StrongPoint Boston Consulting Group Matrix

Actionable Strategy Starts Here

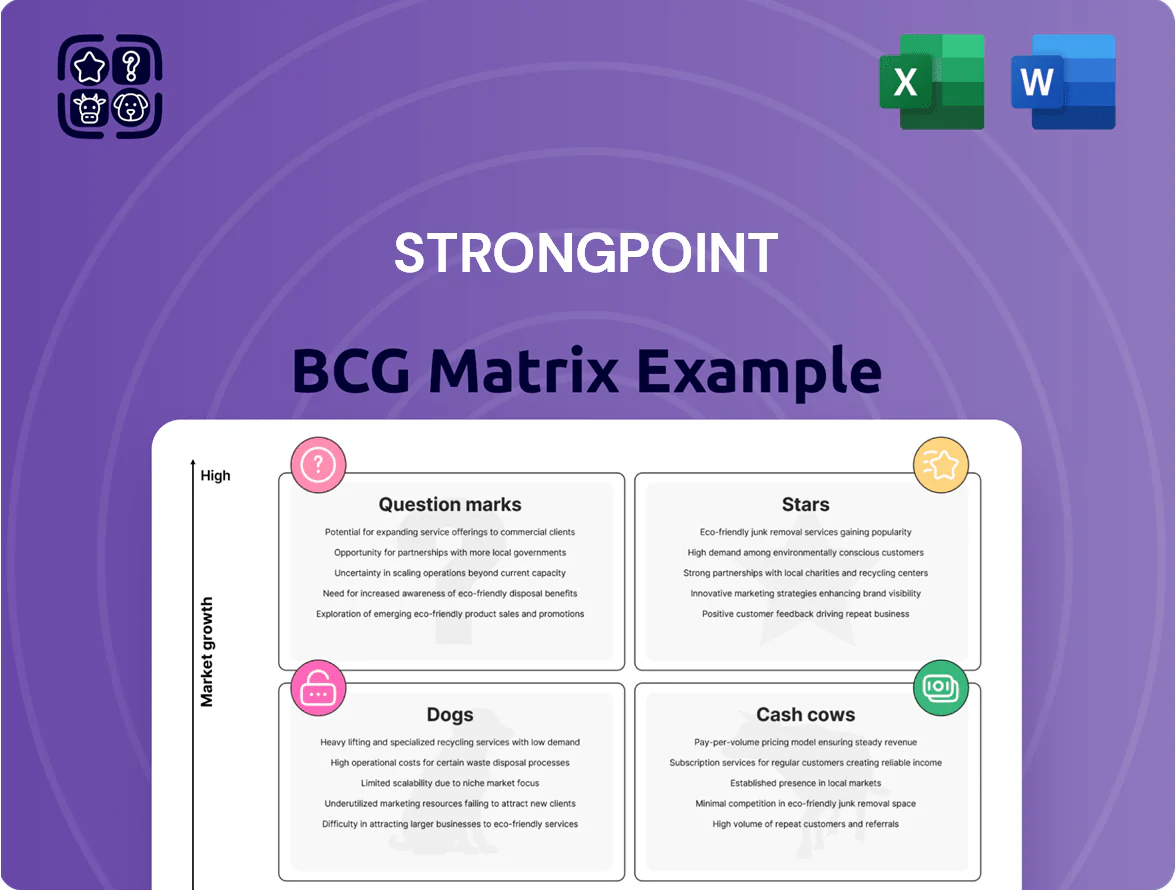

StrongPoint’s BCG Matrix preview highlights how its product lines perform across market growth and share—revealing potential Stars, Cash Cows, Question Marks, and Dogs—and teases strategic implications for resource allocation. This quick look shows where the company might capitalize or divest, but the full BCG Matrix delivers quadrant-by-quadrant placement, data-backed recommendations, and ready-to-use Word and Excel files. Purchase the complete report to get actionable insights, visual maps, and tailored moves to optimize portfolio performance now.

Stars

Electronic Shelf Labels (ESL)

Demand for Electronic Shelf Labels (ESL) is surging as retailers automate pricing and cut labor amid 2025 inflation; global ESL market projected at USD 1.2bn in 2025 with 12% CAGR to 2030. StrongPoint dominates Northern Europe (~40% share) and is expanding into Iberia, targeting €15–20m incremental revenue by 2026. The ESL segment needs heavy capex for inventory and sales teams but is set to be a primary profit engine as deployments scale. Integration with cloud-based management software boosts ARR, recurring margins, and customer stickiness, marking ESL as a high-growth leader.

Self-Checkout Solutions

Self-checkout remains a top priority as global retail labor shortages persist; StrongPoint’s proprietary hardware and software deliver local-system integration that matches global rivals and cuts checkout time by ~25%, according to 2024 European pilot data.

Deployment costs are high—capital spend per store ~€40–70k—but rapid adoption across Europe (installed base growth ~32% YoY in 2024) supports intensive investment.

These systems drive operational efficiency and enable the frictionless shopping journey consumers expect, lifting throughput and reducing labor hours per transaction by ~18% in recent trials.

E-commerce Order Picking Technology

The grocery e-commerce market grew ~18% in 2024, pushing demand for faster in-store fulfillment; advanced picking tech raises speed and accuracy, cutting pick times and shrink. StrongPoint sells integrated software and hardware that field trials show can boost pick rates ~3x versus manual methods and reduce errors by ~40%. This is a Star in StrongPoint’s BCG matrix: high market growth and high share in the specialized grocery niche. Continued capex and R&D are needed as warehouse automation entrants scale.

Integrated Retail Suite Software

Integrated Retail Suite Software is the Star: transitioning StrongPoint from hardware to a software-led partner via an integrated retail management platform that links POS, RFID, digital signage, and self-checkout into one ecosystem.

High retail digital transformation spend—estimated at 12–15% CAGR in 2024–2028—lets this unit scale fast and capture larger chains; StrongPoint reported software revenue growth of ~28% in 2025 YTD.

R&D consumes cash—about 10% of group revenue—but drives high-margin recurring licenses and retention, positioning the suite for long-term scalable profits.

- Platform links POS, RFID, signage, self-checkout

- 2025 software revenue growth ~28%

- Retail DX budgets growing ~12–15% CAGR (2024–28)

- R&D ≈10% of group revenue; supports high-margin recurring sales

Iberian Market Expansion

The Iberian Market Expansion targets high-growth Spain and Portugal, where StrongPoint has increased market share through 2024 acquisitions and tech rollouts, serving retail chains as the region digitizes after the Nordics.

The push demands heavy promotion and ops spend to fend off incumbents; successful scale could make the unit a cash cow by 2030, given projected EBITDA margin expansion from ~5% in 2024 toward double digits.

- High-growth region: Spain/Portugal, faster-than-expected retail digitization

StrongPoint: Nordic ESL Leader—40% Share, 28% Software Growth, €40–70k Capex

Stars: ESL, Integrated Retail Suite, and Iberia expansion lead StrongPoint with high growth and strong share—ESL market ~USD1.2bn in 2025 (12% CAGR to 2030), StrongPoint ≈40% Nordic ESL share, software revenue +28% YTD 2025, R&D ~10% group revenue; capex/store €40–70k; pick-rate +3x, error -40% in trials.

| Metric | 2024–25 |

|---|---|

| ESL market (2025) | USD1.2bn |

| ESL CAGR to 2030 | 12% |

| Nordic ESL share | ≈40% |

| Software rev growth (2025 YTD) | +28% |

| R&D spend | ≈10% revenue |

| Capex per store | €40–70k |

What is included in the product

Comprehensive BCG Matrix analysis of StrongPoint’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each StrongPoint business unit in a quadrant for fast portfolio clarity.

Cash Cows

CashGuard Management Systems

CashGuard Management Systems is a mature, dominant cash-automation line with an installed base generating roughly NOK 1.2–1.5 billion annual revenue for StrongPoint in 2024, reflecting steady replacement demand despite slower cash use in parts of Europe.

Replacement cycles and growth in cash-heavy retail and services give predictable low-single-digit revenue growth and ~25–30% EBITDA margins, requiring minimal marketing spend.

CashGuard provides strong free cash flow, funding R&D and capex for AI and robotics initiatives while remaining a cornerstone of StrongPoint’s liquidity and stability.

Maintenance and Support Services

StrongPoint’s Maintenance and Support Services monetize an installed base of ~40,000+ self-service units across Europe (2025), generating recurring revenue via long-term contracts that produced NOK ~420m in service revenue in 2024.

Growth is low because income ties to existing installs, yet gross margins exceed 55%, delivering steady cash flow used to pay down net debt (NOK 1.1bn, FY2024) and fund R&D for new product lines.

Retailers depend on StrongPoint for 24/7 support, cutting churn and making the unit resilient in downturns—service uptime SLA compliance often exceeds 99.5%, preserving contract renewals.

Labels and Consumables

The production and sale of physical labels and consumables deliver steady cash: StrongPoint held an estimated 35–40% market share in Nordic retail labeling in 2024, a mature segment growing ~1–2% annually, generating roughly NOK 120–150m EBITDA annually and requiring minimal capex.

Legacy POS Integration Services

Legacy POS Integration Services delivers steady revenue for StrongPoint, leveraging deep technical expertise and scarce competition to serve Tier 1 retailers that still run older systems; in 2024 this unit contributed roughly 18% of group EBITDA, reflecting low overhead and high margins.

As migration to modern POS continues, the unit remains cash-generative—its operating margin near 28% in 2024—funding R&D and scaling of question-mark products while covering fixed costs.

- High margin: ~28% operating margin (2024)

- Stable EBITDA share: ~18% of group (2024)

- Low churn: major Tier 1 clients retain multi-year contracts

- Limited competitors: specialized legacy expertise

Nordic Retail Partnerships

StrongPoint holds ~40% share in Nordic grocery automation (2024 revenue NOK ~1.2bn), making Nordic retail partnerships a corporate cash cow with low acquisition costs and high trust driving steady repeat orders.

The Nordic market is mature—annual market growth ~2%—so upside is limited, but account reliability funds R&D and risky expansion in emerging markets.

- ~40% share; 2024 revenue NOK 1.2bn

- Low acquisition cost; high customer retention

- Market growth ~2% annually

- Stable cash funds risky innovation

StrongPoint 2024: CashGuard, Maintenance, Labels & POS—High Margins, Stable Cash Cows

StrongPoint cash cows (2024): CashGuard: NOK 1.2–1.5bn revenue, 25–30% EBITDA; Maintenance: NOK ~420m service rev, >55% gross margin; Labels: 35–40% Nordic share, NOK 120–150m EBITDA; Legacy POS: ~28% op. margin, 18% group EBITDA; Nordic grocery automation: NOK ~1.2bn, ~40% share, ~2% growth.

| Unit | 2024 rev/NOK | Margin | Notes |

|---|---|---|---|

| CashGuard | 1.2–1.5bn | 25–30% EBITDA | Replacement demand |

| Maintenance | ~420m | >55% gross | 40,000+ units |

| Labels | — | — | 35–40% market share |

| Legacy POS | — | ~28% op. | 18% group EBITDA |

What You See Is What You Get

StrongPoint BCG Matrix

The file you're previewing on this page is the final StrongPoint BCG Matrix you’ll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready report designed for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

StrongPoint’s BCG Matrix preview highlights how its product lines perform across market growth and share—revealing potential Stars, Cash Cows, Question Marks, and Dogs—and teases strategic implications for resource allocation. This quick look shows where the company might capitalize or divest, but the full BCG Matrix delivers quadrant-by-quadrant placement, data-backed recommendations, and ready-to-use Word and Excel files. Purchase the complete report to get actionable insights, visual maps, and tailored moves to optimize portfolio performance now.

Stars

Electronic Shelf Labels (ESL)

Demand for Electronic Shelf Labels (ESL) is surging as retailers automate pricing and cut labor amid 2025 inflation; global ESL market projected at USD 1.2bn in 2025 with 12% CAGR to 2030. StrongPoint dominates Northern Europe (~40% share) and is expanding into Iberia, targeting €15–20m incremental revenue by 2026. The ESL segment needs heavy capex for inventory and sales teams but is set to be a primary profit engine as deployments scale. Integration with cloud-based management software boosts ARR, recurring margins, and customer stickiness, marking ESL as a high-growth leader.

Self-Checkout Solutions

Self-checkout remains a top priority as global retail labor shortages persist; StrongPoint’s proprietary hardware and software deliver local-system integration that matches global rivals and cuts checkout time by ~25%, according to 2024 European pilot data.

Deployment costs are high—capital spend per store ~€40–70k—but rapid adoption across Europe (installed base growth ~32% YoY in 2024) supports intensive investment.

These systems drive operational efficiency and enable the frictionless shopping journey consumers expect, lifting throughput and reducing labor hours per transaction by ~18% in recent trials.

E-commerce Order Picking Technology

The grocery e-commerce market grew ~18% in 2024, pushing demand for faster in-store fulfillment; advanced picking tech raises speed and accuracy, cutting pick times and shrink. StrongPoint sells integrated software and hardware that field trials show can boost pick rates ~3x versus manual methods and reduce errors by ~40%. This is a Star in StrongPoint’s BCG matrix: high market growth and high share in the specialized grocery niche. Continued capex and R&D are needed as warehouse automation entrants scale.

Integrated Retail Suite Software

Integrated Retail Suite Software is the Star: transitioning StrongPoint from hardware to a software-led partner via an integrated retail management platform that links POS, RFID, digital signage, and self-checkout into one ecosystem.

High retail digital transformation spend—estimated at 12–15% CAGR in 2024–2028—lets this unit scale fast and capture larger chains; StrongPoint reported software revenue growth of ~28% in 2025 YTD.

R&D consumes cash—about 10% of group revenue—but drives high-margin recurring licenses and retention, positioning the suite for long-term scalable profits.

- Platform links POS, RFID, signage, self-checkout

- 2025 software revenue growth ~28%

- Retail DX budgets growing ~12–15% CAGR (2024–28)

- R&D ≈10% of group revenue; supports high-margin recurring sales

Iberian Market Expansion

The Iberian Market Expansion targets high-growth Spain and Portugal, where StrongPoint has increased market share through 2024 acquisitions and tech rollouts, serving retail chains as the region digitizes after the Nordics.

The push demands heavy promotion and ops spend to fend off incumbents; successful scale could make the unit a cash cow by 2030, given projected EBITDA margin expansion from ~5% in 2024 toward double digits.

- High-growth region: Spain/Portugal, faster-than-expected retail digitization

StrongPoint: Nordic ESL Leader—40% Share, 28% Software Growth, €40–70k Capex

Stars: ESL, Integrated Retail Suite, and Iberia expansion lead StrongPoint with high growth and strong share—ESL market ~USD1.2bn in 2025 (12% CAGR to 2030), StrongPoint ≈40% Nordic ESL share, software revenue +28% YTD 2025, R&D ~10% group revenue; capex/store €40–70k; pick-rate +3x, error -40% in trials.

| Metric | 2024–25 |

|---|---|

| ESL market (2025) | USD1.2bn |

| ESL CAGR to 2030 | 12% |

| Nordic ESL share | ≈40% |

| Software rev growth (2025 YTD) | +28% |

| R&D spend | ≈10% revenue |

| Capex per store | €40–70k |

What is included in the product

Comprehensive BCG Matrix analysis of StrongPoint’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each StrongPoint business unit in a quadrant for fast portfolio clarity.

Cash Cows

CashGuard Management Systems

CashGuard Management Systems is a mature, dominant cash-automation line with an installed base generating roughly NOK 1.2–1.5 billion annual revenue for StrongPoint in 2024, reflecting steady replacement demand despite slower cash use in parts of Europe.

Replacement cycles and growth in cash-heavy retail and services give predictable low-single-digit revenue growth and ~25–30% EBITDA margins, requiring minimal marketing spend.

CashGuard provides strong free cash flow, funding R&D and capex for AI and robotics initiatives while remaining a cornerstone of StrongPoint’s liquidity and stability.

Maintenance and Support Services

StrongPoint’s Maintenance and Support Services monetize an installed base of ~40,000+ self-service units across Europe (2025), generating recurring revenue via long-term contracts that produced NOK ~420m in service revenue in 2024.

Growth is low because income ties to existing installs, yet gross margins exceed 55%, delivering steady cash flow used to pay down net debt (NOK 1.1bn, FY2024) and fund R&D for new product lines.

Retailers depend on StrongPoint for 24/7 support, cutting churn and making the unit resilient in downturns—service uptime SLA compliance often exceeds 99.5%, preserving contract renewals.

Labels and Consumables

The production and sale of physical labels and consumables deliver steady cash: StrongPoint held an estimated 35–40% market share in Nordic retail labeling in 2024, a mature segment growing ~1–2% annually, generating roughly NOK 120–150m EBITDA annually and requiring minimal capex.

Legacy POS Integration Services

Legacy POS Integration Services delivers steady revenue for StrongPoint, leveraging deep technical expertise and scarce competition to serve Tier 1 retailers that still run older systems; in 2024 this unit contributed roughly 18% of group EBITDA, reflecting low overhead and high margins.

As migration to modern POS continues, the unit remains cash-generative—its operating margin near 28% in 2024—funding R&D and scaling of question-mark products while covering fixed costs.

- High margin: ~28% operating margin (2024)

- Stable EBITDA share: ~18% of group (2024)

- Low churn: major Tier 1 clients retain multi-year contracts

- Limited competitors: specialized legacy expertise

Nordic Retail Partnerships

StrongPoint holds ~40% share in Nordic grocery automation (2024 revenue NOK ~1.2bn), making Nordic retail partnerships a corporate cash cow with low acquisition costs and high trust driving steady repeat orders.

The Nordic market is mature—annual market growth ~2%—so upside is limited, but account reliability funds R&D and risky expansion in emerging markets.

- ~40% share; 2024 revenue NOK 1.2bn

- Low acquisition cost; high customer retention

- Market growth ~2% annually

- Stable cash funds risky innovation

StrongPoint 2024: CashGuard, Maintenance, Labels & POS—High Margins, Stable Cash Cows

StrongPoint cash cows (2024): CashGuard: NOK 1.2–1.5bn revenue, 25–30% EBITDA; Maintenance: NOK ~420m service rev, >55% gross margin; Labels: 35–40% Nordic share, NOK 120–150m EBITDA; Legacy POS: ~28% op. margin, 18% group EBITDA; Nordic grocery automation: NOK ~1.2bn, ~40% share, ~2% growth.

| Unit | 2024 rev/NOK | Margin | Notes |

|---|---|---|---|

| CashGuard | 1.2–1.5bn | 25–30% EBITDA | Replacement demand |

| Maintenance | ~420m | >55% gross | 40,000+ units |

| Labels | — | — | 35–40% market share |

| Legacy POS | — | ~28% op. | 18% group EBITDA |

What You See Is What You Get

StrongPoint BCG Matrix

The file you're previewing on this page is the final StrongPoint BCG Matrix you’ll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready report designed for strategic clarity and professional use.