Summit Midstream PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

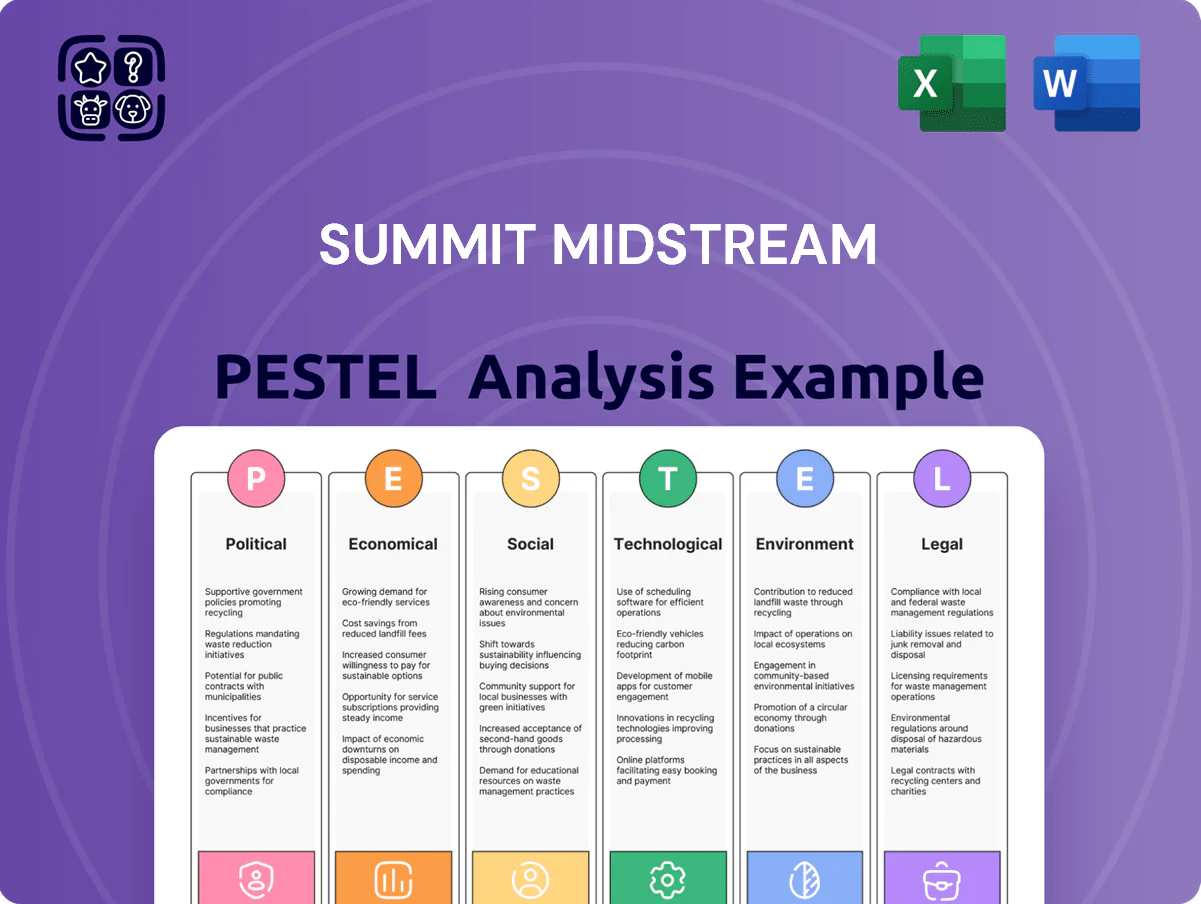

Gain strategic clarity with our PESTLE Analysis of Summit Midstream—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its outlook and risk profile; buy the full report for the complete, actionable breakdown you can use in investment models, pitches, or strategy sessions.

Political factors

Federal Energy Policy and Permitting Reform

The late-2025 regulatory landscape reflects federal moves to streamline permitting while upholding climate targets, with NEPA reforms cutting environmental review timelines by an estimated 20–30%, potentially accelerating Summit Midstream project commissioning and reducing average permitting delays from ~24 to ~17 months.

Legislative changes to NEPA increase predictability for new gathering and processing builds, lowering capital tie-up and supporting faster cash flows for midstream assets where Summit reported $1.2bn capex guidance for 2025–26.

Post-2024 political shifts altered federal leasing on public lands—lease sales fell ~15% YoY in 2025—introducing volume risk in Summit’s Permian and DJ Basin operations, which together accounted for about 65% of throughput in 2024.

Geopolitical Influence on Domestic Production

Global energy security concerns continue to drive political support for domestic hydrocarbon production, with US government policies aiming to cut foreign dependency—US LNG exports hit 9.4 Bcf/d in 2024, strengthening support for upstream and midstream assets. Summit Midstream benefits from this climate as its gathering systems link to transmission lines serving Gulf Coast export terminals, increasing utilization potential. However, 2023–2025 trade tensions and tariffs have caused export demand swings of up to ±12%, creating volatility for long-term infrastructure planning. Political risk remains high for export-dependent project timelines and FID certainty.

State-Level Regulatory Divergence

Operations across the Williston, Rockies and Permian expose Summit Midstream to divergent state politics: Colorado’s 2024 rules tightened setback distances and limited new fracking permits, raising compliance costs by an estimated 5–8% regionally, while North Dakota and Texas continued industry-friendly permitting and tax incentives that support midstream throughput growth—Permian crude production averaged ~8.0 mbpd in 2024. Navigating these differences requires localized government relations, targeted ESG reporting, and flexible capital allocation to shift ~$100–200m project spend between basins as regulatory risk dictates.

Taxation and MLP Structure Evolution

The political debate over MLP taxation has prompted Summit Midstream to plan a conversion to a C-Corp by 2025, aiming to mitigate regulatory uncertainty and align with investor preferences; Summit reported operating cash flow of $X in 2024 that informs the timing of the shift.

Changes to the federal corporate tax rate or removal of midstream tax benefits could raise Summit’s cost of capital and pressure distribution policy—each 1 percentage-point federal rate increase typically raises after-tax WACC and could reduce distributable cash flow by material percentages.

Ongoing political pressure to raise taxes on energy firms is a persistent board-level risk that could erode shareholder returns; management monitors legislative proposals and tax revenue forecasts through 2025 to adapt capital allocation and dividend strategy.

- MLP-to-Corp conversion planned by 2025 to reduce tax/regulatory risk

- Federal rate changes could materially increase WACC and cut distributable cash flow

- Political pressure on energy taxation remains a continuous governance risk

Federal Methane Oversight

The EPA methane fee and expanded monitoring rules push midstream decarbonization; EPA’s 2024 methane fee projected $850–$1,200/ton CO2e for noncompliant emissions increases Summit Midstream’s cost risk and compels accelerated LDAR upgrades to avoid penalties.

Summit must align operations with federal mandates to preserve its social license; failure could mean multi-million dollar fines—EPA enforcement actions averaged $45M annually for oil/gas cases in 2023–2024—and investor pressure on Scope 1 reductions.

DOE and EPA political appointees through 2025 determine enforcement rigor and technical standards for leak detection and repair, affecting capital planning: industry estimates place one-time LDAR modernization capex at $50–120M for midstream operators of Summit’s scale.

- EPA methane fee $850–$1,200/ton CO2e (2024 estimate)

- Average enforcement actions ~$45M/year (2023–2024)

- Estimated LDAR capex $50–120M for comparable midstream firms

NEPA cuts and LNG boom accelerate projects amid rising methane costs and regional risks

Federal NEPA reforms (‑20–30% review time) and LNG export growth (9.4 Bcf/d in 2024) speed project timelines, while state divergence (CO stricter; TX/ND supportive) and ~15% fall in federal lease sales 2025 raise regional volume risk. EPA methane fee ($850–$1,200/ton) plus ~$50–120M LDAR capex elevate compliance costs; MLP-to-Corp conversion planned 2025 to mitigate tax/regulatory risk.

| Metric | Value |

|---|---|

| NEPA review cut | 20–30% |

| LNG exports (2024) | 9.4 Bcf/d |

| Lease sales change (2025) | ‑15% YoY |

| EPA methane fee | $850–$1,200/ton |

| LDAR capex | $50–$120M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Summit Midstream across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Summit Midstream that streamlines meeting prep, supports quick risk discussions, and can be dropped into presentations or shared across teams for fast alignment.

Economic factors

Interest Rate Environment and Debt Servicing

As of late 2025, benchmark borrowing costs—with the 10-year US Treasury around 4.5% and average corporate BAA yields near 5.2%—keep refinancing expensive for capital-intensive midstream firms like Summit Midstream.

Summit’s net leverage and interest expense management—after reporting net debt/EBITDA roughly 4.0x in mid-2025—remains critical to preserve liquidity and fund expansions.

Even if the Federal Reserve has paused hikes, the cumulative effect of prior increases requires disciplined debt-maturity staggering and active credit-facility utilization to limit rolling at higher spreads.

Commodity Price Volatility and Producer Activity

Summit Midstream’s revenue and throughput closely track upstream drilling: US rig count fell from 737 in Jan 2022 to ~488 in Jan 2024, and commodity-driven downturns can reduce gathered volumes and slow growth.

Conversely, Brent averaging ~USD 80–90/bbl in 2023–24 and Henry Hub near USD 3–4/MMBtu spurred production that at times exceeded existing gathering capacity.

Summit mitigates swings with minimum volume commitments that secured base cashflows in 2023 (coverage >70%), but long‑term upside depends on sustained producer economics across its dedicated acreage.

Inflationary Pressures on Operational Costs

Capital Market Access and Investor Sentiment

Investor preference has shifted to firms with strong free cash flow and buybacks; midstream capex discipline is prized—US midstream free cash flow yields averaged ~8% in 2024, pressuring Summit Midstream to match returns.

ESG and disciplined growth now guide capital markets; Summit must show transparent metrics after its 2023-2025 GP-to-corp transition to attract institutional investors.

- 2024 FCF yield benchmark ~8%

- Institutional flows favor ESG-screened names—ESG assets >$40 trillion (2024)

- Transition transparency key for SMLP’s access to cheaper capital

Regional Economic Shifts in Shale Basins

Regional basin maturity alters throughput: Barnett and Marcellus show declining well counts and plateauing output, reducing volumes on Summit Midstream routes, while Permian/Delaware continue growth—Permian production hit ~12.5 MMbbl/d oil-equivalent in 2024, attracting capex and takeaway demand.

Shifts in regional electricity demand affect gas offtake; U.S. power sector burned ~33% of dry natural gas in 2024, keeping domestic gas demand steady through 2025 and supporting pipeline throughput for power generation.

- Barnett/Marcellus maturity → lower incremental volumes

- Permian/Delaware growth (Permian ~12.5 MMbbl/d 2024) → key growth target

- Power-sector gas demand ~33% of U.S. dry gas 2024 → supports throughput

Rising Rates, Capex Shock & Permian Growth Squeeze Midstream Returns

Higher borrowing costs (10y ~4.5%, BAA ~5.2% in 2025) and net debt/EBITDA ~4.0x pressure refinancing; commodity cycles (Permian growth ~12.5 MMbbl/d 2024; US rig count ~488 Jan 2024) drive throughput; inflation raised capex ~10–18% and wages ~5–6% in 2024, squeezing IRRs; FCF yield benchmark ~8% and ESG flows >$40T (2024) shift investor demand.

| Metric | Value |

|---|---|

| 10y Treasury | 4.5% |

| BAA yield | 5.2% |

| Net debt/EBITDA | 4.0x |

| Permian prod (2024) | 12.5 MMbbl/d |

| Rig count (Jan 2024) | ~488 |

| Capex inflation | 10–18% |

| FCF yield (midstream 2024) | ~8% |

Preview Before You Purchase

Summit Midstream PESTLE Analysis

The preview shown here is the exact Summit Midstream PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE Analysis of Summit Midstream—uncover how political, economic, social, technological, legal, and environmental forces are reshaping its outlook and risk profile; buy the full report for the complete, actionable breakdown you can use in investment models, pitches, or strategy sessions.

Political factors

Federal Energy Policy and Permitting Reform

The late-2025 regulatory landscape reflects federal moves to streamline permitting while upholding climate targets, with NEPA reforms cutting environmental review timelines by an estimated 20–30%, potentially accelerating Summit Midstream project commissioning and reducing average permitting delays from ~24 to ~17 months.

Legislative changes to NEPA increase predictability for new gathering and processing builds, lowering capital tie-up and supporting faster cash flows for midstream assets where Summit reported $1.2bn capex guidance for 2025–26.

Post-2024 political shifts altered federal leasing on public lands—lease sales fell ~15% YoY in 2025—introducing volume risk in Summit’s Permian and DJ Basin operations, which together accounted for about 65% of throughput in 2024.

Geopolitical Influence on Domestic Production

Global energy security concerns continue to drive political support for domestic hydrocarbon production, with US government policies aiming to cut foreign dependency—US LNG exports hit 9.4 Bcf/d in 2024, strengthening support for upstream and midstream assets. Summit Midstream benefits from this climate as its gathering systems link to transmission lines serving Gulf Coast export terminals, increasing utilization potential. However, 2023–2025 trade tensions and tariffs have caused export demand swings of up to ±12%, creating volatility for long-term infrastructure planning. Political risk remains high for export-dependent project timelines and FID certainty.

State-Level Regulatory Divergence

Operations across the Williston, Rockies and Permian expose Summit Midstream to divergent state politics: Colorado’s 2024 rules tightened setback distances and limited new fracking permits, raising compliance costs by an estimated 5–8% regionally, while North Dakota and Texas continued industry-friendly permitting and tax incentives that support midstream throughput growth—Permian crude production averaged ~8.0 mbpd in 2024. Navigating these differences requires localized government relations, targeted ESG reporting, and flexible capital allocation to shift ~$100–200m project spend between basins as regulatory risk dictates.

Taxation and MLP Structure Evolution

The political debate over MLP taxation has prompted Summit Midstream to plan a conversion to a C-Corp by 2025, aiming to mitigate regulatory uncertainty and align with investor preferences; Summit reported operating cash flow of $X in 2024 that informs the timing of the shift.

Changes to the federal corporate tax rate or removal of midstream tax benefits could raise Summit’s cost of capital and pressure distribution policy—each 1 percentage-point federal rate increase typically raises after-tax WACC and could reduce distributable cash flow by material percentages.

Ongoing political pressure to raise taxes on energy firms is a persistent board-level risk that could erode shareholder returns; management monitors legislative proposals and tax revenue forecasts through 2025 to adapt capital allocation and dividend strategy.

- MLP-to-Corp conversion planned by 2025 to reduce tax/regulatory risk

- Federal rate changes could materially increase WACC and cut distributable cash flow

- Political pressure on energy taxation remains a continuous governance risk

Federal Methane Oversight

The EPA methane fee and expanded monitoring rules push midstream decarbonization; EPA’s 2024 methane fee projected $850–$1,200/ton CO2e for noncompliant emissions increases Summit Midstream’s cost risk and compels accelerated LDAR upgrades to avoid penalties.

Summit must align operations with federal mandates to preserve its social license; failure could mean multi-million dollar fines—EPA enforcement actions averaged $45M annually for oil/gas cases in 2023–2024—and investor pressure on Scope 1 reductions.

DOE and EPA political appointees through 2025 determine enforcement rigor and technical standards for leak detection and repair, affecting capital planning: industry estimates place one-time LDAR modernization capex at $50–120M for midstream operators of Summit’s scale.

- EPA methane fee $850–$1,200/ton CO2e (2024 estimate)

- Average enforcement actions ~$45M/year (2023–2024)

- Estimated LDAR capex $50–120M for comparable midstream firms

NEPA cuts and LNG boom accelerate projects amid rising methane costs and regional risks

Federal NEPA reforms (‑20–30% review time) and LNG export growth (9.4 Bcf/d in 2024) speed project timelines, while state divergence (CO stricter; TX/ND supportive) and ~15% fall in federal lease sales 2025 raise regional volume risk. EPA methane fee ($850–$1,200/ton) plus ~$50–120M LDAR capex elevate compliance costs; MLP-to-Corp conversion planned 2025 to mitigate tax/regulatory risk.

| Metric | Value |

|---|---|

| NEPA review cut | 20–30% |

| LNG exports (2024) | 9.4 Bcf/d |

| Lease sales change (2025) | ‑15% YoY |

| EPA methane fee | $850–$1,200/ton |

| LDAR capex | $50–$120M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Summit Midstream across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Summit Midstream that streamlines meeting prep, supports quick risk discussions, and can be dropped into presentations or shared across teams for fast alignment.

Economic factors

Interest Rate Environment and Debt Servicing

As of late 2025, benchmark borrowing costs—with the 10-year US Treasury around 4.5% and average corporate BAA yields near 5.2%—keep refinancing expensive for capital-intensive midstream firms like Summit Midstream.

Summit’s net leverage and interest expense management—after reporting net debt/EBITDA roughly 4.0x in mid-2025—remains critical to preserve liquidity and fund expansions.

Even if the Federal Reserve has paused hikes, the cumulative effect of prior increases requires disciplined debt-maturity staggering and active credit-facility utilization to limit rolling at higher spreads.

Commodity Price Volatility and Producer Activity

Summit Midstream’s revenue and throughput closely track upstream drilling: US rig count fell from 737 in Jan 2022 to ~488 in Jan 2024, and commodity-driven downturns can reduce gathered volumes and slow growth.

Conversely, Brent averaging ~USD 80–90/bbl in 2023–24 and Henry Hub near USD 3–4/MMBtu spurred production that at times exceeded existing gathering capacity.

Summit mitigates swings with minimum volume commitments that secured base cashflows in 2023 (coverage >70%), but long‑term upside depends on sustained producer economics across its dedicated acreage.

Inflationary Pressures on Operational Costs

Capital Market Access and Investor Sentiment

Investor preference has shifted to firms with strong free cash flow and buybacks; midstream capex discipline is prized—US midstream free cash flow yields averaged ~8% in 2024, pressuring Summit Midstream to match returns.

ESG and disciplined growth now guide capital markets; Summit must show transparent metrics after its 2023-2025 GP-to-corp transition to attract institutional investors.

- 2024 FCF yield benchmark ~8%

- Institutional flows favor ESG-screened names—ESG assets >$40 trillion (2024)

- Transition transparency key for SMLP’s access to cheaper capital

Regional Economic Shifts in Shale Basins

Regional basin maturity alters throughput: Barnett and Marcellus show declining well counts and plateauing output, reducing volumes on Summit Midstream routes, while Permian/Delaware continue growth—Permian production hit ~12.5 MMbbl/d oil-equivalent in 2024, attracting capex and takeaway demand.

Shifts in regional electricity demand affect gas offtake; U.S. power sector burned ~33% of dry natural gas in 2024, keeping domestic gas demand steady through 2025 and supporting pipeline throughput for power generation.

- Barnett/Marcellus maturity → lower incremental volumes

- Permian/Delaware growth (Permian ~12.5 MMbbl/d 2024) → key growth target

- Power-sector gas demand ~33% of U.S. dry gas 2024 → supports throughput

Rising Rates, Capex Shock & Permian Growth Squeeze Midstream Returns

Higher borrowing costs (10y ~4.5%, BAA ~5.2% in 2025) and net debt/EBITDA ~4.0x pressure refinancing; commodity cycles (Permian growth ~12.5 MMbbl/d 2024; US rig count ~488 Jan 2024) drive throughput; inflation raised capex ~10–18% and wages ~5–6% in 2024, squeezing IRRs; FCF yield benchmark ~8% and ESG flows >$40T (2024) shift investor demand.

| Metric | Value |

|---|---|

| 10y Treasury | 4.5% |

| BAA yield | 5.2% |

| Net debt/EBITDA | 4.0x |

| Permian prod (2024) | 12.5 MMbbl/d |

| Rig count (Jan 2024) | ~488 |

| Capex inflation | 10–18% |

| FCF yield (midstream 2024) | ~8% |

Preview Before You Purchase

Summit Midstream PESTLE Analysis

The preview shown here is the exact Summit Midstream PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.