Stryker Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

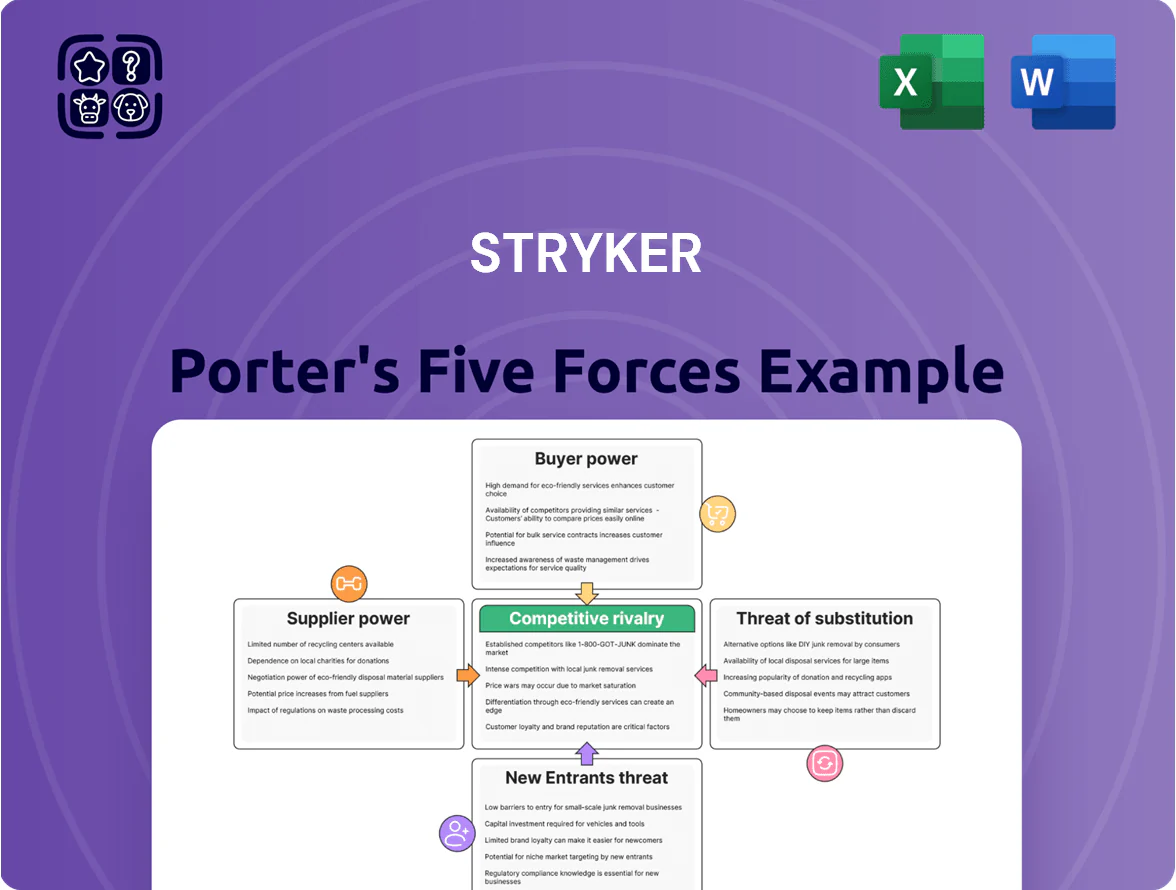

Stryker faces strong intra-industry rivalry driven by innovation cycles and consolidation, moderate supplier power due to specialized components, and high buyer expectations for quality and value; substitute threats are limited but emerging tech poses risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stryker’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Stryker depends on high‑purity inputs—titanium, cobalt‑chrome, and medical‑grade polymers—sourced from a small pool of certified suppliers, giving vendors pricing leverage; in 2024 titanium scrap prices averaged about $5.50/lb and cobalt spot rose ~22% year‑on‑year, raising input cost risk. Any global disruption (mining strikes, trade limits) can quickly raise Stryker’s production costs and extend lead times by weeks to months.

Strict Regulatory Compliance for Vendors

Suppliers in medical tech face strict FDA and ISO 13485 quality rules, raising vendor-entry costs and keeping supplier churn low; for example, 72% of medtech suppliers report regulatory compliance as the top barrier to new contracts (FDA 2024 industry survey).

Stryker cannot rapidly swap vendors because supplier requalification often takes 6–12 months and can cost millions in validation and testing.

That slows sourcing flexibility and boosts incumbent suppliers’ leverage, so Stryker favors proven, compliant partners even if they command 3–7% higher margins to avoid regulatory risk.

Concentration of High-Tech Component Providers

As Stryker adds robotics and digital features to systems like Mako, it relies on specialized semiconductors and software from a handful of global suppliers, cutting Stryker’s bargaining power; the top 5 semiconductor firms held ~60% of market revenue in 2024.

In 2023–24 chip shortages lifted component costs 15–30% in medtech segments, and single-supplier risks can delay device deliveries, increasing inventory and working-capital needs.

Switching Costs for Specialized Tooling

Many Stryker components use custom tooling and proprietary processes developed with long-term suppliers; replacing a supplier often needs capital outlays and 3–9 months of re-tooling and validation, raising operational risk and launch delays.

These high switching costs—estimated at tens of millions for major orthopedic lines—discourage frequent vendor changes, giving suppliers stronger bargaining power over price and lead times.

- Custom tooling -> long lead times (3–9 months)

- Re-tooling cost -> tens of millions for major lines

- Validation risk -> potential regulatory delays

- Net effect -> stronger supplier leverage

Impact of Global Logistics and Inflation

Rising energy costs and global logistics bottlenecks pushed supplier input prices up about 6–9% in 2024, letting some suppliers pass through increases despite Stryker’s scale.

Systemic manufacturing inflation—US PPI for medical equipment rose ~7% year-over-year in 2024—limits Stryker’s bargaining leverage on costs.

Stryker must offset input inflation by improving operational efficiency and pricing to protect 2024 gross margin (~49%).

- Supplier price pass-through ~6–9% (2024)

- US medical equipment PPI +7% YoY (2024)

- Stryker gross margin ~49% (FY2024)

Supplier leverage squeezes Stryker: long requalification, high input inflation

Suppliers hold strong leverage: few certified sources for titanium, cobalt‑chrome, med‑grade polymers and semiconductors, long requalification (6–12 months) and retooling (3–9 months) costs (tens of millions), 2024 input inflation ~6–9% and US med‑equipment PPI +7% cut Stryker’s bargaining power against a ~49% gross margin (FY2024).

| Metric | Value (2024) |

|---|---|

| Requalification | 6–12 months |

| Retooling | 3–9 months; tens of $M |

| Input inflation | 6–9% |

| US med‑equipment PPI | +7% YoY |

| Stryker gross margin | ~49% FY2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Stryker, uncovering competitive pressures, supplier and buyer influence on pricing, entry barriers, substitute threats, and strategic implications for sustaining market leadership.

A concise Porter's Five Forces one-sheet for Stryker—quickly spot supplier, buyer, and competitive pressures to guide surgical device strategy and M&A decisions.

Customers Bargaining Power

Consolidation of Healthcare Providers

The US hospital market saw 40% of hospitals in systems by 2023, and integrated delivery networks (IDNs) now account for roughly 60% of acute-care spend, giving large buyers strong leverage over suppliers like Stryker.

These IDNs use procurement volumes—often millions in annual device spend—to extract deeper discounts and tougher service terms, pressuring Stryker’s margins.

Stryker must offer competitive pricing and outcome-linked contracts to win multi-year IDN deals; in 2024 Stryker reported 10% of revenue tied to large system contracts, raising negotiation stakes.

Influence of Group Purchasing Organizations

Group Purchasing Organizations (GPOs) pool buying power of hospitals and clinics—US GPOs negotiated about 70% of acute care hospital purchases in 2024—so inclusion on a GPO’s approved vendor list strongly affects Stryker’s reach.

Stryker must compete for GPO contracts; winning can open access to thousands of facilities and drive high-volume sales, while losing can cut off sizeable revenue streams in key US regions.

Failure to secure GPO placement often shifts procurement to competitors and can reduce Stryker’s market share in targeted product categories by double-digit percentages within 12–24 months.

Shift Toward Value-Based Procurement

Healthcare buyers are shifting to value-based procurement, linking payment to outcomes; by 2024 roughly 35% of US Medicare payments were tied to value-based models, so hospitals demand outcome data for Stryker devices. Customers press Stryker for trials showing robotic systems cut length-of-stay or readmissions; studies must demonstrate cost-per-case reductions (eg, $1,200–$3,500 per joint case) to justify premium pricing. This compresses margin unless efficacy is proven.

Price Transparency and Digital Procurement

Digital procurement platforms raised price transparency in medtech: 2024 Vizient data shows 60% of US hospitals use e-procurement, enabling easier cost comparisons and tighter vendor scrutiny.

Buyers now use benchmarking to flag price gaps, driving tougher negotiations—Stryker saw hospital contract pressure contribute to a 0.8 percentage-point margin compression in 2024.

Stryker must keep innovating product differentiation—unique features, bundled services, or outcomes data—to justify premiums in a market where list prices are widely visible.

- 60% US hospitals on e-procurement (Vizient, 2024)

- 0.8 pp margin hit tied to contract pressure (Stryker, 2024 results)

- Differentiate via outcomes data, services, bundles

Budgetary Constraints in Public Health

Government-funded hospitals face tight budgets and push Stryker hard on price; in 2024 OECD health spending averaged 9.2% of GDP, tightening procurement choices in many markets.

Where single-payer systems prevail—Canada, UK, Sweden—the state acts as sole buyer, giving customers exceptional bargaining power and driving centralized tendering and volume discounts.

Stryker adapts via tiered pricing, value-based contracting, and local manufacturing; in 2023 the company reported 7% international organic sales growth, reflecting pricing and market mix moves.

- Public buyers more price-sensitive

- Single-payer = high bargaining power

- Stryker uses tiered pricing, contracts, local sourcing

- OECD health spend 9.2% GDP (2024)

Buyer Power, Value-Based Contracts & E‑procurement Squeeze Stryker Margins

Large US IDNs and GPOs (≈60% acute spend; GPOs cover ~70% purchases) give customers strong leverage, forcing Stryker into deeper discounts, outcome-linked deals, and margin pressure (≈0.8 pp in 2024).

Value-based procurement (≈35% Medicare tied to value in 2024) and e-procurement (60% hospitals) raise transparency, so Stryker must use outcomes data, bundles, and tiered pricing to retain share.

| Metric | Value |

|---|---|

| IDN share of acute spend | ≈60% |

| GPO coverage of purchases | ≈70% |

| E-procurement adoption (US hospitals, 2024) | 60% |

| Medicare value-based payments (2024) | ≈35% |

| Stryker margin impact (2024) | −0.8 pp |

What You See Is What You Get

Stryker Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Stryker you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're looking at the actual, final file; once you complete your purchase, you’ll get instant access to this same document. No mockups or samples—the preview is the deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Stryker faces strong intra-industry rivalry driven by innovation cycles and consolidation, moderate supplier power due to specialized components, and high buyer expectations for quality and value; substitute threats are limited but emerging tech poses risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stryker’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

Stryker depends on high‑purity inputs—titanium, cobalt‑chrome, and medical‑grade polymers—sourced from a small pool of certified suppliers, giving vendors pricing leverage; in 2024 titanium scrap prices averaged about $5.50/lb and cobalt spot rose ~22% year‑on‑year, raising input cost risk. Any global disruption (mining strikes, trade limits) can quickly raise Stryker’s production costs and extend lead times by weeks to months.

Strict Regulatory Compliance for Vendors

Suppliers in medical tech face strict FDA and ISO 13485 quality rules, raising vendor-entry costs and keeping supplier churn low; for example, 72% of medtech suppliers report regulatory compliance as the top barrier to new contracts (FDA 2024 industry survey).

Stryker cannot rapidly swap vendors because supplier requalification often takes 6–12 months and can cost millions in validation and testing.

That slows sourcing flexibility and boosts incumbent suppliers’ leverage, so Stryker favors proven, compliant partners even if they command 3–7% higher margins to avoid regulatory risk.

Concentration of High-Tech Component Providers

As Stryker adds robotics and digital features to systems like Mako, it relies on specialized semiconductors and software from a handful of global suppliers, cutting Stryker’s bargaining power; the top 5 semiconductor firms held ~60% of market revenue in 2024.

In 2023–24 chip shortages lifted component costs 15–30% in medtech segments, and single-supplier risks can delay device deliveries, increasing inventory and working-capital needs.

Switching Costs for Specialized Tooling

Many Stryker components use custom tooling and proprietary processes developed with long-term suppliers; replacing a supplier often needs capital outlays and 3–9 months of re-tooling and validation, raising operational risk and launch delays.

These high switching costs—estimated at tens of millions for major orthopedic lines—discourage frequent vendor changes, giving suppliers stronger bargaining power over price and lead times.

- Custom tooling -> long lead times (3–9 months)

- Re-tooling cost -> tens of millions for major lines

- Validation risk -> potential regulatory delays

- Net effect -> stronger supplier leverage

Impact of Global Logistics and Inflation

Rising energy costs and global logistics bottlenecks pushed supplier input prices up about 6–9% in 2024, letting some suppliers pass through increases despite Stryker’s scale.

Systemic manufacturing inflation—US PPI for medical equipment rose ~7% year-over-year in 2024—limits Stryker’s bargaining leverage on costs.

Stryker must offset input inflation by improving operational efficiency and pricing to protect 2024 gross margin (~49%).

- Supplier price pass-through ~6–9% (2024)

- US medical equipment PPI +7% YoY (2024)

- Stryker gross margin ~49% (FY2024)

Supplier leverage squeezes Stryker: long requalification, high input inflation

Suppliers hold strong leverage: few certified sources for titanium, cobalt‑chrome, med‑grade polymers and semiconductors, long requalification (6–12 months) and retooling (3–9 months) costs (tens of millions), 2024 input inflation ~6–9% and US med‑equipment PPI +7% cut Stryker’s bargaining power against a ~49% gross margin (FY2024).

| Metric | Value (2024) |

|---|---|

| Requalification | 6–12 months |

| Retooling | 3–9 months; tens of $M |

| Input inflation | 6–9% |

| US med‑equipment PPI | +7% YoY |

| Stryker gross margin | ~49% FY2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Stryker, uncovering competitive pressures, supplier and buyer influence on pricing, entry barriers, substitute threats, and strategic implications for sustaining market leadership.

A concise Porter's Five Forces one-sheet for Stryker—quickly spot supplier, buyer, and competitive pressures to guide surgical device strategy and M&A decisions.

Customers Bargaining Power

Consolidation of Healthcare Providers

The US hospital market saw 40% of hospitals in systems by 2023, and integrated delivery networks (IDNs) now account for roughly 60% of acute-care spend, giving large buyers strong leverage over suppliers like Stryker.

These IDNs use procurement volumes—often millions in annual device spend—to extract deeper discounts and tougher service terms, pressuring Stryker’s margins.

Stryker must offer competitive pricing and outcome-linked contracts to win multi-year IDN deals; in 2024 Stryker reported 10% of revenue tied to large system contracts, raising negotiation stakes.

Influence of Group Purchasing Organizations

Group Purchasing Organizations (GPOs) pool buying power of hospitals and clinics—US GPOs negotiated about 70% of acute care hospital purchases in 2024—so inclusion on a GPO’s approved vendor list strongly affects Stryker’s reach.

Stryker must compete for GPO contracts; winning can open access to thousands of facilities and drive high-volume sales, while losing can cut off sizeable revenue streams in key US regions.

Failure to secure GPO placement often shifts procurement to competitors and can reduce Stryker’s market share in targeted product categories by double-digit percentages within 12–24 months.

Shift Toward Value-Based Procurement

Healthcare buyers are shifting to value-based procurement, linking payment to outcomes; by 2024 roughly 35% of US Medicare payments were tied to value-based models, so hospitals demand outcome data for Stryker devices. Customers press Stryker for trials showing robotic systems cut length-of-stay or readmissions; studies must demonstrate cost-per-case reductions (eg, $1,200–$3,500 per joint case) to justify premium pricing. This compresses margin unless efficacy is proven.

Price Transparency and Digital Procurement

Digital procurement platforms raised price transparency in medtech: 2024 Vizient data shows 60% of US hospitals use e-procurement, enabling easier cost comparisons and tighter vendor scrutiny.

Buyers now use benchmarking to flag price gaps, driving tougher negotiations—Stryker saw hospital contract pressure contribute to a 0.8 percentage-point margin compression in 2024.

Stryker must keep innovating product differentiation—unique features, bundled services, or outcomes data—to justify premiums in a market where list prices are widely visible.

- 60% US hospitals on e-procurement (Vizient, 2024)

- 0.8 pp margin hit tied to contract pressure (Stryker, 2024 results)

- Differentiate via outcomes data, services, bundles

Budgetary Constraints in Public Health

Government-funded hospitals face tight budgets and push Stryker hard on price; in 2024 OECD health spending averaged 9.2% of GDP, tightening procurement choices in many markets.

Where single-payer systems prevail—Canada, UK, Sweden—the state acts as sole buyer, giving customers exceptional bargaining power and driving centralized tendering and volume discounts.

Stryker adapts via tiered pricing, value-based contracting, and local manufacturing; in 2023 the company reported 7% international organic sales growth, reflecting pricing and market mix moves.

- Public buyers more price-sensitive

- Single-payer = high bargaining power

- Stryker uses tiered pricing, contracts, local sourcing

- OECD health spend 9.2% GDP (2024)

Buyer Power, Value-Based Contracts & E‑procurement Squeeze Stryker Margins

Large US IDNs and GPOs (≈60% acute spend; GPOs cover ~70% purchases) give customers strong leverage, forcing Stryker into deeper discounts, outcome-linked deals, and margin pressure (≈0.8 pp in 2024).

Value-based procurement (≈35% Medicare tied to value in 2024) and e-procurement (60% hospitals) raise transparency, so Stryker must use outcomes data, bundles, and tiered pricing to retain share.

| Metric | Value |

|---|---|

| IDN share of acute spend | ≈60% |

| GPO coverage of purchases | ≈70% |

| E-procurement adoption (US hospitals, 2024) | 60% |

| Medicare value-based payments (2024) | ≈35% |

| Stryker margin impact (2024) | −0.8 pp |

What You See Is What You Get

Stryker Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Stryker you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're looking at the actual, final file; once you complete your purchase, you’ll get instant access to this same document. No mockups or samples—the preview is the deliverable.