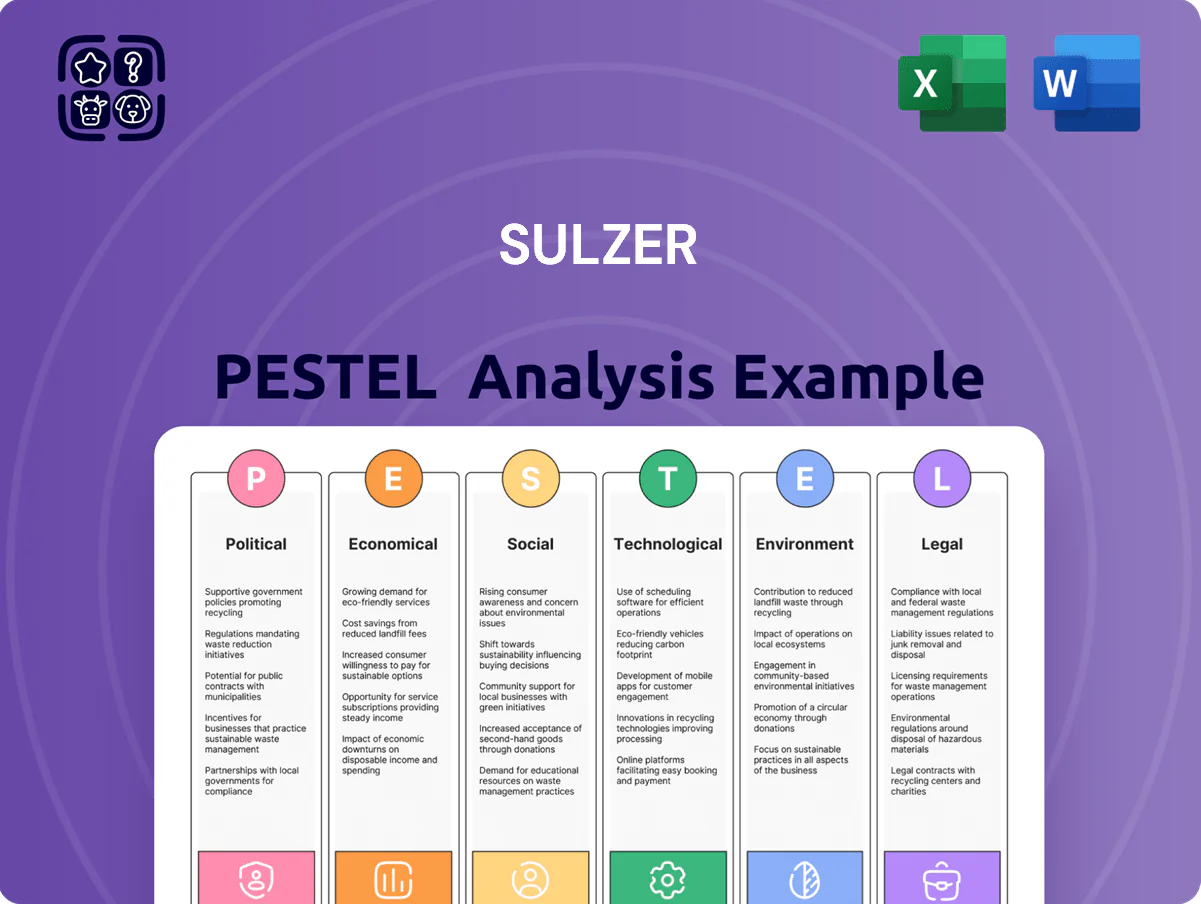

Sulzer PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological innovation are reshaping Sulzer’s outlook in our concise PESTLE summary—ideal for investors and strategists seeking a rapid edge. Purchase the full PESTLE analysis to access detailed, actionable insights on regulatory risks, environmental trends, and market opportunities—formatted for instant use in reports and presentations.

Political factors

Geopolitical instability and trade barriers

Sulzer operates in over 150 countries, so shifting geopolitical alliances and rising protectionism—notably US-China tariffs and EU trade frictions—risk disrupting its global operations and client deliveries.

Trade barriers and sanctions can raise costs for key inputs; for example, 2024 global supply-chain disruptions pushed industrial raw material prices up ~8–12%, squeezing margins for engineering firms like Sulzer.

The company must continuously manage regulatory changes, tariff exposure and localized sourcing to protect 2024 revenue of CHF 3.0bn and preserve timely delivery of fluid-engineering solutions.

Energy security and diversification mandates

Governments are prioritizing energy security and diversification after 2022–24 shocks, driving demand for Sulzer’s pumps and rotating equipment across fossil and renewable sectors; EU energy investments reached €300+ billion in 2024 and US infrastructure spending allocated $65 billion to energy resilience in 2023–24.

Political mandates for energy independence create multi-year pipelines, especially in Europe and North America where €150–200 billion of modernization projects were announced in 2024, benefiting Sulzer’s order backlog and aftermarket services.

Alignment with national energy policies is critical for winning large government-backed contracts; Sulzer’s 2024 revenue of CHF 3.4 billion and CHF 600 million order intake from energy-related projects underscore its exposure and opportunity.

Industrial policy and green subsidies

US Inflation Reduction Act and EU Green Deal Industrial Plan expand subsidies—IRAs clean energy tax credits worth up to $369bn through 2031 and EU’s Net-Zero Industry Act targets scaling key technologies—boost Sulzer’s carbon capture and sustainable separation demand, aligning with divisions contributing roughly 18–22% of group revenues in recent years.

Sulzer must locate manufacturing to capture local incentives and tax credits—US investment tax credits and EU grants can lower capex by 10–30%, affecting site choice for recent €50–100m project pipelines.

Political backing for decarbonization drives Sulzer’s R&D spend, which rose to about 1.8% of sales (~CHF 60–80m annually), positioning the firm to commercialize subsidized green technologies.

Sanctions and export control compliance

- 18% revenue exposure to high-risk markets (2024)

- 50+ jurisdictions monitored

- 12% increase in compliance costs (2024)

- Rapid policy shifts require agile market strategies

Government infrastructure investment programs

Public spending on water management is a key revenue driver for Sulzer’s Flow Equipment; global water infrastructure spending rose to about USD 650 billion in 2024, with OECD estimates of USD 1.7 trillion required by 2030—supporting demand for large pumps and treatment tech.

Massive national infrastructure bills (EU Recovery, US Bipartisan Infrastructure Law) boost multi-year orders; Sulzer’s order intake in water-related projects grew ~12% in 2024.

Political commitment to climate resilience directly affects procurement cycles; maintaining strong public-sector relationships is essential for securing long-term contracts and project pipelines.

- Public spend = major Flow Equipment demand

- Global water capex ~USD 650B (2024)

- EU/US bills drive multi-year orders

- 2024 water-related order intake +12%

- Public-sector relationships critical

Sulzer faces supply‑chain political risk as green subsidies drive multi‑year demand

Political risks: trade barriers, sanctions and shifting alliances threaten Sulzer’s global supply chains and 2024 revenue (CHF 3.4bn); energy/security policies and EU/US stimulus (€300bn EU energy 2024; $65bn US 2023–24) create multi‑year demand; IRAs and EU green subsidies (up to $369bn thru 2031) boost clean-tech orders; 18% revenue from high‑risk markets raises compliance costs (+12% in 2024).

| Metric | Value |

|---|---|

| 2024 revenue | CHF 3.4bn |

| High‑risk market exposure | 18% |

| Compliance cost change (2024) | +12% |

| EU energy spend (2024) | €300bn+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sulzer across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify risks and opportunities.

Condenses Sulzer's full PESTLE into a succinct, shareable brief that teams can drop into presentations or planning decks for fast alignment on external risks and market positioning.

Economic factors

Global interest rate fluctuations and capital expenditure

The prevailing interest rate environment heavily influences capital expenditure by Sulzer’s industrial and energy customers; after global policy rates peaked in 2023–24 (Fed funds ~5.25–5.50%, ECB refi ~4%), high borrowing costs curtailed large infrastructure projects and dented Sulzer’s new equipment order book by mid-2024.

As central banks signalled easing into 2025—market-implied US rate cuts of ~75–100bps by end-2025—demand for industrial expansion and modernization is rebounding, supporting order recovery.

Sulzer must monitor central bank guidance and yield curves to forecast demand cycles and hedge/manage its own debt costs, noting its reported net debt of CHF ~300–400m range (2024) impacts financing flexibility.

Currency exchange rate volatility

As a Swiss-based industrial technology group, Sulzer faces significant exposure to CHF/USD, CHF/EUR and CHF/CNY swings; in 2024 a 5% CHF appreciation vs EUR would have cut reported EUR revenues by roughly the same magnitude for its Euro-heavy sales mix.

Currency moves affect export competitiveness and the translation of foreign profits—about 40% of Sulzer’s 2024 sales were generated outside Switzerland, magnifying translation risk.

Sulzer uses forward contracts and options as part of disciplined hedging; management reported hedges covering a material portion of 12-month FX exposures to stabilize margins and protect quarterly earnings.

Energy price volatility and industrial demand

Fluctuations in global oil and gas prices influence profitability and capex of Sulzer’s energy customers; Brent averaged about 85 USD/bbl in 2024, supporting higher E&P spending that lifts demand for Sulzer’s pumps and rotating equipment. High prices spur exploration and maintenance activity, while extreme volatility—price swings of >40% in 2024—can prompt project delays and contract renegotiations. Sulzer mitigates exposure by expanding water and general industry sales, which accounted for roughly 55% of 2024 order intake, reducing reliance on fossil-fuel markets.

Inflationary pressures on raw materials

The cost of raw materials such as steel, nickel and specialized alloys—accounting for a material share of Sulzer’s manufacturing costs—rose markedly in 2021–2022 and remained elevated into 2024, pressuring margins when price pass-through is limited.

Sulzer pursues operational excellence and supply‑chain optimization, including long‑term contracts and inventory hedging, while relying on commodity market forecasts to inform procurement and multi-year financial planning.

- Raw material inflation elevated COGS percentage in 2022–24

- Pricing escalators needed to protect margins

- Hedging, long-term sourcing and efficiency lower exposure

- Commodity forecasting integral to procurement and planning

Growth trajectories in emerging markets

Growth in emerging markets, notably Southeast Asia and sub-Saharan Africa, offers Sulzer expansion potential as those regions target 4–6% GDP growth (ASEAN avg ~4.5% 2024; Africa ~3.5% 2024) and invest in industrialization, urban water infrastructure and power generation.

Sulzer’s pumps and turbomachinery align with rising capex—EM infrastructure spending projected to rise by $200–300bn annually through 2025—supporting long-term revenue targets, but macro volatility and slower growth could hinder international gains.

- ASEAN GDP ~4.5% (2024)

- Africa GDP ~3.5% (2024)

- EM infrastructure capex +$200–300bn/yr to 2025

- Economic instability = downside risk to Sulzer growth

Sulzer: 2025 rate cuts boost orders; CHF350m net debt constrains capex, FX risk persists

Interest-rate cuts priced for 2025 (US ~75–100bps) support order recovery after 2023–24 tightening; Sulzer net debt ~CHF350m (2024) limits capex flexibility. FX risk: ~40% revenues outside CH, 5% CHF rise ≈ 5% reported EUR revenue hit; hedges cover ~12‑month exposures. Brent avg USD85/bbl (2024) boosts energy demand; raw-material inflation kept COGS elevated 2022–24.

| Metric | 2024 |

|---|---|

| Net debt (CHF) | ~350m |

| Brent (USD/bbl avg) | 85 |

| Revenues outside CH | ~40% |

| ASEAN GDP | ~4.5% |

Same Document Delivered

Sulzer PESTLE Analysis

The preview shown here is the exact Sulzer PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological innovation are reshaping Sulzer’s outlook in our concise PESTLE summary—ideal for investors and strategists seeking a rapid edge. Purchase the full PESTLE analysis to access detailed, actionable insights on regulatory risks, environmental trends, and market opportunities—formatted for instant use in reports and presentations.

Political factors

Geopolitical instability and trade barriers

Sulzer operates in over 150 countries, so shifting geopolitical alliances and rising protectionism—notably US-China tariffs and EU trade frictions—risk disrupting its global operations and client deliveries.

Trade barriers and sanctions can raise costs for key inputs; for example, 2024 global supply-chain disruptions pushed industrial raw material prices up ~8–12%, squeezing margins for engineering firms like Sulzer.

The company must continuously manage regulatory changes, tariff exposure and localized sourcing to protect 2024 revenue of CHF 3.0bn and preserve timely delivery of fluid-engineering solutions.

Energy security and diversification mandates

Governments are prioritizing energy security and diversification after 2022–24 shocks, driving demand for Sulzer’s pumps and rotating equipment across fossil and renewable sectors; EU energy investments reached €300+ billion in 2024 and US infrastructure spending allocated $65 billion to energy resilience in 2023–24.

Political mandates for energy independence create multi-year pipelines, especially in Europe and North America where €150–200 billion of modernization projects were announced in 2024, benefiting Sulzer’s order backlog and aftermarket services.

Alignment with national energy policies is critical for winning large government-backed contracts; Sulzer’s 2024 revenue of CHF 3.4 billion and CHF 600 million order intake from energy-related projects underscore its exposure and opportunity.

Industrial policy and green subsidies

US Inflation Reduction Act and EU Green Deal Industrial Plan expand subsidies—IRAs clean energy tax credits worth up to $369bn through 2031 and EU’s Net-Zero Industry Act targets scaling key technologies—boost Sulzer’s carbon capture and sustainable separation demand, aligning with divisions contributing roughly 18–22% of group revenues in recent years.

Sulzer must locate manufacturing to capture local incentives and tax credits—US investment tax credits and EU grants can lower capex by 10–30%, affecting site choice for recent €50–100m project pipelines.

Political backing for decarbonization drives Sulzer’s R&D spend, which rose to about 1.8% of sales (~CHF 60–80m annually), positioning the firm to commercialize subsidized green technologies.

Sanctions and export control compliance

- 18% revenue exposure to high-risk markets (2024)

- 50+ jurisdictions monitored

- 12% increase in compliance costs (2024)

- Rapid policy shifts require agile market strategies

Government infrastructure investment programs

Public spending on water management is a key revenue driver for Sulzer’s Flow Equipment; global water infrastructure spending rose to about USD 650 billion in 2024, with OECD estimates of USD 1.7 trillion required by 2030—supporting demand for large pumps and treatment tech.

Massive national infrastructure bills (EU Recovery, US Bipartisan Infrastructure Law) boost multi-year orders; Sulzer’s order intake in water-related projects grew ~12% in 2024.

Political commitment to climate resilience directly affects procurement cycles; maintaining strong public-sector relationships is essential for securing long-term contracts and project pipelines.

- Public spend = major Flow Equipment demand

- Global water capex ~USD 650B (2024)

- EU/US bills drive multi-year orders

- 2024 water-related order intake +12%

- Public-sector relationships critical

Sulzer faces supply‑chain political risk as green subsidies drive multi‑year demand

Political risks: trade barriers, sanctions and shifting alliances threaten Sulzer’s global supply chains and 2024 revenue (CHF 3.4bn); energy/security policies and EU/US stimulus (€300bn EU energy 2024; $65bn US 2023–24) create multi‑year demand; IRAs and EU green subsidies (up to $369bn thru 2031) boost clean-tech orders; 18% revenue from high‑risk markets raises compliance costs (+12% in 2024).

| Metric | Value |

|---|---|

| 2024 revenue | CHF 3.4bn |

| High‑risk market exposure | 18% |

| Compliance cost change (2024) | +12% |

| EU energy spend (2024) | €300bn+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sulzer across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify risks and opportunities.

Condenses Sulzer's full PESTLE into a succinct, shareable brief that teams can drop into presentations or planning decks for fast alignment on external risks and market positioning.

Economic factors

Global interest rate fluctuations and capital expenditure

The prevailing interest rate environment heavily influences capital expenditure by Sulzer’s industrial and energy customers; after global policy rates peaked in 2023–24 (Fed funds ~5.25–5.50%, ECB refi ~4%), high borrowing costs curtailed large infrastructure projects and dented Sulzer’s new equipment order book by mid-2024.

As central banks signalled easing into 2025—market-implied US rate cuts of ~75–100bps by end-2025—demand for industrial expansion and modernization is rebounding, supporting order recovery.

Sulzer must monitor central bank guidance and yield curves to forecast demand cycles and hedge/manage its own debt costs, noting its reported net debt of CHF ~300–400m range (2024) impacts financing flexibility.

Currency exchange rate volatility

As a Swiss-based industrial technology group, Sulzer faces significant exposure to CHF/USD, CHF/EUR and CHF/CNY swings; in 2024 a 5% CHF appreciation vs EUR would have cut reported EUR revenues by roughly the same magnitude for its Euro-heavy sales mix.

Currency moves affect export competitiveness and the translation of foreign profits—about 40% of Sulzer’s 2024 sales were generated outside Switzerland, magnifying translation risk.

Sulzer uses forward contracts and options as part of disciplined hedging; management reported hedges covering a material portion of 12-month FX exposures to stabilize margins and protect quarterly earnings.

Energy price volatility and industrial demand

Fluctuations in global oil and gas prices influence profitability and capex of Sulzer’s energy customers; Brent averaged about 85 USD/bbl in 2024, supporting higher E&P spending that lifts demand for Sulzer’s pumps and rotating equipment. High prices spur exploration and maintenance activity, while extreme volatility—price swings of >40% in 2024—can prompt project delays and contract renegotiations. Sulzer mitigates exposure by expanding water and general industry sales, which accounted for roughly 55% of 2024 order intake, reducing reliance on fossil-fuel markets.

Inflationary pressures on raw materials

The cost of raw materials such as steel, nickel and specialized alloys—accounting for a material share of Sulzer’s manufacturing costs—rose markedly in 2021–2022 and remained elevated into 2024, pressuring margins when price pass-through is limited.

Sulzer pursues operational excellence and supply‑chain optimization, including long‑term contracts and inventory hedging, while relying on commodity market forecasts to inform procurement and multi-year financial planning.

- Raw material inflation elevated COGS percentage in 2022–24

- Pricing escalators needed to protect margins

- Hedging, long-term sourcing and efficiency lower exposure

- Commodity forecasting integral to procurement and planning

Growth trajectories in emerging markets

Growth in emerging markets, notably Southeast Asia and sub-Saharan Africa, offers Sulzer expansion potential as those regions target 4–6% GDP growth (ASEAN avg ~4.5% 2024; Africa ~3.5% 2024) and invest in industrialization, urban water infrastructure and power generation.

Sulzer’s pumps and turbomachinery align with rising capex—EM infrastructure spending projected to rise by $200–300bn annually through 2025—supporting long-term revenue targets, but macro volatility and slower growth could hinder international gains.

- ASEAN GDP ~4.5% (2024)

- Africa GDP ~3.5% (2024)

- EM infrastructure capex +$200–300bn/yr to 2025

- Economic instability = downside risk to Sulzer growth

Sulzer: 2025 rate cuts boost orders; CHF350m net debt constrains capex, FX risk persists

Interest-rate cuts priced for 2025 (US ~75–100bps) support order recovery after 2023–24 tightening; Sulzer net debt ~CHF350m (2024) limits capex flexibility. FX risk: ~40% revenues outside CH, 5% CHF rise ≈ 5% reported EUR revenue hit; hedges cover ~12‑month exposures. Brent avg USD85/bbl (2024) boosts energy demand; raw-material inflation kept COGS elevated 2022–24.

| Metric | 2024 |

|---|---|

| Net debt (CHF) | ~350m |

| Brent (USD/bbl avg) | 85 |

| Revenues outside CH | ~40% |

| ASEAN GDP | ~4.5% |

Same Document Delivered

Sulzer PESTLE Analysis

The preview shown here is the exact Sulzer PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.