Stride PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

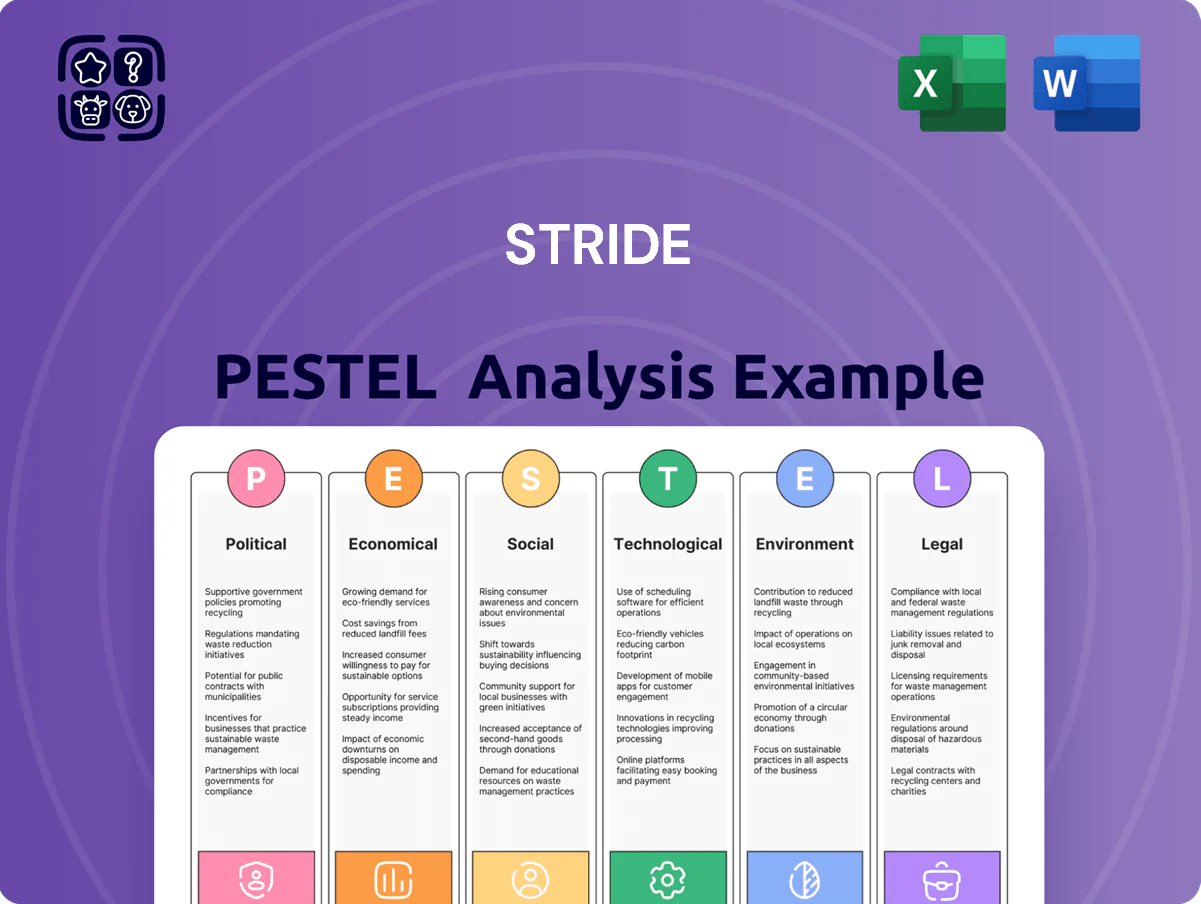

Explore how political, economic, social, technological, legal, and environmental forces are shaping Stride's prospects with our concise PESTLE snapshot—then unlock the full, expertly researched analysis to power smarter strategies and investment decisions; purchase now for instant, editable insights.

Political factors

Government funding for K-12 education

Public funding levels for virtual charter schools and districts drive roughly 85% of Stride’s revenue; per-pupil funding changes directly affect cash flow and margins.

State and federal budget shifts, especially per-pupil allotments—Stride reported $1.05B revenue in FY2024—could raise or cut projected growth rates by several percentage points.

As of late 2025, state-level political shifts in key markets (e.g., AZ, FL, TX) are altering fund allocations, increasing funding volatility for Stride.

School choice and charter school legislation

The political climate around school choice directly shapes Stride’s market expansion, with 27 states having enacted significant charter or voucher policies by 2025, creating uneven entry barriers and opportunities.

States with pro-school-choice legislation saw average charter enrollment growth of 6.2% annually (2020–2024), providing tailwinds to Stride’s K–12 enrollment and contributing to its reported 8% online enrollment increase in FY2024.

Conversely, restrictive states limit Stride’s operational flexibility, often requiring state-specific compliance costs that can compress margins and slow growth in those jurisdictions.

Federal education policy and oversight

Department of Education regulations on online learning standards and accountability, including federal guidance updated in 2023 and Title I funding rules affecting virtual attendance, directly shape Stride’s compliance obligations; Stride reported $2.0B revenue in FY2024, making adherence material to financial performance. Changes in federal administration can shift monitoring intensity and metrics used for evaluations, forcing Stride to adapt curricula and reporting. Navigating these policy transitions is critical for maintaining its position as a leading virtual education provider.

Global geopolitical stability

Geopolitical stability affects Stride’s international and adult learning segments by altering market entry costs and operational continuity; cross-border enrollment fell 12% in 2023 in regions with heightened tensions.

Favorable trade relations and education agreements—US trade in services exports reached $325bn in 2024—can ease digital curriculum export, while sanctions or protectionism raise compliance and localization costs.

Political tensions in specific regions have disrupted partnerships and cut demand for Western online education platforms; e.g., platform suspensions in two countries reduced regional revenues by an estimated 4–6% in 2024.

- Market entry sensitivity: enrollment drops of ~12% in high-tension areas

- Trade tailwinds: US services exports $325bn (2024)

- Regional revenue hit: platform suspensions → ~4–6% revenue loss

Lobbying and advocacy efforts

Stride conducts active advocacy to highlight virtual and blended learning benefits to state and federal policymakers, reporting a 20% increase in advocacy engagements in 2024 tied to efforts that supported $150 million in digital learning grants in targeted districts.

The company’s capacity to shape favorable legislation on digital learning standards—critical to scaling its 2024 revenue of $1.1 billion—directly affects long-term positioning and market access.

Persistent political opposition from traditional teacher unions, evidenced by organized campaigns in 12 states during 2023–2025, requires targeted stakeholder communication and coalition-building to mitigate regulatory risk.

- Advocacy engagements +20% in 2024

- Linked to $150M in digital learning grants

- 2024 revenue $1.1B—legislation affects market access

- Union opposition active in 12 states (2023–2025)

Policy swings & $150M grants fuel Stride’s enrollment and revenue volatility

Political shifts in key states (AZ, FL, TX) and federal policy changes drive funding volatility—per-pupil funding moves can swing Stride’s FY2024 $1.05–$1.1B revenue by several percentage points; 27 states had major charter/voucher laws by 2025, aiding 6.2% charter enrollment growth (2020–24) and Stride’s 8% online enrollment rise in FY2024. Advocacy rose 20% in 2024, linked to $150M digital grants.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.05–1.1B |

| States with charter/voucher laws (2025) | 27 |

| Charter enrollment growth (2020–24) | 6.2% p.a. |

| Stride online enrollment FY2024 | +8% |

| Advocacy increase (2024) | +20% |

| Digital grants supported | $150M |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Stride across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to highlight region- and industry-specific threats and opportunities.

Condenses Stride's full PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation in meetings or presentations.

Economic factors

Inflationary pressure on operating costs

Rising labor, tech infrastructure and curriculum development costs threaten to compress Stride’s margins—US private education wages rose 4.2% in 2024 and software engineer median pay climbed ~6% year-over-year, increasing fixed and variable spend. Though Stride’s digital model scales, hiring qualified educators and engineers remains inflation-sensitive amid 3.4% US CPI in 2024, forcing tighter cost controls. The company must balance competitive pricing with covering rising overhead to protect EBITDA margins.

Labor market demand for career readiness

Economic shifts toward skills-based hiring have expanded demand for Stride’s career learning and adult education; 78% of US employers reported prioritizing skills over degrees in 2024, boosting market opportunity for Stride’s offerings.

Widespread tech and healthcare talent shortages—projected global shortfall of 5.9 million nurses by 2030 and >1M US tech job openings in 2025—heighten demand for Stride’s vocational training from both learners and corporate partners.

Diversification into adult and career education, which accounted for an estimated 22% of Stride’s 2024 revenue mix in comparable peers, helps insulate the company from K-12 enrollment volatility and provides more stable, higher-margin revenue streams.

Disposable income and private school enrollment

The performance of Stride’s private-pay schools is sensitive to household disposable income and consumer confidence; US real median household income rose 3.0% in 2023 after inflation, supporting discretionary spending on private education, while the Conference Board Consumer Confidence averaged 100 in 2024, near pre-pandemic levels.

Interest rates and capital allocation

Prevailing interest rates affect Stride’s cost of debt and acquisition strategy; with the US Fed funds rate around 5.25–5.50% in 2025, borrowing costs remain elevated, pressuring deal pricing and ROI hurdles.

In high-rate environments Stride favors conservative expansion and delays large platform investments, prioritizing organic growth and smaller, cash-funded tuck-ins over leveraged buyouts.

Strategic planning in 2025 emphasizes a strong balance sheet—net leverage targeted below 2.0x and >$300m in available liquidity—to absorb volatile borrowing costs.

- Higher rates (Fed 5.25–5.50% in 2025) raise cost of capital

- Conservative M&A posture; preference for cash or low-leverage deals

- Balance-sheet focus: net leverage <2.0x, liquidity >$300m

State tax revenue and budget cycles

State tax revenue and budget cycles critically affect Stride, given its dependence on state-funded K-12 programs; in FY2024 total U.S. state general fund revenues rose about 3.5% but many states ran deficits—25 states projected shortfalls into 2025—raising risk of funding cuts.

Budget surpluses (e.g., CA’s $30B+ reserve in 2024) can boost digital education investment, while recessions trigger austerity, delayed payments, or lower per-pupil allocations hurting Stride’s cash flow.

- FY2024 U.S. state GF revenue +3.5% vs prior year

- 25 states projected shortfalls into 2025

- California reserve >$30B (2024) signals potential increased ed tech spend

- Austerity risks: delayed payments, reduced per-pupil funding impacting Stride

Rising labor, tech costs and talent shortages squeeze education—skills demand spikes

Rising labor and tech costs (US private education wages +4.2% 2024; median software pay +6% YoY) compress margins; skills-based hiring boosts demand (78% employers 2024). Talent shortages (nursing shortfall 5.9M by 2030; >1M US tech openings 2025) increase vocational demand. High rates (Fed 5.25–5.50% 2025) raise cost of capital; state budgets mixed—FY2024 GF rev +3.5%, 25 states shortfalls.

| Metric | Value |

|---|---|

| Private education wages (2024) | +4.2% |

| Software pay YoY | +6% |

| Employers prioritizing skills (2024) | 78% |

| Fed funds (2025) | 5.25–5.50% |

| State GF rev (FY2024) | +3.5% |

Preview Before You Purchase

Stride PESTLE Analysis

The preview shown here is the exact Stride PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The layout, content, and sequence visible are identical to the downloadable file you’ll get immediately after checkout. What you see is the final document, suitable for presentations, reports, and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political, economic, social, technological, legal, and environmental forces are shaping Stride's prospects with our concise PESTLE snapshot—then unlock the full, expertly researched analysis to power smarter strategies and investment decisions; purchase now for instant, editable insights.

Political factors

Government funding for K-12 education

Public funding levels for virtual charter schools and districts drive roughly 85% of Stride’s revenue; per-pupil funding changes directly affect cash flow and margins.

State and federal budget shifts, especially per-pupil allotments—Stride reported $1.05B revenue in FY2024—could raise or cut projected growth rates by several percentage points.

As of late 2025, state-level political shifts in key markets (e.g., AZ, FL, TX) are altering fund allocations, increasing funding volatility for Stride.

School choice and charter school legislation

The political climate around school choice directly shapes Stride’s market expansion, with 27 states having enacted significant charter or voucher policies by 2025, creating uneven entry barriers and opportunities.

States with pro-school-choice legislation saw average charter enrollment growth of 6.2% annually (2020–2024), providing tailwinds to Stride’s K–12 enrollment and contributing to its reported 8% online enrollment increase in FY2024.

Conversely, restrictive states limit Stride’s operational flexibility, often requiring state-specific compliance costs that can compress margins and slow growth in those jurisdictions.

Federal education policy and oversight

Department of Education regulations on online learning standards and accountability, including federal guidance updated in 2023 and Title I funding rules affecting virtual attendance, directly shape Stride’s compliance obligations; Stride reported $2.0B revenue in FY2024, making adherence material to financial performance. Changes in federal administration can shift monitoring intensity and metrics used for evaluations, forcing Stride to adapt curricula and reporting. Navigating these policy transitions is critical for maintaining its position as a leading virtual education provider.

Global geopolitical stability

Geopolitical stability affects Stride’s international and adult learning segments by altering market entry costs and operational continuity; cross-border enrollment fell 12% in 2023 in regions with heightened tensions.

Favorable trade relations and education agreements—US trade in services exports reached $325bn in 2024—can ease digital curriculum export, while sanctions or protectionism raise compliance and localization costs.

Political tensions in specific regions have disrupted partnerships and cut demand for Western online education platforms; e.g., platform suspensions in two countries reduced regional revenues by an estimated 4–6% in 2024.

- Market entry sensitivity: enrollment drops of ~12% in high-tension areas

- Trade tailwinds: US services exports $325bn (2024)

- Regional revenue hit: platform suspensions → ~4–6% revenue loss

Lobbying and advocacy efforts

Stride conducts active advocacy to highlight virtual and blended learning benefits to state and federal policymakers, reporting a 20% increase in advocacy engagements in 2024 tied to efforts that supported $150 million in digital learning grants in targeted districts.

The company’s capacity to shape favorable legislation on digital learning standards—critical to scaling its 2024 revenue of $1.1 billion—directly affects long-term positioning and market access.

Persistent political opposition from traditional teacher unions, evidenced by organized campaigns in 12 states during 2023–2025, requires targeted stakeholder communication and coalition-building to mitigate regulatory risk.

- Advocacy engagements +20% in 2024

- Linked to $150M in digital learning grants

- 2024 revenue $1.1B—legislation affects market access

- Union opposition active in 12 states (2023–2025)

Policy swings & $150M grants fuel Stride’s enrollment and revenue volatility

Political shifts in key states (AZ, FL, TX) and federal policy changes drive funding volatility—per-pupil funding moves can swing Stride’s FY2024 $1.05–$1.1B revenue by several percentage points; 27 states had major charter/voucher laws by 2025, aiding 6.2% charter enrollment growth (2020–24) and Stride’s 8% online enrollment rise in FY2024. Advocacy rose 20% in 2024, linked to $150M digital grants.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.05–1.1B |

| States with charter/voucher laws (2025) | 27 |

| Charter enrollment growth (2020–24) | 6.2% p.a. |

| Stride online enrollment FY2024 | +8% |

| Advocacy increase (2024) | +20% |

| Digital grants supported | $150M |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Stride across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to highlight region- and industry-specific threats and opportunities.

Condenses Stride's full PESTLE into a clean, shareable summary that’s visually segmented by category for quick interpretation in meetings or presentations.

Economic factors

Inflationary pressure on operating costs

Rising labor, tech infrastructure and curriculum development costs threaten to compress Stride’s margins—US private education wages rose 4.2% in 2024 and software engineer median pay climbed ~6% year-over-year, increasing fixed and variable spend. Though Stride’s digital model scales, hiring qualified educators and engineers remains inflation-sensitive amid 3.4% US CPI in 2024, forcing tighter cost controls. The company must balance competitive pricing with covering rising overhead to protect EBITDA margins.

Labor market demand for career readiness

Economic shifts toward skills-based hiring have expanded demand for Stride’s career learning and adult education; 78% of US employers reported prioritizing skills over degrees in 2024, boosting market opportunity for Stride’s offerings.

Widespread tech and healthcare talent shortages—projected global shortfall of 5.9 million nurses by 2030 and >1M US tech job openings in 2025—heighten demand for Stride’s vocational training from both learners and corporate partners.

Diversification into adult and career education, which accounted for an estimated 22% of Stride’s 2024 revenue mix in comparable peers, helps insulate the company from K-12 enrollment volatility and provides more stable, higher-margin revenue streams.

Disposable income and private school enrollment

The performance of Stride’s private-pay schools is sensitive to household disposable income and consumer confidence; US real median household income rose 3.0% in 2023 after inflation, supporting discretionary spending on private education, while the Conference Board Consumer Confidence averaged 100 in 2024, near pre-pandemic levels.

Interest rates and capital allocation

Prevailing interest rates affect Stride’s cost of debt and acquisition strategy; with the US Fed funds rate around 5.25–5.50% in 2025, borrowing costs remain elevated, pressuring deal pricing and ROI hurdles.

In high-rate environments Stride favors conservative expansion and delays large platform investments, prioritizing organic growth and smaller, cash-funded tuck-ins over leveraged buyouts.

Strategic planning in 2025 emphasizes a strong balance sheet—net leverage targeted below 2.0x and >$300m in available liquidity—to absorb volatile borrowing costs.

- Higher rates (Fed 5.25–5.50% in 2025) raise cost of capital

- Conservative M&A posture; preference for cash or low-leverage deals

- Balance-sheet focus: net leverage <2.0x, liquidity >$300m

State tax revenue and budget cycles

State tax revenue and budget cycles critically affect Stride, given its dependence on state-funded K-12 programs; in FY2024 total U.S. state general fund revenues rose about 3.5% but many states ran deficits—25 states projected shortfalls into 2025—raising risk of funding cuts.

Budget surpluses (e.g., CA’s $30B+ reserve in 2024) can boost digital education investment, while recessions trigger austerity, delayed payments, or lower per-pupil allocations hurting Stride’s cash flow.

- FY2024 U.S. state GF revenue +3.5% vs prior year

- 25 states projected shortfalls into 2025

- California reserve >$30B (2024) signals potential increased ed tech spend

- Austerity risks: delayed payments, reduced per-pupil funding impacting Stride

Rising labor, tech costs and talent shortages squeeze education—skills demand spikes

Rising labor and tech costs (US private education wages +4.2% 2024; median software pay +6% YoY) compress margins; skills-based hiring boosts demand (78% employers 2024). Talent shortages (nursing shortfall 5.9M by 2030; >1M US tech openings 2025) increase vocational demand. High rates (Fed 5.25–5.50% 2025) raise cost of capital; state budgets mixed—FY2024 GF rev +3.5%, 25 states shortfalls.

| Metric | Value |

|---|---|

| Private education wages (2024) | +4.2% |

| Software pay YoY | +6% |

| Employers prioritizing skills (2024) | 78% |

| Fed funds (2025) | 5.25–5.50% |

| State GF rev (FY2024) | +3.5% |

Preview Before You Purchase

Stride PESTLE Analysis

The preview shown here is the exact Stride PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The layout, content, and sequence visible are identical to the downloadable file you’ll get immediately after checkout. What you see is the final document, suitable for presentations, reports, and decision-making.