Sun Country Airlines PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, fuel-price volatility, and evolving traveler preferences are reshaping Sun Country Airlines’ strategic landscape in our concise PESTLE snapshot—useful for investors and strategists alike; buy the full analysis to unlock detailed risk assessments, scenario forecasts, and actionable recommendations tailored to power smarter decisions.

Political factors

Federal Aviation Administration oversight

The FAA maintains strict oversight over Sun Country, enforcing maintenance schedules and pilot certification that affect operational uptime; in 2024 U.S. carriers averaged 99.2% FAA-compliant safety event resolution rates. Changes in federal leadership by end-2025 could tighten protocols or reallocate infrastructure funding—FAA budget was $18.1B in FY2024—potentially slowing Sun Country’s fleet and network expansion within the U.S.

International trade and aviation treaties

Sun Country’s extensive Mexico and Caribbean network—about 40% of its 2025 international ASMs—relies on bilateral air service agreements and trade policies; disruptions to Open Skies or diplomatic ties could reduce access to key leisure markets and hurt 2024–25 international revenue, which accounted for roughly $420 million of total revenue in 2024. Maintaining positive political relations is critical to sustain scheduled routes and yield stability.

Government cargo contract stability

Sun Country’s cargo arm, anchored by Amazon and other logistics partners, is sensitive to federal postal and DOT policy; Amazon accounted for an estimated 25–30% of U.S. e-commerce air capacity in 2024, underscoring contract importance for Sun Country’s revenue mix.

Regulatory shifts tightening requirements for third‑party carriers or changing USPS contracting could compress margins and reduce the carrier’s cargo contribution, which helped drive Sun Country’s cargo revenue growth of roughly 40% year‑over‑year in 2023–24.

Rising political emphasis on domestic supply‑chain resilience, including proposed federal incentives and procurement priorities through 2026, could expand TAM for U.S. air cargo and present scale-up opportunities for Sun Country’s diversified model.

Taxation and airport infrastructure fees

- Average PFCs/ticket ~4.50–18 USD depending on airport

- Federal excise tax currently 7.5% on domestic tickets (as of 2025)

- Leisure sensitivity means small tax rises may reduce load factors

Geopolitical impact on fuel supply

Global political instability in oil-producing regions keeps jet fuel prices elevated; Brent crude averaged about $86/barrel in 2024, keeping U.S. jet fuel near $3.10/gal and pressuring Sun Country’s 2024 fuel expense, which comprised roughly 20–25% of operating costs.

Government moves toward energy independence, strategic reserves releases, or sanctions can ease or worsen supply tightness; U.S. SPR releases in 2024 temporarily capped spikes but do not eliminate volatility.

Sun Country must monitor geopolitical shifts—conflicts, sanctions, or trade disputes—that can trigger sudden fuel-cost surges or supply-chain disruptions, directly impacting margins and fare competitiveness.

- Brent ~ $86/barrel (2024); U.S. jet fuel ~ $3.10/gal (2024)

- Fuel ~20–25% of Sun Country operating costs (2024 estimate)

- SPR releases can blunt but not remove price shocks

Sun Country Faces Regulatory, Tax, Fuel and Political Risks Amid Heavy Mexico/Caribbean & Amazon Exposure

Federal FAA oversight, proposed excise/PFC changes, and bilateral air‑service politics directly affect Sun Country’s network, costs, and cargo contracts; FAA budget $18.1B (FY2024), federal excise tax 7.5% (2025), PFCs ~$4.50–18. Brent $86/bbl, jet fuel ~$3.10/gal (2024). Strong reliance on Mexico/Caribbean (≈40% 2025 intl ASMs) and cargo partners (25–30% Amazon share) raises political exposure.

| Metric | Value (2024/25) |

|---|---|

| FAA budget | $18.1B (FY2024) |

| Federal excise tax | 7.5% (2025) |

| PFCs | $4.50–18 avg |

| Brent / jet fuel | $86/bbl / $3.10/gal (2024) |

| Intl ASMs (Mexico/Carib) | ~40% (2025) |

| Amazon share U.S. e‑commerce air | 25–30% (2024) |

What is included in the product

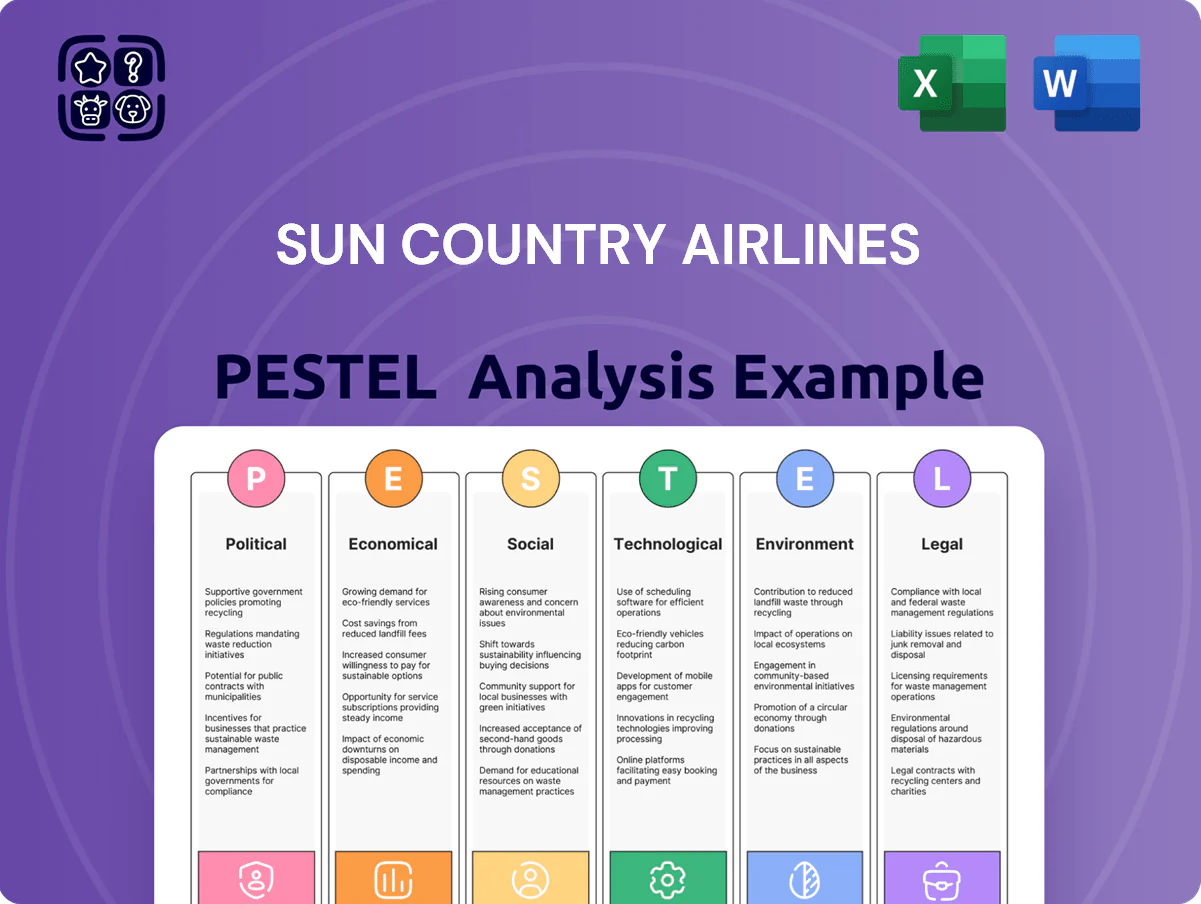

Explores how macro-environmental factors impact Sun Country Airlines across Political, Economic, Social, Technological, Environmental, and Legal dimensions, using current industry data and regional dynamics to identify risks and opportunities.

A concise Sun Country Airlines PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to support risk discussions and strategic planning.

Economic factors

Consumer discretionary spending trends

Sun Country is highly sensitive to shifts in household income and consumer confidence, as leisure travel is often the first expense cut during downturns; US consumer confidence fell to 101.3 in Dec 2025, weighing on bookings. By end-2025 inflationary pressures—core CPI running near 3.8% in 2025—remain a key metric for forecasting seat demand in scheduled service. The airline relies on a strong economic environment to sustain high load factors to vacation destinations, with average load factors of leisure carriers around 85% in 2025.

Fuel price volatility and hedging

Jet fuel accounted for roughly 30-35% of Sun Country Airlines' operating costs pre-2025, with U.S. jet fuel averages spiking to about $3.00–3.50/gal in 2024; this volatility materially impacts margins.

Sun Country employs strategic fuel hedging—covering portions of expected consumption via swaps and options—to smooth quarterly P&L, though long-term price trends above hedge levels can erode profitability.

Global energy shifts (OPEC+ supply moves, 2024 crude range $70–95/bbl) require flexible fare structures and ancillary revenue growth to pass costs while retaining price-sensitive leisure and immigrant-traveler demand.

Interest rates and fleet financing

Rising Federal Reserve policy rates, which averaged about 5.25–5.50% through 2024–2025, have pushed aircraft lease and loan costs higher, increasing Sun Country’s capital expenditure burden for fleet renewals. Elevated rates raise annual borrowing costs and can add tens of millions in interest expenses when financing narrowbody jets. Prudent debt management and negotiating lower spreads or sale-leaseback deals are essential to preserve Sun Country’s low-cost model and competitive fares.

Labor market competition and wage inflation

The US aviation sector reported a pilot shortfall of about 77,000 by 2024 (Airlines for America estimate), pressuring wages; technician shortages similarly pushed aircraft maintenance pay up ~6–8% year-over-year in 2023–24.

Sun Country must balance offering market-competitive pay to secure pilots and A&P mechanics while containing unit costs—labor accounts for roughly 20–25% of operating expenses for low-cost carriers.

Competition from legacy carriers and regional airlines for specialized labor threatens on-time performance and capacity growth targets if recruitment and retention lag.

- Pilot shortfall ~77,000 (A4A, 2024)

- Tech pay growth ~6–8% (2023–24)

- Labor = ~20–25% of LCC operating costs

Cargo demand and e-commerce growth

Sun Country's cargo revenue is closely linked to e-commerce volumes; U.S. e-commerce sales hit about 1.1 trillion USD in 2024, supporting higher parcel demand and express freight for partners like Amazon, which accounted for a growing share of air freight capacity in 2023–24.

Economic slowdowns reduce discretionary spending and same-day delivery demand, causing freight volumes and yield volatility; Sun Country reported cargo and ancillary growth in 2024 but remains exposed to e-commerce cyclicality.

- 2024 U.S. e-commerce: ~1.1 trillion USD

- Amazon: major air freight partner driving capacity needs

- Cyclicality risk: freight volume/yield sensitive to GDP and consumer spending

Macro headwinds, fuel swings, and pilot shortfall squeeze leisure carriers' margins

Economic sensitivity: weaker consumer confidence (101.3 Dec 2025) and core CPI ~3.8% in 2025 pressure leisure booking demand; load factors ~85% for leisure carriers in 2025. Fuel volatility (jet $3.00–3.50/gal in 2024; crude $70–95/bbl 2024) and hedging affect margins. Higher rates (Fed 5.25–5.50% 2024–25) raise financing costs; pilot shortfall ~77,000 (2024) lifts labor pay.

| Metric | Value |

|---|---|

| Consumer confidence | 101.3 (Dec 2025) |

| Core CPI | ~3.8% (2025) |

| Jet fuel | $3.00–3.50/gal (2024) |

| Crude | $70–95/bbl (2024) |

| Fed funds | 5.25–5.50% (2024–25) |

| Pilot shortfall | ~77,000 (2024) |

Preview the Actual Deliverable

Sun Country Airlines PESTLE Analysis

The preview shown here is the exact Sun Country Airlines PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how regulatory shifts, fuel-price volatility, and evolving traveler preferences are reshaping Sun Country Airlines’ strategic landscape in our concise PESTLE snapshot—useful for investors and strategists alike; buy the full analysis to unlock detailed risk assessments, scenario forecasts, and actionable recommendations tailored to power smarter decisions.

Political factors

Federal Aviation Administration oversight

The FAA maintains strict oversight over Sun Country, enforcing maintenance schedules and pilot certification that affect operational uptime; in 2024 U.S. carriers averaged 99.2% FAA-compliant safety event resolution rates. Changes in federal leadership by end-2025 could tighten protocols or reallocate infrastructure funding—FAA budget was $18.1B in FY2024—potentially slowing Sun Country’s fleet and network expansion within the U.S.

International trade and aviation treaties

Sun Country’s extensive Mexico and Caribbean network—about 40% of its 2025 international ASMs—relies on bilateral air service agreements and trade policies; disruptions to Open Skies or diplomatic ties could reduce access to key leisure markets and hurt 2024–25 international revenue, which accounted for roughly $420 million of total revenue in 2024. Maintaining positive political relations is critical to sustain scheduled routes and yield stability.

Government cargo contract stability

Sun Country’s cargo arm, anchored by Amazon and other logistics partners, is sensitive to federal postal and DOT policy; Amazon accounted for an estimated 25–30% of U.S. e-commerce air capacity in 2024, underscoring contract importance for Sun Country’s revenue mix.

Regulatory shifts tightening requirements for third‑party carriers or changing USPS contracting could compress margins and reduce the carrier’s cargo contribution, which helped drive Sun Country’s cargo revenue growth of roughly 40% year‑over‑year in 2023–24.

Rising political emphasis on domestic supply‑chain resilience, including proposed federal incentives and procurement priorities through 2026, could expand TAM for U.S. air cargo and present scale-up opportunities for Sun Country’s diversified model.

Taxation and airport infrastructure fees

- Average PFCs/ticket ~4.50–18 USD depending on airport

- Federal excise tax currently 7.5% on domestic tickets (as of 2025)

- Leisure sensitivity means small tax rises may reduce load factors

Geopolitical impact on fuel supply

Global political instability in oil-producing regions keeps jet fuel prices elevated; Brent crude averaged about $86/barrel in 2024, keeping U.S. jet fuel near $3.10/gal and pressuring Sun Country’s 2024 fuel expense, which comprised roughly 20–25% of operating costs.

Government moves toward energy independence, strategic reserves releases, or sanctions can ease or worsen supply tightness; U.S. SPR releases in 2024 temporarily capped spikes but do not eliminate volatility.

Sun Country must monitor geopolitical shifts—conflicts, sanctions, or trade disputes—that can trigger sudden fuel-cost surges or supply-chain disruptions, directly impacting margins and fare competitiveness.

- Brent ~ $86/barrel (2024); U.S. jet fuel ~ $3.10/gal (2024)

- Fuel ~20–25% of Sun Country operating costs (2024 estimate)

- SPR releases can blunt but not remove price shocks

Sun Country Faces Regulatory, Tax, Fuel and Political Risks Amid Heavy Mexico/Caribbean & Amazon Exposure

Federal FAA oversight, proposed excise/PFC changes, and bilateral air‑service politics directly affect Sun Country’s network, costs, and cargo contracts; FAA budget $18.1B (FY2024), federal excise tax 7.5% (2025), PFCs ~$4.50–18. Brent $86/bbl, jet fuel ~$3.10/gal (2024). Strong reliance on Mexico/Caribbean (≈40% 2025 intl ASMs) and cargo partners (25–30% Amazon share) raises political exposure.

| Metric | Value (2024/25) |

|---|---|

| FAA budget | $18.1B (FY2024) |

| Federal excise tax | 7.5% (2025) |

| PFCs | $4.50–18 avg |

| Brent / jet fuel | $86/bbl / $3.10/gal (2024) |

| Intl ASMs (Mexico/Carib) | ~40% (2025) |

| Amazon share U.S. e‑commerce air | 25–30% (2024) |

What is included in the product

Explores how macro-environmental factors impact Sun Country Airlines across Political, Economic, Social, Technological, Environmental, and Legal dimensions, using current industry data and regional dynamics to identify risks and opportunities.

A concise Sun Country Airlines PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to support risk discussions and strategic planning.

Economic factors

Consumer discretionary spending trends

Sun Country is highly sensitive to shifts in household income and consumer confidence, as leisure travel is often the first expense cut during downturns; US consumer confidence fell to 101.3 in Dec 2025, weighing on bookings. By end-2025 inflationary pressures—core CPI running near 3.8% in 2025—remain a key metric for forecasting seat demand in scheduled service. The airline relies on a strong economic environment to sustain high load factors to vacation destinations, with average load factors of leisure carriers around 85% in 2025.

Fuel price volatility and hedging

Jet fuel accounted for roughly 30-35% of Sun Country Airlines' operating costs pre-2025, with U.S. jet fuel averages spiking to about $3.00–3.50/gal in 2024; this volatility materially impacts margins.

Sun Country employs strategic fuel hedging—covering portions of expected consumption via swaps and options—to smooth quarterly P&L, though long-term price trends above hedge levels can erode profitability.

Global energy shifts (OPEC+ supply moves, 2024 crude range $70–95/bbl) require flexible fare structures and ancillary revenue growth to pass costs while retaining price-sensitive leisure and immigrant-traveler demand.

Interest rates and fleet financing

Rising Federal Reserve policy rates, which averaged about 5.25–5.50% through 2024–2025, have pushed aircraft lease and loan costs higher, increasing Sun Country’s capital expenditure burden for fleet renewals. Elevated rates raise annual borrowing costs and can add tens of millions in interest expenses when financing narrowbody jets. Prudent debt management and negotiating lower spreads or sale-leaseback deals are essential to preserve Sun Country’s low-cost model and competitive fares.

Labor market competition and wage inflation

The US aviation sector reported a pilot shortfall of about 77,000 by 2024 (Airlines for America estimate), pressuring wages; technician shortages similarly pushed aircraft maintenance pay up ~6–8% year-over-year in 2023–24.

Sun Country must balance offering market-competitive pay to secure pilots and A&P mechanics while containing unit costs—labor accounts for roughly 20–25% of operating expenses for low-cost carriers.

Competition from legacy carriers and regional airlines for specialized labor threatens on-time performance and capacity growth targets if recruitment and retention lag.

- Pilot shortfall ~77,000 (A4A, 2024)

- Tech pay growth ~6–8% (2023–24)

- Labor = ~20–25% of LCC operating costs

Cargo demand and e-commerce growth

Sun Country's cargo revenue is closely linked to e-commerce volumes; U.S. e-commerce sales hit about 1.1 trillion USD in 2024, supporting higher parcel demand and express freight for partners like Amazon, which accounted for a growing share of air freight capacity in 2023–24.

Economic slowdowns reduce discretionary spending and same-day delivery demand, causing freight volumes and yield volatility; Sun Country reported cargo and ancillary growth in 2024 but remains exposed to e-commerce cyclicality.

- 2024 U.S. e-commerce: ~1.1 trillion USD

- Amazon: major air freight partner driving capacity needs

- Cyclicality risk: freight volume/yield sensitive to GDP and consumer spending

Macro headwinds, fuel swings, and pilot shortfall squeeze leisure carriers' margins

Economic sensitivity: weaker consumer confidence (101.3 Dec 2025) and core CPI ~3.8% in 2025 pressure leisure booking demand; load factors ~85% for leisure carriers in 2025. Fuel volatility (jet $3.00–3.50/gal in 2024; crude $70–95/bbl 2024) and hedging affect margins. Higher rates (Fed 5.25–5.50% 2024–25) raise financing costs; pilot shortfall ~77,000 (2024) lifts labor pay.

| Metric | Value |

|---|---|

| Consumer confidence | 101.3 (Dec 2025) |

| Core CPI | ~3.8% (2025) |

| Jet fuel | $3.00–3.50/gal (2024) |

| Crude | $70–95/bbl (2024) |

| Fed funds | 5.25–5.50% (2024–25) |

| Pilot shortfall | ~77,000 (2024) |

Preview the Actual Deliverable

Sun Country Airlines PESTLE Analysis

The preview shown here is the exact Sun Country Airlines PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.