Sun Country Airlines Porter's Five Forces Analysis

From Overview to Strategy Blueprint

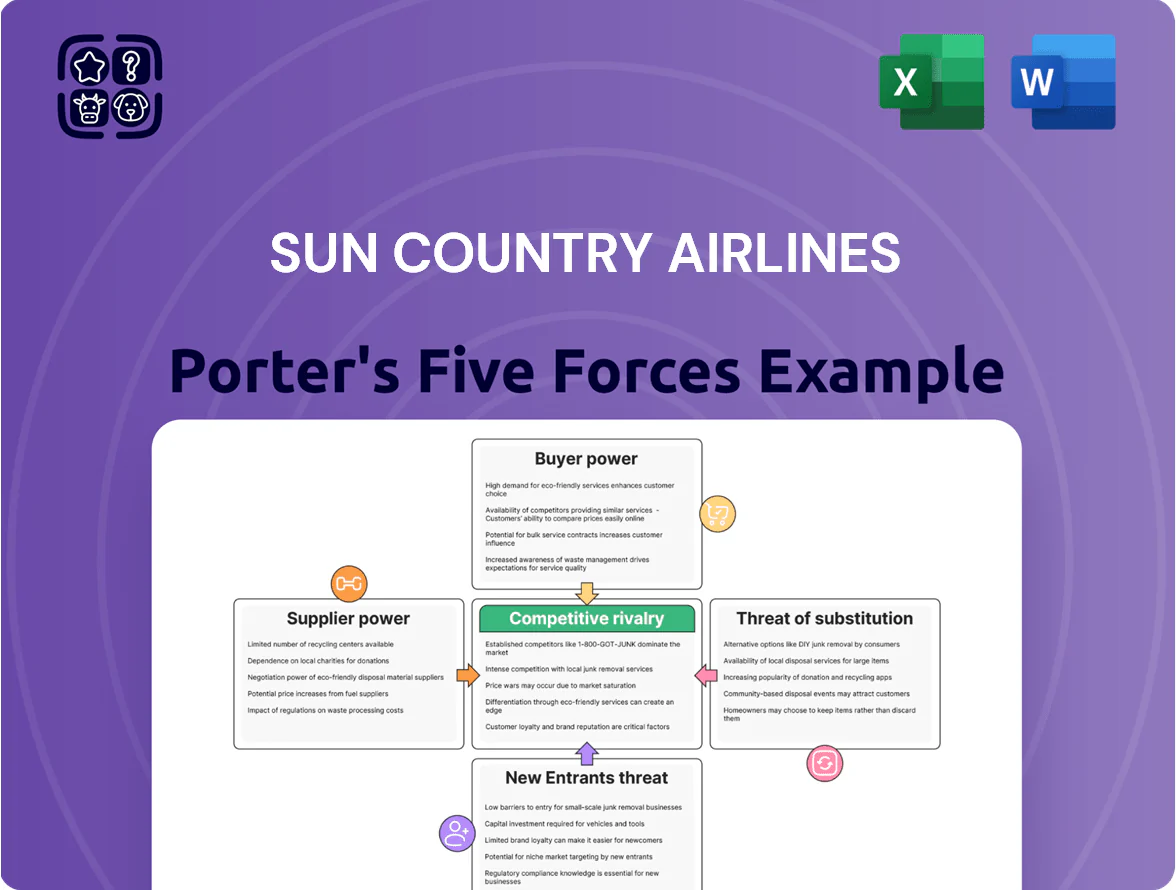

Sun Country Airlines operates in a high-pressure, capital-intensive market where incumbent rivalry and supplier power shape margins while buyer price sensitivity and low switching costs keep pricing volatile.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sun Country Airlines’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated Aircraft Manufacturing Duopoly

The narrow-body market is a Boeing-Airbus duopoly (≈90% share); this limits Sun Country’s bargaining on price and delivery, especially for mid-life 737s where Boeing sets lease/sale terms. As of 2025, global narrow-body backlog >11,000 jets, tightening secondary supply and raising used 737 prices by ~15% YoY in 2024. Any used-aircraft or spare-parts disruption amplifies supplier leverage and delivery risk for Sun Country.

Volatility in Global Fuel Markets

Fuel is one of Sun Country Airlines’ largest variable costs, accounting for roughly 20–25% of operating expenses in 2024; the carrier has virtually no influence on global crude or jet fuel margins.

Sun Country uses hedges—it reported $54 million of fuel-hedging gains in 2023—to blunt volatility, but remains a price taker as OPEC cuts and geopolitical shocks swing prices.

No scalable alternative fuel exists for commercial flights today, so suppliers keep strong leverage over margins and unit costs.

Organized Labor and Specialized Workforce

Airport Authority and Infrastructure Constraints

Airport authorities control gates, slots, and terminal space at Sun Country’s Minneapolis–St. Paul hub, giving them near-monopoly power to set landing fees and rents; MSP reported 2024 landing fee revenue of about $150 million, constraining carrier margins.

Limited gate availability at peak U.S.–Mexico/Caribbean leisure routes raises scheduling conflicts and delay risk; popular Mexican airports saw gate utilization >85% in 2024, reducing Sun Country’s operational flexibility.

- MSP hub dependence — concentrated infrastructure control

- Airport pricing power — landing fees drove $150M at MSP (2024)

- High gate utilization (>85%) at key leisure airports limits growth

- Little room to negotiate rents, increasing fixed costs

Third-Party Maintenance and Technical Services

Sun Country depends on third-party Maintenance, Repair, and Overhaul (MRO) firms to keep its fleet airworthy; in 2024 MRO spend for US low-cost carriers averaged about $3,000–$4,500 per flight hour, concentrating bargaining power with certified heavy-maintenance providers.

The technical depth of modern engines and avionics limits certified providers, so a handful of firms can raise labor and parts prices; this risk contributed to 2024 industry spare-parts inflation of ~6–8%, squeezing airline margins.

- High MRO reliance: outsources heavy checks

- Few certified providers: limited competition

- Cost pass-through: labor/materials up 6–8% in 2024

- Estimated MRO cost: $3k–$4.5k per flight hour (2024)

Supply squeeze lifts used-737s, fuels costs and MRO pain for airlines

Suppliers wield strong leverage: Boeing/Airbus duopoly limits aircraft/parts bargaining, used 737 prices rose ~15% YoY in 2024 amid a >11,000 narrow-body backlog (2025); jet fuel made up ~20–25% of Sun Country’s OPEX in 2024 with the airline a price taker despite $54M hedging gains in 2023; MRO spend ~ $3k–$4.5k/flight-hour (2024) and spare-parts inflation ~6–8% tightened margins.

| Metric | Value |

|---|---|

| Narrow-body backlog (2025) | >11,000 jets |

| Used 737 price change (2024) | +~15% YoY |

| Fuel share of OPEX (2024) | 20–25% |

| Fuel-hedge gains (2023) | $54M |

| MRO cost (2024) | $3k–$4.5k/flight-hr |

| Spare-parts inflation (2024) | ~6–8% |

What is included in the product

Tailored Porter's Five Forces for Sun Country Airlines, highlighting competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, and strategic levers to protect margin and market share.

A concise, one-sheet Porter's Five Forces for Sun Country—quickly spot competitive pressures like fuel cost volatility, low-cost carrier rivalry, and supplier leverage to guide immediate strategic moves.

Customers Bargaining Power

High Price Sensitivity of Leisure Travelers

Most of Sun Country’s passengers are leisure travelers who prioritize fares over loyalty; since 2023 leisure bookings made up ~78% of US domestic leisure airline demand, pushing Sun Country to compete on price.

These customers use metasearch and OTAs—Google Flights, Expedia, Kayak—so a $10–$20 fare gap can trigger switching, forcing frequent fare adjustments.

Result: Sun Country maintained a sub-peak average fare near $120–$140 in 2024 to defend share against ULCCs and legacy carriers’ basic economy.

Revenue Concentration with Amazon Cargo

As Amazon’s contracted carrier, Sun Country relies on a single buyer that booked roughly 40% of its 2024 cargo revenue, giving Amazon strong bargaining power and leverage to demand lower rates and strict service levels.

Amazon’s sophisticated logistics and plans to expand in-house fleet or switch providers could cut Sun Country’s predictable revenue quickly, so the airline must prioritize on-time performance and capacity flexibility to retain the account.

Low Switching Costs for Individual Passengers

Low switching costs let individual passengers shop freely: in 2024 online travel sites reported 73% of US leisure flyers compared fares each booking, and Sun Country’s hybrid model—limited elite loyalty uptake versus legacy carriers—means many are one-time buyers with no retention incentives, so customers push for lower fares and better service at each booking and this weakens Sun Country’s pricing power.

Charter Client Influence and Customization

Sun Country’s charter arm serves high-value clients like pro sports teams and the US Department of Defense, who in 2024 accounted for roughly 15–20% of seasonal revenue and demand bespoke schedules and cabin configurations.

These large buyers exert strong bargaining power, forcing competitive bids among charter operators and demanding high reliability; losing one major contract can cut peak-season operating income by an estimated 10–25%.

Information Symmetry via Digital Platforms

Information symmetry from social media and review sites means Sun Country faces real-time reputation risk—Tripadvisor and Google show airline ratings that shift quickly; 2024 data found 72% of flyers consult reviews before booking.

That transparency forces Sun Country to spend more on customer service and reliability—operational investments cut avoidable delays; Delta’s 2024 on-time score was 78% versus ULCCs ~65%, a gap customers notice.

Customers now spot hidden fees, baggage rules, and on-time stats pre-purchase, raising buyer leverage and increasing churn risk if Sun Country’s NPS drops; 1-point NPS decline can cut repeat bookings by ~0.5% annually.

- 72% consult reviews before booking (2024)

- On-time gap: legacy 78% vs ULCCs ~65% (2024)

- 1-point NPS drop ≈ 0.5% repeat bookings loss

Price-Sensitive Flyers & Big Contracts: Sun Country’s Revenue Squeeze

Buyers—mostly price-sensitive leisure flyers—have high bargaining power due to easy price comparison (73% compare fares in 2024) and low switching costs, forcing Sun Country to keep sub-peak fares near $120–$140 to defend share; large buyers (Amazon cargo ~40% of cargo revenue; pro teams/DoD 15–20% seasonal revenue) exert strong leverage on rates and service, so losing a major contract can cut peak operating income 10–25%.

| Metric | 2024/2025 Value |

|---|---|

| Leisure share of US demand | ~78% |

| Fare sensitivity (compare fares) | 73% |

| Sub-peak avg fare | $120–$140 |

| Amazon cargo share | ~40% of cargo rev |

| Charter high-value clients | 15–20% seasonal rev |

| Loss impact on peak profit | 10–25% |

What You See Is What You Get

Sun Country Airlines Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Sun Country Airlines you’ll receive immediately after purchase—no placeholders, no samples, just the fully formatted, ready-to-use document.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Sun Country Airlines operates in a high-pressure, capital-intensive market where incumbent rivalry and supplier power shape margins while buyer price sensitivity and low switching costs keep pricing volatile.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sun Country Airlines’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated Aircraft Manufacturing Duopoly

The narrow-body market is a Boeing-Airbus duopoly (≈90% share); this limits Sun Country’s bargaining on price and delivery, especially for mid-life 737s where Boeing sets lease/sale terms. As of 2025, global narrow-body backlog >11,000 jets, tightening secondary supply and raising used 737 prices by ~15% YoY in 2024. Any used-aircraft or spare-parts disruption amplifies supplier leverage and delivery risk for Sun Country.

Volatility in Global Fuel Markets

Fuel is one of Sun Country Airlines’ largest variable costs, accounting for roughly 20–25% of operating expenses in 2024; the carrier has virtually no influence on global crude or jet fuel margins.

Sun Country uses hedges—it reported $54 million of fuel-hedging gains in 2023—to blunt volatility, but remains a price taker as OPEC cuts and geopolitical shocks swing prices.

No scalable alternative fuel exists for commercial flights today, so suppliers keep strong leverage over margins and unit costs.

Organized Labor and Specialized Workforce

Airport Authority and Infrastructure Constraints

Airport authorities control gates, slots, and terminal space at Sun Country’s Minneapolis–St. Paul hub, giving them near-monopoly power to set landing fees and rents; MSP reported 2024 landing fee revenue of about $150 million, constraining carrier margins.

Limited gate availability at peak U.S.–Mexico/Caribbean leisure routes raises scheduling conflicts and delay risk; popular Mexican airports saw gate utilization >85% in 2024, reducing Sun Country’s operational flexibility.

- MSP hub dependence — concentrated infrastructure control

- Airport pricing power — landing fees drove $150M at MSP (2024)

- High gate utilization (>85%) at key leisure airports limits growth

- Little room to negotiate rents, increasing fixed costs

Third-Party Maintenance and Technical Services

Sun Country depends on third-party Maintenance, Repair, and Overhaul (MRO) firms to keep its fleet airworthy; in 2024 MRO spend for US low-cost carriers averaged about $3,000–$4,500 per flight hour, concentrating bargaining power with certified heavy-maintenance providers.

The technical depth of modern engines and avionics limits certified providers, so a handful of firms can raise labor and parts prices; this risk contributed to 2024 industry spare-parts inflation of ~6–8%, squeezing airline margins.

- High MRO reliance: outsources heavy checks

- Few certified providers: limited competition

- Cost pass-through: labor/materials up 6–8% in 2024

- Estimated MRO cost: $3k–$4.5k per flight hour (2024)

Supply squeeze lifts used-737s, fuels costs and MRO pain for airlines

Suppliers wield strong leverage: Boeing/Airbus duopoly limits aircraft/parts bargaining, used 737 prices rose ~15% YoY in 2024 amid a >11,000 narrow-body backlog (2025); jet fuel made up ~20–25% of Sun Country’s OPEX in 2024 with the airline a price taker despite $54M hedging gains in 2023; MRO spend ~ $3k–$4.5k/flight-hour (2024) and spare-parts inflation ~6–8% tightened margins.

| Metric | Value |

|---|---|

| Narrow-body backlog (2025) | >11,000 jets |

| Used 737 price change (2024) | +~15% YoY |

| Fuel share of OPEX (2024) | 20–25% |

| Fuel-hedge gains (2023) | $54M |

| MRO cost (2024) | $3k–$4.5k/flight-hr |

| Spare-parts inflation (2024) | ~6–8% |

What is included in the product

Tailored Porter's Five Forces for Sun Country Airlines, highlighting competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, and strategic levers to protect margin and market share.

A concise, one-sheet Porter's Five Forces for Sun Country—quickly spot competitive pressures like fuel cost volatility, low-cost carrier rivalry, and supplier leverage to guide immediate strategic moves.

Customers Bargaining Power

High Price Sensitivity of Leisure Travelers

Most of Sun Country’s passengers are leisure travelers who prioritize fares over loyalty; since 2023 leisure bookings made up ~78% of US domestic leisure airline demand, pushing Sun Country to compete on price.

These customers use metasearch and OTAs—Google Flights, Expedia, Kayak—so a $10–$20 fare gap can trigger switching, forcing frequent fare adjustments.

Result: Sun Country maintained a sub-peak average fare near $120–$140 in 2024 to defend share against ULCCs and legacy carriers’ basic economy.

Revenue Concentration with Amazon Cargo

As Amazon’s contracted carrier, Sun Country relies on a single buyer that booked roughly 40% of its 2024 cargo revenue, giving Amazon strong bargaining power and leverage to demand lower rates and strict service levels.

Amazon’s sophisticated logistics and plans to expand in-house fleet or switch providers could cut Sun Country’s predictable revenue quickly, so the airline must prioritize on-time performance and capacity flexibility to retain the account.

Low Switching Costs for Individual Passengers

Low switching costs let individual passengers shop freely: in 2024 online travel sites reported 73% of US leisure flyers compared fares each booking, and Sun Country’s hybrid model—limited elite loyalty uptake versus legacy carriers—means many are one-time buyers with no retention incentives, so customers push for lower fares and better service at each booking and this weakens Sun Country’s pricing power.

Charter Client Influence and Customization

Sun Country’s charter arm serves high-value clients like pro sports teams and the US Department of Defense, who in 2024 accounted for roughly 15–20% of seasonal revenue and demand bespoke schedules and cabin configurations.

These large buyers exert strong bargaining power, forcing competitive bids among charter operators and demanding high reliability; losing one major contract can cut peak-season operating income by an estimated 10–25%.

Information Symmetry via Digital Platforms

Information symmetry from social media and review sites means Sun Country faces real-time reputation risk—Tripadvisor and Google show airline ratings that shift quickly; 2024 data found 72% of flyers consult reviews before booking.

That transparency forces Sun Country to spend more on customer service and reliability—operational investments cut avoidable delays; Delta’s 2024 on-time score was 78% versus ULCCs ~65%, a gap customers notice.

Customers now spot hidden fees, baggage rules, and on-time stats pre-purchase, raising buyer leverage and increasing churn risk if Sun Country’s NPS drops; 1-point NPS decline can cut repeat bookings by ~0.5% annually.

- 72% consult reviews before booking (2024)

- On-time gap: legacy 78% vs ULCCs ~65% (2024)

- 1-point NPS drop ≈ 0.5% repeat bookings loss

Price-Sensitive Flyers & Big Contracts: Sun Country’s Revenue Squeeze

Buyers—mostly price-sensitive leisure flyers—have high bargaining power due to easy price comparison (73% compare fares in 2024) and low switching costs, forcing Sun Country to keep sub-peak fares near $120–$140 to defend share; large buyers (Amazon cargo ~40% of cargo revenue; pro teams/DoD 15–20% seasonal revenue) exert strong leverage on rates and service, so losing a major contract can cut peak operating income 10–25%.

| Metric | 2024/2025 Value |

|---|---|

| Leisure share of US demand | ~78% |

| Fare sensitivity (compare fares) | 73% |

| Sub-peak avg fare | $120–$140 |

| Amazon cargo share | ~40% of cargo rev |

| Charter high-value clients | 15–20% seasonal rev |

| Loss impact on peak profit | 10–25% |

What You See Is What You Get

Sun Country Airlines Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Sun Country Airlines you’ll receive immediately after purchase—no placeholders, no samples, just the fully formatted, ready-to-use document.