Suntory Beverage & Food PESTLE Analysis

Your Competitive Advantage Starts with This Report

Uncover how regulatory shifts, consumer trends, and technological innovation are reshaping Suntory Beverage & Food’s competitive landscape; our PESTLE snapshot highlights key risks and opportunities to inform smarter strategy and investments—buy the full analysis for a complete, actionable briefing you can use immediately.

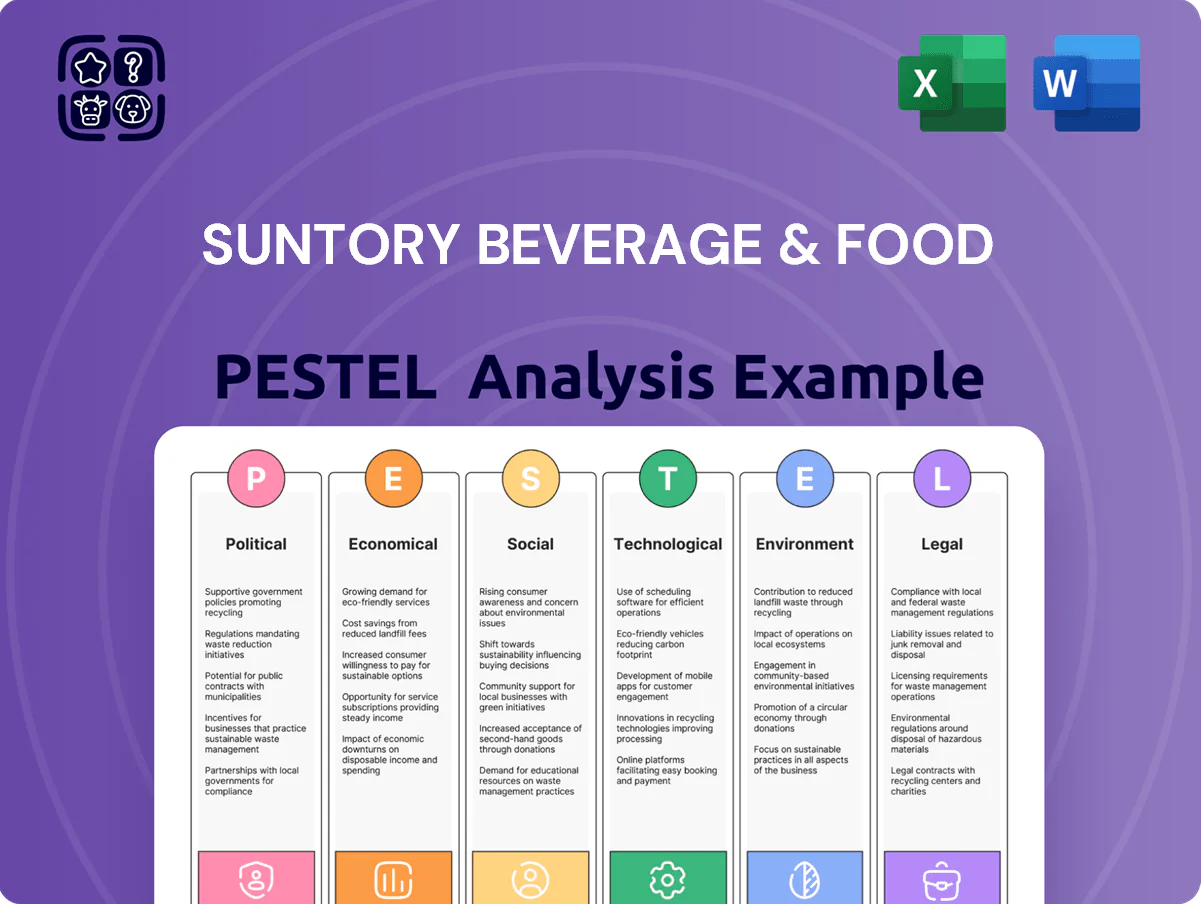

Political factors

Geopolitical instability in key markets

Ongoing geopolitical tensions in Europe and parts of Asia force Suntory to keep agile supply chains; 2024 trade disruptions raised logistics costs ~7% for global beverage firms, prompting contingency routing for Lucozade and Ribena inputs.

Shifting alliances and sanctions risk raw-material access—e.g., concentrate and sugar—potentially affecting 2024 input cost exposure tied to ~12% of COGS for beverage divisions.

Strategic diversification of production—expanding regional plants and contract bottling—remains a priority to buffer localized unrest and preserve FY2025 volume targets.

Global trade policies and tariffs

Changes in international trade agreements and protective tariffs on beverages or ingredients can raise Suntory Beverage & Food’s COGS; a 10% tariff on imported concentrates could add roughly JPY 5–10 billion annually given 2024 ingredient import levels. The company closely monitors Japan’s bilateral trade with China, ASEAN and the US to fine-tune pricing and hedging; in 2024 exports comprised about 18% of group revenue. Fluctuating duties on sugar and fruit concentrates have prompted Suntory to engage trade regulators proactively to mitigate duty volatility.

Taxation on sugar-sweetened beverages

Government moves to expand sugar taxes—over 40 countries globally and recent hikes in parts of Europe and Southeast Asia raising rates by up to 20–30% since 2022—force Suntory Beverage & Food to reformulate and adjust retail pricing; the group accelerated launches of low-sugar and functional lines, which now represent an increasing share of portfolio revenue (company reported 2024 non-ALC health beverage growth of mid-single digits), reducing tax exposure. Maintaining proactive policy engagement helps the firm forecast fiscal shifts and mitigate margin impact.

Stricter marketing regulations to minors

Political pressure to restrict advertising of high-calorie or caffeinated drinks to minors is rising: over 30 countries tightened youth-targeted marketing rules by 2024, and the WHO recommends limits for sugary beverages.

Suntory must ensure campaigns for BOSS Coffee and Orangina meet evolving regional standards to avoid fines and reputational loss; non-compliance risks fines up to several million dollars in some jurisdictions.

This requires transparent messaging and strict adherence to industry self-regulatory codes (e.g., Japan Advertising Consortium, EU Pledge) and updated internal audit controls.

- 30+ countries tightened youth-marketing rules by 2024

- WHO advises limits on sugary drink marketing to minors

- Compliance reduces risk of multi-million-dollar fines and brand damage

- Use self-regulatory codes and stronger internal audits

Governmental focus on plastic reduction

- EU: 30% recycled PET target by 2030

- Japan: ~25% recycling rate target by 2030

- Noncompliance fines up to ~4% of turnover (EU precedent)

- rPET demand ~8% CAGR 2024–2030 increasing capex/OPEX

Rising logistics, tariffs & sugar rules squeeze beverage margins as rPET costs bite

Geopolitical tensions and 2024 trade disruptions raised logistics costs ~7%, risking access to concentrates/sugar (~12% of beverage COGS); tariffs (a 10% tariff could add JPY 5–10bn) and sugar taxes pushed reformulation and low-sugar launches; 30+ countries tightened youth-marketing rules by 2024; EU/Japan recycled-PET targets (30%/25% by 2030) drive capex/OPEX for rPET sourcing.

| Metric | 2024 / Target |

|---|---|

| Logistics cost rise | ~7% |

| COGS exposure (sugar/concentrates) | ~12% |

| Potential 10% tariff impact | JPY 5–10bn |

| Exports of group revenue | ~18% |

| Countries tightening youth-marketing | 30+ |

| EU rPET target | 30% by 2030 |

| Japan recycling target | ~25% by 2030 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Suntory Beverage & Food across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Suntory Beverage & Food that clears complexity for meetings, supports quick risk/positioning discussions, and is easily dropped into presentations or shared across teams.

Economic factors

Impact of global inflation on production

Rising energy, raw-material and logistics costs—global oil up ~10% in 2024 and key commodity input prices up ~6–8% year-on-year—squeezed Suntory Beverage & Food’s gross margin, prompting tighter cost management and efficiency drives.

The company expanded hedging of input commodities and FX and implemented targeted price increases, helping protect operating margin after 2023–24 inflation shocks.

Sustained inflation reduced consumer real incomes; Suntory shifted mix toward value and essential beverage lines as lower-margin premium demand softened in many markets.

Fluctuations in foreign exchange rates

As a global group, Suntory Beverage & Food faces significant currency risk, with the Japanese yen's 2024 decline of about 6% vs the US dollar amplifying translation losses on overseas EBITDA (overseas sales ~¥800 billion in FY2023).

Exchange swings affect valuation of international earnings and raise costs of imported inputs like sugar and PET resin, which comprised roughly 12% of COGS in 2023.

The firm reports use of FX forwards, options and natural hedging; in FY2023 Suntory disclosed hedges covering a substantial portion of 12-month forecasted FX exposures to stabilize margins.

Economic growth rates in emerging markets

Suntory’s expansion hinges on Southeast Asia’s rising middle class—UN ESCAP projects regional GDP growth of 4.5% in 2024 and IMF forecasts 4.6% for 2025—supporting higher disposable income and premium beverage demand.

Economic slowdowns, like Malaysia’s 2023 GDP dip to 3.7% vs 2022’s 8.7% rebound, could reduce purchases of premium and health-oriented SKUs.

Suntory tracks quarterly GDP and household consumption trends to steer capital allocation and target long-term market share gains across ASEAN.

Labor market shortages and wage inflation

Rising labor costs and a shrinking workforce in Japan and developed markets pushed average hourly wages up ~3.5%–4.0% in 2024, raising manufacturing and distribution expenses for Suntory Beverage & Food.

Suntory increased CAPEX toward automation and digital transformation, citing a 2023–24 +12% YoY rise in productivity from robotics and MES deployments to curb labor dependence.

Navigating tight labor markets remains critical to uphold global supply-chain service levels, with localized wage premiums and retention costs impacting margins.

- 2024 wage inflation ~3.5%–4.0%

- Productivity gains ~+12% from automation (2023–24)

- Higher retention/wage premiums pressuring margins

Interest rate volatility and debt servicing

Changes in central bank policies—Bank of Japan shifts and global rate hikes—raise Suntory Beverage & Food's cost of capital, impacting financing for acquisitions and capex; Japan's policy rate rose from -0.1% (2021) to around 0.1%–0.5% in 2024–25, tightening liquidity for firms.

Higher rates increase debt-servicing costs: Suntory's consolidated net debt was about JPY 1.1 trillion in FY2024, so each 100 bps hike raises annual interest expense materially, pressuring investment and dividend flexibility.

The company counters with disciplined capital allocation, targeting leverage ratios and maintaining liquidity buffers—short-term cash and committed facilities covered over 12 months of maturities—to preserve resilience amid interest volatility.

- Net debt ~ JPY 1.1T (FY2024)

- Each 100 bps ↑ materially raises interest expense

- Leverage and liquidity targets guide capital allocation

Rising costs and yen weakness squeeze margins; automation offsets, debt raises risks

Rising input, energy and logistics costs (commodities +6–8% YoY; oil +10% 2024) and yen volatility (JPY -6% vs USD 2024) squeezed margins; hedging and targeted price rises partly offset impacts. Wage inflation (~3.5–4.0% 2024) pushed CAPEX to automation (+12% productivity 2023–24). Net debt ~JPY 1.1T (FY2024) raises interest sensitivity amid tighter global rates.

| Metric | Value |

|---|---|

| Commodities YoY | +6–8% |

| Oil 2024 | +~10% |

| JPY vs USD 2024 | -~6% |

| Wage inflation 2024 | ~3.5–4.0% |

| Automation productivity | +12% (2023–24) |

| Net debt FY2024 | ~JPY 1.1T |

Full Version Awaits

Suntory Beverage & Food PESTLE Analysis

The preview shown here is the exact Suntory Beverage & Food PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Uncover how regulatory shifts, consumer trends, and technological innovation are reshaping Suntory Beverage & Food’s competitive landscape; our PESTLE snapshot highlights key risks and opportunities to inform smarter strategy and investments—buy the full analysis for a complete, actionable briefing you can use immediately.

Political factors

Geopolitical instability in key markets

Ongoing geopolitical tensions in Europe and parts of Asia force Suntory to keep agile supply chains; 2024 trade disruptions raised logistics costs ~7% for global beverage firms, prompting contingency routing for Lucozade and Ribena inputs.

Shifting alliances and sanctions risk raw-material access—e.g., concentrate and sugar—potentially affecting 2024 input cost exposure tied to ~12% of COGS for beverage divisions.

Strategic diversification of production—expanding regional plants and contract bottling—remains a priority to buffer localized unrest and preserve FY2025 volume targets.

Global trade policies and tariffs

Changes in international trade agreements and protective tariffs on beverages or ingredients can raise Suntory Beverage & Food’s COGS; a 10% tariff on imported concentrates could add roughly JPY 5–10 billion annually given 2024 ingredient import levels. The company closely monitors Japan’s bilateral trade with China, ASEAN and the US to fine-tune pricing and hedging; in 2024 exports comprised about 18% of group revenue. Fluctuating duties on sugar and fruit concentrates have prompted Suntory to engage trade regulators proactively to mitigate duty volatility.

Taxation on sugar-sweetened beverages

Government moves to expand sugar taxes—over 40 countries globally and recent hikes in parts of Europe and Southeast Asia raising rates by up to 20–30% since 2022—force Suntory Beverage & Food to reformulate and adjust retail pricing; the group accelerated launches of low-sugar and functional lines, which now represent an increasing share of portfolio revenue (company reported 2024 non-ALC health beverage growth of mid-single digits), reducing tax exposure. Maintaining proactive policy engagement helps the firm forecast fiscal shifts and mitigate margin impact.

Stricter marketing regulations to minors

Political pressure to restrict advertising of high-calorie or caffeinated drinks to minors is rising: over 30 countries tightened youth-targeted marketing rules by 2024, and the WHO recommends limits for sugary beverages.

Suntory must ensure campaigns for BOSS Coffee and Orangina meet evolving regional standards to avoid fines and reputational loss; non-compliance risks fines up to several million dollars in some jurisdictions.

This requires transparent messaging and strict adherence to industry self-regulatory codes (e.g., Japan Advertising Consortium, EU Pledge) and updated internal audit controls.

- 30+ countries tightened youth-marketing rules by 2024

- WHO advises limits on sugary drink marketing to minors

- Compliance reduces risk of multi-million-dollar fines and brand damage

- Use self-regulatory codes and stronger internal audits

Governmental focus on plastic reduction

- EU: 30% recycled PET target by 2030

- Japan: ~25% recycling rate target by 2030

- Noncompliance fines up to ~4% of turnover (EU precedent)

- rPET demand ~8% CAGR 2024–2030 increasing capex/OPEX

Rising logistics, tariffs & sugar rules squeeze beverage margins as rPET costs bite

Geopolitical tensions and 2024 trade disruptions raised logistics costs ~7%, risking access to concentrates/sugar (~12% of beverage COGS); tariffs (a 10% tariff could add JPY 5–10bn) and sugar taxes pushed reformulation and low-sugar launches; 30+ countries tightened youth-marketing rules by 2024; EU/Japan recycled-PET targets (30%/25% by 2030) drive capex/OPEX for rPET sourcing.

| Metric | 2024 / Target |

|---|---|

| Logistics cost rise | ~7% |

| COGS exposure (sugar/concentrates) | ~12% |

| Potential 10% tariff impact | JPY 5–10bn |

| Exports of group revenue | ~18% |

| Countries tightening youth-marketing | 30+ |

| EU rPET target | 30% by 2030 |

| Japan recycling target | ~25% by 2030 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Suntory Beverage & Food across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Suntory Beverage & Food that clears complexity for meetings, supports quick risk/positioning discussions, and is easily dropped into presentations or shared across teams.

Economic factors

Impact of global inflation on production

Rising energy, raw-material and logistics costs—global oil up ~10% in 2024 and key commodity input prices up ~6–8% year-on-year—squeezed Suntory Beverage & Food’s gross margin, prompting tighter cost management and efficiency drives.

The company expanded hedging of input commodities and FX and implemented targeted price increases, helping protect operating margin after 2023–24 inflation shocks.

Sustained inflation reduced consumer real incomes; Suntory shifted mix toward value and essential beverage lines as lower-margin premium demand softened in many markets.

Fluctuations in foreign exchange rates

As a global group, Suntory Beverage & Food faces significant currency risk, with the Japanese yen's 2024 decline of about 6% vs the US dollar amplifying translation losses on overseas EBITDA (overseas sales ~¥800 billion in FY2023).

Exchange swings affect valuation of international earnings and raise costs of imported inputs like sugar and PET resin, which comprised roughly 12% of COGS in 2023.

The firm reports use of FX forwards, options and natural hedging; in FY2023 Suntory disclosed hedges covering a substantial portion of 12-month forecasted FX exposures to stabilize margins.

Economic growth rates in emerging markets

Suntory’s expansion hinges on Southeast Asia’s rising middle class—UN ESCAP projects regional GDP growth of 4.5% in 2024 and IMF forecasts 4.6% for 2025—supporting higher disposable income and premium beverage demand.

Economic slowdowns, like Malaysia’s 2023 GDP dip to 3.7% vs 2022’s 8.7% rebound, could reduce purchases of premium and health-oriented SKUs.

Suntory tracks quarterly GDP and household consumption trends to steer capital allocation and target long-term market share gains across ASEAN.

Labor market shortages and wage inflation

Rising labor costs and a shrinking workforce in Japan and developed markets pushed average hourly wages up ~3.5%–4.0% in 2024, raising manufacturing and distribution expenses for Suntory Beverage & Food.

Suntory increased CAPEX toward automation and digital transformation, citing a 2023–24 +12% YoY rise in productivity from robotics and MES deployments to curb labor dependence.

Navigating tight labor markets remains critical to uphold global supply-chain service levels, with localized wage premiums and retention costs impacting margins.

- 2024 wage inflation ~3.5%–4.0%

- Productivity gains ~+12% from automation (2023–24)

- Higher retention/wage premiums pressuring margins

Interest rate volatility and debt servicing

Changes in central bank policies—Bank of Japan shifts and global rate hikes—raise Suntory Beverage & Food's cost of capital, impacting financing for acquisitions and capex; Japan's policy rate rose from -0.1% (2021) to around 0.1%–0.5% in 2024–25, tightening liquidity for firms.

Higher rates increase debt-servicing costs: Suntory's consolidated net debt was about JPY 1.1 trillion in FY2024, so each 100 bps hike raises annual interest expense materially, pressuring investment and dividend flexibility.

The company counters with disciplined capital allocation, targeting leverage ratios and maintaining liquidity buffers—short-term cash and committed facilities covered over 12 months of maturities—to preserve resilience amid interest volatility.

- Net debt ~ JPY 1.1T (FY2024)

- Each 100 bps ↑ materially raises interest expense

- Leverage and liquidity targets guide capital allocation

Rising costs and yen weakness squeeze margins; automation offsets, debt raises risks

Rising input, energy and logistics costs (commodities +6–8% YoY; oil +10% 2024) and yen volatility (JPY -6% vs USD 2024) squeezed margins; hedging and targeted price rises partly offset impacts. Wage inflation (~3.5–4.0% 2024) pushed CAPEX to automation (+12% productivity 2023–24). Net debt ~JPY 1.1T (FY2024) raises interest sensitivity amid tighter global rates.

| Metric | Value |

|---|---|

| Commodities YoY | +6–8% |

| Oil 2024 | +~10% |

| JPY vs USD 2024 | -~6% |

| Wage inflation 2024 | ~3.5–4.0% |

| Automation productivity | +12% (2023–24) |

| Net debt FY2024 | ~JPY 1.1T |

Full Version Awaits

Suntory Beverage & Food PESTLE Analysis

The preview shown here is the exact Suntory Beverage & Food PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment decisions.