StorageVault PESTLE Analysis

Skip the Research. Get the Strategy.

Explore how political shifts, economic cycles, and tech innovation are shaping StorageVault’s strategic path—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions; purchase the full, editable analysis for a complete, actionable breakdown you can use immediately.

Political factors

Federal and Provincial Taxation Policies

Changes in Canadian federal corporate tax (current general rate 15% federally plus provincial; combined averages ~25–27%) or capital gains inclusions (50% inclusion rate) would directly affect StorageVault’s net income and REIT-like distributions; a 1% effective tax change could swing after-tax income by millions given StorageVault’s 2024 revenue of CAD 221.8M.

Zoning and Land Use Regulations

Housing Affordability Initiatives

Government programs increasing housing density yield smaller units and boost self-storage demand; Canadian urban condo average unit size fell to about 716 sq ft in 2023, supporting StorageVault’s markets where occupancy rose to 94% in 2024. Political pressure to address the housing crisis via multi-family builds (Canada’s purpose-built rental completions up 12% in 2023) indirectly underpins StorageVault’s revenue growth. Policies promoting urbanization and high-density projects—Toronto CMA population up 1.3% in 2024—sustain steady off-site storage needs.

Inter-provincial Trade and Business Regulations

As StorageVault operates under multiple brands across provinces, it must navigate inter-provincial regulatory nuances affecting licensing, taxation and cross-border asset transfers; in 2024 Canada reported 11% growth in self-storage revenue to CAD 2.1 billion, amplifying regulatory exposure.

Differences in provincial labor laws and consumer protection acts force localized governance—varying minimum wages (e.g., Ontario CAD 16.55/hr, Alberta CAD 15.00/hr in 2025) and refund rules impact operating margins and staffing costs.

Stable federal and provincial governments through 2024–2025 support predictable long-term infrastructure investment, enabling StorageVault to pursue CAPEX projects (CAD 40–60M annually historical range) with lower policy risk.

- Must manage province-specific licensing, taxation and consumer rules

- Labor cost variance: Ontario CAD 16.55/hr vs Alberta CAD 15.00/hr (2025)

- 2024 industry revenue CAD 2.1B; CAPEX program ~CAD 40–60M/year

- Political stability through 2024–25 reduces regulatory uncertainty for long-term investments

Infrastructure Spending and Urban Development

Government infrastructure budgets—Canada’s federal Investing in Canada Plan allocates about CAD 180 billion through 2028—drive urban expansion and commercial corridors that raise local storage demand.

StorageVault targets assets near high-growth transit corridors; 2024 rent growth in Toronto CMA storage submarkets was ~4–6%, reflecting proximity premiums.

Tracking municipal transit-oriented development commitments helps forecast future hotspots for portable and fixed storage occupancy and pricing.

- Federal infrastructure CAD 180B to 2028

- Toronto CMA storage rent growth ~4–6% in 2024

- Assets near transit corridors show higher occupancy/pricing

- Monitor municipal TOD plans for future site selection

StorageVault: Tax, zoning & wage shifts tighten supply — 94% occupancy amid CAD221.8M revenue

Political stability and federal/provincial tax rules (combined rates ~25–27%; 50% CG inclusion) materially affect StorageVault’s after-tax income; 2024 revenue CAD 221.8M makes tax shifts impactful. Municipal permitting delays (3–12 months) and zoning changes (Toronto developable industrial land -8% in 2023) tighten supply, supporting 94% occupancy (2024). Provincial labor min wages (Ontario CAD16.55; Alberta CAD15.00 in 2025) and CAD180B federal infrastructure to 2028 shape operating costs and demand.

| Metric | Value |

|---|---|

| 2024 Revenue | CAD 221.8M |

| Industry Revenue 2024 | CAD 2.1B |

| Occupancy 2024 | 94% |

| Toronto zoning change 2023 | -8% developable industrial land |

| Permitting delays | 3–12 months |

| Ontario min wage 2025 | CAD 16.55/hr |

| Federal infra to 2028 | CAD 180B |

What is included in the product

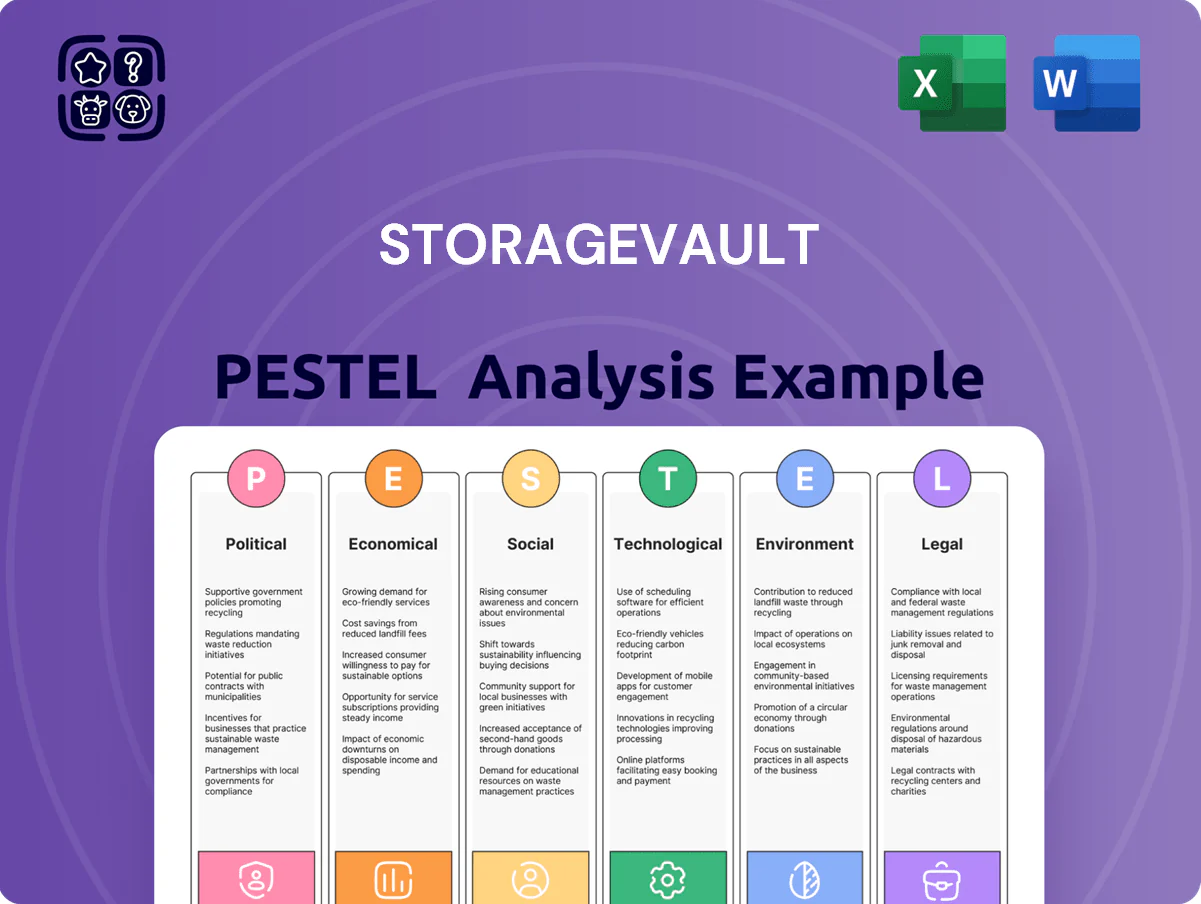

Explores how macro-environmental forces uniquely impact StorageVault across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and regional market dynamics to identify threats, opportunities, and scenario-driven strategic actions for executives, investors, and advisors.

Condenses StorageVault's full PESTLE into a clean, shareable brief that teams can drop into presentations or use in planning sessions to align on external risks and market positioning.

Economic factors

Interest Rate Environment and Cost of Capital

By end-2025 the Bank of Canada policy rate path is the key economic driver for StorageVault’s acquisition-heavy model: the BoC overnight rate rose to 5.00% in 2024 and futures implied a modest easing to ~4.25–4.75% by late 2025, directly impacting borrowing costs.

Elevated rates raise debt service and can compress cap rates, putting downward pressure on property valuations and narrowing acquisition spreads.

A stabilizing or declining rate outlook improves capacity to draw on the $300m+ revolving credit facilities and fund accretive transactions, lowering blended cost of capital and supporting NAV growth.

Inflationary Pressures on Operating Costs

Persistent inflation raised Canadian CPI to 3.4% in 2024, increasing labor, maintenance and utility costs across StorageVault’s ~470-property portfolio; short-term rental repricing helps, but a 200–300 bps spike in operating expenses could compress NOI margins. StorageVault reported adjusted NOI margin near 58% in FY2024, and investors watch management’s ability to preserve that level amid cost volatility.

Real Estate Market Dynamics

Canadian home sales fell 18% year-over-year in 2024 through Nov, lowering move-related storage churn, but 2024 resales still generated steady demand during renovations and downsizing; Statistics Canada reports average renovation spending rose 6% in 2023–24, supporting storage use. Economic slowdowns that trimmed housing activity coincided with a 12% rise in commercial sublease listings in 2024, boosting demand from businesses downsizing offices. Self-storage REITs outperformed office/retail in 2024, with industry occupancy averaging 92% versus 78% for offices, underscoring storage’s defensive profile.

Consumer Spending and Disposable Income

Economic cycles that erode household wealth reduce discretionary spending and can lower demand for storage of nonessential goods; during downturns self-storage often shifts from luxury items to essentials.

Self-storage remains needs-based, but a sharp drop in consumer confidence in Canada (consumer confidence indices fell ~9% in 2024 vs 2023) can cut luxury-item and secondary-unit rentals.

Rising Canadian household debt-to-income (DTI) — ~176% in 2024 — signals higher delinquency and move-out risk for StorageVault tenants.

- Economic downturns shift demand from discretionary to essential storage

- 2024 consumer confidence down ~9% year-over-year, hitting luxury demand

- Canadian household DTI ~176% in 2024 raises tenant credit risk

Business Activity and E-commerce Growth

StorageVault benefits from e-commerce growth: Canadian e-commerce sales rose 7.8% in 2024 to CAD 78.4 billion, bolstering demand for flexible last-mile and inventory storage among SMEs and retailers.

About 18% of StorageVault’s rentable area targets commercial clients; occupancy and average revenue per unit track small business health—SME GDP contribution was ~52% in 2023, impacting utilization.

Economic downturns or tightening consumer spending can reduce SME inventory needs, while continued online retail expansion supports higher long-term demand for decentralized warehousing.

- 2024 Canadian e-commerce: CAD 78.4B (+7.8%)

- StorageVault commercial-focused area: ~18% of rentable space

- SME share of GDP: ~52% (2023)

Higher BoC rates and inflation squeeze NOI amid rising tenant risk; e‑commerce lifts commercial demand

Higher BoC rates (5.00% in 2024; futures ~4.25–4.75% by late-2025) raise debt service and compress cap rates, while inflation (CPI 3.4% in 2024) lifts Opex and pressures NOI; consumer confidence fell ~9% YoY (2024) and household DTI ~176% increase tenant risk, offset by e-commerce growth (CAD78.4B, +7.8% in 2024) supporting commercial demand (~18% rentable area).

| Metric | 2024/Latest |

|---|---|

| BoC policy rate | 5.00% |

| CPI | 3.4% |

| Consumer confidence | -9% YoY |

| Household DTI | ~176% |

| Canadian e-commerce | CAD78.4B (+7.8%) |

| StorageVault commercial area | ~18% |

What You See Is What You Get

StorageVault PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the StorageVault PESTLE Analysis content, structure, and layout are identical to the downloadable file, with no placeholders or teasers, so you can review political, economic, social, technological, legal, and environmental factors immediately upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Explore how political shifts, economic cycles, and tech innovation are shaping StorageVault’s strategic path—our concise PESTLE highlights key external risks and opportunities to inform smarter decisions; purchase the full, editable analysis for a complete, actionable breakdown you can use immediately.

Political factors

Federal and Provincial Taxation Policies

Changes in Canadian federal corporate tax (current general rate 15% federally plus provincial; combined averages ~25–27%) or capital gains inclusions (50% inclusion rate) would directly affect StorageVault’s net income and REIT-like distributions; a 1% effective tax change could swing after-tax income by millions given StorageVault’s 2024 revenue of CAD 221.8M.

Zoning and Land Use Regulations

Housing Affordability Initiatives

Government programs increasing housing density yield smaller units and boost self-storage demand; Canadian urban condo average unit size fell to about 716 sq ft in 2023, supporting StorageVault’s markets where occupancy rose to 94% in 2024. Political pressure to address the housing crisis via multi-family builds (Canada’s purpose-built rental completions up 12% in 2023) indirectly underpins StorageVault’s revenue growth. Policies promoting urbanization and high-density projects—Toronto CMA population up 1.3% in 2024—sustain steady off-site storage needs.

Inter-provincial Trade and Business Regulations

As StorageVault operates under multiple brands across provinces, it must navigate inter-provincial regulatory nuances affecting licensing, taxation and cross-border asset transfers; in 2024 Canada reported 11% growth in self-storage revenue to CAD 2.1 billion, amplifying regulatory exposure.

Differences in provincial labor laws and consumer protection acts force localized governance—varying minimum wages (e.g., Ontario CAD 16.55/hr, Alberta CAD 15.00/hr in 2025) and refund rules impact operating margins and staffing costs.

Stable federal and provincial governments through 2024–2025 support predictable long-term infrastructure investment, enabling StorageVault to pursue CAPEX projects (CAD 40–60M annually historical range) with lower policy risk.

- Must manage province-specific licensing, taxation and consumer rules

- Labor cost variance: Ontario CAD 16.55/hr vs Alberta CAD 15.00/hr (2025)

- 2024 industry revenue CAD 2.1B; CAPEX program ~CAD 40–60M/year

- Political stability through 2024–25 reduces regulatory uncertainty for long-term investments

Infrastructure Spending and Urban Development

Government infrastructure budgets—Canada’s federal Investing in Canada Plan allocates about CAD 180 billion through 2028—drive urban expansion and commercial corridors that raise local storage demand.

StorageVault targets assets near high-growth transit corridors; 2024 rent growth in Toronto CMA storage submarkets was ~4–6%, reflecting proximity premiums.

Tracking municipal transit-oriented development commitments helps forecast future hotspots for portable and fixed storage occupancy and pricing.

- Federal infrastructure CAD 180B to 2028

- Toronto CMA storage rent growth ~4–6% in 2024

- Assets near transit corridors show higher occupancy/pricing

- Monitor municipal TOD plans for future site selection

StorageVault: Tax, zoning & wage shifts tighten supply — 94% occupancy amid CAD221.8M revenue

Political stability and federal/provincial tax rules (combined rates ~25–27%; 50% CG inclusion) materially affect StorageVault’s after-tax income; 2024 revenue CAD 221.8M makes tax shifts impactful. Municipal permitting delays (3–12 months) and zoning changes (Toronto developable industrial land -8% in 2023) tighten supply, supporting 94% occupancy (2024). Provincial labor min wages (Ontario CAD16.55; Alberta CAD15.00 in 2025) and CAD180B federal infrastructure to 2028 shape operating costs and demand.

| Metric | Value |

|---|---|

| 2024 Revenue | CAD 221.8M |

| Industry Revenue 2024 | CAD 2.1B |

| Occupancy 2024 | 94% |

| Toronto zoning change 2023 | -8% developable industrial land |

| Permitting delays | 3–12 months |

| Ontario min wage 2025 | CAD 16.55/hr |

| Federal infra to 2028 | CAD 180B |

What is included in the product

Explores how macro-environmental forces uniquely impact StorageVault across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and regional market dynamics to identify threats, opportunities, and scenario-driven strategic actions for executives, investors, and advisors.

Condenses StorageVault's full PESTLE into a clean, shareable brief that teams can drop into presentations or use in planning sessions to align on external risks and market positioning.

Economic factors

Interest Rate Environment and Cost of Capital

By end-2025 the Bank of Canada policy rate path is the key economic driver for StorageVault’s acquisition-heavy model: the BoC overnight rate rose to 5.00% in 2024 and futures implied a modest easing to ~4.25–4.75% by late 2025, directly impacting borrowing costs.

Elevated rates raise debt service and can compress cap rates, putting downward pressure on property valuations and narrowing acquisition spreads.

A stabilizing or declining rate outlook improves capacity to draw on the $300m+ revolving credit facilities and fund accretive transactions, lowering blended cost of capital and supporting NAV growth.

Inflationary Pressures on Operating Costs

Persistent inflation raised Canadian CPI to 3.4% in 2024, increasing labor, maintenance and utility costs across StorageVault’s ~470-property portfolio; short-term rental repricing helps, but a 200–300 bps spike in operating expenses could compress NOI margins. StorageVault reported adjusted NOI margin near 58% in FY2024, and investors watch management’s ability to preserve that level amid cost volatility.

Real Estate Market Dynamics

Canadian home sales fell 18% year-over-year in 2024 through Nov, lowering move-related storage churn, but 2024 resales still generated steady demand during renovations and downsizing; Statistics Canada reports average renovation spending rose 6% in 2023–24, supporting storage use. Economic slowdowns that trimmed housing activity coincided with a 12% rise in commercial sublease listings in 2024, boosting demand from businesses downsizing offices. Self-storage REITs outperformed office/retail in 2024, with industry occupancy averaging 92% versus 78% for offices, underscoring storage’s defensive profile.

Consumer Spending and Disposable Income

Economic cycles that erode household wealth reduce discretionary spending and can lower demand for storage of nonessential goods; during downturns self-storage often shifts from luxury items to essentials.

Self-storage remains needs-based, but a sharp drop in consumer confidence in Canada (consumer confidence indices fell ~9% in 2024 vs 2023) can cut luxury-item and secondary-unit rentals.

Rising Canadian household debt-to-income (DTI) — ~176% in 2024 — signals higher delinquency and move-out risk for StorageVault tenants.

- Economic downturns shift demand from discretionary to essential storage

- 2024 consumer confidence down ~9% year-over-year, hitting luxury demand

- Canadian household DTI ~176% in 2024 raises tenant credit risk

Business Activity and E-commerce Growth

StorageVault benefits from e-commerce growth: Canadian e-commerce sales rose 7.8% in 2024 to CAD 78.4 billion, bolstering demand for flexible last-mile and inventory storage among SMEs and retailers.

About 18% of StorageVault’s rentable area targets commercial clients; occupancy and average revenue per unit track small business health—SME GDP contribution was ~52% in 2023, impacting utilization.

Economic downturns or tightening consumer spending can reduce SME inventory needs, while continued online retail expansion supports higher long-term demand for decentralized warehousing.

- 2024 Canadian e-commerce: CAD 78.4B (+7.8%)

- StorageVault commercial-focused area: ~18% of rentable space

- SME share of GDP: ~52% (2023)

Higher BoC rates and inflation squeeze NOI amid rising tenant risk; e‑commerce lifts commercial demand

Higher BoC rates (5.00% in 2024; futures ~4.25–4.75% by late-2025) raise debt service and compress cap rates, while inflation (CPI 3.4% in 2024) lifts Opex and pressures NOI; consumer confidence fell ~9% YoY (2024) and household DTI ~176% increase tenant risk, offset by e-commerce growth (CAD78.4B, +7.8% in 2024) supporting commercial demand (~18% rentable area).

| Metric | 2024/Latest |

|---|---|

| BoC policy rate | 5.00% |

| CPI | 3.4% |

| Consumer confidence | -9% YoY |

| Household DTI | ~176% |

| Canadian e-commerce | CAD78.4B (+7.8%) |

| StorageVault commercial area | ~18% |

What You See Is What You Get

StorageVault PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the StorageVault PESTLE Analysis content, structure, and layout are identical to the downloadable file, with no placeholders or teasers, so you can review political, economic, social, technological, legal, and environmental factors immediately upon checkout.