability via credit and prepayment products: higher Selic raises cost of capital but enabled net interest income, with average Selic at 13.75% in 2023–2024 and falling to ~9.25% by mid‑2025 per central bank data. Stabilization around late‑2025 near current levels will set the balance between StoneCo's funding costs and financial revenue, affecting NIMs and credit spreads.

Inflationary Trends and Consumer Spending

Persistent inflation in Brazil—IPCA at 4.9% in 2024 YTD—erodes consumer purchasing power and can compress StoneCo’s Total Payment Volume (TPV) as discretionary spending falls despite higher nominal transaction values.

Higher prices may lift TPV nominally but reduce transaction counts and average ticket frequency, especially in lower-income segments where real wages lag inflation.

StoneCo adjusts credit risk models and underwriting limits; in 2024 the company cited increased provisions and closer monitoring of merchant churn to protect ecosystem health.

Currency Exchange Rate Volatility

The BRL/USD rate averaged about 5.10 in 2024 and traded near 5.25 in early 2025; because StoneCo’s hardware and cloud costs are largely dollar-denominated, a 10% depreciation of the Real can erode gross margins materially, increasing reported operating costs in BRL terms.

Credit Market Liquidity and Risk Appetite

Credit market liquidity in Brazil shapes StoneCo’s SME loan growth; tighter liquidity in 2024-25 raised funding costs as Brazil’s corporate credit spreads widened to ~220–260 bps vs. pre-2020 levels, limiting origination.

Economic cycles alter institutional lenders’ risk appetite and capital market access; in 2024 Brazil’s SELIC at 11.75% tightened bank balance sheets, reducing willingness to take unsecured merchant credit exposure.

In stronger conditions StoneCo can securitize receivables and lower funding costs—2023–24 securitizations in Brazil totaled ~BRL 180–210 billion, improving pricing and enabling competitive SME credit offers.

- Higher liquidity → easier loan book expansion

- Tight liquidity + high SELIC → higher funding costs, reduced appetite

- Securitization market (~BRL 180–210bn) aids competitive credit in good cycles

GDP Growth and Formalization of the Economy

Brazil's GDP grew 3.2% in 2023 and IMF forecasts ~2.1% for 2024, directly influencing retail and services demand that drives StoneCo's payment volumes.

Economic expansion spurs new merchants and POS adoption; StoneCo reported TPV growth of 21% in FY2023, reflecting this linkage.

Formalization continues: electronic transactions rose ~12% y/y in 2023 vs cash, offering structural upside independent of cyclical swings.

- GDP growth ~3.2% (2023); IMF ~2.1% (2024)

- StoneCo TPV +21% FY2023

- Electronic transactions +12% y/y (2023)

Falling Selic and strong GDP boost NII and TPV despite inflation & FX pressure

Selic fell from 13.75% (2023–24 avg) to ~9.25% by mid‑2025, raising NII vs funding costs; IPCA ~4.9% (2024 YTD) weakens real consumption; BRL/USD ~5.10 (2024) → 5.25 (early 2025) pressures dollar costs; GDP 3.2% (2023) vs IMF 2.1% (2024) supports TPV growth (StoneCo TPV +21% FY2023).

| Metric | Value |

|---|---|

| Selic | ~9.25% (mid‑2025) |

| IPCA | 4.9% (2024 YTD) |

| BRL/USD | ~5.10–5.25 (2024–25) |

| GDP | 3.2% (2023) |

| StoneCo TPV | +21% (FY2023) |

What You See Is What You Get

StoneCo PESTLE Analysis

The preview shown here is the exact StoneCo PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment.

No placeholders or teasers—this is the real, professionally structured analysis you’ll own upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our concise PESTLE Analysis of StoneCo—unpack how political shifts, economic trends, social dynamics, technological innovation, legal changes, and environmental factors will shape its trajectory; perfect for investors and strategists seeking actionable clarity. Buy the full report to access the complete, editable analysis and make smarter, faster decisions.

Political factors

Central Bank Independence and Monetary Policy

The autonomy of the Brazilian Central Bank is vital for StoneCo, providing a predictable monetary environment; Brazil's Selic rate stood at 10.75% in Dec 2025 consensus forecasts, and stable leadership through 2025 supports investor confidence in the real, which traded near 5.2 BRL/USD in 2024–2025; political interference in rate decisions could spike volatility, raising StoneCo's funding costs and compressing margins on its credit products.

Implementation of Comprehensive Tax Reforms

The shift toward a unified VAT in Brazil, targeted for phased implementation from 2024-2025, materially affects StoneCo’s payments and services segment, which processed R$78.5 billion in TPV in FY2024; simplification could reduce compliance costs but forces system overhauls.

StoneCo faces one-time IT and billing investments—industry estimates suggest 0.5–1.5% of revenues—while reviewing pricing to protect 2024 gross margins of ~36%.

Proactive merchant support and API upgrades will be critical to retain SMEs and limit churn amid regulatory rollout and potential short-term margin pressure.

Government Programs for SME Support

Federal programs like Brasil Mais Produtivo and BNDES credit lines that allocated over BRL 30 billion to SMEs in 2024 boost demand for StoneCo’s POS, gateway and banking services, expanding its addressable SME market; formalization drives digital adoption, with Brazil’s formal SME base rising 6.8% YoY to ~5.2 million in 2024, increasing potential merchant clients for StoneCo.

Regulatory Lobbying and Industry Influence

StoneCo navigates a Brazilian political arena where legacy banks resist fintech growth; in 2024 fintechs captured over 18% of payment volume, intensifying regulatory battles.

StoneCo is active in associations like Febraban and ABFintechs, lobbying for open access; such advocacy is key as proposed interchange cap changes could cut merchant acquiring revenue by an estimated 5–8%.

Legislative shifts on credit-card rules and interchange fees—where Brazil processed R$2.7 trillion in card transactions in 2024—directly affect StoneCo’s TPV-linked margins and fee income.

- Fintechs >18% payment volume share in 2024

- R$2.7 trillion card transactions in 2024

- Interchange cap risk could reduce acquiring revenue 5–8%

Geopolitical Relations and Foreign Investment

Brazil's active BRICS+ role and improving trade ties with the US affect foreign capital flows; foreign direct investment into Brazil totaled about $47.7 billion in 2023, signaling investor appetite that benefits exporters like StoneCo.

As a Nasdaq-listed firm, StoneCo remains sensitive to perceptions of Brazilian political risk—Brazil's EMBI sovereign spread averaged ~370 bps in 2024, influencing international investor demand and cost of capital.

Stable geopolitics supports long-term institutional investment critical for StoneCo's valuation and market access; foreign ownership in Brazilian equities was ~22% in 2024, underpinning liquidity for Nasdaq-listed issuers.

- 2023 FDI into Brazil: $47.7B

- EMBI spread avg 2024: ~370 bps

- Foreign ownership of Brazilian equities 2024: ~22%

StoneCo: VAT risks shave revenue but SME credit and formalization boost growth; markets watch EMBI

Political stability and Central Bank autonomy support predictable funding costs (Selic ~10.75% in 2025 consensus) while VAT reform (phased 2024–25) and potential interchange caps threaten 5–8% of acquiring revenue; BNDES/SME credit (BRL30B in 2024) and rising formal SMEs (+6.8% to ~5.2M in 2024) expand StoneCo’s market, but EMBI ~370bps and 22% foreign equity ownership keep Nasdaq sentiment sensitive.

| Metric | Value |

|---|---|

| Selic (2025 consensus) | 10.75% |

| Card volume (2024) | R$2.7T |

| SME credit via BNDES (2024) | BRL30B |

| Formal SMEs (2024) | ~5.2M (+6.8% YoY) |

| Fintech payment share (2024) | >18% |

| EMBI (avg 2024) | ~370bps |

What is included in the product

Explores how external macro-environmental factors uniquely affect StoneCo across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and forward-looking insights to inform strategy, risk management, and investor communications.

A concise, visually segmented PESTLE summary for StoneCo that removes clutter and supports quick decision-making in meetings or presentations.

Economic factors

Fluctuations in the Selic Interest Rate

The Selic rate, Brazil's benchmark, directly drives StoneCo's profitability via credit and prepayment products: higher Selic raises cost of capital but enabled net interest income, with average Selic at 13.75% in 2023–2024 and falling to ~9.25% by mid‑2025 per central bank data. Stabilization around late‑2025 near current levels will set the balance between StoneCo's funding costs and financial revenue, affecting NIMs and credit spreads.

Inflationary Trends and Consumer Spending

Persistent inflation in Brazil—IPCA at 4.9% in 2024 YTD—erodes consumer purchasing power and can compress StoneCo’s Total Payment Volume (TPV) as discretionary spending falls despite higher nominal transaction values.

Higher prices may lift TPV nominally but reduce transaction counts and average ticket frequency, especially in lower-income segments where real wages lag inflation.

StoneCo adjusts credit risk models and underwriting limits; in 2024 the company cited increased provisions and closer monitoring of merchant churn to protect ecosystem health.

Currency Exchange Rate Volatility

The BRL/USD rate averaged about 5.10 in 2024 and traded near 5.25 in early 2025; because StoneCo’s hardware and cloud costs are largely dollar-denominated, a 10% depreciation of the Real can erode gross margins materially, increasing reported operating costs in BRL terms.

Credit Market Liquidity and Risk Appetite

Credit market liquidity in Brazil shapes StoneCo’s SME loan growth; tighter liquidity in 2024-25 raised funding costs as Brazil’s corporate credit spreads widened to ~220–260 bps vs. pre-2020 levels, limiting origination.

Economic cycles alter institutional lenders’ risk appetite and capital market access; in 2024 Brazil’s SELIC at 11.75% tightened bank balance sheets, reducing willingness to take unsecured merchant credit exposure.

In stronger conditions StoneCo can securitize receivables and lower funding costs—2023–24 securitizations in Brazil totaled ~BRL 180–210 billion, improving pricing and enabling competitive SME credit offers.

- Higher liquidity → easier loan book expansion

- Tight liquidity + high SELIC → higher funding costs, reduced appetite

- Securitization market (~BRL 180–210bn) aids competitive credit in good cycles

GDP Growth and Formalization of the Economy

Brazil's GDP grew 3.2% in 2023 and IMF forecasts ~2.1% for 2024, directly influencing retail and services demand that drives StoneCo's payment volumes.

Economic expansion spurs new merchants and POS adoption; StoneCo reported TPV growth of 21% in FY2023, reflecting this linkage.

Formalization continues: electronic transactions rose ~12% y/y in 2023 vs cash, offering structural upside independent of cyclical swings.

- GDP growth ~3.2% (2023); IMF ~2.1% (2024)

- StoneCo TPV +21% FY2023

- Electronic transactions +12% y/y (2023)

Falling Selic and strong GDP boost NII and TPV despite inflation & FX pressure

Selic fell from 13.75% (2023–24 avg) to ~9.25% by mid‑2025, raising NII vs funding costs; IPCA ~4.9% (2024 YTD) weakens real consumption; BRL/USD ~5.10 (2024) → 5.25 (early 2025) pressures dollar costs; GDP 3.2% (2023) vs IMF 2.1% (2024) supports TPV growth (StoneCo TPV +21% FY2023).

| Metric | Value |

|---|---|

| Selic | ~9.25% (mid‑2025) |

| IPCA | 4.9% (2024 YTD) |

| BRL/USD | ~5.10–5.25 (2024–25) |

| GDP | 3.2% (2023) |

| StoneCo TPV | +21% (FY2023) |

What You See Is What You Get

StoneCo PESTLE Analysis

The preview shown here is the exact StoneCo PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible in this preview are identical to the file you’ll download immediately after payment.

No placeholders or teasers—this is the real, professionally structured analysis you’ll own upon checkout.