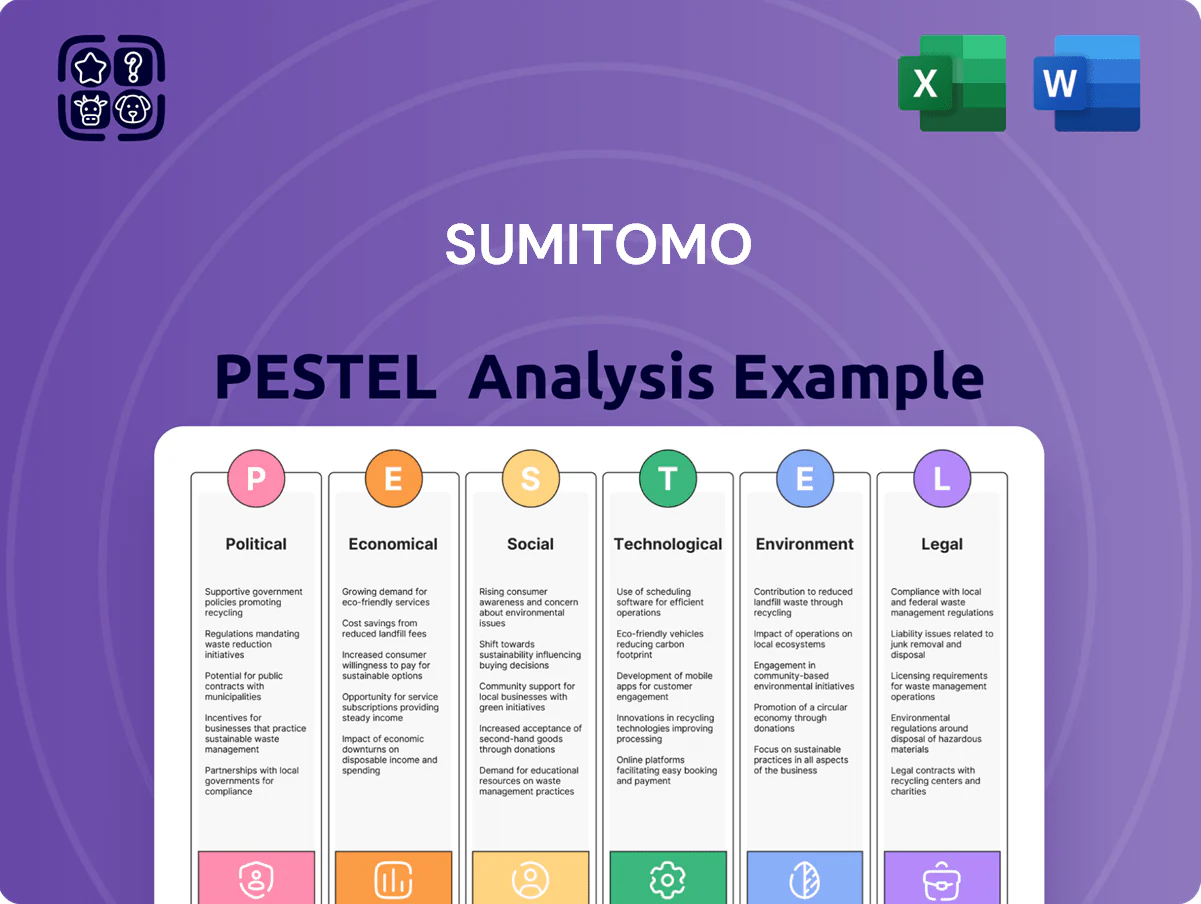

Sumitomo PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological advances are reshaping Sumitomo’s strategic outlook—our concise PESTLE preview highlights key external drivers and risks. Ideal for investors and strategists, the full analysis delivers actionable intelligence, editable charts, and scenario-based implications. Purchase the complete PESTLE now to turn external insights into smarter decisions.

Political factors

Geopolitical Trade Rivalries

The intensifying US-China strategic competition forces Sumitomo to adopt cautious supply chain and asset-allocation strategies, with global trade tensions contributing to a 12% increase in logistics contingency spending across Japanese trading houses in 2024. Sumitomo must navigate shifting alliances and potential sanctions that could affect its roughly $35bn international revenue exposure in FY2024. The company emphasizes flexible logistics networks and dual-sourcing to limit disruption risk from sudden policy changes in key markets.

Energy Security Policies

Governments are boosting energy security—G7 critical minerals strategies target 2030 supply resilience, and Japan earmarked ¥2.4 trillion (2024–2026) for energy security; Sumitomo aligns investments to secure long-term offtake and JV deals with states to access lithium, copper and rare earths.

Regional Stability in Emerging Markets

Political volatility in developing regions where Sumitomo holds major infrastructure and mining stakes—notably in Southeast Asia and Africa, contributing roughly 12% of consolidated revenues in FY2024—remains a key risk for contracts and asset security.

Japanese Economic Diplomacy

As a major trading house, Sumitomo leverages Japanese economic diplomacy—Japan's ODA was ¥1.15 trillion in FY2023—to gain market access and co-finance infrastructure projects, lowering entry barriers in Southeast Asia and Africa.

Alignment with bilateral trade deals and the Japan-ASEAN partnership helps Sumitomo secure large public-private projects; Sumitomo Mitsui Financial Group-backed financing often underwrites these deals.

In 2024 Sumitomo reported overseas revenue of about ¥4.2 trillion, reflecting gains from government-supported contracts.

- Japan ODA FY2023: ¥1.15 trillion

- Sumitomo overseas revenue ~¥4.2 trillion (2024)

- Strong Japan-ASEAN ties enable PPP wins

Global Tax Policy Changes

The OECD/G20 Inclusive Framework's 15% global minimum tax, endorsed by over 140 jurisdictions, tightens Sumitomo's tax planning and could raise effective tax rates on foreign subsidiaries by 2–5 percentage points versus pre-2021 structures.

Maintaining profitability and reputation requires a centralized compliance framework; in 2024 Sumitomo reported increased tax-related governance costs and reassigned treasury roles to its Singapore and London hubs.

Policy shifts prompt re-evaluation of earnings booking and regional hub locations, with scenarios showing potential after-tax profit margin impacts of up to 3% in high-profit jurisdictions.

- 15% global minimum tax: affects subsidiary structuring

- 2–5 pp potential ETR increase vs pre-2021

- Compliance and governance costs rose in 2024

- Hub location choices can shift up to 3% after-tax margins

Sumitomo shifts to dual-sourcing as sanctions, energy funds, and tax risks rise

US-China rivalry and sanctions risk push Sumitomo toward dual-sourcing and flexible logistics, raising contingency logistics spending ~12% in 2024; overseas revenue ~¥4.2tn (2024) heightens exposure. G7/Japan energy security funds (Japan ¥2.4tn 2024–26) drive JV offtake deals for lithium, copper and rare earths. Political instability in SEA/Africa (≈12% revenue) threatens assets; OECD 15% minimum tax may raise ETR 2–5 pp, increasing compliance costs.

| Metric | Value |

|---|---|

| Overseas revenue (2024) | ¥4.2tn |

| Logistics contingency spend increase (2024) | ~12% |

| Japan energy security budget (2024–26) | ¥2.4tn |

| Revenue from SEA/Africa | ~12% |

| Potential ETR rise (OECD 15%) | 2–5 pp |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sumitomo across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trend-driven insights to identify threats, opportunities, and implications for strategy and investment decisions.

A concise, shareable Sumitomo PESTLE summary organized by category to speed meeting prep and support cross-team alignment on external risks and market positioning.

Economic factors

Currency Exchange Volatility

Fluctuations in the Japanese Yen—which swung roughly 10% versus the US dollar between 2023 and 2025—materially affect Sumitomo by altering translated overseas profits; a weaker yen boosted FY2024 reported overseas earnings by an estimated ¥45–60 billion. Sumitomo uses forward contracts, currency swaps and options as part of a sophisticated hedging program that covered about 65% of forecasted FX exposure in 2024. Persistent volatility can erode export price competitiveness or raise import costs across Sumitomo’s diversified global operations, impacting margins in metals, chemicals and machinery segments.

Commodity Price Fluctuations

The Mineral Resources and Energy segments’ profits swing with iron ore, copper and LNG prices; iron ore averaged about 120 USD/t in 2024 and copper near 9,000 USD/t, directly affecting Sumitomo’s FY2024 revenue exposure (commodity-linked revenues >20%) and capital spending capacity. Global GDP growth and China’s industrial demand drive cycle-linked earnings, so Sumitomo offsets volatility by shifting investments into less cyclical sectors such as infrastructure and high-value services.

Global Interest Rate Environments

Changes in global monetary policy, such as the Fed and ECB tightening in 2022–24 that lifted 10-year yields to ~4% in 2024, raise Sumitomo’s cost of capital for large debt-financed infrastructure projects, squeezing margins and increasing financing costs. Higher rates push up hurdle rates for new investments and can reduce NPV on long-term projects. Maintaining a conservative debt-to-equity ratio is critical to preserve its credit rating and access to affordable funding.

Inflationary Pressure on Operations

Rising labor, raw material and logistics costs have pressured Sumitomo’s manufacturing and construction margins; Japan’s CPI rose 3.2% YoY in 2024, while global commodity prices kept input costs elevated.

To protect margins, Sumitomo pursues cost-optimization and supply‑contract renegotiations; procurement savings targets reportedly exceeded ¥40 billion in FY2024.

Persistent inflation can reduce consumer spending, weighing on Sumitomo’s retail and media units—Japan household spending fell 1.5% YoY in 2024.

- Input-cost inflation: Japan CPI +3.2% (2024)

- Procurement savings: >¥40bn target FY2024

- Household spending: -1.5% YoY (2024)

Growth in Emerging Economies

Growth in emerging economies across Asia and Africa drives sustained demand for transportation, telecoms and urban infrastructure; McKinsey estimates infrastructure spending in Asia could reach $3.9 trillion annually by 2030 and Africa’s infrastructure gap is ~$130–170 billion per year (2024 figures).

Sumitomo targets these high-growth regions to offset Japan’s low GDP growth (~0.5% in 2024) by pursuing projects in Southeast Asia and Africa, requiring localized economic analysis and multi-year capital commitments aligned with regional development plans.

- Asia infra spend ~ $3.9T/yr by 2030 (McKinsey 2024)

- Africa infra gap $130–170B/yr (2024)

- Japan GDP growth ~0.5% in 2024

- Requires localized analysis and long-term capital commitment

FX swings, commodity exposure and cost cuts reshape FY24 profits amid weak Japan demand

Exchange volatility (JPY ±10% vs USD 2023–25) shifted FY2024 overseas earnings by ~¥45–60bn; 65% FX hedge coverage in 2024. Commodity exposure: iron ore ~$120/t, copper ~$9,000/t (2024), commodity-linked revenue >20%. Japan CPI +3.2% and household spending -1.5% (2024) pressured margins; procurement savings >¥40bn FY2024. Japan GDP ~0.5% (2024); Asia infra spend ~$3.9T/yr by 2030.

| Metric | 2024 |

|---|---|

| JPY vs USD | ±10% |

| FX hedge | 65% |

| Iron ore | $120/t |

| Copper | $9,000/t |

| Japan CPI | +3.2% |

| Household spend | -1.5% |

| Procurement savings | ¥>40bn |

| Japan GDP | ~0.5% |

Preview Before You Purchase

Sumitomo PESTLE Analysis

The preview shown here is the exact Sumitomo PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the final file you’ll be able to download immediately after buying.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological advances are reshaping Sumitomo’s strategic outlook—our concise PESTLE preview highlights key external drivers and risks. Ideal for investors and strategists, the full analysis delivers actionable intelligence, editable charts, and scenario-based implications. Purchase the complete PESTLE now to turn external insights into smarter decisions.

Political factors

Geopolitical Trade Rivalries

The intensifying US-China strategic competition forces Sumitomo to adopt cautious supply chain and asset-allocation strategies, with global trade tensions contributing to a 12% increase in logistics contingency spending across Japanese trading houses in 2024. Sumitomo must navigate shifting alliances and potential sanctions that could affect its roughly $35bn international revenue exposure in FY2024. The company emphasizes flexible logistics networks and dual-sourcing to limit disruption risk from sudden policy changes in key markets.

Energy Security Policies

Governments are boosting energy security—G7 critical minerals strategies target 2030 supply resilience, and Japan earmarked ¥2.4 trillion (2024–2026) for energy security; Sumitomo aligns investments to secure long-term offtake and JV deals with states to access lithium, copper and rare earths.

Regional Stability in Emerging Markets

Political volatility in developing regions where Sumitomo holds major infrastructure and mining stakes—notably in Southeast Asia and Africa, contributing roughly 12% of consolidated revenues in FY2024—remains a key risk for contracts and asset security.

Japanese Economic Diplomacy

As a major trading house, Sumitomo leverages Japanese economic diplomacy—Japan's ODA was ¥1.15 trillion in FY2023—to gain market access and co-finance infrastructure projects, lowering entry barriers in Southeast Asia and Africa.

Alignment with bilateral trade deals and the Japan-ASEAN partnership helps Sumitomo secure large public-private projects; Sumitomo Mitsui Financial Group-backed financing often underwrites these deals.

In 2024 Sumitomo reported overseas revenue of about ¥4.2 trillion, reflecting gains from government-supported contracts.

- Japan ODA FY2023: ¥1.15 trillion

- Sumitomo overseas revenue ~¥4.2 trillion (2024)

- Strong Japan-ASEAN ties enable PPP wins

Global Tax Policy Changes

The OECD/G20 Inclusive Framework's 15% global minimum tax, endorsed by over 140 jurisdictions, tightens Sumitomo's tax planning and could raise effective tax rates on foreign subsidiaries by 2–5 percentage points versus pre-2021 structures.

Maintaining profitability and reputation requires a centralized compliance framework; in 2024 Sumitomo reported increased tax-related governance costs and reassigned treasury roles to its Singapore and London hubs.

Policy shifts prompt re-evaluation of earnings booking and regional hub locations, with scenarios showing potential after-tax profit margin impacts of up to 3% in high-profit jurisdictions.

- 15% global minimum tax: affects subsidiary structuring

- 2–5 pp potential ETR increase vs pre-2021

- Compliance and governance costs rose in 2024

- Hub location choices can shift up to 3% after-tax margins

Sumitomo shifts to dual-sourcing as sanctions, energy funds, and tax risks rise

US-China rivalry and sanctions risk push Sumitomo toward dual-sourcing and flexible logistics, raising contingency logistics spending ~12% in 2024; overseas revenue ~¥4.2tn (2024) heightens exposure. G7/Japan energy security funds (Japan ¥2.4tn 2024–26) drive JV offtake deals for lithium, copper and rare earths. Political instability in SEA/Africa (≈12% revenue) threatens assets; OECD 15% minimum tax may raise ETR 2–5 pp, increasing compliance costs.

| Metric | Value |

|---|---|

| Overseas revenue (2024) | ¥4.2tn |

| Logistics contingency spend increase (2024) | ~12% |

| Japan energy security budget (2024–26) | ¥2.4tn |

| Revenue from SEA/Africa | ~12% |

| Potential ETR rise (OECD 15%) | 2–5 pp |

What is included in the product

Explores how external macro-environmental factors uniquely affect Sumitomo across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trend-driven insights to identify threats, opportunities, and implications for strategy and investment decisions.

A concise, shareable Sumitomo PESTLE summary organized by category to speed meeting prep and support cross-team alignment on external risks and market positioning.

Economic factors

Currency Exchange Volatility

Fluctuations in the Japanese Yen—which swung roughly 10% versus the US dollar between 2023 and 2025—materially affect Sumitomo by altering translated overseas profits; a weaker yen boosted FY2024 reported overseas earnings by an estimated ¥45–60 billion. Sumitomo uses forward contracts, currency swaps and options as part of a sophisticated hedging program that covered about 65% of forecasted FX exposure in 2024. Persistent volatility can erode export price competitiveness or raise import costs across Sumitomo’s diversified global operations, impacting margins in metals, chemicals and machinery segments.

Commodity Price Fluctuations

The Mineral Resources and Energy segments’ profits swing with iron ore, copper and LNG prices; iron ore averaged about 120 USD/t in 2024 and copper near 9,000 USD/t, directly affecting Sumitomo’s FY2024 revenue exposure (commodity-linked revenues >20%) and capital spending capacity. Global GDP growth and China’s industrial demand drive cycle-linked earnings, so Sumitomo offsets volatility by shifting investments into less cyclical sectors such as infrastructure and high-value services.

Global Interest Rate Environments

Changes in global monetary policy, such as the Fed and ECB tightening in 2022–24 that lifted 10-year yields to ~4% in 2024, raise Sumitomo’s cost of capital for large debt-financed infrastructure projects, squeezing margins and increasing financing costs. Higher rates push up hurdle rates for new investments and can reduce NPV on long-term projects. Maintaining a conservative debt-to-equity ratio is critical to preserve its credit rating and access to affordable funding.

Inflationary Pressure on Operations

Rising labor, raw material and logistics costs have pressured Sumitomo’s manufacturing and construction margins; Japan’s CPI rose 3.2% YoY in 2024, while global commodity prices kept input costs elevated.

To protect margins, Sumitomo pursues cost-optimization and supply‑contract renegotiations; procurement savings targets reportedly exceeded ¥40 billion in FY2024.

Persistent inflation can reduce consumer spending, weighing on Sumitomo’s retail and media units—Japan household spending fell 1.5% YoY in 2024.

- Input-cost inflation: Japan CPI +3.2% (2024)

- Procurement savings: >¥40bn target FY2024

- Household spending: -1.5% YoY (2024)

Growth in Emerging Economies

Growth in emerging economies across Asia and Africa drives sustained demand for transportation, telecoms and urban infrastructure; McKinsey estimates infrastructure spending in Asia could reach $3.9 trillion annually by 2030 and Africa’s infrastructure gap is ~$130–170 billion per year (2024 figures).

Sumitomo targets these high-growth regions to offset Japan’s low GDP growth (~0.5% in 2024) by pursuing projects in Southeast Asia and Africa, requiring localized economic analysis and multi-year capital commitments aligned with regional development plans.

- Asia infra spend ~ $3.9T/yr by 2030 (McKinsey 2024)

- Africa infra gap $130–170B/yr (2024)

- Japan GDP growth ~0.5% in 2024

- Requires localized analysis and long-term capital commitment

FX swings, commodity exposure and cost cuts reshape FY24 profits amid weak Japan demand

Exchange volatility (JPY ±10% vs USD 2023–25) shifted FY2024 overseas earnings by ~¥45–60bn; 65% FX hedge coverage in 2024. Commodity exposure: iron ore ~$120/t, copper ~$9,000/t (2024), commodity-linked revenue >20%. Japan CPI +3.2% and household spending -1.5% (2024) pressured margins; procurement savings >¥40bn FY2024. Japan GDP ~0.5% (2024); Asia infra spend ~$3.9T/yr by 2030.

| Metric | 2024 |

|---|---|

| JPY vs USD | ±10% |

| FX hedge | 65% |

| Iron ore | $120/t |

| Copper | $9,000/t |

| Japan CPI | +3.2% |

| Household spend | -1.5% |

| Procurement savings | ¥>40bn |

| Japan GDP | ~0.5% |

Preview Before You Purchase

Sumitomo PESTLE Analysis

The preview shown here is the exact Sumitomo PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the final file you’ll be able to download immediately after buying.