Sunac China Holdings PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how regulatory pressure, property-cycle dynamics, and ESG trends are reshaping Sunac China Holdings’ outlook—our concise PESTLE flags key risks and growth levers for investors and strategists; buy the full analysis to access detailed data, scenario impact assessments, and ready-to-use recommendations.

Political factors

Government focus on real estate stabilization

Support for debt risk resolution

Chinese authorities actively pushed debt restructuring for major developers like Sunac, coordinating regulators and banks to approve onshore extensions and offshore plans through 2025; by mid-2025 Sunac secured yuan bond extensions totaling about CNY 60 billion and agreed offshore restructuring reducing external debt by roughly USD 4.1 billion.

Urbanization and land supply policies

State-led urbanization drives demand for Sunac’s high-end residential and cultural tourism projects across city clusters; in 2024 urbanization rate hit 66.9% and mega-city development sustained luxury housing demand.

In 2025 local governments tightened land supply—reducing premium land auctions by ~12% YTD—to curb costs and advance common prosperity, pressuring margins on new land parcels.

Policies shift Sunac toward Tier-1 and strong Tier-2 cities where 2024 GDP per capita and policy-backed housing prioritization preserve project feasibility and lower acquisition risks.

Geopolitical influence on capital access

Rising geopolitical tensions through early 2026 have constrained Chinese developers’ access to international capital; offshore issuance for China property fell ~58% y/y in 2025, pushing Sunac to cut foreign funding reliance.

Sunac shifted toward domestic policy-led financing—using preferential bank credit and 2025 state-backed joint ventures with SOEs totaling ~RMB 22.4bn—to stabilize liquidity.

Political friction keeps offshore investor appetite muted, with non-China investor holdings of China real estate bonds dropping to ~12% of total by 2025, forcing Sunac to prioritize onshore funding and SOE cooperation.

- Offshore issuance down ~58% y/y in 2025

- Sunac SOE joint ventures ~RMB 22.4bn in 2025

- Non-China investor holdings ~12% of China RE bonds by 2025

Social stability through guaranteed delivery

By end-2025 the state-mandated guaranteed home delivery became Sunac’s primary operational benchmark; missing targets risks direct state intervention or additional winding-up petitions, as seen in 2024–25 when delayed handovers contributed to regulatory scrutiny and liquidity stress.

Sunac now prioritizes completing 120+ major projects slated for delivery in 2025–26 over new land acquisitions, aligning strategy with social stability goals and reducing expansion-driven revenue growth.

- Guaranteed delivery = core KPI; noncompliance → political/legal action

- 120+ projects prioritized for 2025–26

- Shift from land purchases to project completion

- Focus reduces short-term growth but mitigates state risk

Beijing’s CNY200bn lifeline eases Sunac strain as USD4.1bn offshore cut boosts deliveries

| Metric | Value |

|---|---|

| Pledged loan quota change | +CNY200bn (2025) |

| Sunac cash/pledged pressure | CNY18.3bn (2025) |

| Onshore extensions | CNY60bn (mid-2025) |

| Offshore debt cut | USD4.1bn |

| Offshore issuance change | -58% y/y (2025) |

| Non-China bond holdings | ~12% (2025) |

| SOE joint ventures | RMB22.4bn (2025) |

| Priority projects | 120+ (2025–26) |

What is included in the product

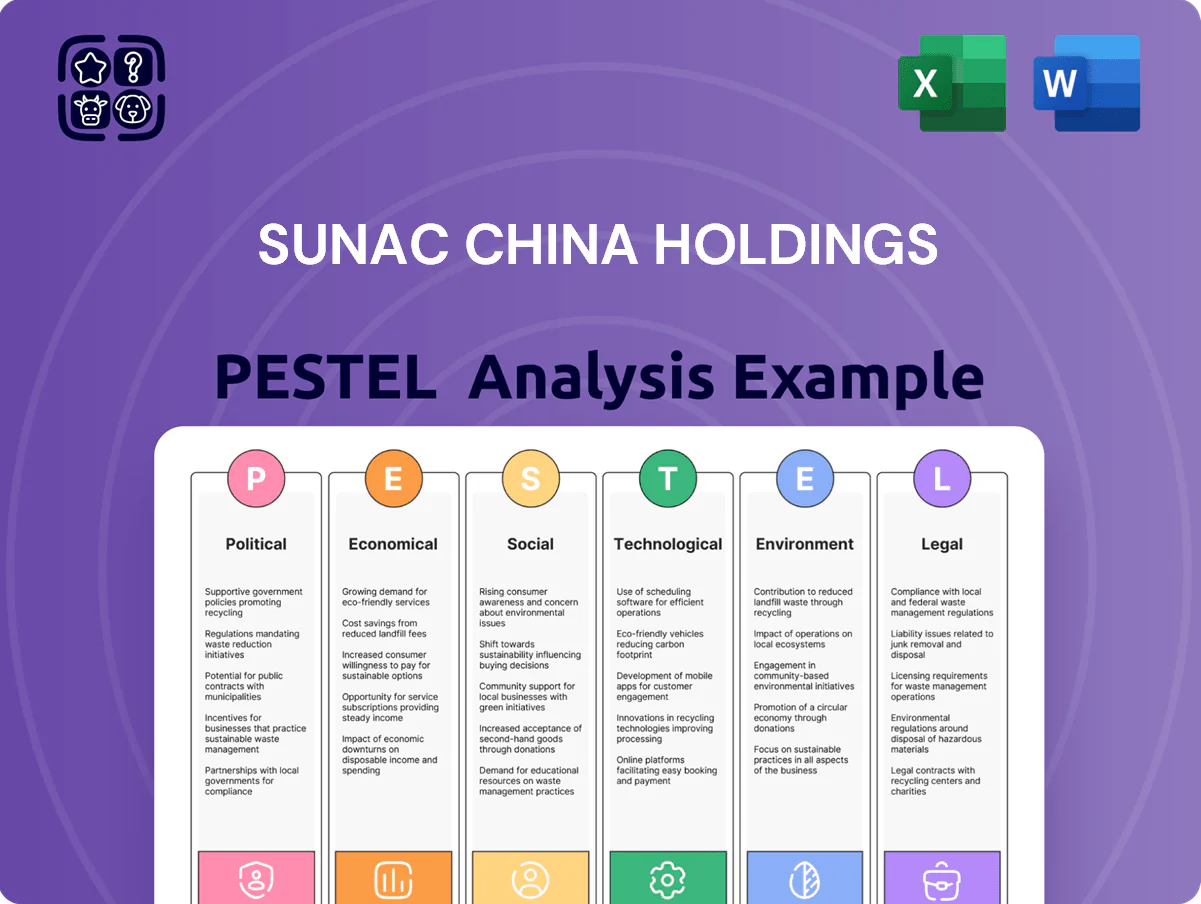

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Sunac China Holdings, pairing current data and trends with actionable insights to identify risks, opportunities, and strategic responses for executives, investors, and advisors.

A concise PESTLE snapshot of Sunac China Holdings that highlights regulatory, economic, social, technological, legal, and environmental risks and opportunities for quick inclusion in presentations or strategic briefings.

Economic factors

Narrowing losses and revenue stabilization

By end-2025 Sunac reported narrowing net losses—Rmb4.8bn vs Rmb18.6bn in 2024—indicating a fragile recovery after the severe downturn. Revenue recognition stabilized as Rmb32.5bn of backlog was converted into recognized income in 2025, though total revenue of Rmb58.3bn remained below peak levels. Management shifted emphasis from rapid expansion to securing positive operating cash flow, achieving operating cash inflows of Rmb6.1bn in 2025.

Successful large-scale debt restructuring

Sunac completed a landmark restructuring by late 2025, converting about USD 10.2 billion of offshore debt and sizable onshore obligations into mandatory convertible bonds and equity, cutting annual interest costs by an estimated USD 450–600 million and lowering its net debt/asset ratio from ~68% in 2023 to roughly 52% post-restructuring; this restored investor confidence and confirmed its going-concern status to major institutional creditors.

Soft demand in the property market

The start of 2026 shows cautious housing recovery with national new home sales down ~4% YoY in 2025 and unsold residential stock near 22 months of supply; Tier-1 cities (Shanghai, Beijing) see stable prices, but Sunac’s lower-tier projects face weak sell-through and longer days-on-market. The firm must rely on flexible pricing, phased launches and presales to protect cash amid no guaranteed price appreciation.

Monetary easing and mortgage affordability

Significant interest rate cuts and lower down-payment rules in 2025 lowered average mortgage rates to ~3.6% and reduced minimum down-payments to 15% in key cities, improving affordability for Sunac’s mid-to-high income buyers.

These stimulus measures target first-time buyers and upgraders, matching Sunac’s focus on high-end residential units and supporting demand recovery.

Sunac is using favorable mortgage terms to speed sales turnover—presales rose ~22% YoY in H1 2025—and revive premium projects via joint-ventures and channel partnerships.

- Average mortgage rate ~3.6% (2025)

- Minimum down-payment cut to 15% in major cities

- Sunac presales +22% YoY H1 2025

- Accelerated project revitalization through JVs

Diversification into cultural tourism and services

Sunac’s economic model shifted toward diversified segments—cultural tourism, ice and snow operations, and property management—raising non-property revenue to 28% of total revenue by 2025, reducing exposure to residential cycles.

By end-2025 these non-residential sectors delivered steadier recurring cashflows, supporting gross margin stability amid weaker property sales.

The turnaround of Sunac Services to profitability in 2025 (reported net profit margin ~4.5%) underscores the growing economic weight of service businesses for the group.

- Non-property revenue ~28% of total (2025)

- Sunac Services net margin ~4.5% (2025)

- Recurring revenue share up vs 2022 (~18%)

Sunac narrows 2025 loss to Rmb4.8bn as presales surge 22% and debt cut

Economic recovery in 2025 narrowed Sunac losses to Rmb4.8bn; revenue Rmb58.3bn; operating cash inflow Rmb6.1bn. Restructuring cut annual interest by ~USD500m and net debt/asset to ~52%. Presales +22% H1 2025; mortgage rate ~3.6%; down-payments 15%. Non-property revenue 28%; Sunac Services margin ~4.5%.

| Metric | 2025 |

|---|---|

| Net loss | Rmb4.8bn |

| Revenue | Rmb58.3bn |

| Op cash inflow | Rmb6.1bn |

| Presales H1 YoY | +22% |

Same Document Delivered

Sunac China Holdings PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, containing the complete Sunac China Holdings PESTLE analysis with findings, implications, and supporting data.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how regulatory pressure, property-cycle dynamics, and ESG trends are reshaping Sunac China Holdings’ outlook—our concise PESTLE flags key risks and growth levers for investors and strategists; buy the full analysis to access detailed data, scenario impact assessments, and ready-to-use recommendations.

Political factors

Government focus on real estate stabilization

Support for debt risk resolution

Chinese authorities actively pushed debt restructuring for major developers like Sunac, coordinating regulators and banks to approve onshore extensions and offshore plans through 2025; by mid-2025 Sunac secured yuan bond extensions totaling about CNY 60 billion and agreed offshore restructuring reducing external debt by roughly USD 4.1 billion.

Urbanization and land supply policies

State-led urbanization drives demand for Sunac’s high-end residential and cultural tourism projects across city clusters; in 2024 urbanization rate hit 66.9% and mega-city development sustained luxury housing demand.

In 2025 local governments tightened land supply—reducing premium land auctions by ~12% YTD—to curb costs and advance common prosperity, pressuring margins on new land parcels.

Policies shift Sunac toward Tier-1 and strong Tier-2 cities where 2024 GDP per capita and policy-backed housing prioritization preserve project feasibility and lower acquisition risks.

Geopolitical influence on capital access

Rising geopolitical tensions through early 2026 have constrained Chinese developers’ access to international capital; offshore issuance for China property fell ~58% y/y in 2025, pushing Sunac to cut foreign funding reliance.

Sunac shifted toward domestic policy-led financing—using preferential bank credit and 2025 state-backed joint ventures with SOEs totaling ~RMB 22.4bn—to stabilize liquidity.

Political friction keeps offshore investor appetite muted, with non-China investor holdings of China real estate bonds dropping to ~12% of total by 2025, forcing Sunac to prioritize onshore funding and SOE cooperation.

- Offshore issuance down ~58% y/y in 2025

- Sunac SOE joint ventures ~RMB 22.4bn in 2025

- Non-China investor holdings ~12% of China RE bonds by 2025

Social stability through guaranteed delivery

By end-2025 the state-mandated guaranteed home delivery became Sunac’s primary operational benchmark; missing targets risks direct state intervention or additional winding-up petitions, as seen in 2024–25 when delayed handovers contributed to regulatory scrutiny and liquidity stress.

Sunac now prioritizes completing 120+ major projects slated for delivery in 2025–26 over new land acquisitions, aligning strategy with social stability goals and reducing expansion-driven revenue growth.

- Guaranteed delivery = core KPI; noncompliance → political/legal action

- 120+ projects prioritized for 2025–26

- Shift from land purchases to project completion

- Focus reduces short-term growth but mitigates state risk

Beijing’s CNY200bn lifeline eases Sunac strain as USD4.1bn offshore cut boosts deliveries

| Metric | Value |

|---|---|

| Pledged loan quota change | +CNY200bn (2025) |

| Sunac cash/pledged pressure | CNY18.3bn (2025) |

| Onshore extensions | CNY60bn (mid-2025) |

| Offshore debt cut | USD4.1bn |

| Offshore issuance change | -58% y/y (2025) |

| Non-China bond holdings | ~12% (2025) |

| SOE joint ventures | RMB22.4bn (2025) |

| Priority projects | 120+ (2025–26) |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Sunac China Holdings, pairing current data and trends with actionable insights to identify risks, opportunities, and strategic responses for executives, investors, and advisors.

A concise PESTLE snapshot of Sunac China Holdings that highlights regulatory, economic, social, technological, legal, and environmental risks and opportunities for quick inclusion in presentations or strategic briefings.

Economic factors

Narrowing losses and revenue stabilization

By end-2025 Sunac reported narrowing net losses—Rmb4.8bn vs Rmb18.6bn in 2024—indicating a fragile recovery after the severe downturn. Revenue recognition stabilized as Rmb32.5bn of backlog was converted into recognized income in 2025, though total revenue of Rmb58.3bn remained below peak levels. Management shifted emphasis from rapid expansion to securing positive operating cash flow, achieving operating cash inflows of Rmb6.1bn in 2025.

Successful large-scale debt restructuring

Sunac completed a landmark restructuring by late 2025, converting about USD 10.2 billion of offshore debt and sizable onshore obligations into mandatory convertible bonds and equity, cutting annual interest costs by an estimated USD 450–600 million and lowering its net debt/asset ratio from ~68% in 2023 to roughly 52% post-restructuring; this restored investor confidence and confirmed its going-concern status to major institutional creditors.

Soft demand in the property market

The start of 2026 shows cautious housing recovery with national new home sales down ~4% YoY in 2025 and unsold residential stock near 22 months of supply; Tier-1 cities (Shanghai, Beijing) see stable prices, but Sunac’s lower-tier projects face weak sell-through and longer days-on-market. The firm must rely on flexible pricing, phased launches and presales to protect cash amid no guaranteed price appreciation.

Monetary easing and mortgage affordability

Significant interest rate cuts and lower down-payment rules in 2025 lowered average mortgage rates to ~3.6% and reduced minimum down-payments to 15% in key cities, improving affordability for Sunac’s mid-to-high income buyers.

These stimulus measures target first-time buyers and upgraders, matching Sunac’s focus on high-end residential units and supporting demand recovery.

Sunac is using favorable mortgage terms to speed sales turnover—presales rose ~22% YoY in H1 2025—and revive premium projects via joint-ventures and channel partnerships.

- Average mortgage rate ~3.6% (2025)

- Minimum down-payment cut to 15% in major cities

- Sunac presales +22% YoY H1 2025

- Accelerated project revitalization through JVs

Diversification into cultural tourism and services

Sunac’s economic model shifted toward diversified segments—cultural tourism, ice and snow operations, and property management—raising non-property revenue to 28% of total revenue by 2025, reducing exposure to residential cycles.

By end-2025 these non-residential sectors delivered steadier recurring cashflows, supporting gross margin stability amid weaker property sales.

The turnaround of Sunac Services to profitability in 2025 (reported net profit margin ~4.5%) underscores the growing economic weight of service businesses for the group.

- Non-property revenue ~28% of total (2025)

- Sunac Services net margin ~4.5% (2025)

- Recurring revenue share up vs 2022 (~18%)

Sunac narrows 2025 loss to Rmb4.8bn as presales surge 22% and debt cut

Economic recovery in 2025 narrowed Sunac losses to Rmb4.8bn; revenue Rmb58.3bn; operating cash inflow Rmb6.1bn. Restructuring cut annual interest by ~USD500m and net debt/asset to ~52%. Presales +22% H1 2025; mortgage rate ~3.6%; down-payments 15%. Non-property revenue 28%; Sunac Services margin ~4.5%.

| Metric | 2025 |

|---|---|

| Net loss | Rmb4.8bn |

| Revenue | Rmb58.3bn |

| Op cash inflow | Rmb6.1bn |

| Presales H1 YoY | +22% |

Same Document Delivered

Sunac China Holdings PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use, containing the complete Sunac China Holdings PESTLE analysis with findings, implications, and supporting data.