Sun Pharma Industries Boston Consulting Group Matrix

Unlock Strategic Clarity

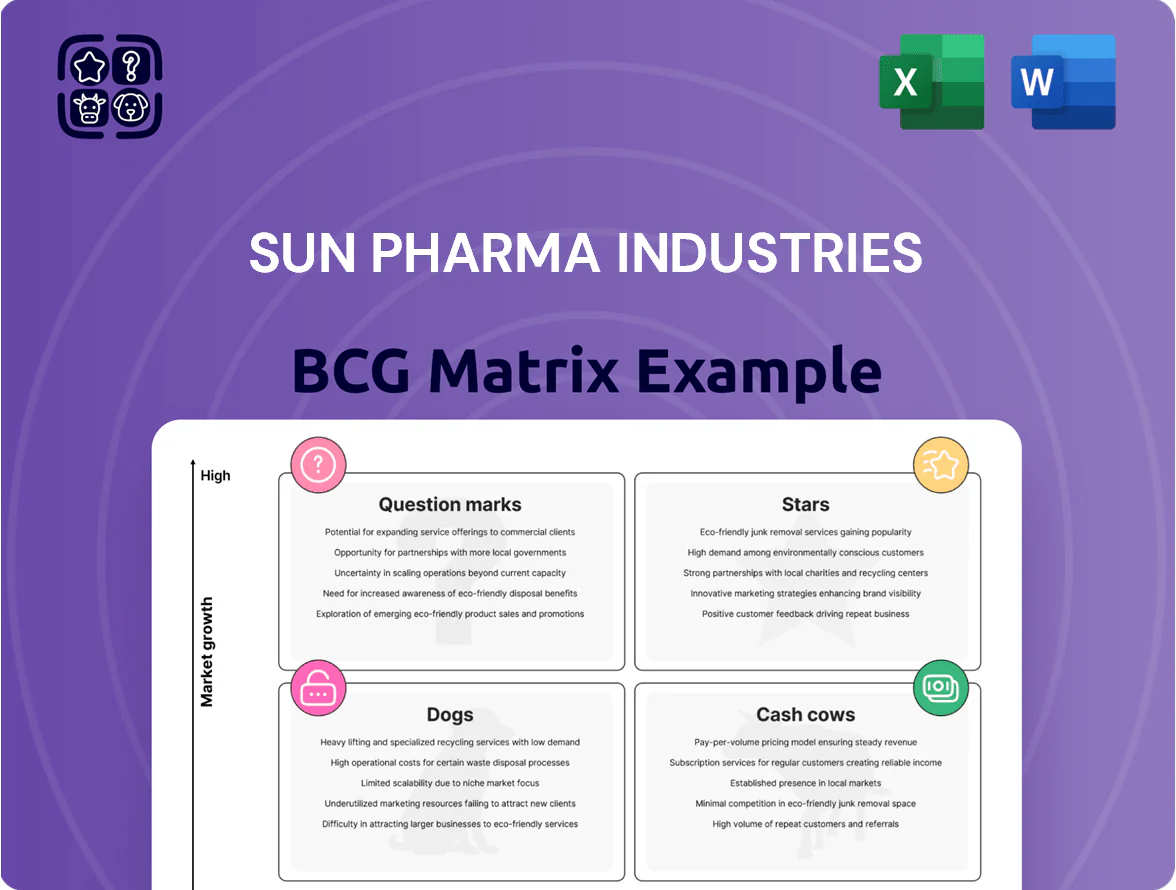

Sun Pharma’s BCG Matrix preview highlights its mix of high-growth specialty APIs and mature dermatology franchises—showing where leadership, investment, or divestment decisions are most critical as the pharma landscape shifts. Purchase the full BCG Matrix for quadrant-level placements, revenue and market-share drivers, and actionable recommendations tailored to R&D, portfolio pruning, and capital allocation. Get the complete Word report plus an Excel summary to present and execute strategy with clarity.

Stars

Global Specialty Portfolio

As of late 2025, Sun Pharma’s Global Specialty Portfolio—led by Ilumya (dermatology), Cequa (ophthalmology) and Winlevi (acne)—shows high growth and strong market share across key markets, with specialty now contributing nearly 20% of consolidated revenues (≈USD 1.9–2.1 billion in 2025). These brands need continued R&D and global marketing spend—ongoing Phase IV/label-expansion studies and promotion—to fend off emerging biologics and generics. Given sustained double-digit CAGR in specialty sales since 2022, the segment is shifting from growth engine toward a future cash pillar, but sustained investment is required to preserve pricing and market access.

Dermatology Segment Leadership

Sun Pharma holds a leading global dermatology position, driven by ~35% share in branded topical treatments and strong sales from Taro and its specialty acne and psoriasis portfolio, contributing ~₹6,200 crore (≈$750M) in FY2024 dermatology revenue.

Market growth runs ~6–8% CAGR to 2028, high regulatory and formulation barriers let Sun command premium pricing and ~25–30% gross margins in key dermatology SKUs.

Sun invests ~₹1,000–1,200 crore yearly in dermatology R&D (2023–24) to defend vs new molecular entities from Novartis, LEO Pharma and Galderma; ongoing pipeline additions are critical to retain share.

Taro Pharmaceutical Integration

With Taro fully integrated in 2025, Sun Pharma holds an estimated >30% share of the US generic topical market, cementing its Star status in the BCG matrix.

The segment grows ~8–10% CAGR for complex generics (2022–2027), and Sun plans $200–250M capex through 2026 for sterile/OTC upgrades and US-FDA compliance.

Combined sales from Taro topical portfolio and Sun’s global channels are projected to drive $450–600M annual revenue by 2026, making it a primary revenue engine.

Chronic Therapy in Emerging Markets

Sun Pharma’s move into chronic areas like oncology and neuro-sciences in emerging markets is a high-growth, high-share play, with management targeting double-digit CAGR in these segments and oncology sales rising ~22% YoY in FY2024.

Improving regional healthcare—per-capita health spend up ~6% annually in EMs through 2024—fuels demand for advanced chronic therapies, expanding addressable patients by millions.

Sun Pharma is investing in local distribution and supply chains, allocating several hundred million dollars since 2022 to capture market share and scale patient access.

- Oncology sales +22% YoY (FY2024)

- EM per-capita health spend +6% CAGR to 2024

- Hundreds of $mn invested in local distribution since 2022

Advanced Complex Generics

Sun Pharma’s Advanced Complex Generics, centered on complex injectables and inhalation, target a fast-growing niche—global complex generics market projected at $30bn by 2025—where few rivals compete due to technical barriers.

These products deliver high market share and strong cash flows; Sun reported formulation revenues of ~$1.8bn in FY2024, with specialty complex injectables driving margins above corporate average.

High capex for specialized plants and costly bioequivalence (BE) studies—BE trials often >$2–5m per product—keep these offerings in the Star quadrant despite strong returns.

- High-growth niche: complex generics market ≈$30bn (2025)

- Strong market share: injectables/inhalation key to Sun’s ~$1.8bn formulation sales (FY2024)

- Cash generators but capex-heavy: BE studies $2–5m each; specialized facilities costly

Sun Pharma: Specialty, Dermatology & Injectables Fuel $1.9–2.1B Specialty Surge

Stars: Sun Pharma’s specialty dermatology, Taro topical portfolio and complex injectables show high growth (8–12% CAGR) and leading share—specialty ≈$2.0B (2025), dermatology ≈₹6,200 crore FY2024, formulation sales ~$1.8B FY2024; capex $200–250M to 2026; R&D ₹1,000–1,200 crore/yr (2023–24).

| Metric | Value |

|---|---|

| Specialty revenue 2025 | $1.9–2.1B |

| Dermatology FY2024 | ₹6,200 crore (~$750M) |

| Formulation sales FY2024 | $1.8B |

| R&D (2023–24) | ₹1,000–1,200 crore/yr |

| Capex to 2026 | $200–250M |

What is included in the product

BCG Matrix review of Sun Pharma: quadrant-by-quadrant strategic insights, investment/hold/divest recommendations, and trend-driven risk/opportunity notes.

One-page BCG matrix placing Sun Pharma business units into clear quadrants for quick strategic decisions and investor briefings

Cash Cows

India Domestic Formulations

Sun Pharma leads India’s pharmaceutical market with a >8% market share (IMS Health, 2025), anchoring a mature domestic formulations franchise that produced approximately INR 28,500 crore in FY2024-25 revenue, making it a prime cash cow.

The branded generics base yields high free cash flow and needs relatively low incremental marketing spend versus new launches, supporting >INR 4,500 crore annual R&D funding for global specialty programs.

Generic Cardiology Portfolio

Sun Pharma’s Generic Cardiology Portfolio is a cash cow: in FY2024 it delivered ~INR 3,400 crore revenue (≈USD 410m) with operating margins around 28%, reflecting stable market share in a mature Indian cardiology market growing ~3% annually.

Low volume growth but high margins come from scale manufacturing and physician trust; free cash flow funds debt reduction (net debt fell 12% in 2024) and paid for specialty M&A such as the 2023 acquisition of Caraco-related assets.

Active Pharmaceutical Ingredients (API)

The Active Pharmaceutical Ingredients (API) unit at Sun Pharma holds a dominant market share in a slow-growing global API market estimated at USD 173 billion in 2024, delivering steady cash flow from high-volume, low-margin sales.

By running cost-efficient plants—Sun Pharma reported consolidated manufacturing margin of ~24% in FY2024—the unit secures internal supply, lowers COGS, and supports group margins.

Minimal promotional spend is needed; the business focuses on operational excellence and environmental compliance, where capital upkeep and ESG investments of ~$40–60 million annually preserve licence-to-operate and cash generation.

Psychiatry and Neurology Brands

Sun Pharma’s psychiatry and neurology brands are long-standing cash cows, holding leading market shares in India (combined CNS market share ~28% as of FY2024) and strong positions in semi-regulated markets, delivering predictable revenues of roughly INR 1,400–1,600 crore annually from these portfolios in 2024.

Growth has plateaued—annual volume growth ~1–3%—but high brand loyalty and pricing power sustain margins near company average, funding R&D and commercialization of higher-growth Question Marks.

These stable cash flows underwrite launches and scale-up costs for pipeline assets and biosimilars, enabling conversion of select Question Marks into Stars without tapping external debt.

- Leading CNS share ~28% (FY2024)

- Revenue from psychiatry/neurology ~INR 1.4–1.6k crore (2024)

- Volume growth 1–3% annually

- Makes internal funding for pipeline scale-up possible

Gastroenterology Mature Products

The gastroenterology mature-products portfolio at Sun Pharma Industries generates steady cash with estimated annual revenues around INR 1.2–1.5 billion (FY2024) from high penetration in both rural and urban markets.

Low capex needs and stable gross margins near 55% make these SKUs reliable cash cows, requiring mainly maintenance capex to sustain market share.

Their reach is supported by Sun Pharma’s 2000+ distributor network and >40,000 retail touchpoints, keeping competitive threats manageable with modest sales spend.

- Revenue FY2024 ~INR 1.2–1.5B

- Gross margin ~55%

- Distributor reach 2000+

- Retail touchpoints 40,000+

- Capex: maintenance-level only

Sun Pharma: Indian formulations & APIs drive cash flow — strong margins, big R&D war chest

Sun Pharma’s Indian branded generics and APIs are cash cows: FY2024-25 domestic formulations ~INR 28,500 crore; cardiology ~INR 3,400 crore (28% margin); CNS ~INR 1,400–1,600 crore; gastro ~INR 120–150 crore; consolidated manufacturing margin ~24%; annual ESG/capex upkeep ~INR 300–450 crore; free cash funds R&D >INR 4,500 crore and cut net debt 12% in 2024.

| Segment | FY2024(₹ crore) | Margin/% |

|---|---|---|

| Domestic formulations | 28,500 | — |

| Cardiology | 3,400 | 28% |

| CNS | 1,400–1,600 | ≈Company avg |

| Gastro | 120–150 | 55% gross |

| API | — | Low-margin, high-volume |

What You’re Viewing Is Included

Sun Pharma Industries BCG Matrix

The Sun Pharma Industries BCG Matrix you're previewing on this page is the exact final file you'll receive after purchase—no watermarks, no demo content—just a fully formatted, strategy-ready report tailored for clear portfolio analysis. This preview mirrors the downloadable report, crafted with market-backed insights and professional layout, delivered immediately to your inbox. Once purchased, the document is yours to edit, print, or present without further changes.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Sun Pharma’s BCG Matrix preview highlights its mix of high-growth specialty APIs and mature dermatology franchises—showing where leadership, investment, or divestment decisions are most critical as the pharma landscape shifts. Purchase the full BCG Matrix for quadrant-level placements, revenue and market-share drivers, and actionable recommendations tailored to R&D, portfolio pruning, and capital allocation. Get the complete Word report plus an Excel summary to present and execute strategy with clarity.

Stars

Global Specialty Portfolio

As of late 2025, Sun Pharma’s Global Specialty Portfolio—led by Ilumya (dermatology), Cequa (ophthalmology) and Winlevi (acne)—shows high growth and strong market share across key markets, with specialty now contributing nearly 20% of consolidated revenues (≈USD 1.9–2.1 billion in 2025). These brands need continued R&D and global marketing spend—ongoing Phase IV/label-expansion studies and promotion—to fend off emerging biologics and generics. Given sustained double-digit CAGR in specialty sales since 2022, the segment is shifting from growth engine toward a future cash pillar, but sustained investment is required to preserve pricing and market access.

Dermatology Segment Leadership

Sun Pharma holds a leading global dermatology position, driven by ~35% share in branded topical treatments and strong sales from Taro and its specialty acne and psoriasis portfolio, contributing ~₹6,200 crore (≈$750M) in FY2024 dermatology revenue.

Market growth runs ~6–8% CAGR to 2028, high regulatory and formulation barriers let Sun command premium pricing and ~25–30% gross margins in key dermatology SKUs.

Sun invests ~₹1,000–1,200 crore yearly in dermatology R&D (2023–24) to defend vs new molecular entities from Novartis, LEO Pharma and Galderma; ongoing pipeline additions are critical to retain share.

Taro Pharmaceutical Integration

With Taro fully integrated in 2025, Sun Pharma holds an estimated >30% share of the US generic topical market, cementing its Star status in the BCG matrix.

The segment grows ~8–10% CAGR for complex generics (2022–2027), and Sun plans $200–250M capex through 2026 for sterile/OTC upgrades and US-FDA compliance.

Combined sales from Taro topical portfolio and Sun’s global channels are projected to drive $450–600M annual revenue by 2026, making it a primary revenue engine.

Chronic Therapy in Emerging Markets

Sun Pharma’s move into chronic areas like oncology and neuro-sciences in emerging markets is a high-growth, high-share play, with management targeting double-digit CAGR in these segments and oncology sales rising ~22% YoY in FY2024.

Improving regional healthcare—per-capita health spend up ~6% annually in EMs through 2024—fuels demand for advanced chronic therapies, expanding addressable patients by millions.

Sun Pharma is investing in local distribution and supply chains, allocating several hundred million dollars since 2022 to capture market share and scale patient access.

- Oncology sales +22% YoY (FY2024)

- EM per-capita health spend +6% CAGR to 2024

- Hundreds of $mn invested in local distribution since 2022

Advanced Complex Generics

Sun Pharma’s Advanced Complex Generics, centered on complex injectables and inhalation, target a fast-growing niche—global complex generics market projected at $30bn by 2025—where few rivals compete due to technical barriers.

These products deliver high market share and strong cash flows; Sun reported formulation revenues of ~$1.8bn in FY2024, with specialty complex injectables driving margins above corporate average.

High capex for specialized plants and costly bioequivalence (BE) studies—BE trials often >$2–5m per product—keep these offerings in the Star quadrant despite strong returns.

- High-growth niche: complex generics market ≈$30bn (2025)

- Strong market share: injectables/inhalation key to Sun’s ~$1.8bn formulation sales (FY2024)

- Cash generators but capex-heavy: BE studies $2–5m each; specialized facilities costly

Sun Pharma: Specialty, Dermatology & Injectables Fuel $1.9–2.1B Specialty Surge

Stars: Sun Pharma’s specialty dermatology, Taro topical portfolio and complex injectables show high growth (8–12% CAGR) and leading share—specialty ≈$2.0B (2025), dermatology ≈₹6,200 crore FY2024, formulation sales ~$1.8B FY2024; capex $200–250M to 2026; R&D ₹1,000–1,200 crore/yr (2023–24).

| Metric | Value |

|---|---|

| Specialty revenue 2025 | $1.9–2.1B |

| Dermatology FY2024 | ₹6,200 crore (~$750M) |

| Formulation sales FY2024 | $1.8B |

| R&D (2023–24) | ₹1,000–1,200 crore/yr |

| Capex to 2026 | $200–250M |

What is included in the product

BCG Matrix review of Sun Pharma: quadrant-by-quadrant strategic insights, investment/hold/divest recommendations, and trend-driven risk/opportunity notes.

One-page BCG matrix placing Sun Pharma business units into clear quadrants for quick strategic decisions and investor briefings

Cash Cows

India Domestic Formulations

Sun Pharma leads India’s pharmaceutical market with a >8% market share (IMS Health, 2025), anchoring a mature domestic formulations franchise that produced approximately INR 28,500 crore in FY2024-25 revenue, making it a prime cash cow.

The branded generics base yields high free cash flow and needs relatively low incremental marketing spend versus new launches, supporting >INR 4,500 crore annual R&D funding for global specialty programs.

Generic Cardiology Portfolio

Sun Pharma’s Generic Cardiology Portfolio is a cash cow: in FY2024 it delivered ~INR 3,400 crore revenue (≈USD 410m) with operating margins around 28%, reflecting stable market share in a mature Indian cardiology market growing ~3% annually.

Low volume growth but high margins come from scale manufacturing and physician trust; free cash flow funds debt reduction (net debt fell 12% in 2024) and paid for specialty M&A such as the 2023 acquisition of Caraco-related assets.

Active Pharmaceutical Ingredients (API)

The Active Pharmaceutical Ingredients (API) unit at Sun Pharma holds a dominant market share in a slow-growing global API market estimated at USD 173 billion in 2024, delivering steady cash flow from high-volume, low-margin sales.

By running cost-efficient plants—Sun Pharma reported consolidated manufacturing margin of ~24% in FY2024—the unit secures internal supply, lowers COGS, and supports group margins.

Minimal promotional spend is needed; the business focuses on operational excellence and environmental compliance, where capital upkeep and ESG investments of ~$40–60 million annually preserve licence-to-operate and cash generation.

Psychiatry and Neurology Brands

Sun Pharma’s psychiatry and neurology brands are long-standing cash cows, holding leading market shares in India (combined CNS market share ~28% as of FY2024) and strong positions in semi-regulated markets, delivering predictable revenues of roughly INR 1,400–1,600 crore annually from these portfolios in 2024.

Growth has plateaued—annual volume growth ~1–3%—but high brand loyalty and pricing power sustain margins near company average, funding R&D and commercialization of higher-growth Question Marks.

These stable cash flows underwrite launches and scale-up costs for pipeline assets and biosimilars, enabling conversion of select Question Marks into Stars without tapping external debt.

- Leading CNS share ~28% (FY2024)

- Revenue from psychiatry/neurology ~INR 1.4–1.6k crore (2024)

- Volume growth 1–3% annually

- Makes internal funding for pipeline scale-up possible

Gastroenterology Mature Products

The gastroenterology mature-products portfolio at Sun Pharma Industries generates steady cash with estimated annual revenues around INR 1.2–1.5 billion (FY2024) from high penetration in both rural and urban markets.

Low capex needs and stable gross margins near 55% make these SKUs reliable cash cows, requiring mainly maintenance capex to sustain market share.

Their reach is supported by Sun Pharma’s 2000+ distributor network and >40,000 retail touchpoints, keeping competitive threats manageable with modest sales spend.

- Revenue FY2024 ~INR 1.2–1.5B

- Gross margin ~55%

- Distributor reach 2000+

- Retail touchpoints 40,000+

- Capex: maintenance-level only

Sun Pharma: Indian formulations & APIs drive cash flow — strong margins, big R&D war chest

Sun Pharma’s Indian branded generics and APIs are cash cows: FY2024-25 domestic formulations ~INR 28,500 crore; cardiology ~INR 3,400 crore (28% margin); CNS ~INR 1,400–1,600 crore; gastro ~INR 120–150 crore; consolidated manufacturing margin ~24%; annual ESG/capex upkeep ~INR 300–450 crore; free cash funds R&D >INR 4,500 crore and cut net debt 12% in 2024.

| Segment | FY2024(₹ crore) | Margin/% |

|---|---|---|

| Domestic formulations | 28,500 | — |

| Cardiology | 3,400 | 28% |

| CNS | 1,400–1,600 | ≈Company avg |

| Gastro | 120–150 | 55% gross |

| API | — | Low-margin, high-volume |

What You’re Viewing Is Included

Sun Pharma Industries BCG Matrix

The Sun Pharma Industries BCG Matrix you're previewing on this page is the exact final file you'll receive after purchase—no watermarks, no demo content—just a fully formatted, strategy-ready report tailored for clear portfolio analysis. This preview mirrors the downloadable report, crafted with market-backed insights and professional layout, delivered immediately to your inbox. Once purchased, the document is yours to edit, print, or present without further changes.