Sungrow Power Supply Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Sungrow Power Supply faces moderate rivalry, strong buyer negotiation from project developers, supplier leverage for key components, rising substitute pressure from alternative storage tech, and high barriers for some entrants due to scale and certification—this snapshot highlights strategic pinch points and growth levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sungrow Power Supply’s competitive dynamics, market pressures, and strategic advantages in detail.

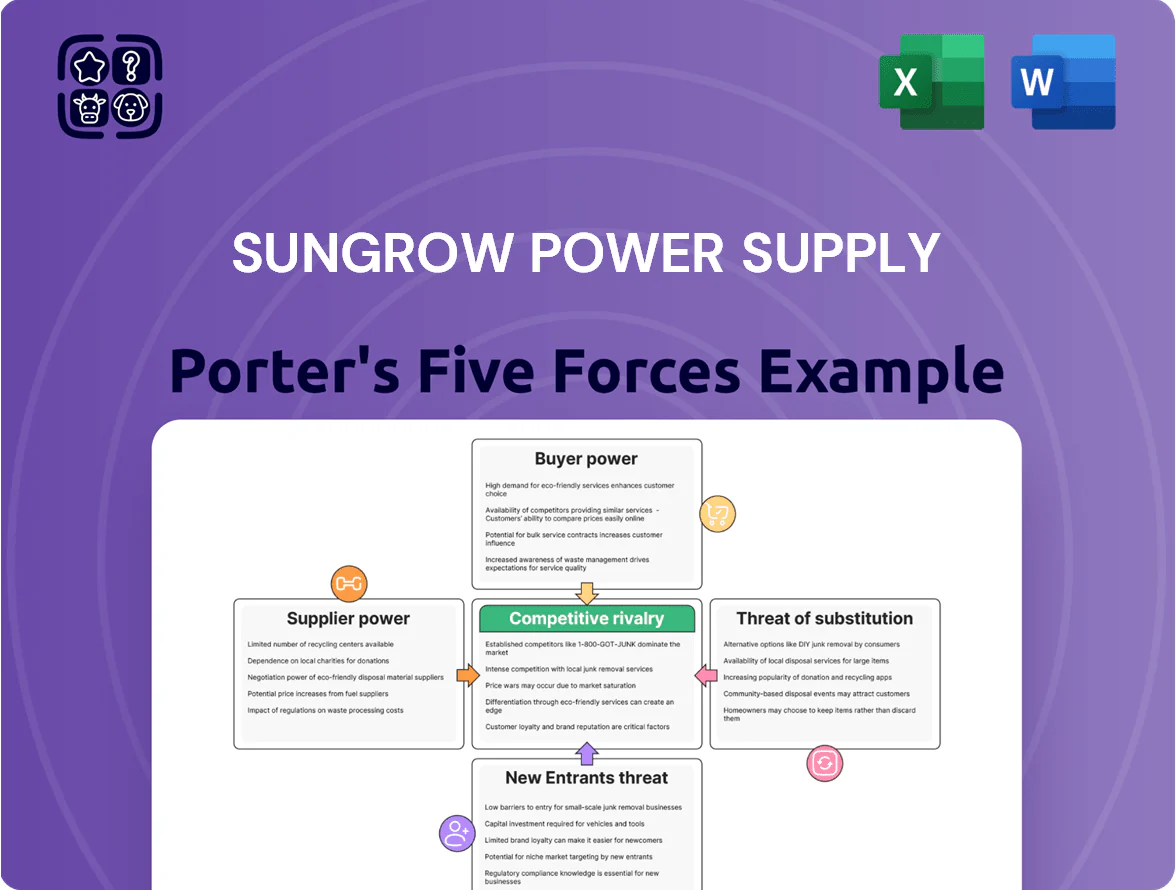

Suppliers Bargaining Power

Semiconductor and IGBT Module Dependency

The production of Sungrow Power Supply inverters and energy storage systems depends heavily on power semiconductors and IGBT modules, a market where 3–5 global players control over 70% of high-end supply as of 2025. Sungrow has diversified suppliers across China, Japan, and Europe, but a 2024–25 global chip shortfall raised IGBT spot prices by ~30%, giving suppliers strong pricing leverage. Any renewed shortage could delay shipments and press gross margins, since IGBTs account for roughly 12–18% of BOM cost in large inverters. Managing long-term contracts and strategic inventory remains critical to stabilize production schedules and costs.

Raw Material Price Volatility

Suppliers of copper, aluminum and lithium-based components push prices with market swings; lithium carbonate rose ~45% in 2021–2022 and averaged $20,000/ton in 2023, feeding into Sungrow Power Supply’s costs. Rising renewable demand tightens supply, so raw-material moves can cut gross margin — Sungrow reported a 2023 gross margin of ~18.6%, sensitive to commodity cycles. The firm uses long-term contracts and hedges but remains exposed to spot swings.

Battery Cell Supply Constraints

Battery cell supply for Sungrow Power’s ESS is controlled by a few tier-one manufacturers—LG Energy Solution, CATL (Contemporary Amperex Technology Co. Ltd.), and Panasonic—who held roughly 60–70% of global lithium-ion cell capacity in 2024, tightening pricing power.

As Sungrow scales ESS revenue (2024 storage revenue ~US$1.1bn), negotiating discounts depends on order volume and multi‑year offtake deals; larger procurements can cut cell cost per kWh by 5–12%.

Supplier power rises when EV makers demand capacity—EV battery demand grew 35% in 2024—so spot shortages or premium pricing can squeeze Sungrow’s margins and delivery timelines.

Vertical Integration of Components

Sungrow has vertically integrated production of key components to cut vendor reliance, covering roughly 15–20% of inverter parts in-house by 2024 while still sourcing specialized electronic parts.

High-performance capacitors and inductors remain hard to substitute; a small set of qualified suppliers controls advanced specs, giving them measurable bargaining power over price and lead times.

Strict technical specs for high-efficiency inverters narrow the vendor pool to likely fewer than 10 global suppliers meeting Sungrow’s 98%+ efficiency targets in 2025.

- In-house parts: 15–20% (2024)

- Qualified suppliers: <10 globally for key specs (2025)

- Efficiency target: 98%+ for premium inverters

- Supplier leverage: higher on caps/inductors, affects lead times/costs

Geopolitical Supply Chain Risks

- 60–80% of inverter components concentrated in East Asia

- 70% global electronics manufacturing in region

- Export controls 2023–25 led to 10–25% cost jumps

- Lead-time spikes to 12–20 weeks

Component concentration, export curbs push costs + lead times—squeezing margins

Suppliers hold medium‑high power: 3–5 IGBT leaders control >70% high‑end supply (2025), IGBTs = 12–18% BOM; battery cells (CATL, LG, Panasonic) = 60–70% capacity (2024); Sungrow in‑houses 15–20% parts (2024). Geopolitics and 2023–25 export curbs raised component costs 10–25% and lead times to 12–20 weeks, pressuring margins and delivery.

| Metric | Value |

|---|---|

| IGBT share (high‑end) | >70% (2025) |

| IGBT BOM | 12–18% |

| Cell capacity | 60–70% (2024) |

| In‑house parts | 15–20% (2024) |

| Cost jump | 10–25% (2023–25) |

| Lead times | 12–20 wks |

What is included in the product

Tailored Porter's Five Forces analysis for Sungrow Power Supply that uncovers competitive intensity, buyer and supplier power, entry barriers, and substitution threats with strategic implications for pricing and profitability.

A concise Porter's Five Forces one-sheet for Sungrow that highlights competitive threats and relief strategies—ideal for quick strategic decisions and boardroom slides.

Customers Bargaining Power

High Concentration of Utility-Scale Buyers

A significant share of Sungrow Power Supply’s 2024 revenue—about 42% per company filings—comes from utility developers and state-owned enterprises that buy in large volumes, giving these customers strong bargaining power.

High-volume buyers push for lower prices, longer warranties, and net-90 or net-180 payment terms, squeezing gross margins; Sungrow reported a 2024 gross margin of ~17.8%.

During tender rounds, buyers can switch to other tier-one inverter suppliers like Huawei or SMA, increasing price competition and forcing Sungrow to offer concessions to win contracts.

Low Switching Costs for Standardized Products

Low switching costs for standardized string and central inverters mean buyers can move quickly: a 2024 IEA report showed inverter vendor churn rates near 18% in commercial PV markets, and a 1–2% higher efficiency or attractive financing (0%–2% APR programs common in 2023–24) often wins deals.

So Sungrow must push product improvements and premium after-sales: the company spent 5.1% of 2024 revenue on R&D and extended warranties, aiming to cut churn and defend market share.

Price Sensitivity in Residential Markets

In residential distributed generation, buyers are price sensitive: global average residential solar system cost fell to about $2.20/W in 2024, but upfront CAPEX remains a barrier, so customers press for lower prices.

With subsidies dropping—rooftop incentives declined in major markets like Germany and Australia since 2022—demand shifts to lower-cost solutions, raising buyer bargaining power.

Sungrow must protect its premium inverter margins (2024 gross margin about 26%) while competing on price in retail channels to avoid losing share.

Increased Information Transparency

The PV industry's maturity has driven strong information transparency: 2024 benchmarking shows top-tier inverter efficiencies cluster 98.5–99.2% and average module-level pricing variance is under 8%, so customers use third-party datasets and rankings to pit Sungrow against Huawei and SMA, boosting buyer leverage and narrowing Sungrow’s ability to charge premiums without clear tech differentiation; in 2025 R&D spend parity (Sungrow ~3.2% of revenue) also tempers premium claims.

- Industry inverter efficiency range: 98.5–99.2%

- Pricing variance across vendors: <8%

- Sungrow R&D ~3.2% of revenue (2025)

- Third-party rankings drive negotiation leverage

Performance-Linked Contractual Demands

Institutional buyers now put strict performance guarantees and liquidated damages into contracts, shifting warranty and operational risk to Sungrow; in 2024 about 30% of large utility-scale PV tenders in China required ≥ Availability 99.5% clauses.

To avoid penalties Sungrow must prove long-term reliability and O&M capabilities, raising lifecycle costs and capital tied to reserves; a single 1% availability shortfall can cost millions on GW-scale projects.

The push for integrated one-stop solutions means customers expect inverters, storage, BESS control, and O&M bundled at flat prices, squeezing margins and increasing bargaining power.

- 30% of 2024 tenders required ≥99.5% availability

- 1% availability shortfall = multi-million USD loss on GW projects

- Bundled one-stop demand compresses margins

Sungrow squeezed: utility buyers compress margins, driving high churn and heavy R&D spend

Large utility/state buyers (≈42% of Sungrow 2024 revenue) wield strong leverage, forcing price cuts, long payment terms, and strict availability warranties (≈30% of 2024 tenders ≥99.5%), squeezing margins (2024 gross margin ~17.8%; premium products ~26%). Low switching costs, tight efficiency band (98.5–99.2%), <8% price variance, and third-party rankings raise churn (~18% vendor churn in 2024 commercial PV), so Sungrow spends ~5.1% of 2024 revenue on R&D/warranties to defend share.

| Metric | Value |

|---|---|

| Utility/state revenue share (2024) | ≈42% |

| Gross margin (2024) | ≈17.8% |

| Premium product margin (2024) | ≈26% |

| Tenders ≥99.5% avail (2024) | ≈30% |

| Vendor churn (2024) | ≈18% |

| Efficiency range | 98.5–99.2% |

| Pricing variance | <8% |

| R&D/warranties spend (2024) | ≈5.1% revenue |

Preview the Actual Deliverable

Sungrow Power Supply Porter's Five Forces Analysis

This preview shows the exact Sungrow Power Supply Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is a fully formatted, ready-to-use file covering competitive rivalry, supplier and buyer power, threats of new entrants and substitutes with data-driven insights.

You're looking at the actual deliverable; once you buy, you'll get instant access to this same professional report for download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Sungrow Power Supply faces moderate rivalry, strong buyer negotiation from project developers, supplier leverage for key components, rising substitute pressure from alternative storage tech, and high barriers for some entrants due to scale and certification—this snapshot highlights strategic pinch points and growth levers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sungrow Power Supply’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor and IGBT Module Dependency

The production of Sungrow Power Supply inverters and energy storage systems depends heavily on power semiconductors and IGBT modules, a market where 3–5 global players control over 70% of high-end supply as of 2025. Sungrow has diversified suppliers across China, Japan, and Europe, but a 2024–25 global chip shortfall raised IGBT spot prices by ~30%, giving suppliers strong pricing leverage. Any renewed shortage could delay shipments and press gross margins, since IGBTs account for roughly 12–18% of BOM cost in large inverters. Managing long-term contracts and strategic inventory remains critical to stabilize production schedules and costs.

Raw Material Price Volatility

Suppliers of copper, aluminum and lithium-based components push prices with market swings; lithium carbonate rose ~45% in 2021–2022 and averaged $20,000/ton in 2023, feeding into Sungrow Power Supply’s costs. Rising renewable demand tightens supply, so raw-material moves can cut gross margin — Sungrow reported a 2023 gross margin of ~18.6%, sensitive to commodity cycles. The firm uses long-term contracts and hedges but remains exposed to spot swings.

Battery Cell Supply Constraints

Battery cell supply for Sungrow Power’s ESS is controlled by a few tier-one manufacturers—LG Energy Solution, CATL (Contemporary Amperex Technology Co. Ltd.), and Panasonic—who held roughly 60–70% of global lithium-ion cell capacity in 2024, tightening pricing power.

As Sungrow scales ESS revenue (2024 storage revenue ~US$1.1bn), negotiating discounts depends on order volume and multi‑year offtake deals; larger procurements can cut cell cost per kWh by 5–12%.

Supplier power rises when EV makers demand capacity—EV battery demand grew 35% in 2024—so spot shortages or premium pricing can squeeze Sungrow’s margins and delivery timelines.

Vertical Integration of Components

Sungrow has vertically integrated production of key components to cut vendor reliance, covering roughly 15–20% of inverter parts in-house by 2024 while still sourcing specialized electronic parts.

High-performance capacitors and inductors remain hard to substitute; a small set of qualified suppliers controls advanced specs, giving them measurable bargaining power over price and lead times.

Strict technical specs for high-efficiency inverters narrow the vendor pool to likely fewer than 10 global suppliers meeting Sungrow’s 98%+ efficiency targets in 2025.

- In-house parts: 15–20% (2024)

- Qualified suppliers: <10 globally for key specs (2025)

- Efficiency target: 98%+ for premium inverters

- Supplier leverage: higher on caps/inductors, affects lead times/costs

Geopolitical Supply Chain Risks

- 60–80% of inverter components concentrated in East Asia

- 70% global electronics manufacturing in region

- Export controls 2023–25 led to 10–25% cost jumps

- Lead-time spikes to 12–20 weeks

Component concentration, export curbs push costs + lead times—squeezing margins

Suppliers hold medium‑high power: 3–5 IGBT leaders control >70% high‑end supply (2025), IGBTs = 12–18% BOM; battery cells (CATL, LG, Panasonic) = 60–70% capacity (2024); Sungrow in‑houses 15–20% parts (2024). Geopolitics and 2023–25 export curbs raised component costs 10–25% and lead times to 12–20 weeks, pressuring margins and delivery.

| Metric | Value |

|---|---|

| IGBT share (high‑end) | >70% (2025) |

| IGBT BOM | 12–18% |

| Cell capacity | 60–70% (2024) |

| In‑house parts | 15–20% (2024) |

| Cost jump | 10–25% (2023–25) |

| Lead times | 12–20 wks |

What is included in the product

Tailored Porter's Five Forces analysis for Sungrow Power Supply that uncovers competitive intensity, buyer and supplier power, entry barriers, and substitution threats with strategic implications for pricing and profitability.

A concise Porter's Five Forces one-sheet for Sungrow that highlights competitive threats and relief strategies—ideal for quick strategic decisions and boardroom slides.

Customers Bargaining Power

High Concentration of Utility-Scale Buyers

A significant share of Sungrow Power Supply’s 2024 revenue—about 42% per company filings—comes from utility developers and state-owned enterprises that buy in large volumes, giving these customers strong bargaining power.

High-volume buyers push for lower prices, longer warranties, and net-90 or net-180 payment terms, squeezing gross margins; Sungrow reported a 2024 gross margin of ~17.8%.

During tender rounds, buyers can switch to other tier-one inverter suppliers like Huawei or SMA, increasing price competition and forcing Sungrow to offer concessions to win contracts.

Low Switching Costs for Standardized Products

Low switching costs for standardized string and central inverters mean buyers can move quickly: a 2024 IEA report showed inverter vendor churn rates near 18% in commercial PV markets, and a 1–2% higher efficiency or attractive financing (0%–2% APR programs common in 2023–24) often wins deals.

So Sungrow must push product improvements and premium after-sales: the company spent 5.1% of 2024 revenue on R&D and extended warranties, aiming to cut churn and defend market share.

Price Sensitivity in Residential Markets

In residential distributed generation, buyers are price sensitive: global average residential solar system cost fell to about $2.20/W in 2024, but upfront CAPEX remains a barrier, so customers press for lower prices.

With subsidies dropping—rooftop incentives declined in major markets like Germany and Australia since 2022—demand shifts to lower-cost solutions, raising buyer bargaining power.

Sungrow must protect its premium inverter margins (2024 gross margin about 26%) while competing on price in retail channels to avoid losing share.

Increased Information Transparency

The PV industry's maturity has driven strong information transparency: 2024 benchmarking shows top-tier inverter efficiencies cluster 98.5–99.2% and average module-level pricing variance is under 8%, so customers use third-party datasets and rankings to pit Sungrow against Huawei and SMA, boosting buyer leverage and narrowing Sungrow’s ability to charge premiums without clear tech differentiation; in 2025 R&D spend parity (Sungrow ~3.2% of revenue) also tempers premium claims.

- Industry inverter efficiency range: 98.5–99.2%

- Pricing variance across vendors: <8%

- Sungrow R&D ~3.2% of revenue (2025)

- Third-party rankings drive negotiation leverage

Performance-Linked Contractual Demands

Institutional buyers now put strict performance guarantees and liquidated damages into contracts, shifting warranty and operational risk to Sungrow; in 2024 about 30% of large utility-scale PV tenders in China required ≥ Availability 99.5% clauses.

To avoid penalties Sungrow must prove long-term reliability and O&M capabilities, raising lifecycle costs and capital tied to reserves; a single 1% availability shortfall can cost millions on GW-scale projects.

The push for integrated one-stop solutions means customers expect inverters, storage, BESS control, and O&M bundled at flat prices, squeezing margins and increasing bargaining power.

- 30% of 2024 tenders required ≥99.5% availability

- 1% availability shortfall = multi-million USD loss on GW projects

- Bundled one-stop demand compresses margins

Sungrow squeezed: utility buyers compress margins, driving high churn and heavy R&D spend

Large utility/state buyers (≈42% of Sungrow 2024 revenue) wield strong leverage, forcing price cuts, long payment terms, and strict availability warranties (≈30% of 2024 tenders ≥99.5%), squeezing margins (2024 gross margin ~17.8%; premium products ~26%). Low switching costs, tight efficiency band (98.5–99.2%), <8% price variance, and third-party rankings raise churn (~18% vendor churn in 2024 commercial PV), so Sungrow spends ~5.1% of 2024 revenue on R&D/warranties to defend share.

| Metric | Value |

|---|---|

| Utility/state revenue share (2024) | ≈42% |

| Gross margin (2024) | ≈17.8% |

| Premium product margin (2024) | ≈26% |

| Tenders ≥99.5% avail (2024) | ≈30% |

| Vendor churn (2024) | ≈18% |

| Efficiency range | 98.5–99.2% |

| Pricing variance | <8% |

| R&D/warranties spend (2024) | ≈5.1% revenue |

Preview the Actual Deliverable

Sungrow Power Supply Porter's Five Forces Analysis

This preview shows the exact Sungrow Power Supply Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is a fully formatted, ready-to-use file covering competitive rivalry, supplier and buyer power, threats of new entrants and substitutes with data-driven insights.

You're looking at the actual deliverable; once you buy, you'll get instant access to this same professional report for download and use.