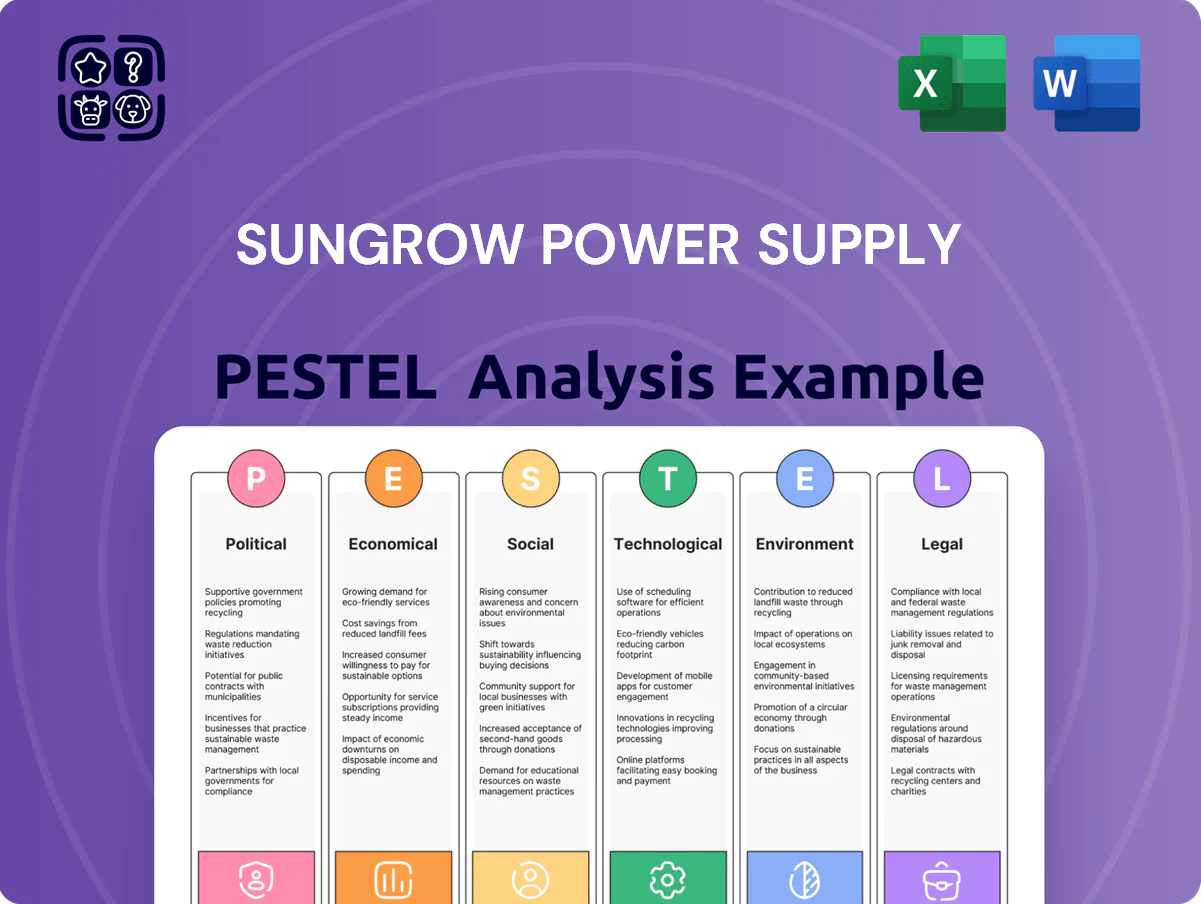

Sungrow Power Supply PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, supply-chain dynamics, and rapid solar-tech innovation are shaping Sungrow Power Supply’s strategic risks and opportunities; our concise PESTLE highlights the external forces you need to track. Purchase the full PESTLE for a sector-specific, actionable roadmap—download ready-to-use insights in Word and Excel to inform investments, pitches, or strategic planning instantly.

Political factors

Geopolitical Trade Tensions

Trade barriers and tariffs by the US and EU on Chinese renewable components have raised Sungrow’s average tariff exposure to an estimated 10–25% on inverter and module shipments, constraining market access in 2024–25 and increasing landed costs.

These measures, aimed at protecting domestic manufacturers, force Sungrow to absorb higher import duties or invest in localized manufacturing; Sungrow reported CAPEX expansion in 2024 to diversify production footprint.

Shifts in international relations have caused supply‑chain cost volatility—raw‑material logistics and freight pushed regional project pricing up by ~5–12% in 2024, affecting demand timing across key markets.

Global Decarbonization Policies

National net-zero pledges aligned with the Paris Agreement underpin demand for PV inverters and storage; as of 2025, 136 countries have net-zero targets, supporting Sungrow’s long-term growth.

Governments deployed over $600 billion in clean energy subsidies and tax incentives in 2024–25, boosting global solar installations 18% YoY and increasing inverter and ESS uptake.

Sungrow, a top inverter supplier with ~16% global market share in 2024, directly benefits from policies accelerating the shift from fossil fuels.

Energy Security Priorities

Many governments now treat renewable infrastructure as national security, driving €120bn+ EU energy sovereignty funds and US IRA incentives toward local storage and grid stability—areas where Sungrow, with 60+ GW global inverter installations, is well positioned.

This policy momentum boosts demand for Sungrow’s batteries and inverters but increases requirements for domestic manufacturing and supply-chain transparency.

Regulators are imposing tighter checks on component origins for critical infrastructure, raising compliance costs and potential localization investments for Sungrow.

Chinese Domestic Industrial Policy

The New Quality Productive Forces initiative channels subsidized loans and tax breaks to green-tech leaders; Sungrow received government-backed R&D grants totaling about CNY 1.2 billion in 2024, boosting inverter and energy-storage development.

Aligning with Beijing’s push for global tech leadership, Sungrow benefits from preferential procurement and domestic market share—China’s renewable equipment exports reached $54.3 billion in 2024, supporting scale.

Home-market support and Belt and Road financing pipelines facilitate international projects; by end-2024 Sungrow had projects in 95 countries, aided by state-backed financing and export credit mechanisms.

- 2024 R&D grants ~CNY 1.2bn

- China renewable equipment exports $54.3bn (2024)

- Projects in 95 countries by 2024

Regulatory Stability in Emerging Markets

- 12 policy reversals in 2024 across target regions

- 2025 goal: 20% revenue from non-China markets

- Mitigation: geographic diversification and local stakeholder engagement

Tariffs, subsidies and localization reshape PV/ESS: Sungrow scales amid $600B+ clean‑energy surge

Political factors: trade tariffs (10–25% on Chinese inverters/modules) and 2024–25 localization rules raise landed costs and compliance; $600B+ global clean-energy subsidies (2024–25) and 136 net‑zero countries drive PV/ESS demand; EU/US energy‑sovereignty funds (€120B+) and China support (CNY1.2B R&D grants) aid Sungrow’s scale but increase localization and supply‑chain scrutiny.

| Metric | 2024–25 |

|---|---|

| Tariff exposure | 10–25% |

| Global clean‑energy subsidies | $600B+ |

| Net‑zero countries | 136 |

| China R&D grants to Sungrow | CNY1.2B |

| EU energy funds / US IRA | €120B+ |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Sungrow Power Supply, with data-backed trends and sector-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Sungrow Power Supply that relieves prep pain by offering an easily shareable, editable snapshot for meetings, presentations, and client reports—ready to drop into slides or strategy packs and tailored with region- or business-specific notes.

Economic factors

Interest Rate Fluctuations

As a capital-intensive industry, renewable energy is highly sensitive to borrowing costs; global policy rate hikes in 2022–2023 pushed weighted average cost of capital on utility-scale solar projects above 6–8%, slowing new builds. High rates deter developers by raising levelized cost of energy and project IRRs, delaying purchases of Sungrow inverters and storage. A shift toward lower rates in 2024–2025—real policy easing across major central banks trimming term lending by ~50–150 bps—would likely boost demand for Sungrow’s equipment as financing becomes cheaper. Sungrow’s 2024 backlog and Q3 2025 order flows would benefit materially from renewed project initiation.

Raw Material Price Volatility

The profitability of Sungrow’s energy storage arm is tightly tied to lithium, copper and semiconductor prices; lithium carbonate averaged about $45,000/ton in 2025 while copper was near $9,000/ton, and semiconductor shortages lifted module costs by roughly 12% in 2024, so cost swings can compress margins if not passed to customers.

Currency Exchange Rate Risks

With over 60% of 2024 revenue from overseas markets, Sungrow faces Renminbi volatility versus the US dollar and euro; a 5% RMB depreciation in 2023 reduced reported USD revenue by roughly 3–4% for comparable sales volumes.

Large swings can erode export competitiveness and alter the USD/EUR valuation of foreign subsidiaries, affecting net income and ROE.

Sungrow employs forward contracts and currency swaps—hedging ~40–60% of anticipated FX exposure in recent years—to stabilize margins.

Global Inflationary Pressures

Persistent global inflation raised input costs; raw material and freight inflation added ~8–12% to inverter manufacturing costs in 2022–2024, pressuring Sungrow’s cost-leadership margins.

Higher fossil fuel prices bolster solar demand, but 2024 real wage erosion and higher mortgage costs slowed residential PV uptake in key markets by ~3–5% year-over-year.

Maintaining premium tech while cutting unit costs through scale and localized production is crucial to protect ASPs and 2024 gross margins (reported ~15–18%).

- Input/logistics inflation +8–12% (2022–24)

- Residential PV adoption -3–5% YoY in 2024 in some markets

- Sungrow 2024 gross margin ~15–18%

Growth of the Green Finance Market

The proliferation of green bonds and ESG-linked loans unlocked over USD 1.2 trillion in sustainable finance in 2024, giving Sungrow and its utility-scale clients access to lower-cost, specialized capital that can reduce WACC by an estimated 100–250 bps on large renewable projects, improving project IRRs and making Sungrow’s inverters and storage solutions more competitive.

The maturation of compliance and voluntary carbon markets—valued at ~USD 2.6 billion (compliance) and USD 1.3 billion (voluntary) in 2024—creates secondary revenue for project owners via carbon credits and offtake-linked products, indirectly raising demand for Sungrow equipment through enhanced project economics and financing structures.

- 2024 sustainable finance: USD 1.2 trillion

- WACC reduction potential: 100–250 bps

- Compliance carbon market 2024: ~USD 2.6 billion

- Voluntary carbon market 2024: ~USD 1.3 billion

Macro shocks to margins: commodity, rates, FX & sustainable finance reshaping WACC

Economic factors: rate-driven financing swings (WACCs rose >6–8% in 2022–23; easing trimmed policy rates ~50–150 bps in 2024–25), commodity cost volatility (Li2CO3 ~$45k/ton in 2025; Cu ~$9k/ton), RMB FX risk (5% depreciation → ~3–4% USD revenue hit), input inflation +8–12% (2022–24), sustainable finance USD1.2T (2024) cutting WACC 100–250bps.

| Metric | Value |

|---|---|

| Li2CO3 2025 | $45,000/t |

| Copper 2025 | $9,000/t |

| Input inflation | +8–12% |

| Sustainable finance 2024 | $1.2T |

Full Version Awaits

Sungrow Power Supply PESTLE Analysis

The preview shown here is the exact Sungrow Power Supply PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in the preview are the same file you’ll be able to download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, supply-chain dynamics, and rapid solar-tech innovation are shaping Sungrow Power Supply’s strategic risks and opportunities; our concise PESTLE highlights the external forces you need to track. Purchase the full PESTLE for a sector-specific, actionable roadmap—download ready-to-use insights in Word and Excel to inform investments, pitches, or strategic planning instantly.

Political factors

Geopolitical Trade Tensions

Trade barriers and tariffs by the US and EU on Chinese renewable components have raised Sungrow’s average tariff exposure to an estimated 10–25% on inverter and module shipments, constraining market access in 2024–25 and increasing landed costs.

These measures, aimed at protecting domestic manufacturers, force Sungrow to absorb higher import duties or invest in localized manufacturing; Sungrow reported CAPEX expansion in 2024 to diversify production footprint.

Shifts in international relations have caused supply‑chain cost volatility—raw‑material logistics and freight pushed regional project pricing up by ~5–12% in 2024, affecting demand timing across key markets.

Global Decarbonization Policies

National net-zero pledges aligned with the Paris Agreement underpin demand for PV inverters and storage; as of 2025, 136 countries have net-zero targets, supporting Sungrow’s long-term growth.

Governments deployed over $600 billion in clean energy subsidies and tax incentives in 2024–25, boosting global solar installations 18% YoY and increasing inverter and ESS uptake.

Sungrow, a top inverter supplier with ~16% global market share in 2024, directly benefits from policies accelerating the shift from fossil fuels.

Energy Security Priorities

Many governments now treat renewable infrastructure as national security, driving €120bn+ EU energy sovereignty funds and US IRA incentives toward local storage and grid stability—areas where Sungrow, with 60+ GW global inverter installations, is well positioned.

This policy momentum boosts demand for Sungrow’s batteries and inverters but increases requirements for domestic manufacturing and supply-chain transparency.

Regulators are imposing tighter checks on component origins for critical infrastructure, raising compliance costs and potential localization investments for Sungrow.

Chinese Domestic Industrial Policy

The New Quality Productive Forces initiative channels subsidized loans and tax breaks to green-tech leaders; Sungrow received government-backed R&D grants totaling about CNY 1.2 billion in 2024, boosting inverter and energy-storage development.

Aligning with Beijing’s push for global tech leadership, Sungrow benefits from preferential procurement and domestic market share—China’s renewable equipment exports reached $54.3 billion in 2024, supporting scale.

Home-market support and Belt and Road financing pipelines facilitate international projects; by end-2024 Sungrow had projects in 95 countries, aided by state-backed financing and export credit mechanisms.

- 2024 R&D grants ~CNY 1.2bn

- China renewable equipment exports $54.3bn (2024)

- Projects in 95 countries by 2024

Regulatory Stability in Emerging Markets

- 12 policy reversals in 2024 across target regions

- 2025 goal: 20% revenue from non-China markets

- Mitigation: geographic diversification and local stakeholder engagement

Tariffs, subsidies and localization reshape PV/ESS: Sungrow scales amid $600B+ clean‑energy surge

Political factors: trade tariffs (10–25% on Chinese inverters/modules) and 2024–25 localization rules raise landed costs and compliance; $600B+ global clean-energy subsidies (2024–25) and 136 net‑zero countries drive PV/ESS demand; EU/US energy‑sovereignty funds (€120B+) and China support (CNY1.2B R&D grants) aid Sungrow’s scale but increase localization and supply‑chain scrutiny.

| Metric | 2024–25 |

|---|---|

| Tariff exposure | 10–25% |

| Global clean‑energy subsidies | $600B+ |

| Net‑zero countries | 136 |

| China R&D grants to Sungrow | CNY1.2B |

| EU energy funds / US IRA | €120B+ |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Sungrow Power Supply, with data-backed trends and sector-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for Sungrow Power Supply that relieves prep pain by offering an easily shareable, editable snapshot for meetings, presentations, and client reports—ready to drop into slides or strategy packs and tailored with region- or business-specific notes.

Economic factors

Interest Rate Fluctuations

As a capital-intensive industry, renewable energy is highly sensitive to borrowing costs; global policy rate hikes in 2022–2023 pushed weighted average cost of capital on utility-scale solar projects above 6–8%, slowing new builds. High rates deter developers by raising levelized cost of energy and project IRRs, delaying purchases of Sungrow inverters and storage. A shift toward lower rates in 2024–2025—real policy easing across major central banks trimming term lending by ~50–150 bps—would likely boost demand for Sungrow’s equipment as financing becomes cheaper. Sungrow’s 2024 backlog and Q3 2025 order flows would benefit materially from renewed project initiation.

Raw Material Price Volatility

The profitability of Sungrow’s energy storage arm is tightly tied to lithium, copper and semiconductor prices; lithium carbonate averaged about $45,000/ton in 2025 while copper was near $9,000/ton, and semiconductor shortages lifted module costs by roughly 12% in 2024, so cost swings can compress margins if not passed to customers.

Currency Exchange Rate Risks

With over 60% of 2024 revenue from overseas markets, Sungrow faces Renminbi volatility versus the US dollar and euro; a 5% RMB depreciation in 2023 reduced reported USD revenue by roughly 3–4% for comparable sales volumes.

Large swings can erode export competitiveness and alter the USD/EUR valuation of foreign subsidiaries, affecting net income and ROE.

Sungrow employs forward contracts and currency swaps—hedging ~40–60% of anticipated FX exposure in recent years—to stabilize margins.

Global Inflationary Pressures

Persistent global inflation raised input costs; raw material and freight inflation added ~8–12% to inverter manufacturing costs in 2022–2024, pressuring Sungrow’s cost-leadership margins.

Higher fossil fuel prices bolster solar demand, but 2024 real wage erosion and higher mortgage costs slowed residential PV uptake in key markets by ~3–5% year-over-year.

Maintaining premium tech while cutting unit costs through scale and localized production is crucial to protect ASPs and 2024 gross margins (reported ~15–18%).

- Input/logistics inflation +8–12% (2022–24)

- Residential PV adoption -3–5% YoY in 2024 in some markets

- Sungrow 2024 gross margin ~15–18%

Growth of the Green Finance Market

The proliferation of green bonds and ESG-linked loans unlocked over USD 1.2 trillion in sustainable finance in 2024, giving Sungrow and its utility-scale clients access to lower-cost, specialized capital that can reduce WACC by an estimated 100–250 bps on large renewable projects, improving project IRRs and making Sungrow’s inverters and storage solutions more competitive.

The maturation of compliance and voluntary carbon markets—valued at ~USD 2.6 billion (compliance) and USD 1.3 billion (voluntary) in 2024—creates secondary revenue for project owners via carbon credits and offtake-linked products, indirectly raising demand for Sungrow equipment through enhanced project economics and financing structures.

- 2024 sustainable finance: USD 1.2 trillion

- WACC reduction potential: 100–250 bps

- Compliance carbon market 2024: ~USD 2.6 billion

- Voluntary carbon market 2024: ~USD 1.3 billion

Macro shocks to margins: commodity, rates, FX & sustainable finance reshaping WACC

Economic factors: rate-driven financing swings (WACCs rose >6–8% in 2022–23; easing trimmed policy rates ~50–150 bps in 2024–25), commodity cost volatility (Li2CO3 ~$45k/ton in 2025; Cu ~$9k/ton), RMB FX risk (5% depreciation → ~3–4% USD revenue hit), input inflation +8–12% (2022–24), sustainable finance USD1.2T (2024) cutting WACC 100–250bps.

| Metric | Value |

|---|---|

| Li2CO3 2025 | $45,000/t |

| Copper 2025 | $9,000/t |

| Input inflation | +8–12% |

| Sustainable finance 2024 | $1.2T |

Full Version Awaits

Sungrow Power Supply PESTLE Analysis

The preview shown here is the exact Sungrow Power Supply PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in the preview are the same file you’ll be able to download immediately after payment.