Subsea 7 Porter's Five Forces Analysis

Don't Miss the Bigger Picture

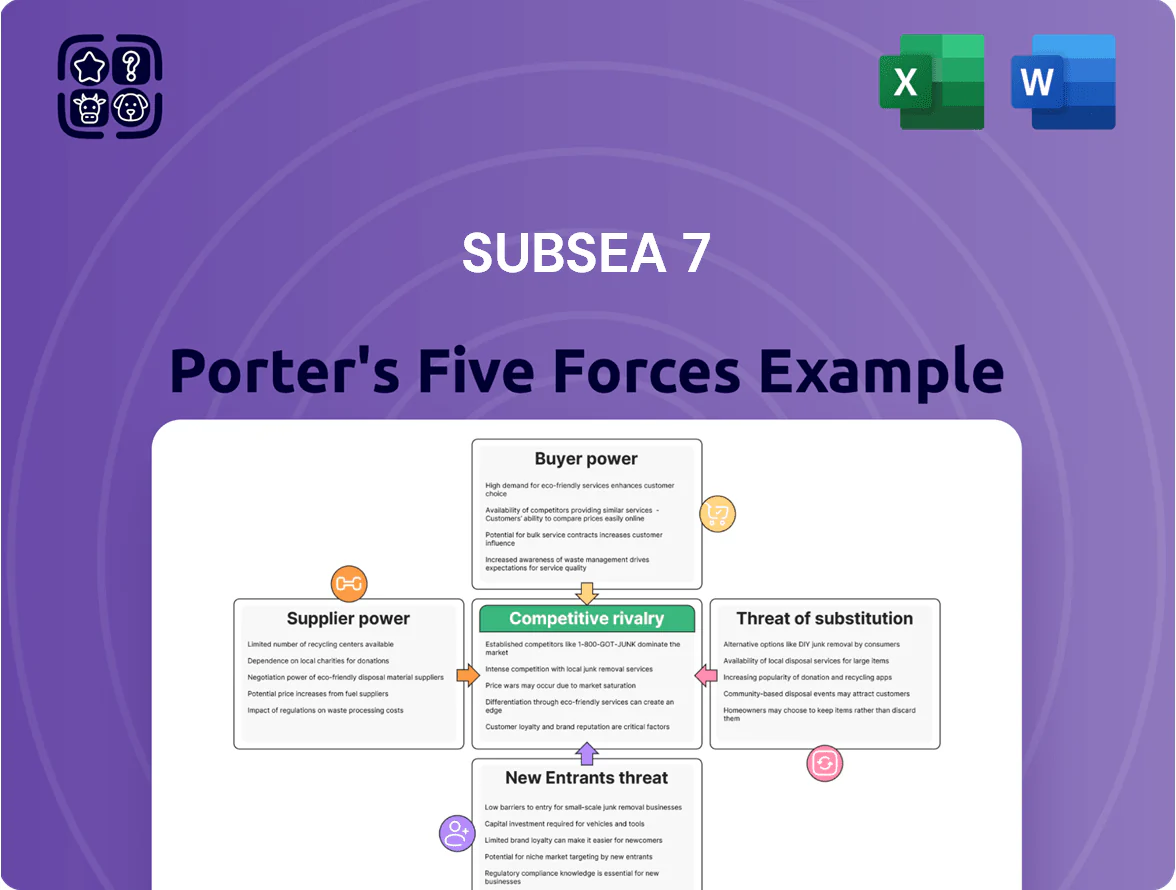

Subsea 7 navigates a landscape shaped by intense rivalry, significant buyer power, and the ever-present threat of new entrants. Understanding these forces is crucial for any stakeholder in the offshore energy sector.

The complete report reveals the real forces shaping Subsea 7’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Specialized Equipment and Vessel Suppliers

Subsea 7's operations are critically dependent on a narrow pool of suppliers providing highly specialized vessels, advanced subsea equipment, and intricate components essential for complex offshore projects. The limited number of entities capable of manufacturing and supplying these technically demanding and capital-intensive assets inherently grants these suppliers substantial bargaining power.

This supplier leverage is amplified by the constrained subsea vessel market observed throughout 2024 and extending into 2025. With demand for these specialized assets consistently outstripping available supply, suppliers are in a strong position to dictate terms, driving up costs for Subsea 7 and impacting project profitability.

Highly Skilled Labor and Expertise

The bargaining power of suppliers, particularly those providing highly skilled labor and specialized expertise, is a significant factor for Subsea 7. Access to a niche workforce, encompassing subsea engineers, project managers, and offshore specialists accustomed to challenging environments, is paramount for successful project execution. The limited availability of this talent pool inherently grants these professionals considerable leverage, influencing compensation packages and retention strategies.

In 2024, the global demand for specialized subsea talent remained robust, driven by ongoing offshore energy development and renewable energy projects. Companies like Subsea 7, which heavily rely on this expertise, must actively invest in talent acquisition and development to mitigate the impact of this supplier power. Subsea 7's reported commitment to employee development and safety underscores the strategic importance of managing its human capital as a critical resource.

Raw Material and Component Suppliers

Suppliers of essential raw materials, such as specialized steel for subsea pipelines and intricate electronic components for control systems, possess moderate bargaining power. While these materials may be less specialized than the vessels themselves, the critical nature of their quality and timely delivery for Subsea 7's complex projects grants these suppliers leverage. For instance, in 2024, the global steel market experienced price volatility, with benchmark hot-rolled coil prices fluctuating significantly due to production issues and demand shifts, directly impacting the cost of pipeline materials.

This power is amplified when there are few qualified vendors for specific, high-grade materials or when global supply chains face disruptions. Subsea 7's reliance on long-term, high-value projects necessitates a stable and predictable supply chain. Any interruption or significant price increase from these suppliers can directly impact project timelines and profitability, giving them a stronger hand in negotiations.

Technology and Software Providers

The bargaining power of technology and software providers in the subsea sector is significant, driven by the industry's growing dependence on advanced digital solutions. Companies like Subsea 7 are actively integrating AI, autonomous systems, and sophisticated software to enhance operational efficiency and safety. For instance, specialized software for subsea engineering, data analytics, and remote monitoring often represents unique capabilities that are not easily replicated, giving these suppliers considerable leverage. In 2024, the demand for such digital transformation tools in the offshore energy market continued to surge, with Subsea 7 itself investing heavily in these areas as part of its strategic focus on digitalization.

Suppliers of proprietary subsea technology and specialized software hold sway due to the critical and often unique functions they provide. These can range from advanced subsea robotics and control systems to complex simulation and project management platforms. The ability of these providers to offer solutions that directly impact project timelines, cost-effectiveness, and risk mitigation in complex offshore environments grants them substantial bargaining power. Subsea 7's strategic imperative to leverage digitalization means that securing and maintaining access to cutting-edge technological partnerships is paramount, further amplifying the influence of these key suppliers.

The increasing reliance on digital twins, predictive maintenance algorithms, and AI-driven operational optimization in the offshore energy sector underscores the bargaining power of technology and software providers. These firms often possess intellectual property and expertise that are difficult for companies like Subsea 7 to develop internally. For example, the market for subsea autonomous inspection and intervention systems saw significant growth in 2024, with specialized software being a key differentiator. This reliance on external innovation for competitive advantage positions these tech suppliers favorably in negotiations.

- High demand for specialized subsea software: The offshore energy sector's push for efficiency and safety in 2024 amplified the need for advanced engineering, project management, and remote operation software.

- Proprietary technology as a differentiator: Suppliers offering unique subsea robotics, control systems, and data analytics platforms leverage their exclusive capabilities to negotiate favorable terms.

- Digitalization strategy dependence: Subsea 7's commitment to digitalization means its ability to adopt new technologies is tied to the offerings and pricing of key software and technology providers.

- Intellectual property and expertise: The value of unique algorithms, AI solutions, and specialized engineering tools creates a strong bargaining position for technology suppliers.

Logistics and Specialized Services

Subsea 7's reliance on specialized logistics and support services, beyond just equipment, significantly impacts supplier bargaining power. These services, crucial for operations in demanding offshore settings, often involve niche expertise and high-risk execution, giving suppliers leverage. For instance, companies providing specialized subsea welding or remotely operated vehicle (ROV) support in deepwater fields can command premium pricing due to the limited availability of qualified providers and the critical nature of their contributions to project success.

The unique demands of subsea construction mean that suppliers offering critical maintenance, repair, and specialized personnel often hold substantial sway. Their ability to ensure operational continuity and safety in remote or hazardous locations is paramount, allowing them to negotiate favorable terms. For example, a supplier of highly specialized diving support or underwater inspection services might have considerable power if they possess unique certifications or a proven track record in extreme environments, which are difficult for Subsea 7 to replicate internally or source elsewhere.

- Specialized Services: Subsea 7 relies on suppliers for niche capabilities like deepwater ROV operations, subsea welding, and specialized vessel crewing.

- Geographic Concentration: In remote offshore regions, the pool of qualified service providers can be small, increasing supplier bargaining power.

- Safety and Risk: The high-risk nature of subsea work means suppliers with impeccable safety records and specialized risk mitigation expertise are highly valued, enabling them to charge more.

- Operational Continuity: Downtime in subsea projects is extremely costly, giving suppliers of essential maintenance and repair services significant leverage.

Supplier Bargaining Power in Offshore Operations

The bargaining power of suppliers for Subsea 7 is considerable, stemming from the highly specialized nature of the equipment, vessels, and skilled labor required for offshore projects. This concentration of expertise and capital-intensive assets in the hands of a few providers allows them to command higher prices and dictate terms. For instance, the limited availability of advanced subsea construction vessels in 2024, coupled with robust demand from offshore energy and renewable projects, significantly strengthened the negotiating position of vessel owners.

Furthermore, the critical reliance on proprietary technology and specialized software for operational efficiency and safety amplifies supplier leverage. Companies developing unique subsea robotics, data analytics platforms, or AI-driven solutions often hold intellectual property that is difficult for clients like Subsea 7 to replicate. This dependence, particularly as Subsea 7 pursues its digitalization strategy, grants these technology providers substantial influence over pricing and access.

The scarcity of highly skilled subsea personnel, including engineers and specialized technicians, also contributes to supplier power. In 2024, the global demand for such talent remained high, driven by both traditional energy and emerging offshore wind developments. Subsea 7's need for these specialized skills means that labor providers or individual contractors with in-demand expertise are in a strong position to negotiate favorable compensation and working conditions.

| Supplier Category | Key Factors Influencing Bargaining Power | Impact on Subsea 7 | 2024/2025 Trend |

| Specialized Vessels & Equipment | Limited number of manufacturers/owners; High capital investment | Increased charter rates and equipment costs; Potential project delays due to availability | High demand, tight supply, driving up costs |

| Skilled Labor & Expertise | Niche skill sets; High demand across industries | Higher labor costs; Challenges in talent acquisition and retention | Robust demand, wage inflation |

| Proprietary Technology & Software | Unique capabilities; Intellectual property protection | Licensing fees; Dependence on specific vendors for critical functions | Growing demand for digital solutions, increasing vendor influence |

| Raw Materials (e.g., Steel) | Market volatility; Criticality of quality and timely delivery | Fluctuating material costs; Supply chain disruption risks | Price volatility observed in 2024, impacting project budgets |

What is included in the product

This Porter's Five Forces analysis for Subsea 7 dissects the competitive intensity within the subsea engineering and construction sector, examining buyer and supplier power, the threat of new entrants and substitutes, and the rivalry among existing players.

Instantly identify and mitigate competitive threats with a dynamic Porter's Five Forces analysis, tailored for Subsea 7's complex market landscape.

Customers Bargaining Power

Large, Concentrated Client Base

Subsea 7's bargaining power of customers is significantly influenced by its large, concentrated client base. Its primary customers are major international and national oil and gas companies, alongside substantial offshore wind developers. These entities are typically large, financially robust organizations with extensive project portfolios.

The concentrated nature of these clients means they possess considerable leverage. This allows them to exert significant influence over contract terms, pricing structures, and the precise specifications of projects they commission. For instance, in 2023, the top five oil and gas supermajors accounted for a substantial portion of global upstream capital expenditure, highlighting their market dominance and, consequently, their buying power.

Long-Term Project Engagement

The nature of offshore energy projects, particularly those involving deepwater and intricate SURF (Subsea Umbilicals, Risers, and Flowlines) installations, inherently leads to long-term engagements, often stretching across several years. This extended timeframe and the need for specialized, integrated solutions mean customers frequently look for enduring partnerships.

Subsea 7's consistent multi-year contracts, such as its ongoing work with Equinor, exemplify this trend. These long-term commitments allow clients to negotiate more favorable terms and conditions over the entire duration of the project, solidifying their bargaining power.

Project Scale and Strategic Importance

Subsea 7's customers, often major energy companies, engage in strategically vital projects like deepwater oil and gas or large-scale offshore wind farms. These EPCI contracts, frequently valued in the hundreds of millions or even billions of dollars, give clients significant leverage due to the project's critical nature to their operations and strategic objectives.

The immense scale and paramount importance of these offshore energy infrastructure projects mean clients demand exceptional performance, rigorous cost controls, and a clear allocation of project risks. This inherent client involvement translates directly into a strong bargaining position for customers when negotiating terms with Subsea 7.

Access to Alternative Providers

Even though the subsea Engineering, Procurement, Construction, and Installation (EPCI) market generally presents significant hurdles for new entrants, major clients often have established relationships with a select few other global offshore service providers, like Allseas or DeepOcean. This limited pool of highly competent alternatives means customers can request competitive proposals, thereby enhancing their negotiation leverage.

Subsea 7's robust order backlog, which stood at approximately $10.2 billion as of the first quarter of 2024, suggests strong demand for its specialized services. However, the presence of capable competitors means that while demand is high, customers can still exert pressure by seeking bids from these other established players.

- Limited but Capable Competitors: Major clients can leverage relationships with a few key global offshore service firms like Allseas and DeepOcean.

- Competitive Bidding: The ability to solicit bids from these providers increases customer bargaining power.

- Strong Demand vs. Leverage: Subsea 7's substantial backlog (around $10.2 billion in Q1 2024) indicates high demand, yet customer leverage remains a factor.

Commodity Price Volatility

Commodity price volatility significantly impacts Subsea 7's customer base, primarily oil and gas companies. When crude oil and natural gas prices are low, these customers often reduce their capital expenditures. This reduction can lead them to defer or cancel projects, or demand lower prices for Subsea 7's services, thereby amplifying their bargaining power.

Despite this sensitivity, the nature of deepwater projects offers some insulation against short-term price swings. These projects typically have long lead times, meaning that decisions made during periods of higher prices often proceed even if prices subsequently decline. For example, in 2024, the Brent crude oil price averaged around $83 per barrel, showing a degree of stability, but the potential for sharp declines remains a constant consideration for Subsea 7's clients.

- Customer Cost Sensitivity: Oil and gas companies' investment decisions are directly tied to oil and gas prices, impacting Subsea 7's project pipeline.

- Project Deferrals: Low commodity prices in 2024 could prompt customers to postpone or cancel offshore projects, increasing pressure on service providers.

- Deepwater Resilience: Long development cycles for deepwater fields mean that even with price volatility, committed projects are likely to continue.

- Negotiating Leverage: Reduced customer spending power during price downturns translates to stronger customer demands for lower service costs from Subsea 7.

Customer Leverage Shapes Subsea Project Dynamics

Subsea 7's customers, primarily major oil and gas firms and offshore wind developers, wield significant bargaining power due to their concentrated nature and the substantial value of the projects they commission. These clients, often multinational corporations, can leverage their financial clout and the critical importance of these large-scale EPCI contracts, which can run into hundreds of millions or billions of dollars, to negotiate favorable terms and pricing. Their ability to solicit bids from a limited pool of highly capable competitors, such as Allseas and DeepOcean, further amplifies their negotiation leverage.

The bargaining power of Subsea 7's customers is also influenced by commodity price volatility. When oil and gas prices are low, these clients often reduce capital expenditures, leading them to defer projects or demand lower prices for Subsea 7's services, thus increasing their leverage. For instance, while Brent crude averaged around $83 per barrel in 2024, potential price declines can prompt customers to exert greater pressure on service providers for cost reductions.

| Customer Type | Bargaining Power Drivers | Example Impact |

|---|---|---|

| Major Oil & Gas Companies | Concentrated client base, large project value, commodity price sensitivity | Can demand lower pricing during periods of low oil prices, potentially deferring projects. |

| Offshore Wind Developers | Long-term project engagements, strategic importance of projects | Seek stable, long-term partnerships with favorable terms due to project scale. |

Full Version Awaits

Subsea 7 Porter's Five Forces Analysis

This preview showcases the complete Subsea 7 Porter's Five Forces Analysis, offering a detailed examination of industry rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes. The document you see here is precisely what you will receive immediately after purchase, ensuring no discrepancies or missing information. You're looking at the actual, professionally formatted analysis, ready for your immediate use and strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Subsea 7 navigates a landscape shaped by intense rivalry, significant buyer power, and the ever-present threat of new entrants. Understanding these forces is crucial for any stakeholder in the offshore energy sector.

The complete report reveals the real forces shaping Subsea 7’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Specialized Equipment and Vessel Suppliers

Subsea 7's operations are critically dependent on a narrow pool of suppliers providing highly specialized vessels, advanced subsea equipment, and intricate components essential for complex offshore projects. The limited number of entities capable of manufacturing and supplying these technically demanding and capital-intensive assets inherently grants these suppliers substantial bargaining power.

This supplier leverage is amplified by the constrained subsea vessel market observed throughout 2024 and extending into 2025. With demand for these specialized assets consistently outstripping available supply, suppliers are in a strong position to dictate terms, driving up costs for Subsea 7 and impacting project profitability.

Highly Skilled Labor and Expertise

The bargaining power of suppliers, particularly those providing highly skilled labor and specialized expertise, is a significant factor for Subsea 7. Access to a niche workforce, encompassing subsea engineers, project managers, and offshore specialists accustomed to challenging environments, is paramount for successful project execution. The limited availability of this talent pool inherently grants these professionals considerable leverage, influencing compensation packages and retention strategies.

In 2024, the global demand for specialized subsea talent remained robust, driven by ongoing offshore energy development and renewable energy projects. Companies like Subsea 7, which heavily rely on this expertise, must actively invest in talent acquisition and development to mitigate the impact of this supplier power. Subsea 7's reported commitment to employee development and safety underscores the strategic importance of managing its human capital as a critical resource.

Raw Material and Component Suppliers

Suppliers of essential raw materials, such as specialized steel for subsea pipelines and intricate electronic components for control systems, possess moderate bargaining power. While these materials may be less specialized than the vessels themselves, the critical nature of their quality and timely delivery for Subsea 7's complex projects grants these suppliers leverage. For instance, in 2024, the global steel market experienced price volatility, with benchmark hot-rolled coil prices fluctuating significantly due to production issues and demand shifts, directly impacting the cost of pipeline materials.

This power is amplified when there are few qualified vendors for specific, high-grade materials or when global supply chains face disruptions. Subsea 7's reliance on long-term, high-value projects necessitates a stable and predictable supply chain. Any interruption or significant price increase from these suppliers can directly impact project timelines and profitability, giving them a stronger hand in negotiations.

Technology and Software Providers

The bargaining power of technology and software providers in the subsea sector is significant, driven by the industry's growing dependence on advanced digital solutions. Companies like Subsea 7 are actively integrating AI, autonomous systems, and sophisticated software to enhance operational efficiency and safety. For instance, specialized software for subsea engineering, data analytics, and remote monitoring often represents unique capabilities that are not easily replicated, giving these suppliers considerable leverage. In 2024, the demand for such digital transformation tools in the offshore energy market continued to surge, with Subsea 7 itself investing heavily in these areas as part of its strategic focus on digitalization.

Suppliers of proprietary subsea technology and specialized software hold sway due to the critical and often unique functions they provide. These can range from advanced subsea robotics and control systems to complex simulation and project management platforms. The ability of these providers to offer solutions that directly impact project timelines, cost-effectiveness, and risk mitigation in complex offshore environments grants them substantial bargaining power. Subsea 7's strategic imperative to leverage digitalization means that securing and maintaining access to cutting-edge technological partnerships is paramount, further amplifying the influence of these key suppliers.

The increasing reliance on digital twins, predictive maintenance algorithms, and AI-driven operational optimization in the offshore energy sector underscores the bargaining power of technology and software providers. These firms often possess intellectual property and expertise that are difficult for companies like Subsea 7 to develop internally. For example, the market for subsea autonomous inspection and intervention systems saw significant growth in 2024, with specialized software being a key differentiator. This reliance on external innovation for competitive advantage positions these tech suppliers favorably in negotiations.

- High demand for specialized subsea software: The offshore energy sector's push for efficiency and safety in 2024 amplified the need for advanced engineering, project management, and remote operation software.

- Proprietary technology as a differentiator: Suppliers offering unique subsea robotics, control systems, and data analytics platforms leverage their exclusive capabilities to negotiate favorable terms.

- Digitalization strategy dependence: Subsea 7's commitment to digitalization means its ability to adopt new technologies is tied to the offerings and pricing of key software and technology providers.

- Intellectual property and expertise: The value of unique algorithms, AI solutions, and specialized engineering tools creates a strong bargaining position for technology suppliers.

Logistics and Specialized Services

Subsea 7's reliance on specialized logistics and support services, beyond just equipment, significantly impacts supplier bargaining power. These services, crucial for operations in demanding offshore settings, often involve niche expertise and high-risk execution, giving suppliers leverage. For instance, companies providing specialized subsea welding or remotely operated vehicle (ROV) support in deepwater fields can command premium pricing due to the limited availability of qualified providers and the critical nature of their contributions to project success.

The unique demands of subsea construction mean that suppliers offering critical maintenance, repair, and specialized personnel often hold substantial sway. Their ability to ensure operational continuity and safety in remote or hazardous locations is paramount, allowing them to negotiate favorable terms. For example, a supplier of highly specialized diving support or underwater inspection services might have considerable power if they possess unique certifications or a proven track record in extreme environments, which are difficult for Subsea 7 to replicate internally or source elsewhere.

- Specialized Services: Subsea 7 relies on suppliers for niche capabilities like deepwater ROV operations, subsea welding, and specialized vessel crewing.

- Geographic Concentration: In remote offshore regions, the pool of qualified service providers can be small, increasing supplier bargaining power.

- Safety and Risk: The high-risk nature of subsea work means suppliers with impeccable safety records and specialized risk mitigation expertise are highly valued, enabling them to charge more.

- Operational Continuity: Downtime in subsea projects is extremely costly, giving suppliers of essential maintenance and repair services significant leverage.

Supplier Bargaining Power in Offshore Operations

The bargaining power of suppliers for Subsea 7 is considerable, stemming from the highly specialized nature of the equipment, vessels, and skilled labor required for offshore projects. This concentration of expertise and capital-intensive assets in the hands of a few providers allows them to command higher prices and dictate terms. For instance, the limited availability of advanced subsea construction vessels in 2024, coupled with robust demand from offshore energy and renewable projects, significantly strengthened the negotiating position of vessel owners.

Furthermore, the critical reliance on proprietary technology and specialized software for operational efficiency and safety amplifies supplier leverage. Companies developing unique subsea robotics, data analytics platforms, or AI-driven solutions often hold intellectual property that is difficult for clients like Subsea 7 to replicate. This dependence, particularly as Subsea 7 pursues its digitalization strategy, grants these technology providers substantial influence over pricing and access.

The scarcity of highly skilled subsea personnel, including engineers and specialized technicians, also contributes to supplier power. In 2024, the global demand for such talent remained high, driven by both traditional energy and emerging offshore wind developments. Subsea 7's need for these specialized skills means that labor providers or individual contractors with in-demand expertise are in a strong position to negotiate favorable compensation and working conditions.

| Supplier Category | Key Factors Influencing Bargaining Power | Impact on Subsea 7 | 2024/2025 Trend |

| Specialized Vessels & Equipment | Limited number of manufacturers/owners; High capital investment | Increased charter rates and equipment costs; Potential project delays due to availability | High demand, tight supply, driving up costs |

| Skilled Labor & Expertise | Niche skill sets; High demand across industries | Higher labor costs; Challenges in talent acquisition and retention | Robust demand, wage inflation |

| Proprietary Technology & Software | Unique capabilities; Intellectual property protection | Licensing fees; Dependence on specific vendors for critical functions | Growing demand for digital solutions, increasing vendor influence |

| Raw Materials (e.g., Steel) | Market volatility; Criticality of quality and timely delivery | Fluctuating material costs; Supply chain disruption risks | Price volatility observed in 2024, impacting project budgets |

What is included in the product

This Porter's Five Forces analysis for Subsea 7 dissects the competitive intensity within the subsea engineering and construction sector, examining buyer and supplier power, the threat of new entrants and substitutes, and the rivalry among existing players.

Instantly identify and mitigate competitive threats with a dynamic Porter's Five Forces analysis, tailored for Subsea 7's complex market landscape.

Customers Bargaining Power

Large, Concentrated Client Base

Subsea 7's bargaining power of customers is significantly influenced by its large, concentrated client base. Its primary customers are major international and national oil and gas companies, alongside substantial offshore wind developers. These entities are typically large, financially robust organizations with extensive project portfolios.

The concentrated nature of these clients means they possess considerable leverage. This allows them to exert significant influence over contract terms, pricing structures, and the precise specifications of projects they commission. For instance, in 2023, the top five oil and gas supermajors accounted for a substantial portion of global upstream capital expenditure, highlighting their market dominance and, consequently, their buying power.

Long-Term Project Engagement

The nature of offshore energy projects, particularly those involving deepwater and intricate SURF (Subsea Umbilicals, Risers, and Flowlines) installations, inherently leads to long-term engagements, often stretching across several years. This extended timeframe and the need for specialized, integrated solutions mean customers frequently look for enduring partnerships.

Subsea 7's consistent multi-year contracts, such as its ongoing work with Equinor, exemplify this trend. These long-term commitments allow clients to negotiate more favorable terms and conditions over the entire duration of the project, solidifying their bargaining power.

Project Scale and Strategic Importance

Subsea 7's customers, often major energy companies, engage in strategically vital projects like deepwater oil and gas or large-scale offshore wind farms. These EPCI contracts, frequently valued in the hundreds of millions or even billions of dollars, give clients significant leverage due to the project's critical nature to their operations and strategic objectives.

The immense scale and paramount importance of these offshore energy infrastructure projects mean clients demand exceptional performance, rigorous cost controls, and a clear allocation of project risks. This inherent client involvement translates directly into a strong bargaining position for customers when negotiating terms with Subsea 7.

Access to Alternative Providers

Even though the subsea Engineering, Procurement, Construction, and Installation (EPCI) market generally presents significant hurdles for new entrants, major clients often have established relationships with a select few other global offshore service providers, like Allseas or DeepOcean. This limited pool of highly competent alternatives means customers can request competitive proposals, thereby enhancing their negotiation leverage.

Subsea 7's robust order backlog, which stood at approximately $10.2 billion as of the first quarter of 2024, suggests strong demand for its specialized services. However, the presence of capable competitors means that while demand is high, customers can still exert pressure by seeking bids from these other established players.

- Limited but Capable Competitors: Major clients can leverage relationships with a few key global offshore service firms like Allseas and DeepOcean.

- Competitive Bidding: The ability to solicit bids from these providers increases customer bargaining power.

- Strong Demand vs. Leverage: Subsea 7's substantial backlog (around $10.2 billion in Q1 2024) indicates high demand, yet customer leverage remains a factor.

Commodity Price Volatility

Commodity price volatility significantly impacts Subsea 7's customer base, primarily oil and gas companies. When crude oil and natural gas prices are low, these customers often reduce their capital expenditures. This reduction can lead them to defer or cancel projects, or demand lower prices for Subsea 7's services, thereby amplifying their bargaining power.

Despite this sensitivity, the nature of deepwater projects offers some insulation against short-term price swings. These projects typically have long lead times, meaning that decisions made during periods of higher prices often proceed even if prices subsequently decline. For example, in 2024, the Brent crude oil price averaged around $83 per barrel, showing a degree of stability, but the potential for sharp declines remains a constant consideration for Subsea 7's clients.

- Customer Cost Sensitivity: Oil and gas companies' investment decisions are directly tied to oil and gas prices, impacting Subsea 7's project pipeline.

- Project Deferrals: Low commodity prices in 2024 could prompt customers to postpone or cancel offshore projects, increasing pressure on service providers.

- Deepwater Resilience: Long development cycles for deepwater fields mean that even with price volatility, committed projects are likely to continue.

- Negotiating Leverage: Reduced customer spending power during price downturns translates to stronger customer demands for lower service costs from Subsea 7.

Customer Leverage Shapes Subsea Project Dynamics

Subsea 7's customers, primarily major oil and gas firms and offshore wind developers, wield significant bargaining power due to their concentrated nature and the substantial value of the projects they commission. These clients, often multinational corporations, can leverage their financial clout and the critical importance of these large-scale EPCI contracts, which can run into hundreds of millions or billions of dollars, to negotiate favorable terms and pricing. Their ability to solicit bids from a limited pool of highly capable competitors, such as Allseas and DeepOcean, further amplifies their negotiation leverage.

The bargaining power of Subsea 7's customers is also influenced by commodity price volatility. When oil and gas prices are low, these clients often reduce capital expenditures, leading them to defer projects or demand lower prices for Subsea 7's services, thus increasing their leverage. For instance, while Brent crude averaged around $83 per barrel in 2024, potential price declines can prompt customers to exert greater pressure on service providers for cost reductions.

| Customer Type | Bargaining Power Drivers | Example Impact |

|---|---|---|

| Major Oil & Gas Companies | Concentrated client base, large project value, commodity price sensitivity | Can demand lower pricing during periods of low oil prices, potentially deferring projects. |

| Offshore Wind Developers | Long-term project engagements, strategic importance of projects | Seek stable, long-term partnerships with favorable terms due to project scale. |

Full Version Awaits

Subsea 7 Porter's Five Forces Analysis

This preview showcases the complete Subsea 7 Porter's Five Forces Analysis, offering a detailed examination of industry rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes. The document you see here is precisely what you will receive immediately after purchase, ensuring no discrepancies or missing information. You're looking at the actual, professionally formatted analysis, ready for your immediate use and strategic decision-making.