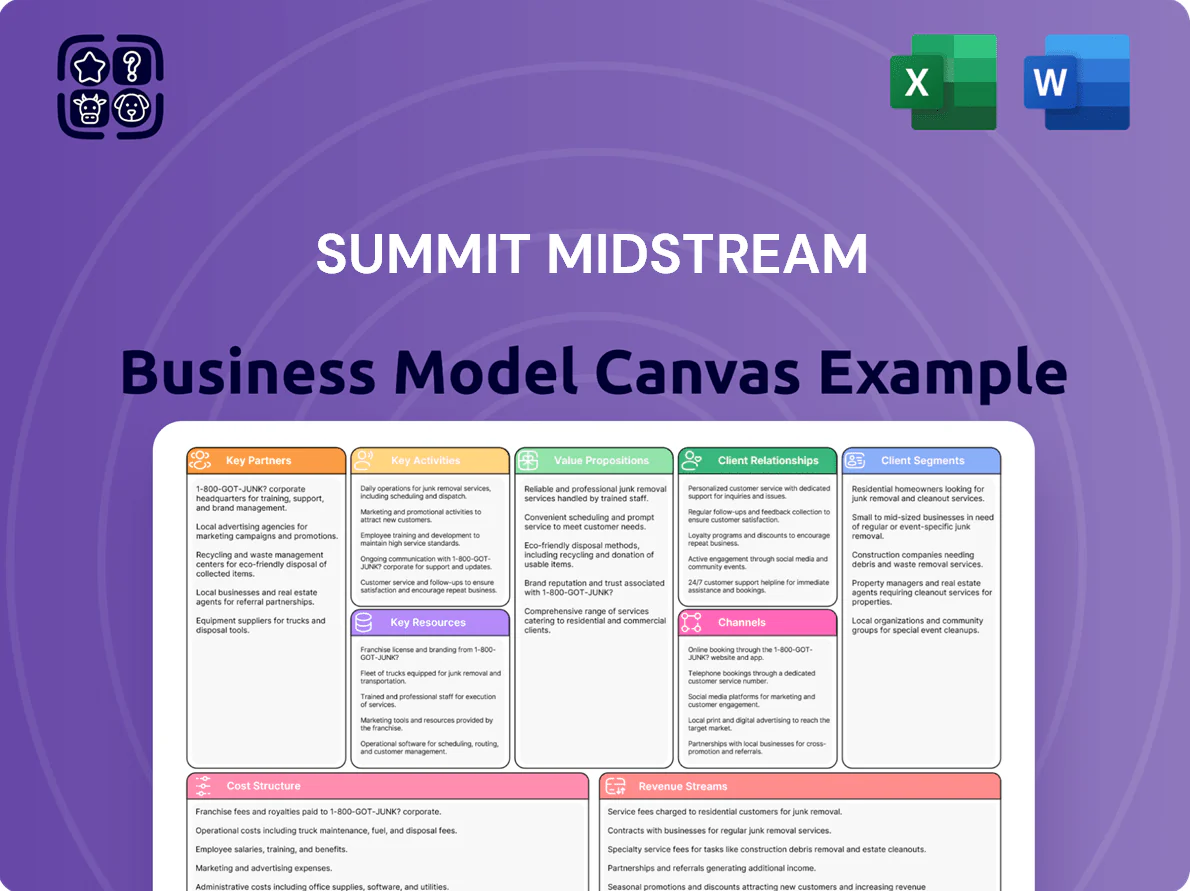

Summit Midstream Business Model Canvas

Summit Midstream Business Model Canvas: Downloadable, Investor-Ready Roadmap

Unlock Summit Midstream’s strategic playbook with our full Business Model Canvas — a concise, sector-specific roadmap showing how the company creates value, scales operations, and monetizes infrastructure; perfect for investors, advisors, and strategists seeking actionable, downloadable insights in Word and Excel to inform decisions and benchmarking.

Partnerships

Upstream Exploration and Production Companies

Summit Midstream depends on long-term contracts with E&P partners who commit ~85% of wellhead volumes, supplying the natural gas, crude oil and produced water that drive throughput; in 2024 Summit reported average gathered volumes of ~1.2 Bcf/d gas and 140 MBbl/d liquids across its systems. By aligning with active drillers in the Permian, Rockies and Northeast—regions that accounted for ~72% of its throughput—Summit secures steady hydrocarbon flows and predictable fee-based revenues.

Joint Venture Infrastructure Partners

Collaborations like the Double E Pipeline joint venture let Summit Midstream split capital expenditures and operational risk—Double E added 300,000 barrels/day takeaway capacity in 2024—cutting Summit’s project capex share by roughly 45% on that build. By late 2025 such joint ventures supply critical takeaway from the Delaware Basin to Gulf Coast and Permian hubs, accounting for an estimated 38% of Summit’s contracted throughput capacity and preserving competitive access to premium markets.

Financial Institutions and Capital Providers

Summit Midstream maintains revolving credit lines and access to debt markets via major commercial banks and institutional investors, supporting ~ $300–500 million of available liquidity as of Q4 2025 for maintenance capex and growth projects.

Regulatory and Environmental Agencies

Summit Midstream must coordinate with federal and state regulators—notably FERC and state environmental boards—to meet safety and emissions rules, file regular reports, pass inspections, and secure permits; in 2024 FERC issued ~1,200 pipeline-related actions and EPA tracked a 6% rise in inspections, so timely compliance cuts shutdown risk and legal costs.

- Regular reporting, inspections, permitting

- FERC ~1,200 pipeline actions (2024)

- EPA inspections +6% (2024)

- Reduces legal risk and downtime

Downstream Pipeline and Market Hub Operators

Interconnect agreements with long-haul pipelines and regional market hubs let Summit Midstream move gathered crude and NGLs to end-users; in 2024 Summit’s throughput-linked contracts covered ~1.2 million barrels/day of takeaway capacity, anchoring revenue and reducing basis risk.

Close coordination with these downstream operators ensures deliveries meet tight quality specs and timing, cutting penalties and supporting midstream fee margins (average tolls ~$0.60–$1.20/barrel in 2024).

- Exit points: long-haul pipelines, regional market hubs

- 2024 takeaway capacity: ~1.2 million b/d

- Typical tolls: $0.60–$1.20 per barrel (2024)

- Focus: quality specs, delivery timing, penalty avoidance

Summit secures 1.2 Bcf/d and 140 MBbl/d with 85% contracts, $300–500M liquidity

Summit relies on long-term E&P contracts (~85% committed volumes) and JV pipelines (Double E added 300,000 b/d in 2024) plus ~$300–500M liquidity to secure throughput (~1.2 Bcf/d gas, 140 MBbl/d liquids in 2024) while meeting FERC/EPA rules to limit downtime and legal costs.

| Metric | 2024–25 |

|---|---|

| Gathered gas | 1.2 Bcf/d |

| Liquids | 140 MBbl/d |

| Contracted commit | ~85% |

| Takeaway added (Double E) | 300,000 b/d (2024) |

| Liquidity | $300–500M (Q4 2025) |

| FERC actions | ~1,200 (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Summit Midstream detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and risk factors, aligned with the company’s real-world midstream operations and strategic plans for investor presentations and internal decision-making.

High-level, editable one-page snapshot of Summit Midstream’s business model that saves hours of formatting while making team collaboration easy and ideal for boardroom reviews or side-by-side company comparisons.

Activities

Gathering and Compression Operations

Summit Midstream physically gathers natural gas and crude from wellheads via ~6,200 miles of low-pressure pipelines across the DJ Basin, Powder River and Williston; its network feeds processing plants and larger lines. Summit runs dozens of compression stations that raise gas pressure to transport volumes—2024 throughput ~1.1 Bcf/d—forming the core of daily field ops and driving ~65% of asset-level EBITDA.

Natural Gas Processing and Treating

Summit Midstream removes water, CO2, and H2S to meet pipeline specs, processing ~2.1 Bcf/d capacity in 2025 and cutting impurity-driven penalties; this ensures safe long-haul transport and compliance with FERC and state regs.

Its cryogenic plants recover NGLs (ethane, propane, butane), producing ~120 Mbpd of NGLs in 2025, boosting realized product value and fee-linked margin per Mcf for midstream contracts.

Produced Water Management

Summit Midstream runs dedicated water gathering systems and Class II disposal wells to collect, treat, and recycle produced water, supporting E&P uptime in water-intensive basins; in 2024 Summit reported handling roughly 45 million barrels of produced water year-to-date across the Permian and Delaware basins. This service reduces truck trips, cuts disposal costs for producers (typical Midland Basin disposal ~2.50–4.00 per barrel in 2024) and helps clients meet growing regulatory and ESG demands.

Infrastructure Engineering and Construction

Summit Midstream continuously plans, designs, and builds pipeline segments and facility expansions—handling land acquisition, environmental surveys, and technical engineering—to optimize flow and support producer growth; efficient project execution drove ~220 MMcf/d of new takeaway capacity added in 2024 and supported a 6% volume growth year-over-year.

- Land deals: dozens in 2024, avg. right-of-way cost $12k/acre

- Added capacity: ~220 MMcf/d in 2024

- Project ROI: typical IRR 12–18% on midstream expansions

Contract Management and Commercial Optimization

Summit actively manages fee-based contracts—including minimum volume commitments and acreage dedications—covering roughly 85% of throughput, with ~5 years weighted-average contract life as of Q4 2025; the commercial team re-contracts expiries and wins nearby producer capacity to lock steady cash flows and hedge commodity volatility.

- ~85% fee-based coverage

- ~5 years WACL (Q4 2025)

- focus: re-contract expiries, capture nearby producers

- reduces revenue sensitivity to commodity swings

Summit Midstream: 6,200 mi, 1.1 Bcf/d throughput, 2.1 Bcf/d processing & 85% fee-based

Summit Midstream gathers and compresses ~1.1 Bcf/d (2024) via 6,200 miles of pipelines, operates processing (2.1 Bcf/d capacity in 2025) and cryogenic NGL recovery (~120 Mbpd NGLs in 2025), handles ~45M barrels produced water (2024), added ~220 MMcf/d takeaway (2024), and maintains ~85% fee-based coverage with ~5-year WACL (Q4 2025).

| Metric | Value |

|---|---|

| Pipelines (miles) | 6,200 |

| Throughput (2024) | 1.1 Bcf/d |

| Processing capacity (2025) | 2.1 Bcf/d |

| NGLs (2025) | 120 Mbpd |

| Produced water (2024) | 45M bbl |

| Added capacity (2024) | 220 MMcf/d |

| Fee-based coverage | 85% |

| WACL (Q4 2025) | ~5 yrs |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Summit Midstream Business Model Canvas—no mockup or sample. Upon purchase, you'll receive this exact file with all sections and content included, ready to edit and present. The deliverable matches the preview in structure and formatting, available for immediate download. What you see here is what you’ll own.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Summit Midstream Business Model Canvas: Downloadable, Investor-Ready Roadmap

Unlock Summit Midstream’s strategic playbook with our full Business Model Canvas — a concise, sector-specific roadmap showing how the company creates value, scales operations, and monetizes infrastructure; perfect for investors, advisors, and strategists seeking actionable, downloadable insights in Word and Excel to inform decisions and benchmarking.

Partnerships

Upstream Exploration and Production Companies

Summit Midstream depends on long-term contracts with E&P partners who commit ~85% of wellhead volumes, supplying the natural gas, crude oil and produced water that drive throughput; in 2024 Summit reported average gathered volumes of ~1.2 Bcf/d gas and 140 MBbl/d liquids across its systems. By aligning with active drillers in the Permian, Rockies and Northeast—regions that accounted for ~72% of its throughput—Summit secures steady hydrocarbon flows and predictable fee-based revenues.

Joint Venture Infrastructure Partners

Collaborations like the Double E Pipeline joint venture let Summit Midstream split capital expenditures and operational risk—Double E added 300,000 barrels/day takeaway capacity in 2024—cutting Summit’s project capex share by roughly 45% on that build. By late 2025 such joint ventures supply critical takeaway from the Delaware Basin to Gulf Coast and Permian hubs, accounting for an estimated 38% of Summit’s contracted throughput capacity and preserving competitive access to premium markets.

Financial Institutions and Capital Providers

Summit Midstream maintains revolving credit lines and access to debt markets via major commercial banks and institutional investors, supporting ~ $300–500 million of available liquidity as of Q4 2025 for maintenance capex and growth projects.

Regulatory and Environmental Agencies

Summit Midstream must coordinate with federal and state regulators—notably FERC and state environmental boards—to meet safety and emissions rules, file regular reports, pass inspections, and secure permits; in 2024 FERC issued ~1,200 pipeline-related actions and EPA tracked a 6% rise in inspections, so timely compliance cuts shutdown risk and legal costs.

- Regular reporting, inspections, permitting

- FERC ~1,200 pipeline actions (2024)

- EPA inspections +6% (2024)

- Reduces legal risk and downtime

Downstream Pipeline and Market Hub Operators

Interconnect agreements with long-haul pipelines and regional market hubs let Summit Midstream move gathered crude and NGLs to end-users; in 2024 Summit’s throughput-linked contracts covered ~1.2 million barrels/day of takeaway capacity, anchoring revenue and reducing basis risk.

Close coordination with these downstream operators ensures deliveries meet tight quality specs and timing, cutting penalties and supporting midstream fee margins (average tolls ~$0.60–$1.20/barrel in 2024).

- Exit points: long-haul pipelines, regional market hubs

- 2024 takeaway capacity: ~1.2 million b/d

- Typical tolls: $0.60–$1.20 per barrel (2024)

- Focus: quality specs, delivery timing, penalty avoidance

Summit secures 1.2 Bcf/d and 140 MBbl/d with 85% contracts, $300–500M liquidity

Summit relies on long-term E&P contracts (~85% committed volumes) and JV pipelines (Double E added 300,000 b/d in 2024) plus ~$300–500M liquidity to secure throughput (~1.2 Bcf/d gas, 140 MBbl/d liquids in 2024) while meeting FERC/EPA rules to limit downtime and legal costs.

| Metric | 2024–25 |

|---|---|

| Gathered gas | 1.2 Bcf/d |

| Liquids | 140 MBbl/d |

| Contracted commit | ~85% |

| Takeaway added (Double E) | 300,000 b/d (2024) |

| Liquidity | $300–500M (Q4 2025) |

| FERC actions | ~1,200 (2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Summit Midstream detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and risk factors, aligned with the company’s real-world midstream operations and strategic plans for investor presentations and internal decision-making.

High-level, editable one-page snapshot of Summit Midstream’s business model that saves hours of formatting while making team collaboration easy and ideal for boardroom reviews or side-by-side company comparisons.

Activities

Gathering and Compression Operations

Summit Midstream physically gathers natural gas and crude from wellheads via ~6,200 miles of low-pressure pipelines across the DJ Basin, Powder River and Williston; its network feeds processing plants and larger lines. Summit runs dozens of compression stations that raise gas pressure to transport volumes—2024 throughput ~1.1 Bcf/d—forming the core of daily field ops and driving ~65% of asset-level EBITDA.

Natural Gas Processing and Treating

Summit Midstream removes water, CO2, and H2S to meet pipeline specs, processing ~2.1 Bcf/d capacity in 2025 and cutting impurity-driven penalties; this ensures safe long-haul transport and compliance with FERC and state regs.

Its cryogenic plants recover NGLs (ethane, propane, butane), producing ~120 Mbpd of NGLs in 2025, boosting realized product value and fee-linked margin per Mcf for midstream contracts.

Produced Water Management

Summit Midstream runs dedicated water gathering systems and Class II disposal wells to collect, treat, and recycle produced water, supporting E&P uptime in water-intensive basins; in 2024 Summit reported handling roughly 45 million barrels of produced water year-to-date across the Permian and Delaware basins. This service reduces truck trips, cuts disposal costs for producers (typical Midland Basin disposal ~2.50–4.00 per barrel in 2024) and helps clients meet growing regulatory and ESG demands.

Infrastructure Engineering and Construction

Summit Midstream continuously plans, designs, and builds pipeline segments and facility expansions—handling land acquisition, environmental surveys, and technical engineering—to optimize flow and support producer growth; efficient project execution drove ~220 MMcf/d of new takeaway capacity added in 2024 and supported a 6% volume growth year-over-year.

- Land deals: dozens in 2024, avg. right-of-way cost $12k/acre

- Added capacity: ~220 MMcf/d in 2024

- Project ROI: typical IRR 12–18% on midstream expansions

Contract Management and Commercial Optimization

Summit actively manages fee-based contracts—including minimum volume commitments and acreage dedications—covering roughly 85% of throughput, with ~5 years weighted-average contract life as of Q4 2025; the commercial team re-contracts expiries and wins nearby producer capacity to lock steady cash flows and hedge commodity volatility.

- ~85% fee-based coverage

- ~5 years WACL (Q4 2025)

- focus: re-contract expiries, capture nearby producers

- reduces revenue sensitivity to commodity swings

Summit Midstream: 6,200 mi, 1.1 Bcf/d throughput, 2.1 Bcf/d processing & 85% fee-based

Summit Midstream gathers and compresses ~1.1 Bcf/d (2024) via 6,200 miles of pipelines, operates processing (2.1 Bcf/d capacity in 2025) and cryogenic NGL recovery (~120 Mbpd NGLs in 2025), handles ~45M barrels produced water (2024), added ~220 MMcf/d takeaway (2024), and maintains ~85% fee-based coverage with ~5-year WACL (Q4 2025).

| Metric | Value |

|---|---|

| Pipelines (miles) | 6,200 |

| Throughput (2024) | 1.1 Bcf/d |

| Processing capacity (2025) | 2.1 Bcf/d |

| NGLs (2025) | 120 Mbpd |

| Produced water (2024) | 45M bbl |

| Added capacity (2024) | 220 MMcf/d |

| Fee-based coverage | 85% |

| WACL (Q4 2025) | ~5 yrs |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Summit Midstream Business Model Canvas—no mockup or sample. Upon purchase, you'll receive this exact file with all sections and content included, ready to edit and present. The deliverable matches the preview in structure and formatting, available for immediate download. What you see here is what you’ll own.