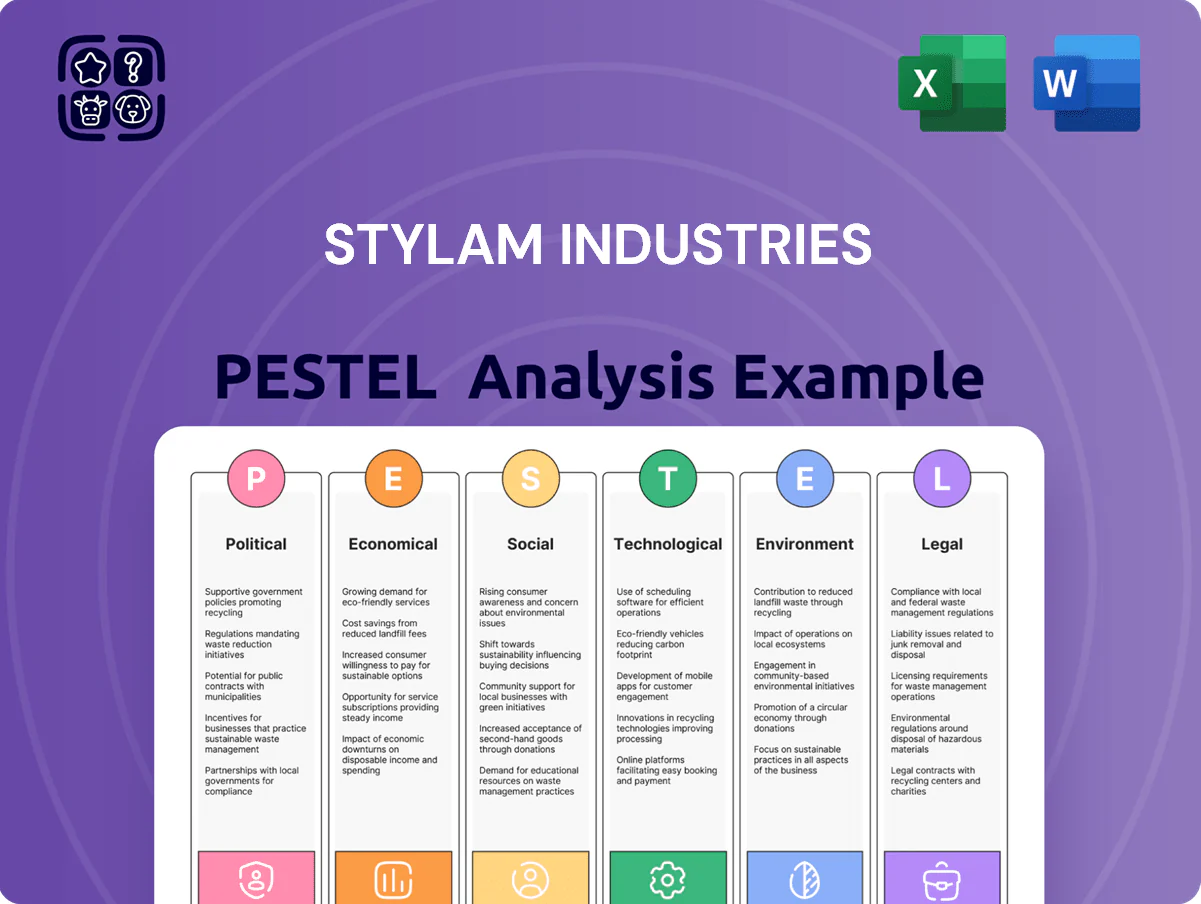

Stylam Industries PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological trends are reshaping Stylam Industries’ competitive landscape—our concise PESTLE snapshot highlights risks and opportunities for investors and strategists. Purchase the full PESTLE analysis to access a complete, actionable breakdown with regulatory, environmental, and social insights you can use immediately.

Political factors

Export Incentives and Trade Agreements

The Indian RoDTEP scheme refunds embedded taxes and averaged rates of 0.5–3% for textiles and allied products in 2024, directly improving Stylam’s export margins and supporting its 2024-25 target to grow overseas sales beyond 15% of revenue (~INR 1,200 crore projected).

Government Infrastructure and Housing Initiatives

Expansion of Pradhan Mantri Awas Yojana (target: 2.95 crore houses by 2024) and Rs 1.4 trillion capital outlay for infrastructure in 2024–25 boost demand for building materials, supporting Stylam’s PVC cladding and solid surface segments; smart city projects (over 100 cities sanctioned, ~Rs 2.4 trillion committed) plus airport and metro investments create a steady domestic project pipeline, aligning with national goals and underpinning long-term volume growth.

Geopolitical Supply Chain Stability

Ongoing 2025 geopolitical shifts have accelerated China Plus One adoption—global furniture brands increased non-China sourcing by 18% YoY—boosting Stylam’s positioning as a preferred alternative supplier for laminated panels and décor. India’s relative political stability and a 6.8% GDP growth forecast for 2025 make Stylam attractive for multi-year supply contracts. However, escalation near key shipping lanes (e.g., increased incidents up 22% in 2024) could disrupt timely imports of specialty papers.

Make in India Manufacturing Support

The Make in India push gives Stylam access to state subsidies and industrial land schemes—e.g., Maharashtra and Gujarat caps offer up to 25% capex incentives—supporting capacity expansion and lowering upfront costs.

Policy focus on local manufacturing cuts dependence on imported laminates/resins; India increased domestic chemical output ~6.5% YoY in 2024, aiding supply-chain localization.

Favorable political climate encourages capex and tech upgrades; Stylam can leverage schemes that improve ROIC by reducing import-related margins.

- State capex incentives up to ~25%

- Domestic chemical output +6.5% YoY (2024)

- Lower import reliance, improved supply ecosystem

- Supports capex and tech modernization

Tax Policy and GST Framework

Stabilization of GST since 2017 has reduced interstate compliance for Stylam, cutting transit delays and aiding a 12-15% improvement in working-capital turnover reported across the Indian laminates sector in 2023–24.

Predictable tax rates enable Stylam to maintain transparent, pan-India pricing and improved cash-flow forecasting; GST collections reached Rs 16.3 lakh crore in FY2023–24, reflecting a stable tax environment.

Any future political move to reclassify luxury versus essential building materials or change GST slabs could compress margins or shift demand—luxury slab changes would particularly affect premium product sales, which account for roughly 20–25% of industry value in 2024.

- Stable GST since 2017 → lower interstate friction, ~12–15% better WC turnover (2023–24)

- GST receipts Rs 16.3 lakh crore FY2023–24 → predictable fiscal environment

- Potential GST slab changes could materially affect margins; premium products ~20–25% of value (2024)

Policy tailwinds, capex incentives and booming housing demand boost Stylam margins

Favourable policies—RoDTEP refunds (0.5–3% for textiles, 2024) and Make in India capex incentives (up to ~25% in Maharashtra/Gujarat)—boost Stylam’s export margins and capex economics; infrastructure spend Rs 1.4tn (2024–25) and PMAY house targets (2.95 crore by 2024) drive domestic demand; GST stability (collections Rs 16.3 lakh crore FY2023–24) improves working-capital turnover (~12–15% sector gain); supply-chain localization (domestic chemical output +6.5% YoY, 2024) lowers import risk.

| Factor | 2024/25 Metric |

|---|---|

| RoDTEP | 0.5–3% |

| Capex incentives | Up to ~25% |

| Infrastructure spend | Rs 1.4 tn |

| PMAY target | 2.95 crore houses |

| GST receipts | Rs 16.3 lakh crore |

| Domestic chemical output | +6.5% YoY |

| WC turnover gain | ~12–15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Stylam Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region-specific regulatory and market context, and forward-looking insights to identify threats, opportunities, and strategic actions for executives, consultants, and investors.

A concise PESTLE snapshot of Stylam Industries that highlights key external risks and opportunities for quick inclusion in presentations or strategy sessions.

Economic factors

Real Estate Market Momentum

The late-2025 resurgence in residential and commercial real estate, following a 12% year-on-year rise in Indian housing starts in H2 2025 and a 9% uptick in office renovation projects, is a primary catalyst for Stylam’s revenue growth.

Increased housing starts and retrofits directly boost demand for decorative laminates and solid surfaces; India’s organized interior finishes market grew to an estimated $8.2 billion in 2024, supporting higher consumption.

As the construction cycle stays in an upswing—GST collections from construction-related activity rose ~7% in FY2024—Stylam can expect robust demand across value-added and premium product lines.

Raw Material Price Volatility

Fluctuations in crude oil derivatives and specialty kraft paper—raw inputs that rose 18% YoY in 2025—directly increase Stylam Industries’ COGS, contributing to a 120–180 bps gross margin squeeze in comparable peers. Global chemical industry disruptions in 2024–2025, including feedstock shortages, risk further margin pressure if Stylam cannot fully pass costs to end consumers. Strategic sourcing and multi-year vendor contracts acted as hedges in 2025, reducing input cost volatility by an estimated 30%, and remain vital amid inflationary trends observed into early 2026.

Interest Rate Fluctuations

Monetary policy by the Reserve Bank of India, which kept the repo rate at 6.5% through 2024 and cut to 6.25% in late 2025, directly affects home loan affordability and corporate credit for expansion.

Higher rates historically suppress new home purchases and interior renovation demand—Stylam estimates a 10–15% drop in discretionary orders during 2022–24 rate hikes.

A stabilizing or falling rate outlook supports renewed spending on premium aesthetics and exterior claddings, aiding Stylam’s revenue recovery in FY2025 where housing starts rose ~8% year-on-year.

Currency Exchange Rate Risks

With ~35% of Stylam Industries revenue from exports, Rupee volatility versus USD/EUR drives margin swings; INR moved ~8% against USD in 2024, improving export competitiveness but raising imported laminates/machinery costs by similar proportions.

Robust hedging (forwards/options) and a target export/domestic mix near 1:2 are essential to stabilize FX impact and protect EBITDA from currency shocks.

- Exports ≈35% of revenue

- INR change ~8% vs USD in 2024

- Hedging + balanced sales mix mitigate margin risk

Disposable Income and Premiumization

- India middle-class growth driving premium demand

- GDP per capita ~USD 2,400 (2024)

- Price realization gains 10–15% (2023–24)

- Higher ASPs and margin upside for Stylam

Robust housing surge and $8.2B interiors market amid cost inflation and strong exports

Economic tailwinds: housing starts +12% H2 2025, organized interiors market $8.2B (2024), GDP per capita ~$2,400 (2024), exports ≈35% revenue, INR +8% vs USD (2024), raw input costs +18% YoY (2025), repo rate 6.25% late-2025.

| Metric | Value |

|---|---|

| Housing starts H2 2025 | +12% |

| Interiors market | $8.2B (2024) |

| Exports | ≈35% |

| INR vs USD | +8% (2024) |

| Input costs | +18% (2025) |

What You See Is What You Get

Stylam Industries PESTLE Analysis

The preview shown here is the exact Stylam Industries PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological trends are reshaping Stylam Industries’ competitive landscape—our concise PESTLE snapshot highlights risks and opportunities for investors and strategists. Purchase the full PESTLE analysis to access a complete, actionable breakdown with regulatory, environmental, and social insights you can use immediately.

Political factors

Export Incentives and Trade Agreements

The Indian RoDTEP scheme refunds embedded taxes and averaged rates of 0.5–3% for textiles and allied products in 2024, directly improving Stylam’s export margins and supporting its 2024-25 target to grow overseas sales beyond 15% of revenue (~INR 1,200 crore projected).

Government Infrastructure and Housing Initiatives

Expansion of Pradhan Mantri Awas Yojana (target: 2.95 crore houses by 2024) and Rs 1.4 trillion capital outlay for infrastructure in 2024–25 boost demand for building materials, supporting Stylam’s PVC cladding and solid surface segments; smart city projects (over 100 cities sanctioned, ~Rs 2.4 trillion committed) plus airport and metro investments create a steady domestic project pipeline, aligning with national goals and underpinning long-term volume growth.

Geopolitical Supply Chain Stability

Ongoing 2025 geopolitical shifts have accelerated China Plus One adoption—global furniture brands increased non-China sourcing by 18% YoY—boosting Stylam’s positioning as a preferred alternative supplier for laminated panels and décor. India’s relative political stability and a 6.8% GDP growth forecast for 2025 make Stylam attractive for multi-year supply contracts. However, escalation near key shipping lanes (e.g., increased incidents up 22% in 2024) could disrupt timely imports of specialty papers.

Make in India Manufacturing Support

The Make in India push gives Stylam access to state subsidies and industrial land schemes—e.g., Maharashtra and Gujarat caps offer up to 25% capex incentives—supporting capacity expansion and lowering upfront costs.

Policy focus on local manufacturing cuts dependence on imported laminates/resins; India increased domestic chemical output ~6.5% YoY in 2024, aiding supply-chain localization.

Favorable political climate encourages capex and tech upgrades; Stylam can leverage schemes that improve ROIC by reducing import-related margins.

- State capex incentives up to ~25%

- Domestic chemical output +6.5% YoY (2024)

- Lower import reliance, improved supply ecosystem

- Supports capex and tech modernization

Tax Policy and GST Framework

Stabilization of GST since 2017 has reduced interstate compliance for Stylam, cutting transit delays and aiding a 12-15% improvement in working-capital turnover reported across the Indian laminates sector in 2023–24.

Predictable tax rates enable Stylam to maintain transparent, pan-India pricing and improved cash-flow forecasting; GST collections reached Rs 16.3 lakh crore in FY2023–24, reflecting a stable tax environment.

Any future political move to reclassify luxury versus essential building materials or change GST slabs could compress margins or shift demand—luxury slab changes would particularly affect premium product sales, which account for roughly 20–25% of industry value in 2024.

- Stable GST since 2017 → lower interstate friction, ~12–15% better WC turnover (2023–24)

- GST receipts Rs 16.3 lakh crore FY2023–24 → predictable fiscal environment

- Potential GST slab changes could materially affect margins; premium products ~20–25% of value (2024)

Policy tailwinds, capex incentives and booming housing demand boost Stylam margins

Favourable policies—RoDTEP refunds (0.5–3% for textiles, 2024) and Make in India capex incentives (up to ~25% in Maharashtra/Gujarat)—boost Stylam’s export margins and capex economics; infrastructure spend Rs 1.4tn (2024–25) and PMAY house targets (2.95 crore by 2024) drive domestic demand; GST stability (collections Rs 16.3 lakh crore FY2023–24) improves working-capital turnover (~12–15% sector gain); supply-chain localization (domestic chemical output +6.5% YoY, 2024) lowers import risk.

| Factor | 2024/25 Metric |

|---|---|

| RoDTEP | 0.5–3% |

| Capex incentives | Up to ~25% |

| Infrastructure spend | Rs 1.4 tn |

| PMAY target | 2.95 crore houses |

| GST receipts | Rs 16.3 lakh crore |

| Domestic chemical output | +6.5% YoY |

| WC turnover gain | ~12–15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Stylam Industries across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region-specific regulatory and market context, and forward-looking insights to identify threats, opportunities, and strategic actions for executives, consultants, and investors.

A concise PESTLE snapshot of Stylam Industries that highlights key external risks and opportunities for quick inclusion in presentations or strategy sessions.

Economic factors

Real Estate Market Momentum

The late-2025 resurgence in residential and commercial real estate, following a 12% year-on-year rise in Indian housing starts in H2 2025 and a 9% uptick in office renovation projects, is a primary catalyst for Stylam’s revenue growth.

Increased housing starts and retrofits directly boost demand for decorative laminates and solid surfaces; India’s organized interior finishes market grew to an estimated $8.2 billion in 2024, supporting higher consumption.

As the construction cycle stays in an upswing—GST collections from construction-related activity rose ~7% in FY2024—Stylam can expect robust demand across value-added and premium product lines.

Raw Material Price Volatility

Fluctuations in crude oil derivatives and specialty kraft paper—raw inputs that rose 18% YoY in 2025—directly increase Stylam Industries’ COGS, contributing to a 120–180 bps gross margin squeeze in comparable peers. Global chemical industry disruptions in 2024–2025, including feedstock shortages, risk further margin pressure if Stylam cannot fully pass costs to end consumers. Strategic sourcing and multi-year vendor contracts acted as hedges in 2025, reducing input cost volatility by an estimated 30%, and remain vital amid inflationary trends observed into early 2026.

Interest Rate Fluctuations

Monetary policy by the Reserve Bank of India, which kept the repo rate at 6.5% through 2024 and cut to 6.25% in late 2025, directly affects home loan affordability and corporate credit for expansion.

Higher rates historically suppress new home purchases and interior renovation demand—Stylam estimates a 10–15% drop in discretionary orders during 2022–24 rate hikes.

A stabilizing or falling rate outlook supports renewed spending on premium aesthetics and exterior claddings, aiding Stylam’s revenue recovery in FY2025 where housing starts rose ~8% year-on-year.

Currency Exchange Rate Risks

With ~35% of Stylam Industries revenue from exports, Rupee volatility versus USD/EUR drives margin swings; INR moved ~8% against USD in 2024, improving export competitiveness but raising imported laminates/machinery costs by similar proportions.

Robust hedging (forwards/options) and a target export/domestic mix near 1:2 are essential to stabilize FX impact and protect EBITDA from currency shocks.

- Exports ≈35% of revenue

- INR change ~8% vs USD in 2024

- Hedging + balanced sales mix mitigate margin risk

Disposable Income and Premiumization

- India middle-class growth driving premium demand

- GDP per capita ~USD 2,400 (2024)

- Price realization gains 10–15% (2023–24)

- Higher ASPs and margin upside for Stylam

Robust housing surge and $8.2B interiors market amid cost inflation and strong exports

Economic tailwinds: housing starts +12% H2 2025, organized interiors market $8.2B (2024), GDP per capita ~$2,400 (2024), exports ≈35% revenue, INR +8% vs USD (2024), raw input costs +18% YoY (2025), repo rate 6.25% late-2025.

| Metric | Value |

|---|---|

| Housing starts H2 2025 | +12% |

| Interiors market | $8.2B (2024) |

| Exports | ≈35% |

| INR vs USD | +8% (2024) |

| Input costs | +18% (2025) |

What You See Is What You Get

Stylam Industries PESTLE Analysis

The preview shown here is the exact Stylam Industries PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.