Straumann Holding Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

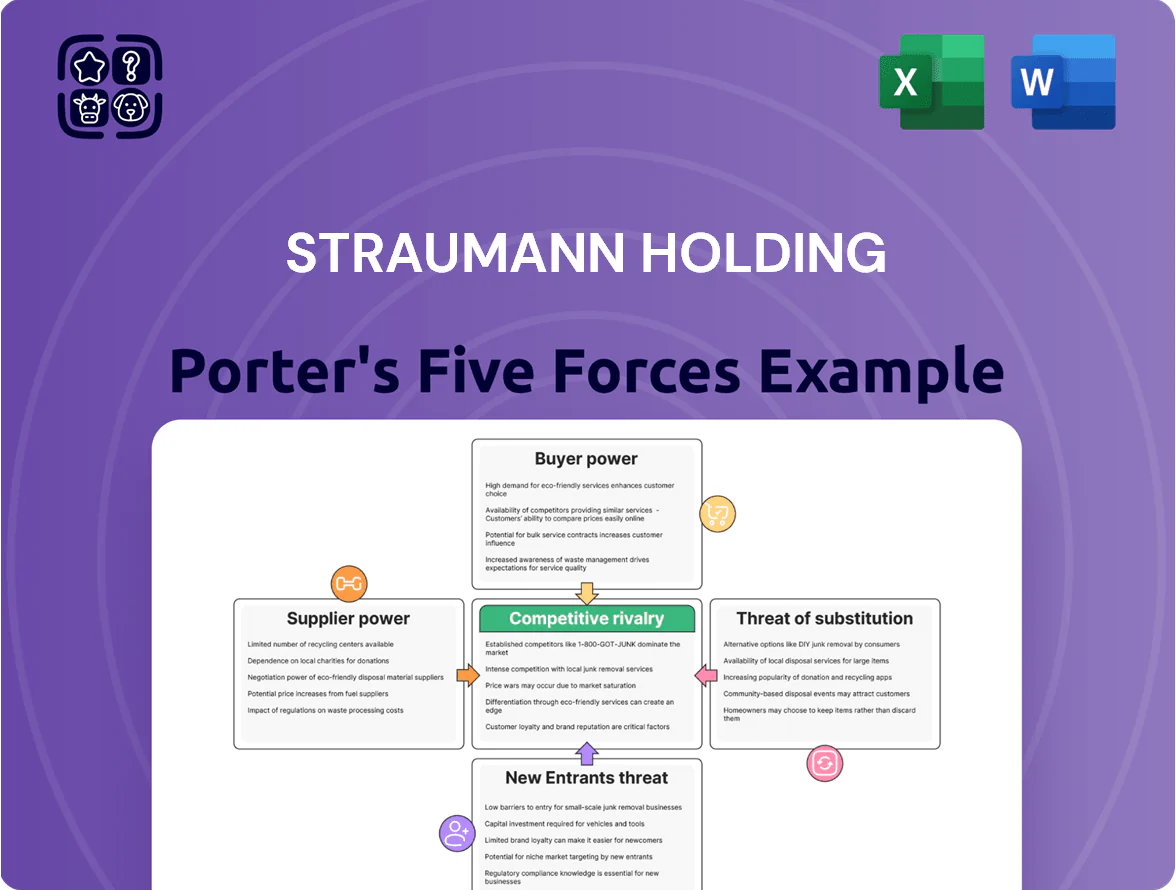

Straumann Holding operates in a high-tech, consolidated dental implant market where strong supplier relationships, differentiated products, and regulatory barriers limit new entrants but intensify rivalry among incumbents and accelerate innovation.

Suppliers Bargaining Power

Specialized Raw Material Requirements

Straumann’s implants need medical-grade titanium and zirconia; global certified suppliers number fewer than 30 due to strict MDR/ISO 13485 rules, giving suppliers moderate leverage. Straumann held €1.7bn inventory turnover in 2024 and uses multi-year contracts and qualified audits to secure supply and quality. Short supplier pool raises switching costs and price sensitivity, but Straumann’s scale and long-term ties limit supplier price power.

Precision Manufacturing Equipment

Straumann depends on a small set of high-precision milling and dental 3D-printing vendors, creating supplier power; in 2024 Straumann capital expenditures on production equipment were CHF 163m, signaling heavy reliance on specialist kit.

Strategic Software Integrations

As Straumann integrates third-party scanning and planning software, suppliers of proprietary design tools and AI hold meaningful leverage because switching or re-certifying integrations can cost millions and months of R&D; in 2024 Straumann reported digital sales growth of ~14% and >€300m invested in digital initiatives, so supplier dependence forces Straumann into collaborative contracts, joint roadmaps, revenue-sharing deals, and API standardization to keep its ecosystem seamless and reduce downtime risk.

Energy and Logistics Costs

Energy and logistics cost swings directly affect Straumann’s global manufacturing: a 2024 IEA-style rise in industrial electricity prices of about 8–12% in Europe and a 15% jump in global airfreight rates in 2022–24 increased production overheads for medical components.

Temperature-controlled logistics providers tightened capacity by 2025, raising spot rates ~10–18%, boosting supplier power; Straumann’s scale and long-term contracts reduce exposure but cannot fully offset pass-through cost pressure on gross margins.

- Industrial power +8–12% (Europe, 2024)

- Airfreight +15% (2022–24)

- Temp-controlled rate rise 10–18% (through 2025)

- Scale/long-term contracts partially mitigate margin impact

Labor Market for Specialized Talent

The global pool of specialized MedTech engineers and materials scientists is tight; in 2024 demand grew ~6% while supply rose ~1–2%, pressuring salaries and slowing R&D throughput.

Competition from implants and diagnostics firms raises recruitment costs; Straumann’s 2024 R&D spend was CHF 174m, so talent scarcity directly limits pace of product innovation.

Retaining this human capital is vital for Straumann’s premium implant margin and time-to-market in a segment where clinical differentiation matters.

- 2024 R&D spend CHF 174m

- MedTech skilled labor demand +6% (2024)

- Supply growth ~1–2% (2024)

- Talent shortage slows innovation and raises hiring costs

Supplier power tight despite Straumann scale—capex/R&D cushion; talent and logistics squeeze

Suppliers have moderate-to-high leverage: <€30 certified titanium/zirconia vendors, specialist milling/3D-printing providers, proprietary software and temp-logistics concentrate price/power despite Straumann’s scale, multi-year contracts, CHF 163m capex (2024) and CHF 174m R&D (2024) which partly mitigate risk; talent scarcity (+6% demand vs 1–2% supply, 2024) raises costs and slows innovation.

| Metric | 2024/24–25 |

|---|---|

| Certified material suppliers | <30 |

| Capex (production) | CHF 163m (2024) |

| R&D spend | CHF 174m (2024) |

| Airfreight rise | +15% (2022–24) |

| Industrial power (EU) | +8–12% (2024) |

| Temp-logistics spot rates | +10–18% (through 2025) |

| MedTech talent demand vs supply | +6% vs 1–2% (2024) |

What is included in the product

Tailored Porter's Five Forces assessment for Straumann Holding that highlights competitive rivalry, supplier and buyer bargaining power, threats from new entrants and substitutes, and identifies disruptive forces and strategic defenses shaping its market position.

Compact Porter's Five Forces snapshot for Straumann—quickly pinpoint competitive pressures and relief strategies to guide product, pricing, and M&A decisions.

Customers Bargaining Power

Consolidation of Dental Service Organizations

The rise of large Dental Service Organizations (DSOs) like Smile Brands and Heartland Dental—which together managed over 10,000 clinics in the US by 2024—shifts bargaining power away from solo dentists to corporate buyers; DSOs buy implants and restorative products in high volumes and demand double-digit discounts and uniform pricing across networks. Straumann must bundle implants, digital workflows, training, and service-level agreements to secure preferred-provider deals and protect margins; in 2024 Straumann reported 6% revenue exposure to DSO contracts, a figure likely to grow.

High Switching Costs for Practitioners

Dentists invest sizable sums—often $20k–$100k per clinic—for Straumann-compatible surgical kits, CAD/CAM scanners, and training; retraining and retooling can cost months of revenue and thousands per practitioner. A 2024 Straumann report shows >60% of implant procedures use their platforms in key markets, creating technical lock-in that lowers individual practitioners’ bargaining power.

Sensitivity to Patient Economic Conditions

Access to Clinical Data and Education

Customers increasingly select Straumann for its clinical evidence and training: Straumann published 150+ peer-reviewed studies in 2024 and trained over 20,000 clinicians through its education arm, boosting perceived clinical certainty.

This reliance on Straumann’s scientific backing and hands-on programs raises switching costs, so clinics rarely shift to lower-cost, less-proven brands despite price pressure.

The value-added service model constrains customer bargaining power because outcomes and training reduce the weight of price in purchasing decisions.

- 150+ peer-reviewed studies (2024)

- 20,000+ clinicians trained (2024)

- Higher switching cost limits price-driven churn

Increasing Demand for Integrated Solutions

Straumann’s push into integrated solutions — implants, intraoral scanners, and clear aligners — strengthens customer retention by offering a single digital workflow; in 2024 Straumann’s clear aligner segment grew ~25% YoY, and its digital solutions now account for ~18% of group sales, making it easier for clinics to stay within one brand family and reducing component cherry-picking.

Straumann's CHF1.87bn 2024: Clinical lock‑in, digital growth and DSO price pressure

Large DSOs (10,000+ US clinics by 2024) and price-sensitive patients push Straumann to bundle products, offer discounts and financing; 2024 revenue CHF 1.87bn with ~6% DSO exposure. Clinical lock-in (150+ peer-reviewed studies; 20,000+ clinicians trained in 2024) and integrated digital solutions (digital = ~18% sales; aligners +25% YoY) raise switching costs and limit pure price-driven churn.

| Metric | 2024 |

|---|---|

| Group revenue | CHF 1.87bn |

| DSO exposure | 6% |

| Peer-reviewed studies | 150+ |

| Clinicians trained | 20,000+ |

| Digital sales | ~18% |

| Aligner growth | ~25% YoY |

Full Version Awaits

Straumann Holding Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Straumann Holding you'll receive—no placeholders, no mockups—fully formatted and ready for download immediately after purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Straumann Holding operates in a high-tech, consolidated dental implant market where strong supplier relationships, differentiated products, and regulatory barriers limit new entrants but intensify rivalry among incumbents and accelerate innovation.

Suppliers Bargaining Power

Specialized Raw Material Requirements

Straumann’s implants need medical-grade titanium and zirconia; global certified suppliers number fewer than 30 due to strict MDR/ISO 13485 rules, giving suppliers moderate leverage. Straumann held €1.7bn inventory turnover in 2024 and uses multi-year contracts and qualified audits to secure supply and quality. Short supplier pool raises switching costs and price sensitivity, but Straumann’s scale and long-term ties limit supplier price power.

Precision Manufacturing Equipment

Straumann depends on a small set of high-precision milling and dental 3D-printing vendors, creating supplier power; in 2024 Straumann capital expenditures on production equipment were CHF 163m, signaling heavy reliance on specialist kit.

Strategic Software Integrations

As Straumann integrates third-party scanning and planning software, suppliers of proprietary design tools and AI hold meaningful leverage because switching or re-certifying integrations can cost millions and months of R&D; in 2024 Straumann reported digital sales growth of ~14% and >€300m invested in digital initiatives, so supplier dependence forces Straumann into collaborative contracts, joint roadmaps, revenue-sharing deals, and API standardization to keep its ecosystem seamless and reduce downtime risk.

Energy and Logistics Costs

Energy and logistics cost swings directly affect Straumann’s global manufacturing: a 2024 IEA-style rise in industrial electricity prices of about 8–12% in Europe and a 15% jump in global airfreight rates in 2022–24 increased production overheads for medical components.

Temperature-controlled logistics providers tightened capacity by 2025, raising spot rates ~10–18%, boosting supplier power; Straumann’s scale and long-term contracts reduce exposure but cannot fully offset pass-through cost pressure on gross margins.

- Industrial power +8–12% (Europe, 2024)

- Airfreight +15% (2022–24)

- Temp-controlled rate rise 10–18% (through 2025)

- Scale/long-term contracts partially mitigate margin impact

Labor Market for Specialized Talent

The global pool of specialized MedTech engineers and materials scientists is tight; in 2024 demand grew ~6% while supply rose ~1–2%, pressuring salaries and slowing R&D throughput.

Competition from implants and diagnostics firms raises recruitment costs; Straumann’s 2024 R&D spend was CHF 174m, so talent scarcity directly limits pace of product innovation.

Retaining this human capital is vital for Straumann’s premium implant margin and time-to-market in a segment where clinical differentiation matters.

- 2024 R&D spend CHF 174m

- MedTech skilled labor demand +6% (2024)

- Supply growth ~1–2% (2024)

- Talent shortage slows innovation and raises hiring costs

Supplier power tight despite Straumann scale—capex/R&D cushion; talent and logistics squeeze

Suppliers have moderate-to-high leverage: <€30 certified titanium/zirconia vendors, specialist milling/3D-printing providers, proprietary software and temp-logistics concentrate price/power despite Straumann’s scale, multi-year contracts, CHF 163m capex (2024) and CHF 174m R&D (2024) which partly mitigate risk; talent scarcity (+6% demand vs 1–2% supply, 2024) raises costs and slows innovation.

| Metric | 2024/24–25 |

|---|---|

| Certified material suppliers | <30 |

| Capex (production) | CHF 163m (2024) |

| R&D spend | CHF 174m (2024) |

| Airfreight rise | +15% (2022–24) |

| Industrial power (EU) | +8–12% (2024) |

| Temp-logistics spot rates | +10–18% (through 2025) |

| MedTech talent demand vs supply | +6% vs 1–2% (2024) |

What is included in the product

Tailored Porter's Five Forces assessment for Straumann Holding that highlights competitive rivalry, supplier and buyer bargaining power, threats from new entrants and substitutes, and identifies disruptive forces and strategic defenses shaping its market position.

Compact Porter's Five Forces snapshot for Straumann—quickly pinpoint competitive pressures and relief strategies to guide product, pricing, and M&A decisions.

Customers Bargaining Power

Consolidation of Dental Service Organizations

The rise of large Dental Service Organizations (DSOs) like Smile Brands and Heartland Dental—which together managed over 10,000 clinics in the US by 2024—shifts bargaining power away from solo dentists to corporate buyers; DSOs buy implants and restorative products in high volumes and demand double-digit discounts and uniform pricing across networks. Straumann must bundle implants, digital workflows, training, and service-level agreements to secure preferred-provider deals and protect margins; in 2024 Straumann reported 6% revenue exposure to DSO contracts, a figure likely to grow.

High Switching Costs for Practitioners

Dentists invest sizable sums—often $20k–$100k per clinic—for Straumann-compatible surgical kits, CAD/CAM scanners, and training; retraining and retooling can cost months of revenue and thousands per practitioner. A 2024 Straumann report shows >60% of implant procedures use their platforms in key markets, creating technical lock-in that lowers individual practitioners’ bargaining power.

Sensitivity to Patient Economic Conditions

Access to Clinical Data and Education

Customers increasingly select Straumann for its clinical evidence and training: Straumann published 150+ peer-reviewed studies in 2024 and trained over 20,000 clinicians through its education arm, boosting perceived clinical certainty.

This reliance on Straumann’s scientific backing and hands-on programs raises switching costs, so clinics rarely shift to lower-cost, less-proven brands despite price pressure.

The value-added service model constrains customer bargaining power because outcomes and training reduce the weight of price in purchasing decisions.

- 150+ peer-reviewed studies (2024)

- 20,000+ clinicians trained (2024)

- Higher switching cost limits price-driven churn

Increasing Demand for Integrated Solutions

Straumann’s push into integrated solutions — implants, intraoral scanners, and clear aligners — strengthens customer retention by offering a single digital workflow; in 2024 Straumann’s clear aligner segment grew ~25% YoY, and its digital solutions now account for ~18% of group sales, making it easier for clinics to stay within one brand family and reducing component cherry-picking.

Straumann's CHF1.87bn 2024: Clinical lock‑in, digital growth and DSO price pressure

Large DSOs (10,000+ US clinics by 2024) and price-sensitive patients push Straumann to bundle products, offer discounts and financing; 2024 revenue CHF 1.87bn with ~6% DSO exposure. Clinical lock-in (150+ peer-reviewed studies; 20,000+ clinicians trained in 2024) and integrated digital solutions (digital = ~18% sales; aligners +25% YoY) raise switching costs and limit pure price-driven churn.

| Metric | 2024 |

|---|---|

| Group revenue | CHF 1.87bn |

| DSO exposure | 6% |

| Peer-reviewed studies | 150+ |

| Clinicians trained | 20,000+ |

| Digital sales | ~18% |

| Aligner growth | ~25% YoY |

Full Version Awaits

Straumann Holding Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Straumann Holding you'll receive—no placeholders, no mockups—fully formatted and ready for download immediately after purchase.