Sumitomo Realty Porter's Five Forces Analysis

From Overview to Strategy Blueprint

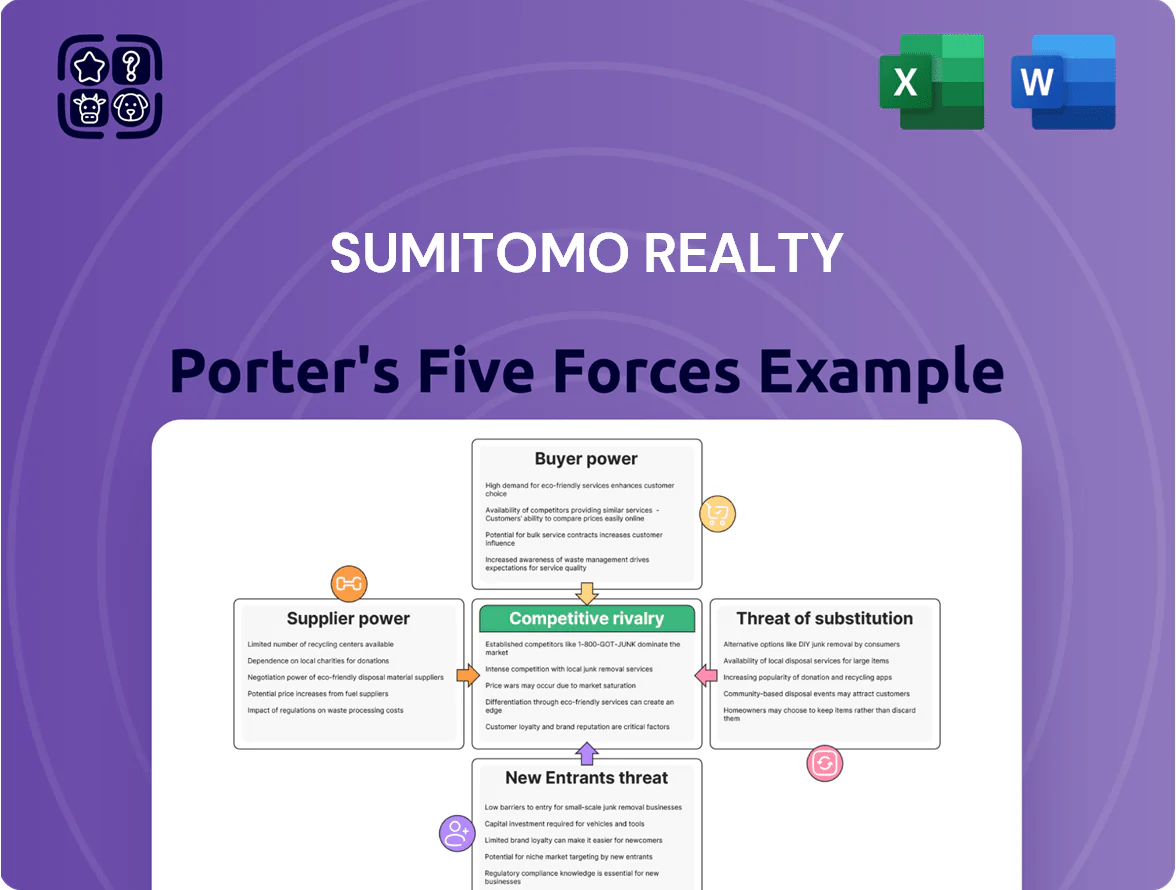

Sumitomo Realty faces mixed pressures: strong buyer negotiation in mature urban markets, moderate supplier influence, high rivalry among diversified developers, and manageable threats from substitutes but potential disruption from alternative real estate models and policy shifts.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sumitomo Realty’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Rising construction and material costs

The bargaining power of suppliers is high as construction material inflation ran near 5–7% annually through 2023–2025, raising input costs for Sumitomo Realty on large urban redevelopments and condo projects.

Sumitomo depends on specialized contractors for complex builds, so supplier leverage translates into margin pressure and scope-linked cost pass-throughs.

With Japan reporting a 2024 construction labor shortfall of roughly 300,000 workers, contractors can command premiums of 5–15% and extend lead times, delaying revenue recognition and increasing financing needs.

Scarcity of prime land in Tokyo

Landowners in central Tokyo—especially Chiyoda, Minato, and Chūō—wield strong leverage because developable plots under 1 ha are scarce; vacancy-adjusted office land supply fell below 5% in 2024, pushing land prices up 12% YoY in prime 5 Wards (MLIT data). Sumitomo Realty often pays premium prices or enters joint ventures to secure flagship sites for its 2024 office portfolio, giving owners power to set price and contract terms.

Dependence on financial institutions

Sumitomo Realty’s strong balance sheet (¥1.9 trillion equity, FY2024) still relies on banks and bond markets because real estate is capital-intensive; around 60% of project funding is debt-backed. As the Bank of Japan began normalizing policy in 2024, lending spreads widened and lenders pushed tighter covenants, lifting average new loan rates by ~80–120 basis points versus 2021. That raises the company’s cost of capital for new developments and for refinancing long-term debt.

Specialized labor and technical expertise

Suppliers of specialized seismic engineering and base-isolation tech hold strong bargaining power because Japan’s building code and Sumitomo Realty’s premium portfolio demand ≤10−6 annual exceedance probabilities in quake resilience and ISO-level quality; only ~30 domestic firms meet these specs, so switching costs and lead times (often 6–12 months) keep prices and contract terms favorable to suppliers.

- ~30 qualified firms nationally

- 6–12 month lead times

- High switching costs, limited alternatives

- Critical for safety and premium branding

Energy and sustainability service providers

Suppliers of green certifications and renewables have stronger bargaining power as ESG mandates push developers to decarbonize by 2026; global corporate net-zero commitments rose to 4,000+ firms by 2024, increasing demand for these services.

Vendors can charge premiums—solar+storage prices rose ~8% in Japan 2023–25—forcing Sumitomo Realty to absorb higher capex to keep premium Tokyo office yields and institutional tenants.

- High demand: 4,000+ corporate net-zero pledges (2024)

- Price pressure: solar+storage cost up ~8% (Japan, 2023–25)

- Impact: raised capex per building, lowers near-term NOI

- Necessity: required to retain institutional lessees

Tokyo construction margins squeezed: inflation, labor shortfall, scarce prime land

Supplier power is high: construction inflation 5–7% (2023–25) and 300k labor shortfall (2024) raise costs; specialized contractors and ~30 seismic-tech firms command 5–15% premiums and 6–12 month lead times; central Tokyo land scarcity cut vacancy <5% (2024) and pushed prime land +12% YoY; ¥1.9T equity (FY2024) but ~60% debt funding, loan spreads +80–120bps since 2021.

| Metric | Value |

|---|---|

| Construction inflation (2023–25) | 5–7% |

| Labor shortfall (Japan, 2024) | ~300,000 |

| Qualified seismic firms | ~30 |

| Prime land price change (5 Wards, 2024) | +12% YoY |

| Equity (Sumitomo FY2024) | ¥1.9 trillion |

| Project debt funding | ~60% |

| Loan spread change vs 2021 | +80–120 bps |

What is included in the product

Tailored Porter's Five Forces analysis for Sumitomo Realty that uncovers competitive intensity, buyer and supplier influence, entry barriers, substitutes, and emerging disruptors to inform strategic positioning and risk mitigation.

Concise Porter's Five Forces snapshot for Sumitomo Realty—instantly highlights competitive pressures and strategic levers to speed decision-making and de-risk investment choices.

Customers Bargaining Power

Consolidation of large corporate tenants

Major corporate tenants in Tokyo lease large blocks—top firms take 20–40% of a building and sign 5–15 year leases—giving them strong bargaining power over Sumitomo Realty, which in 2024 reported Tokyo office occupancy exposure of ~60% to such corporates. These anchors secure discounts of 5–20% per m2 or bespoke fit-out incentives worth millions JPY. A single relocation can spike vacancy by 5–10 percentage points, so Sumitomo actively offers concessions and flexible terms to retain them.

Increased price sensitivity in the residential sector

Individual condominium buyers face record-high prices and rising mortgage rates at end-2025—average Tokyo condo price ~¥85.6M and Japan 10-year mortgage-linked rate up ~120 basis points year-over-year—so price sensitivity rises and buyers push for better amenities, quality, or discounts; Sumitomo Realty must protect its premium brand while confronting a shrinking middle class (household median income ~¥5.2M) that limits willingness to pay.

Availability of market information and transparency

The rise of digital real estate platforms lets commercial and residential buyers compare prices and specs instantly, cutting information asymmetry that once favored big developers like Sumitomo Realty. In Japan, online listings grew ~28% from 2019–2024, and 62% of lessees cite web research as key negotiation leverage in 2024. That transparency strengthens customer bargaining, pressuring lease rates and sales margins downward.

Demand for flexible leasing terms

Post-pandemic work patterns push office tenants toward shorter leases and scale-on-demand; global flexible office demand rose 18% in 2023 and Japan saw flexible workspace supply grow ~12% in 2024.

This shifts bargaining power to customers, forcing Sumitomo Realty to move from long-term rigid contracts—its traditional base of multi-year leases—to offer modular leases and plug-and-play fit-outs to retain top clients.

Failure to adapt risks higher vacancy and revenue volatility; offering flexible terms can protect rent roll and preserve relationships with high-value tenants.

- Flexible office demand +18% (2023)

- Japan flexible supply +12% (2024)

- Risk: higher vacancy, revenue swings

- Action: modular leases, scalable space, turnkey fit-outs

Quality and brand reputation expectations

Discerning customers in luxury residential and Grade-A office segments demand impeccable management and maintenance; failure risks immediate switching to rivals like Mitsui Fudosan or Mitsubishi Estate, which held combined ¥4.2 trillion real estate revenues in FY2024, highlighting competitive pull.

This expectation functions as indirect bargaining power, forcing Sumitomo Realty to invest heavily in service quality—Sumitomo spent ¥62.4 billion on property management and maintenance in FY2024 to retain premium tenants.

- High standards → easy switching to Mitsui/Mitsubishi

- FY2024: Mitsui+Mitsubishi ≈ ¥4.2T revenue

- Sumitomo FY2024 maintenance spend ¥62.4B

Rising tenant power: discounts, web-savvy lessees & flexible-space surge reshape Tokyo market

Customers hold strong bargaining power: large corporate tenants (≈60% exposure in Tokyo, 5–15yr leases) secure 5–20% rent/m2 discounts and fit-out incentives; condo buyers face avg Tokyo price ¥85.6M (2025) and higher rates, raising price sensitivity; digital listings +28% (2019–24) and 62% of lessees use web research (2024) increase transparency; flexible office supply +12% (2024) shifts demands to modular leases.

| Metric | Value |

|---|---|

| Corp tenant exposure (Tokyo) | ≈60% |

| Typical tenant discount | 5–20%/m2 |

| Avg Tokyo condo price (2025) | ¥85.6M |

| Online listings growth (2019–24) | +28% |

| Lessee web research (2024) | 62% |

| Flexible workspace supply (Japan, 2024) | +12% |

Full Version Awaits

Sumitomo Realty Porter's Five Forces Analysis

This preview shows the exact Sumitomo Realty Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, just the full, professionally formatted document.

You're viewing the same final file provided upon download: a ready-to-use strategic assessment covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Sumitomo Realty faces mixed pressures: strong buyer negotiation in mature urban markets, moderate supplier influence, high rivalry among diversified developers, and manageable threats from substitutes but potential disruption from alternative real estate models and policy shifts.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sumitomo Realty’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Rising construction and material costs

The bargaining power of suppliers is high as construction material inflation ran near 5–7% annually through 2023–2025, raising input costs for Sumitomo Realty on large urban redevelopments and condo projects.

Sumitomo depends on specialized contractors for complex builds, so supplier leverage translates into margin pressure and scope-linked cost pass-throughs.

With Japan reporting a 2024 construction labor shortfall of roughly 300,000 workers, contractors can command premiums of 5–15% and extend lead times, delaying revenue recognition and increasing financing needs.

Scarcity of prime land in Tokyo

Landowners in central Tokyo—especially Chiyoda, Minato, and Chūō—wield strong leverage because developable plots under 1 ha are scarce; vacancy-adjusted office land supply fell below 5% in 2024, pushing land prices up 12% YoY in prime 5 Wards (MLIT data). Sumitomo Realty often pays premium prices or enters joint ventures to secure flagship sites for its 2024 office portfolio, giving owners power to set price and contract terms.

Dependence on financial institutions

Sumitomo Realty’s strong balance sheet (¥1.9 trillion equity, FY2024) still relies on banks and bond markets because real estate is capital-intensive; around 60% of project funding is debt-backed. As the Bank of Japan began normalizing policy in 2024, lending spreads widened and lenders pushed tighter covenants, lifting average new loan rates by ~80–120 basis points versus 2021. That raises the company’s cost of capital for new developments and for refinancing long-term debt.

Specialized labor and technical expertise

Suppliers of specialized seismic engineering and base-isolation tech hold strong bargaining power because Japan’s building code and Sumitomo Realty’s premium portfolio demand ≤10−6 annual exceedance probabilities in quake resilience and ISO-level quality; only ~30 domestic firms meet these specs, so switching costs and lead times (often 6–12 months) keep prices and contract terms favorable to suppliers.

- ~30 qualified firms nationally

- 6–12 month lead times

- High switching costs, limited alternatives

- Critical for safety and premium branding

Energy and sustainability service providers

Suppliers of green certifications and renewables have stronger bargaining power as ESG mandates push developers to decarbonize by 2026; global corporate net-zero commitments rose to 4,000+ firms by 2024, increasing demand for these services.

Vendors can charge premiums—solar+storage prices rose ~8% in Japan 2023–25—forcing Sumitomo Realty to absorb higher capex to keep premium Tokyo office yields and institutional tenants.

- High demand: 4,000+ corporate net-zero pledges (2024)

- Price pressure: solar+storage cost up ~8% (Japan, 2023–25)

- Impact: raised capex per building, lowers near-term NOI

- Necessity: required to retain institutional lessees

Tokyo construction margins squeezed: inflation, labor shortfall, scarce prime land

Supplier power is high: construction inflation 5–7% (2023–25) and 300k labor shortfall (2024) raise costs; specialized contractors and ~30 seismic-tech firms command 5–15% premiums and 6–12 month lead times; central Tokyo land scarcity cut vacancy <5% (2024) and pushed prime land +12% YoY; ¥1.9T equity (FY2024) but ~60% debt funding, loan spreads +80–120bps since 2021.

| Metric | Value |

|---|---|

| Construction inflation (2023–25) | 5–7% |

| Labor shortfall (Japan, 2024) | ~300,000 |

| Qualified seismic firms | ~30 |

| Prime land price change (5 Wards, 2024) | +12% YoY |

| Equity (Sumitomo FY2024) | ¥1.9 trillion |

| Project debt funding | ~60% |

| Loan spread change vs 2021 | +80–120 bps |

What is included in the product

Tailored Porter's Five Forces analysis for Sumitomo Realty that uncovers competitive intensity, buyer and supplier influence, entry barriers, substitutes, and emerging disruptors to inform strategic positioning and risk mitigation.

Concise Porter's Five Forces snapshot for Sumitomo Realty—instantly highlights competitive pressures and strategic levers to speed decision-making and de-risk investment choices.

Customers Bargaining Power

Consolidation of large corporate tenants

Major corporate tenants in Tokyo lease large blocks—top firms take 20–40% of a building and sign 5–15 year leases—giving them strong bargaining power over Sumitomo Realty, which in 2024 reported Tokyo office occupancy exposure of ~60% to such corporates. These anchors secure discounts of 5–20% per m2 or bespoke fit-out incentives worth millions JPY. A single relocation can spike vacancy by 5–10 percentage points, so Sumitomo actively offers concessions and flexible terms to retain them.

Increased price sensitivity in the residential sector

Individual condominium buyers face record-high prices and rising mortgage rates at end-2025—average Tokyo condo price ~¥85.6M and Japan 10-year mortgage-linked rate up ~120 basis points year-over-year—so price sensitivity rises and buyers push for better amenities, quality, or discounts; Sumitomo Realty must protect its premium brand while confronting a shrinking middle class (household median income ~¥5.2M) that limits willingness to pay.

Availability of market information and transparency

The rise of digital real estate platforms lets commercial and residential buyers compare prices and specs instantly, cutting information asymmetry that once favored big developers like Sumitomo Realty. In Japan, online listings grew ~28% from 2019–2024, and 62% of lessees cite web research as key negotiation leverage in 2024. That transparency strengthens customer bargaining, pressuring lease rates and sales margins downward.

Demand for flexible leasing terms

Post-pandemic work patterns push office tenants toward shorter leases and scale-on-demand; global flexible office demand rose 18% in 2023 and Japan saw flexible workspace supply grow ~12% in 2024.

This shifts bargaining power to customers, forcing Sumitomo Realty to move from long-term rigid contracts—its traditional base of multi-year leases—to offer modular leases and plug-and-play fit-outs to retain top clients.

Failure to adapt risks higher vacancy and revenue volatility; offering flexible terms can protect rent roll and preserve relationships with high-value tenants.

- Flexible office demand +18% (2023)

- Japan flexible supply +12% (2024)

- Risk: higher vacancy, revenue swings

- Action: modular leases, scalable space, turnkey fit-outs

Quality and brand reputation expectations

Discerning customers in luxury residential and Grade-A office segments demand impeccable management and maintenance; failure risks immediate switching to rivals like Mitsui Fudosan or Mitsubishi Estate, which held combined ¥4.2 trillion real estate revenues in FY2024, highlighting competitive pull.

This expectation functions as indirect bargaining power, forcing Sumitomo Realty to invest heavily in service quality—Sumitomo spent ¥62.4 billion on property management and maintenance in FY2024 to retain premium tenants.

- High standards → easy switching to Mitsui/Mitsubishi

- FY2024: Mitsui+Mitsubishi ≈ ¥4.2T revenue

- Sumitomo FY2024 maintenance spend ¥62.4B

Rising tenant power: discounts, web-savvy lessees & flexible-space surge reshape Tokyo market

Customers hold strong bargaining power: large corporate tenants (≈60% exposure in Tokyo, 5–15yr leases) secure 5–20% rent/m2 discounts and fit-out incentives; condo buyers face avg Tokyo price ¥85.6M (2025) and higher rates, raising price sensitivity; digital listings +28% (2019–24) and 62% of lessees use web research (2024) increase transparency; flexible office supply +12% (2024) shifts demands to modular leases.

| Metric | Value |

|---|---|

| Corp tenant exposure (Tokyo) | ≈60% |

| Typical tenant discount | 5–20%/m2 |

| Avg Tokyo condo price (2025) | ¥85.6M |

| Online listings growth (2019–24) | +28% |

| Lessee web research (2024) | 62% |

| Flexible workspace supply (Japan, 2024) | +12% |

Full Version Awaits

Sumitomo Realty Porter's Five Forces Analysis

This preview shows the exact Sumitomo Realty Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, just the full, professionally formatted document.

You're viewing the same final file provided upon download: a ready-to-use strategic assessment covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry.