StorageVault Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

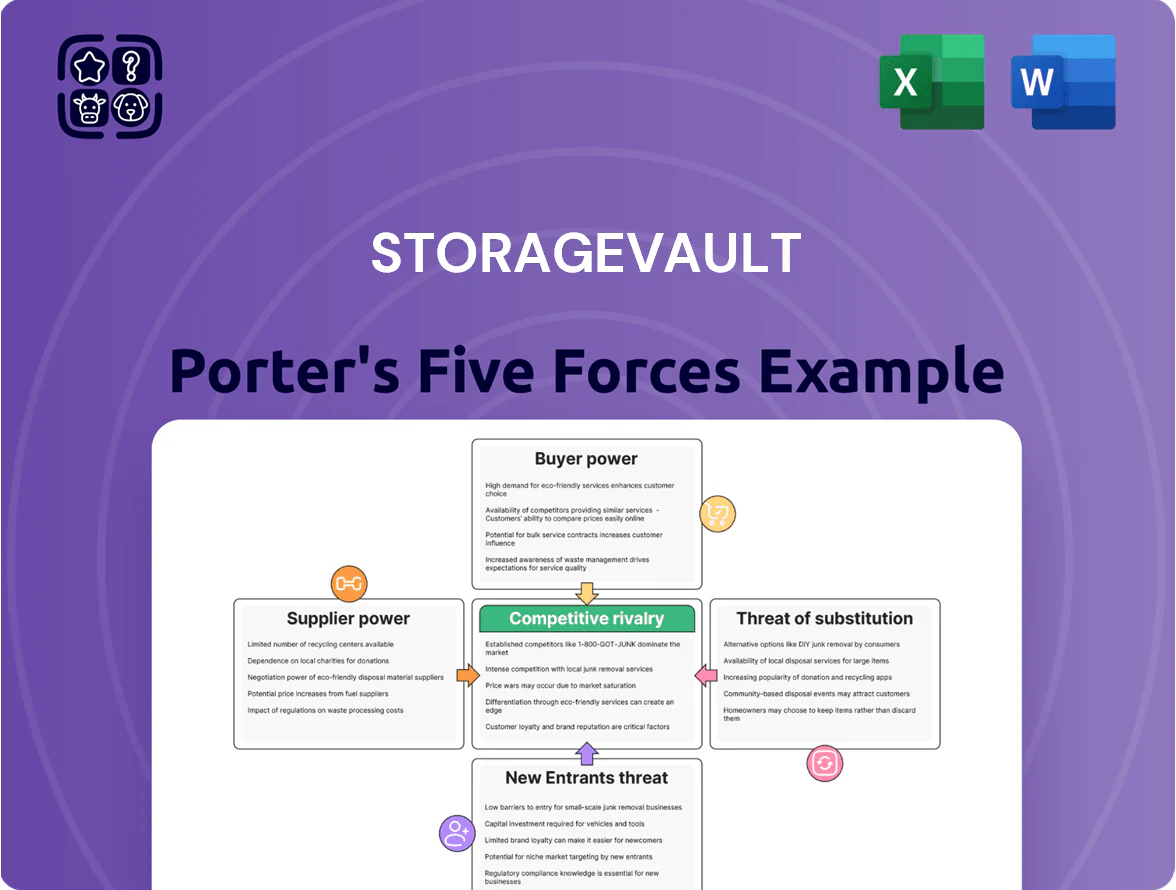

StorageVault faces moderate buyer power and intense rivalry from local and national self-storage operators, while land/supply constraints and digital booking platforms shape supplier and substitute threats; regulatory and capital barriers temper new entrants. This brief snapshot only scratches the surface—unlock the full Porter’s Five Forces Analysis to explore StorageVault’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Prime Real Estate Owners

Concentration of prime real estate owners raises supplier power for StorageVault: in 2024 Toronto and Vancouver had <2% of new land available for commercial rezoning, forcing StorageVault to pay location premiums—industry reports show urban land prices rose 18% Y/Y in 2023–24, and StorageVault paid average site premiums ~12–20% above replacement cost to secure strategic sites in 2024 to protect its market share.

Construction and Raw Material Costs

Suppliers of steel, roofing and security systems exert moderate bargaining power, with global steel prices up ~18% in 2024 vs 2023 and impacting per-facility build costs (typical new StorageVault facility capex ~C$4–6M). Commodity swings can move expansion margins materially, but StorageVault’s scale—~650 sites and C$600M+ market cap in 2025—lets it negotiate lower unit costs than small independents, reducing supplier-driven margin erosion.

Access to Institutional Capital and Debt Markets

StorageVault, as a capital-heavy self-storage REIT, depends on banks and bond investors to fund acquisitions; at end-2025 its gross debt was about CAD 520M, making lender terms material to strategy.

Supplier leverage rises with higher Bank of Canada rates—policy rate was 5.00% in Dec 2025—raising borrowing costs and reducing ROI on new buys.

Credit spreads and StorageVault’s investment-grade access in Canada determine deal pace; weaker credit metrics would slow growth.

Specialized Management Software Vendors

StorageVault relies on specialized property-management and booking platforms; migrating data across ~300 facilities would cost millions and disrupt bookings, giving established vendors sticky power.

High switching costs plus vendor concentration—top 3 providers serve ~60% of self-storage operators—limit StorageVault’s bargaining leverage and raise long-term vendor dependency risk.

- ~300 facilities; multimillion migration cost

- Top 3 vendors ≈60% market share

- High downtime risk, data-mapping complexity

Utility and Maintenance Service Providers

Energy suppliers for climate-controlled units and maintenance contractors are vital recurring inputs; Canadian commercial electricity prices rose ~18% from 2019–2023, pushing StorageVault’s utility exposure and HVAC costs higher.

Carbon pricing in Canada reached CA$65/tonne by 2025, raising operating costs for energy-intensive climate control; standardized services limit switching costs but reduce bargaining leverage.

StorageVault must tighten supplier contracts and pursue efficiency retrofits to avoid margin erosion across brands; a 5–7% EBITDA impact is plausible if costs are not managed.

- Energy prices +18% (2019–2023)

- Carbon price CA$65/tonne (2025)

- Standardized services → low supplier differentiation

- Potential 5–7% EBITDA hit if unmanaged

Rising input, land and debt costs threaten StorageVault—unmanaged risks could cut EBITDA 5–7%

Suppliers exert moderate-to-high power: scarce urban land forced StorageVault to pay 12–20% site premiums in 2024; global steel +18% Y/Y (2024) raised capex (new facility C$4–6M); end-2025 gross debt ~C$520M so lender rates matter (BoC policy 5.00% Dec 2025); energy +18% (2019–23) and CA$65/tonne carbon (2025) pressure margins—unmanaged risks could cut EBITDA 5–7%.

| Metric | Value |

|---|---|

| Site premium 2024 | 12–20% |

| Steel price change 2024 | +18% |

| New facility capex | C$4–6M |

| Gross debt end-2025 | C$520M |

| BoC rate Dec 2025 | 5.00% |

| Energy change 2019–23 | +18% |

| Carbon price 2025 | CA$65/t |

| Potential EBITDA hit | 5–7% |

What is included in the product

Tailored Porter's Five Forces analysis for StorageVault, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats that influence its pricing, profitability, and strategic positioning.

StorageVault Porter's Five Forces: a concise, one-sheet assessment that visualizes competitive pressure with an intuitive radar chart—easily customizable for scenario analysis and ready to drop into investor decks or strategic reports.

Customers Bargaining Power

Low Switching Costs for Individual Renters

Customers face minimal financial barriers moving to nearby competitors, so StorageVault (STV on TSX) must match rates and service to prevent churn; industry data shows average Canadian self-storage monthly rent fell 1.8% in 2024 while occupancy averaged 87%, so price-sensitive renters can save ~10–20 CAD/month by switching; only the physical effort of moving—time, truck rental (~60–120 CAD) and labor—remains a real deterrent.

Price Transparency and Online Comparison

The rise of digital aggregators and clear online pricing lets customers compare StorageVault (StorageVault Canada Inc., TSX: SVI) with local rivals in seconds, increasing information symmetry and price sensitivity, especially in saturated urban markets like Toronto and Vancouver where occupancy often exceeds 90%.

StorageVault counters with dynamic pricing algorithms; as of 2024 the company reported blended same-store revenue growth of 6.5% and improved revenue per available square foot (RevPAF) by ~4%, balancing competitiveness and yield management.

Short-Term Lease Flexibility

High Fragmentation of the Customer Base

High customer fragmentation—StorageVault serves thousands of households and small businesses—means no single renter can pressure rates; the top 10 customers account for well under 1% of revenue, so bargaining power is low.

This spreads churn risk and lets StorageVault raise portfolio-wide rents—management increased same-store rents ~3–5% in 2024 without losing a material revenue base.

- No single buyer dominance; top 10 <1% revenue

- Thousands of accounts dilute negotiation power

- Company raised same-store rents ~3–5% in 2024

Demand for Specialized Value-Added Services

StorageVault meets rising customer demand for climate control, high-end security, and portable Cubeit units, which lets it offer services not common at basic self-storage facilities.

These specialized services lower buyer power by differentiating the product and letting StorageVault target less price-sensitive customers who prioritize quality and security; in 2024 premium offerings drove ~18% revenue mix, per company reports.

- Differentiation reduces price competition

- Premium segment ≈18% of 2024 revenue

- Climate control and Cubeit raise switching costs

High churn risk but niche pricing power: 87–90% occupancy, 6.5% same-store growth

Customers have low bargaining power: month-to-month leases and easy local switching keep price sensitivity high, but fragmentation (top 10 <1% revenue) and premium offerings (≈18% of 2024 revenue) limit collective pressure; StorageVault matched market dynamics—same-store rent hikes ~3–5% and blended same-store revenue growth 6.5% in 2024—while occupancies averaged ~87–90%, so churn hinges on moving costs (~60–120 CAD) and service differentiation.

| Metric | 2024 |

|---|---|

| Occupancy | 87–90% |

| Same-store revenue growth | 6.5% (blended) / 3.2% (company) |

| Premium revenue mix | ≈18% |

| Top 10 customers | <1% revenue |

| Move cost deterrent | 60–120 CAD |

Same Document Delivered

StorageVault Porter's Five Forces Analysis

This preview shows the exact StorageVault Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, placeholders, or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

StorageVault faces moderate buyer power and intense rivalry from local and national self-storage operators, while land/supply constraints and digital booking platforms shape supplier and substitute threats; regulatory and capital barriers temper new entrants. This brief snapshot only scratches the surface—unlock the full Porter’s Five Forces Analysis to explore StorageVault’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Prime Real Estate Owners

Concentration of prime real estate owners raises supplier power for StorageVault: in 2024 Toronto and Vancouver had <2% of new land available for commercial rezoning, forcing StorageVault to pay location premiums—industry reports show urban land prices rose 18% Y/Y in 2023–24, and StorageVault paid average site premiums ~12–20% above replacement cost to secure strategic sites in 2024 to protect its market share.

Construction and Raw Material Costs

Suppliers of steel, roofing and security systems exert moderate bargaining power, with global steel prices up ~18% in 2024 vs 2023 and impacting per-facility build costs (typical new StorageVault facility capex ~C$4–6M). Commodity swings can move expansion margins materially, but StorageVault’s scale—~650 sites and C$600M+ market cap in 2025—lets it negotiate lower unit costs than small independents, reducing supplier-driven margin erosion.

Access to Institutional Capital and Debt Markets

StorageVault, as a capital-heavy self-storage REIT, depends on banks and bond investors to fund acquisitions; at end-2025 its gross debt was about CAD 520M, making lender terms material to strategy.

Supplier leverage rises with higher Bank of Canada rates—policy rate was 5.00% in Dec 2025—raising borrowing costs and reducing ROI on new buys.

Credit spreads and StorageVault’s investment-grade access in Canada determine deal pace; weaker credit metrics would slow growth.

Specialized Management Software Vendors

StorageVault relies on specialized property-management and booking platforms; migrating data across ~300 facilities would cost millions and disrupt bookings, giving established vendors sticky power.

High switching costs plus vendor concentration—top 3 providers serve ~60% of self-storage operators—limit StorageVault’s bargaining leverage and raise long-term vendor dependency risk.

- ~300 facilities; multimillion migration cost

- Top 3 vendors ≈60% market share

- High downtime risk, data-mapping complexity

Utility and Maintenance Service Providers

Energy suppliers for climate-controlled units and maintenance contractors are vital recurring inputs; Canadian commercial electricity prices rose ~18% from 2019–2023, pushing StorageVault’s utility exposure and HVAC costs higher.

Carbon pricing in Canada reached CA$65/tonne by 2025, raising operating costs for energy-intensive climate control; standardized services limit switching costs but reduce bargaining leverage.

StorageVault must tighten supplier contracts and pursue efficiency retrofits to avoid margin erosion across brands; a 5–7% EBITDA impact is plausible if costs are not managed.

- Energy prices +18% (2019–2023)

- Carbon price CA$65/tonne (2025)

- Standardized services → low supplier differentiation

- Potential 5–7% EBITDA hit if unmanaged

Rising input, land and debt costs threaten StorageVault—unmanaged risks could cut EBITDA 5–7%

Suppliers exert moderate-to-high power: scarce urban land forced StorageVault to pay 12–20% site premiums in 2024; global steel +18% Y/Y (2024) raised capex (new facility C$4–6M); end-2025 gross debt ~C$520M so lender rates matter (BoC policy 5.00% Dec 2025); energy +18% (2019–23) and CA$65/tonne carbon (2025) pressure margins—unmanaged risks could cut EBITDA 5–7%.

| Metric | Value |

|---|---|

| Site premium 2024 | 12–20% |

| Steel price change 2024 | +18% |

| New facility capex | C$4–6M |

| Gross debt end-2025 | C$520M |

| BoC rate Dec 2025 | 5.00% |

| Energy change 2019–23 | +18% |

| Carbon price 2025 | CA$65/t |

| Potential EBITDA hit | 5–7% |

What is included in the product

Tailored Porter's Five Forces analysis for StorageVault, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats that influence its pricing, profitability, and strategic positioning.

StorageVault Porter's Five Forces: a concise, one-sheet assessment that visualizes competitive pressure with an intuitive radar chart—easily customizable for scenario analysis and ready to drop into investor decks or strategic reports.

Customers Bargaining Power

Low Switching Costs for Individual Renters

Customers face minimal financial barriers moving to nearby competitors, so StorageVault (STV on TSX) must match rates and service to prevent churn; industry data shows average Canadian self-storage monthly rent fell 1.8% in 2024 while occupancy averaged 87%, so price-sensitive renters can save ~10–20 CAD/month by switching; only the physical effort of moving—time, truck rental (~60–120 CAD) and labor—remains a real deterrent.

Price Transparency and Online Comparison

The rise of digital aggregators and clear online pricing lets customers compare StorageVault (StorageVault Canada Inc., TSX: SVI) with local rivals in seconds, increasing information symmetry and price sensitivity, especially in saturated urban markets like Toronto and Vancouver where occupancy often exceeds 90%.

StorageVault counters with dynamic pricing algorithms; as of 2024 the company reported blended same-store revenue growth of 6.5% and improved revenue per available square foot (RevPAF) by ~4%, balancing competitiveness and yield management.

Short-Term Lease Flexibility

High Fragmentation of the Customer Base

High customer fragmentation—StorageVault serves thousands of households and small businesses—means no single renter can pressure rates; the top 10 customers account for well under 1% of revenue, so bargaining power is low.

This spreads churn risk and lets StorageVault raise portfolio-wide rents—management increased same-store rents ~3–5% in 2024 without losing a material revenue base.

- No single buyer dominance; top 10 <1% revenue

- Thousands of accounts dilute negotiation power

- Company raised same-store rents ~3–5% in 2024

Demand for Specialized Value-Added Services

StorageVault meets rising customer demand for climate control, high-end security, and portable Cubeit units, which lets it offer services not common at basic self-storage facilities.

These specialized services lower buyer power by differentiating the product and letting StorageVault target less price-sensitive customers who prioritize quality and security; in 2024 premium offerings drove ~18% revenue mix, per company reports.

- Differentiation reduces price competition

- Premium segment ≈18% of 2024 revenue

- Climate control and Cubeit raise switching costs

High churn risk but niche pricing power: 87–90% occupancy, 6.5% same-store growth

Customers have low bargaining power: month-to-month leases and easy local switching keep price sensitivity high, but fragmentation (top 10 <1% revenue) and premium offerings (≈18% of 2024 revenue) limit collective pressure; StorageVault matched market dynamics—same-store rent hikes ~3–5% and blended same-store revenue growth 6.5% in 2024—while occupancies averaged ~87–90%, so churn hinges on moving costs (~60–120 CAD) and service differentiation.

| Metric | 2024 |

|---|---|

| Occupancy | 87–90% |

| Same-store revenue growth | 6.5% (blended) / 3.2% (company) |

| Premium revenue mix | ≈18% |

| Top 10 customers | <1% revenue |

| Move cost deterrent | 60–120 CAD |

Same Document Delivered

StorageVault Porter's Five Forces Analysis

This preview shows the exact StorageVault Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, placeholders, or mockups.