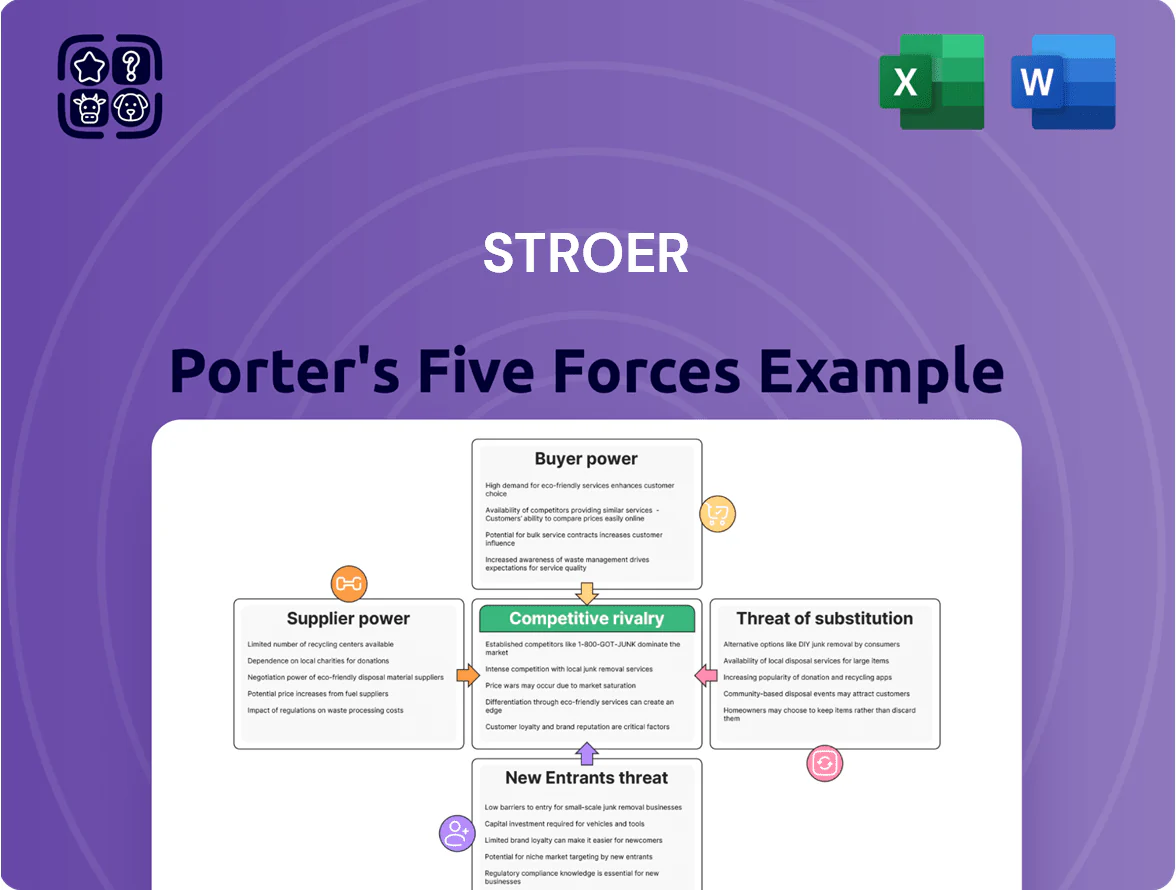

Stroer Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Suppliers Bargaining Power

Municipalities and Local Authorities

Local governments hold strong leverage over Ströer by awarding exclusive public-space advertising concessions, typically tendered every 10–15 years; Germany alone issued ~€1.2bn in outdoor advertising concessions in 2023, shaping long-term revenue streams.

These contracts are high-stakes: a single city concession can represent 8–15% of Ströer’s municipal site revenue; losing bids can cut growth and ROIC.

To win tenders, Ströer must sustain close municipal ties and meet ESG requirements—by 2024 about 60% of German tenders explicitly required carbon reduction or circularity plans.

Digital Hardware and Technology Providers

Energy and Utility Companies

Operating 150,000+ digital screens and illuminated billboards, Stroer faces heavy electricity use; a 10% rise in wholesale power prices could cut margins by ~2–3 percentage points based on 2024 energy spend of ~€120m. Fluctuating spot prices and grid fees give suppliers strong leverage, while the 2025 push to procure renewables (target: 60%+ green power) aims to stabilize costs and comply with EU CO2 reporting and likely capex for onsite PV and PPA contracts.

Data and Analytics Partners

Ströer depends on external audience measurement and location-data vendors for programmatic targeting, and those suppliers can push prices—industry fees for premium mobile location data rose ~12% in 2024.

But Ströer’s owned digital publishing and DOOH (digital out‑of‑home) footprint generated ~€520m first-party ad inventory revenue in FY 2024, cutting reliance on third-party providers.

- External data vendors hold moderate leverage via pricing

- First-party data (≈€520m revenue 2024) lowers dependence

- Hybrid sourcing mitigates supplier power but raises integration costs

Real Estate and Private Landowners

Stroer: Moderate supplier power, €520m DOOH edge amid €1.2bn German concession market

Suppliers exert moderate power: municipal concession authorities (key gatekeepers) shape long-term revenue—Germany issued ~€1.2bn outdoor concessions in 2023—and losing a city bid can cut municipal-site revenue by 8–15%. Tech and LED vendors (Samsung, Leyard) and ad-tech/data providers gained leverage as DOOH grows, but Stroer’s €520m first‑party inventory (2024) and €45m ad‑tech R&D reduce dependence; 2024 energy spend ~€120m and €200m lease costs remain material.

| Metric | 2023–2025 / 2024 |

|---|---|

| German outdoor concessions (2023) | €1.2bn |

| First‑party DOOH revenue (2024) | €520m |

| CapEx (2024) | €204m |

| Ad‑tech R&D (2024) | €45m |

| Energy spend (2024) | €120m |

| Lease/rental costs (2024) | €200m |

| Premium location rent growth (2024) | +6% YoY |

What is included in the product

Tailored Porter’s Five Forces analysis for Stroer that uncovers competitive dynamics, assesses supplier and buyer power, evaluates entry barriers and substitutes, and highlights disruptive threats and strategic levers to protect market share.

A concise five-forces snapshot tailored to Ströer—quickly pinpoint digital advertising pressures and relief levers for faster strategic decisions.

Customers Bargaining Power

Consolidation of Media Agencies

Consolidation of media agencies concentrates a large share of global ad spend—WPP, Publicis, Omnicom and IPG handled roughly 45% of global media investments in 2024—giving them strong bargaining power to demand volume discounts and preferential terms.

Ströer counters by selling exclusive cross-channel bundles that pair OOH (out-of-home) networks with high-traffic digital sites; in 2024 these bundles lifted blended CPMs by about 12% versus standalone OOH, reducing squeeze from agency-led negotiations.

Availability of Programmatic Buying

The shift to programmatic buying in out-of-home (OOH) has raised price transparency, letting buyers bid in real time for slots and locations and squeezing static CPMs; Ströer reported programmatic sales grew to ~24% of revenue in 2024, increasing buyer leverage.

Low Switching Costs for Advertisers

Brands can reallocate marketing budgets across TV, social, and outdoor with little friction; in 2024 global ad spend shifted 8% toward digital, showing fluidity between channels. If Ströer raises prices without boosting reach or engagement, advertisers can move budgets to Meta or Google, which together captured 56% of global digital ad revenue in 2023. Keeping competitive CPM (cost per mille) rates—often €2–€10 for programmatic display in Germany in 2024—is vital to hold mobile ad spend.

Demand for Measurable Return on Investment

By late 2025 advertisers demand precise attribution for OOH spending, pushing Ströer to show how ads drive store visits and online sales; industry studies show 62% of marketers require ROI measurement for offline channels and 48% shift budgets if attribution is weak.

Customers force Ströer to invest in its OOH-plus data stack—location analytics, pixel matching, and transaction linkage—since clients reduce campaign spend by ~15% without reliable attribution.

Direct Sales to Small and Medium Enterprises

Ströer’s large base of local SMEs—over 200,000 active advertisers in 2024—spreads revenue across regions, lowering dependence on big clients and reducing customer bargaining power.

SMEs individually have limited leverage versus multinationals, letting Ströer keep higher margins on local inventory (local OOH gross margin ~48% in 2024).

Easy booking platforms cut friction, raise repeat rates (estimated 30% YoY growth in digital SME bookings in 2024), and support scalable, profitable SME sales.

- 200,000+ active SME advertisers (2024)

- Local OOH gross margin ~48% (2024)

- Digital SME bookings +30% YoY (2024)

Ströer boosts CPMs +12% with OOH+digital bundles as agencies squeeze buyers, ROI demanded

Buyers have mixed leverage: big agencies (WPP, Publicis, Omnicom, IPG) controlled ~45% of global media buying in 2024 and push discounts, while Ströer offsets this with exclusive OOH+digital bundles that raised blended CPMs ~12% and programmatic sales at ~24% of revenue (2024), yet advertisers demand offline ROI (62% require it) or cut spend (~15%), forcing Ströer to invest in analytics.

| Metric | 2024 |

|---|---|

| Agency share of ad spend | ~45% |

| Ströer programmatic revenue | ~24% |

| Blended CPM lift (bundles) | +12% |

| Marketers needing offline ROI | 62% |

| Spend cut if no attribution | ~15% |

What You See Is What You Get

Stroer Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Ströer you’ll receive after purchase—no samples or placeholders, fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Suppliers Bargaining Power

Municipalities and Local Authorities

Local governments hold strong leverage over Ströer by awarding exclusive public-space advertising concessions, typically tendered every 10–15 years; Germany alone issued ~€1.2bn in outdoor advertising concessions in 2023, shaping long-term revenue streams.

These contracts are high-stakes: a single city concession can represent 8–15% of Ströer’s municipal site revenue; losing bids can cut growth and ROIC.

To win tenders, Ströer must sustain close municipal ties and meet ESG requirements—by 2024 about 60% of German tenders explicitly required carbon reduction or circularity plans.

Digital Hardware and Technology Providers

Energy and Utility Companies

Operating 150,000+ digital screens and illuminated billboards, Stroer faces heavy electricity use; a 10% rise in wholesale power prices could cut margins by ~2–3 percentage points based on 2024 energy spend of ~€120m. Fluctuating spot prices and grid fees give suppliers strong leverage, while the 2025 push to procure renewables (target: 60%+ green power) aims to stabilize costs and comply with EU CO2 reporting and likely capex for onsite PV and PPA contracts.

Data and Analytics Partners

Ströer depends on external audience measurement and location-data vendors for programmatic targeting, and those suppliers can push prices—industry fees for premium mobile location data rose ~12% in 2024.

But Ströer’s owned digital publishing and DOOH (digital out‑of‑home) footprint generated ~€520m first-party ad inventory revenue in FY 2024, cutting reliance on third-party providers.

- External data vendors hold moderate leverage via pricing

- First-party data (≈€520m revenue 2024) lowers dependence

- Hybrid sourcing mitigates supplier power but raises integration costs

Real Estate and Private Landowners

Stroer: Moderate supplier power, €520m DOOH edge amid €1.2bn German concession market

Suppliers exert moderate power: municipal concession authorities (key gatekeepers) shape long-term revenue—Germany issued ~€1.2bn outdoor concessions in 2023—and losing a city bid can cut municipal-site revenue by 8–15%. Tech and LED vendors (Samsung, Leyard) and ad-tech/data providers gained leverage as DOOH grows, but Stroer’s €520m first‑party inventory (2024) and €45m ad‑tech R&D reduce dependence; 2024 energy spend ~€120m and €200m lease costs remain material.

| Metric | 2023–2025 / 2024 |

|---|---|

| German outdoor concessions (2023) | €1.2bn |

| First‑party DOOH revenue (2024) | €520m |

| CapEx (2024) | €204m |

| Ad‑tech R&D (2024) | €45m |

| Energy spend (2024) | €120m |

| Lease/rental costs (2024) | €200m |

| Premium location rent growth (2024) | +6% YoY |

What is included in the product

Tailored Porter’s Five Forces analysis for Stroer that uncovers competitive dynamics, assesses supplier and buyer power, evaluates entry barriers and substitutes, and highlights disruptive threats and strategic levers to protect market share.

A concise five-forces snapshot tailored to Ströer—quickly pinpoint digital advertising pressures and relief levers for faster strategic decisions.

Customers Bargaining Power

Consolidation of Media Agencies

Consolidation of media agencies concentrates a large share of global ad spend—WPP, Publicis, Omnicom and IPG handled roughly 45% of global media investments in 2024—giving them strong bargaining power to demand volume discounts and preferential terms.

Ströer counters by selling exclusive cross-channel bundles that pair OOH (out-of-home) networks with high-traffic digital sites; in 2024 these bundles lifted blended CPMs by about 12% versus standalone OOH, reducing squeeze from agency-led negotiations.

Availability of Programmatic Buying

The shift to programmatic buying in out-of-home (OOH) has raised price transparency, letting buyers bid in real time for slots and locations and squeezing static CPMs; Ströer reported programmatic sales grew to ~24% of revenue in 2024, increasing buyer leverage.

Low Switching Costs for Advertisers

Brands can reallocate marketing budgets across TV, social, and outdoor with little friction; in 2024 global ad spend shifted 8% toward digital, showing fluidity between channels. If Ströer raises prices without boosting reach or engagement, advertisers can move budgets to Meta or Google, which together captured 56% of global digital ad revenue in 2023. Keeping competitive CPM (cost per mille) rates—often €2–€10 for programmatic display in Germany in 2024—is vital to hold mobile ad spend.

Demand for Measurable Return on Investment

By late 2025 advertisers demand precise attribution for OOH spending, pushing Ströer to show how ads drive store visits and online sales; industry studies show 62% of marketers require ROI measurement for offline channels and 48% shift budgets if attribution is weak.

Customers force Ströer to invest in its OOH-plus data stack—location analytics, pixel matching, and transaction linkage—since clients reduce campaign spend by ~15% without reliable attribution.

Direct Sales to Small and Medium Enterprises

Ströer’s large base of local SMEs—over 200,000 active advertisers in 2024—spreads revenue across regions, lowering dependence on big clients and reducing customer bargaining power.

SMEs individually have limited leverage versus multinationals, letting Ströer keep higher margins on local inventory (local OOH gross margin ~48% in 2024).

Easy booking platforms cut friction, raise repeat rates (estimated 30% YoY growth in digital SME bookings in 2024), and support scalable, profitable SME sales.

- 200,000+ active SME advertisers (2024)

- Local OOH gross margin ~48% (2024)

- Digital SME bookings +30% YoY (2024)

Ströer boosts CPMs +12% with OOH+digital bundles as agencies squeeze buyers, ROI demanded

Buyers have mixed leverage: big agencies (WPP, Publicis, Omnicom, IPG) controlled ~45% of global media buying in 2024 and push discounts, while Ströer offsets this with exclusive OOH+digital bundles that raised blended CPMs ~12% and programmatic sales at ~24% of revenue (2024), yet advertisers demand offline ROI (62% require it) or cut spend (~15%), forcing Ströer to invest in analytics.

| Metric | 2024 |

|---|---|

| Agency share of ad spend | ~45% |

| Ströer programmatic revenue | ~24% |

| Blended CPM lift (bundles) | +12% |

| Marketers needing offline ROI | 62% |

| Spend cut if no attribution | ~15% |

What You See Is What You Get

Stroer Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Ströer you’ll receive after purchase—no samples or placeholders, fully formatted and ready for immediate download and use.