Stride Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

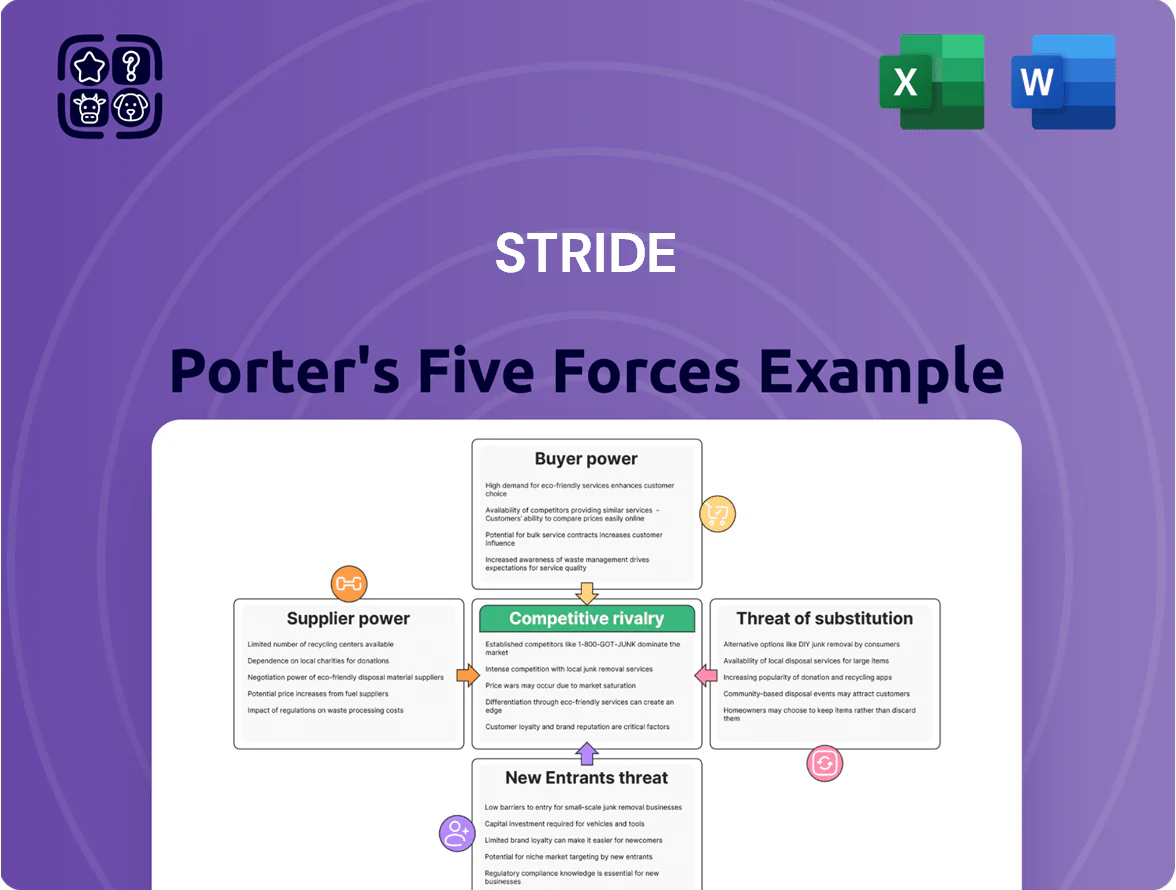

Stride’s Five Forces snapshot highlights key pressures—buyer sensitivity, supplier leverage, entrant threats, substitutes, and competitor rivalry—shaping its market position and margins.

This brief overview teases strategic vulnerabilities and strengths; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Cloud Infrastructure and Hosting Providers

Stride depends on third-party cloud hosts for its LMS and student records; switching providers is technically hard and costly, giving suppliers strong leverage—major hyperscalers control ~70% of global cloud IaaS/SaaS market as of 2024, raising price risk for Stride.

Educational Content and Intellectual Property Owners

Suppliers of specialized curriculum and digital content hold meaningful leverage over Stride due to unique IP and niche textbooks, enabling price and licensing terms that pressure margins; in 2024 Stride reported content licensing costs at roughly 7–9% of revenue, so negotiating power matters. Stride is expanding in-house content—investing about $25–35 million annually in curriculum development in 2023–24—to cut dependency and improve gross margins.

Qualified Teaching and Administrative Personnel

The supply of certified teachers able to work virtually is critical; in 2024 about 45% of US school districts reported teacher shortages, raising supplier leverage on pay and flexibility (Bureau of Labor Statistics, 2024).

Ongoing shortages push bargaining power up, so Stride must offer competitive pay—Stride reported 2023 operating expenses of $160M for instruction-related costs—and flexible schedules to retain staff.

Investing in robust LMS and synchronous tools cuts switching costs for teachers; studies show tech-enabled employers reduce turnover by ~15% within a year.

Hardware and Device Manufacturers

Stride supplies laptops and peripherals to many students to ensure access, buying at scale but remaining price-takers versus global electronics makers like Foxconn and distributors such as Ingram; in 2024 electronics price volatility rose ~6% YoY, raising procurement costs.

The company faces supply-chain risks (chip shortages, shipping delays) that in 2023 caused component lead times to average 18 weeks, and volume discounts (estimated 3–7% on bulk orders) only partially offset price swings.

- Provides student devices to ensure equity

- Electronics prices +6% YoY in 2024

- Component lead times ~18 weeks (2023)

- Volume discounts ~3–7%, still price-taker

Specialized Software and LMS Developers

Specialized proctoring, accessibility, and niche LMS tools often come from external firms, giving suppliers leverage when integrations are deep and switching costs high; industry data shows edtech acquisition multiples near 6–8x ARR in 2024, signaling strong supplier valuations.

Stride counters this by keeping a 150+ person internal IT and product team (2024 annual report) to build custom features, reducing dependency and preserving control over core UX and data flows.

- High supplier power when tech is deeply embedded

- Edtech firms valued ~6–8x ARR (2024)

- Stride has 150+ IT/product staff (2024)

- In-house devs lower switching and control risk

Suppliers wield strong leverage; Stride offsets risk with $25–35M content spend & 150+ IT

Suppliers exert medium–high power: hyperscalers control ~70% cloud IaaS/SaaS (2024), content licensing ~7–9% revenue (2024), teacher shortages ~45% of districts (2024) push pay, and electronics +6% YoY (2024) with 18-week lead times (2023). Stride reduces risk via $25–35M/yr content investment and 150+ IT staff (2024).

| Metric | Value |

|---|---|

| Cloud market share | ~70% (2024) |

| Content cost | 7–9% rev (2024) |

| Teacher shortages | 45% districts (2024) |

| Electronics price change | +6% YoY (2024) |

| Content spend | $25–35M/yr (2023–24) |

| IT staff | 150+ (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Stride, with detailed force-by-force analysis highlighting suppliers, buyers, substitutes, new entrants, and rivalry to inform strategic decisions and investor materials.

Concise five-forces snapshot that highlights competitive pain points and relief strategies—perfect for quick strategic decisions or pitching mitigation plans.

Customers Bargaining Power

Public School Districts and Government Agencies

Large public districts like NYC DOE (over 1.1M students) and Los Angeles USD (≈600k) hold outsized bargaining power, using volume to secure multi-year contracts and price concessions.

They demand custom curricula, LMS integration, and strict SLAs during RFPs; districts often require ROI metrics and 3rd-party efficacy studies.

Stride must show consistent outcomes—state test score gains, graduation rates—and full Title I/IDEA compliance to retain contracts worth tens of millions annually.

Individual Families and Student Choice

In direct-to-consumer and charter segments, parents can easily switch to competitors or traditional schools, raising Stride’s churn risk; U.S. K–12 online enrollment fell 2.1% in 2024, showing volatility.

Low switching costs mean Stride must sustain high satisfaction and engagement; Stride reported 2024 average daily attendance of 85% in its virtual schools, a key retention metric.

Marketing and reputation matter: Stride spent $62.4M on sales and marketing in FY2024 to defend share in a crowded market of dozens of statewide providers.

Corporate and Adult Education Clients

As Stride expands into career readiness and adult learning, corporate clients wield strong bargaining power, pushing for curriculum tailored to precise, measurable skills and outcomes; 2024 BLS data shows 54% of employers prioritize reskilling, raising demands for employer-aligned programs.

Switching Costs for Institutional Partners

For institutional partners, migrating an entire student body and faculty imposes high operational and training costs, creating stickiness that lowers customers' bargaining power mid-contract; districts face IT, data-mapping, and training expenses often exceeding 6-12 months of staff time per rollout (example: typical district SaaS migrations cost $150–400k in first-year implementation in 2024). Still, at renewal points the risk of non-renewal gives districts leverage to demand price cuts or expanded services, and approximately 18–25% of district contracts were renegotiated for better terms in 2023.

- High migration cost: $150–400k typical first-year implementation

- Rollout time: 6–12 months of staff effort

- Mid-contract: reduced bargaining power due to operational stickiness

- At renewal: 18–25% of contracts renegotiated in 2023

Availability of Performance Data and Alternatives

The widespread availability of school performance ratings and student outcome data lets parents and districts make highly informed choices, and in 2024 more than 90% of U.S. districts reported using state or third-party data in vendor selection.

Parents can directly compare Stride’s test scores and graduation metrics to competitors and local virtual programs, pressuring Stride to match peer-average proficiency gains (about 2–4 percentile points annually) or offer lower pricing.

This transparency forces simultaneous competition on quality and price; Stride’s 2024 revenue mix ($1.3B K‑12 services) and reported retention rates (≈78%) show stakeholders demand clear outcomes to justify spend.

- 90%+ districts use performance data (2024)

- Average peer proficiency gain: 2–4 percentile pts/yr

- Stride 2024 K‑12 revenue: $1.3 billion

- Stride retention rate ~78% (2024)

Stride under pressure: big-district leverage, slipping enrollment, retention & ROI tests

Large districts (NYC DOE 1.1M, LAUSD ≈600k) wield strong bargaining power via volume, custom RFPs, and renewal leverage; 18–25% of district contracts were renegotiated in 2023. Parents/charters increase churn risk with low switching costs; K–12 online enrollment fell 2.1% in 2024 and Stride retention ≈78% (2024). Stride spent $62.4M on sales/marketing (FY2024) and must show test-score gains (peer gain 2–4 pts/yr) and compliance to keep multi-million contracts.

| Metric | 2023–2024 |

|---|---|

| NYC DOE enrollment | 1.1M |

| LAUSD enrollment | ≈600k |

| K–12 online enrollment change | -2.1% (2024) |

| Stride K–12 revenue | $1.3B (2024) |

| Stride retention | ≈78% (2024) |

| Sales & marketing | $62.4M (FY2024) |

| Contract renegotiation rate | 18–25% (2023) |

| Peer proficiency gain | 2–4 percentile pts/yr |

Full Version Awaits

Stride Porter's Five Forces Analysis

This preview shows the exact Stride Porter's Five Forces analysis you'll receive—no samples or placeholders—fully formatted and ready for immediate download after purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Stride’s Five Forces snapshot highlights key pressures—buyer sensitivity, supplier leverage, entrant threats, substitutes, and competitor rivalry—shaping its market position and margins.

This brief overview teases strategic vulnerabilities and strengths; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Cloud Infrastructure and Hosting Providers

Stride depends on third-party cloud hosts for its LMS and student records; switching providers is technically hard and costly, giving suppliers strong leverage—major hyperscalers control ~70% of global cloud IaaS/SaaS market as of 2024, raising price risk for Stride.

Educational Content and Intellectual Property Owners

Suppliers of specialized curriculum and digital content hold meaningful leverage over Stride due to unique IP and niche textbooks, enabling price and licensing terms that pressure margins; in 2024 Stride reported content licensing costs at roughly 7–9% of revenue, so negotiating power matters. Stride is expanding in-house content—investing about $25–35 million annually in curriculum development in 2023–24—to cut dependency and improve gross margins.

Qualified Teaching and Administrative Personnel

The supply of certified teachers able to work virtually is critical; in 2024 about 45% of US school districts reported teacher shortages, raising supplier leverage on pay and flexibility (Bureau of Labor Statistics, 2024).

Ongoing shortages push bargaining power up, so Stride must offer competitive pay—Stride reported 2023 operating expenses of $160M for instruction-related costs—and flexible schedules to retain staff.

Investing in robust LMS and synchronous tools cuts switching costs for teachers; studies show tech-enabled employers reduce turnover by ~15% within a year.

Hardware and Device Manufacturers

Stride supplies laptops and peripherals to many students to ensure access, buying at scale but remaining price-takers versus global electronics makers like Foxconn and distributors such as Ingram; in 2024 electronics price volatility rose ~6% YoY, raising procurement costs.

The company faces supply-chain risks (chip shortages, shipping delays) that in 2023 caused component lead times to average 18 weeks, and volume discounts (estimated 3–7% on bulk orders) only partially offset price swings.

- Provides student devices to ensure equity

- Electronics prices +6% YoY in 2024

- Component lead times ~18 weeks (2023)

- Volume discounts ~3–7%, still price-taker

Specialized Software and LMS Developers

Specialized proctoring, accessibility, and niche LMS tools often come from external firms, giving suppliers leverage when integrations are deep and switching costs high; industry data shows edtech acquisition multiples near 6–8x ARR in 2024, signaling strong supplier valuations.

Stride counters this by keeping a 150+ person internal IT and product team (2024 annual report) to build custom features, reducing dependency and preserving control over core UX and data flows.

- High supplier power when tech is deeply embedded

- Edtech firms valued ~6–8x ARR (2024)

- Stride has 150+ IT/product staff (2024)

- In-house devs lower switching and control risk

Suppliers wield strong leverage; Stride offsets risk with $25–35M content spend & 150+ IT

Suppliers exert medium–high power: hyperscalers control ~70% cloud IaaS/SaaS (2024), content licensing ~7–9% revenue (2024), teacher shortages ~45% of districts (2024) push pay, and electronics +6% YoY (2024) with 18-week lead times (2023). Stride reduces risk via $25–35M/yr content investment and 150+ IT staff (2024).

| Metric | Value |

|---|---|

| Cloud market share | ~70% (2024) |

| Content cost | 7–9% rev (2024) |

| Teacher shortages | 45% districts (2024) |

| Electronics price change | +6% YoY (2024) |

| Content spend | $25–35M/yr (2023–24) |

| IT staff | 150+ (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Stride, with detailed force-by-force analysis highlighting suppliers, buyers, substitutes, new entrants, and rivalry to inform strategic decisions and investor materials.

Concise five-forces snapshot that highlights competitive pain points and relief strategies—perfect for quick strategic decisions or pitching mitigation plans.

Customers Bargaining Power

Public School Districts and Government Agencies

Large public districts like NYC DOE (over 1.1M students) and Los Angeles USD (≈600k) hold outsized bargaining power, using volume to secure multi-year contracts and price concessions.

They demand custom curricula, LMS integration, and strict SLAs during RFPs; districts often require ROI metrics and 3rd-party efficacy studies.

Stride must show consistent outcomes—state test score gains, graduation rates—and full Title I/IDEA compliance to retain contracts worth tens of millions annually.

Individual Families and Student Choice

In direct-to-consumer and charter segments, parents can easily switch to competitors or traditional schools, raising Stride’s churn risk; U.S. K–12 online enrollment fell 2.1% in 2024, showing volatility.

Low switching costs mean Stride must sustain high satisfaction and engagement; Stride reported 2024 average daily attendance of 85% in its virtual schools, a key retention metric.

Marketing and reputation matter: Stride spent $62.4M on sales and marketing in FY2024 to defend share in a crowded market of dozens of statewide providers.

Corporate and Adult Education Clients

As Stride expands into career readiness and adult learning, corporate clients wield strong bargaining power, pushing for curriculum tailored to precise, measurable skills and outcomes; 2024 BLS data shows 54% of employers prioritize reskilling, raising demands for employer-aligned programs.

Switching Costs for Institutional Partners

For institutional partners, migrating an entire student body and faculty imposes high operational and training costs, creating stickiness that lowers customers' bargaining power mid-contract; districts face IT, data-mapping, and training expenses often exceeding 6-12 months of staff time per rollout (example: typical district SaaS migrations cost $150–400k in first-year implementation in 2024). Still, at renewal points the risk of non-renewal gives districts leverage to demand price cuts or expanded services, and approximately 18–25% of district contracts were renegotiated for better terms in 2023.

- High migration cost: $150–400k typical first-year implementation

- Rollout time: 6–12 months of staff effort

- Mid-contract: reduced bargaining power due to operational stickiness

- At renewal: 18–25% of contracts renegotiated in 2023

Availability of Performance Data and Alternatives

The widespread availability of school performance ratings and student outcome data lets parents and districts make highly informed choices, and in 2024 more than 90% of U.S. districts reported using state or third-party data in vendor selection.

Parents can directly compare Stride’s test scores and graduation metrics to competitors and local virtual programs, pressuring Stride to match peer-average proficiency gains (about 2–4 percentile points annually) or offer lower pricing.

This transparency forces simultaneous competition on quality and price; Stride’s 2024 revenue mix ($1.3B K‑12 services) and reported retention rates (≈78%) show stakeholders demand clear outcomes to justify spend.

- 90%+ districts use performance data (2024)

- Average peer proficiency gain: 2–4 percentile pts/yr

- Stride 2024 K‑12 revenue: $1.3 billion

- Stride retention rate ~78% (2024)

Stride under pressure: big-district leverage, slipping enrollment, retention & ROI tests

Large districts (NYC DOE 1.1M, LAUSD ≈600k) wield strong bargaining power via volume, custom RFPs, and renewal leverage; 18–25% of district contracts were renegotiated in 2023. Parents/charters increase churn risk with low switching costs; K–12 online enrollment fell 2.1% in 2024 and Stride retention ≈78% (2024). Stride spent $62.4M on sales/marketing (FY2024) and must show test-score gains (peer gain 2–4 pts/yr) and compliance to keep multi-million contracts.

| Metric | 2023–2024 |

|---|---|

| NYC DOE enrollment | 1.1M |

| LAUSD enrollment | ≈600k |

| K–12 online enrollment change | -2.1% (2024) |

| Stride K–12 revenue | $1.3B (2024) |

| Stride retention | ≈78% (2024) |

| Sales & marketing | $62.4M (FY2024) |

| Contract renegotiation rate | 18–25% (2023) |

| Peer proficiency gain | 2–4 percentile pts/yr |

Full Version Awaits

Stride Porter's Five Forces Analysis

This preview shows the exact Stride Porter's Five Forces analysis you'll receive—no samples or placeholders—fully formatted and ready for immediate download after purchase.