Superior Group of Companies SWOT Analysis

Make Insightful Decisions Backed by Expert Research

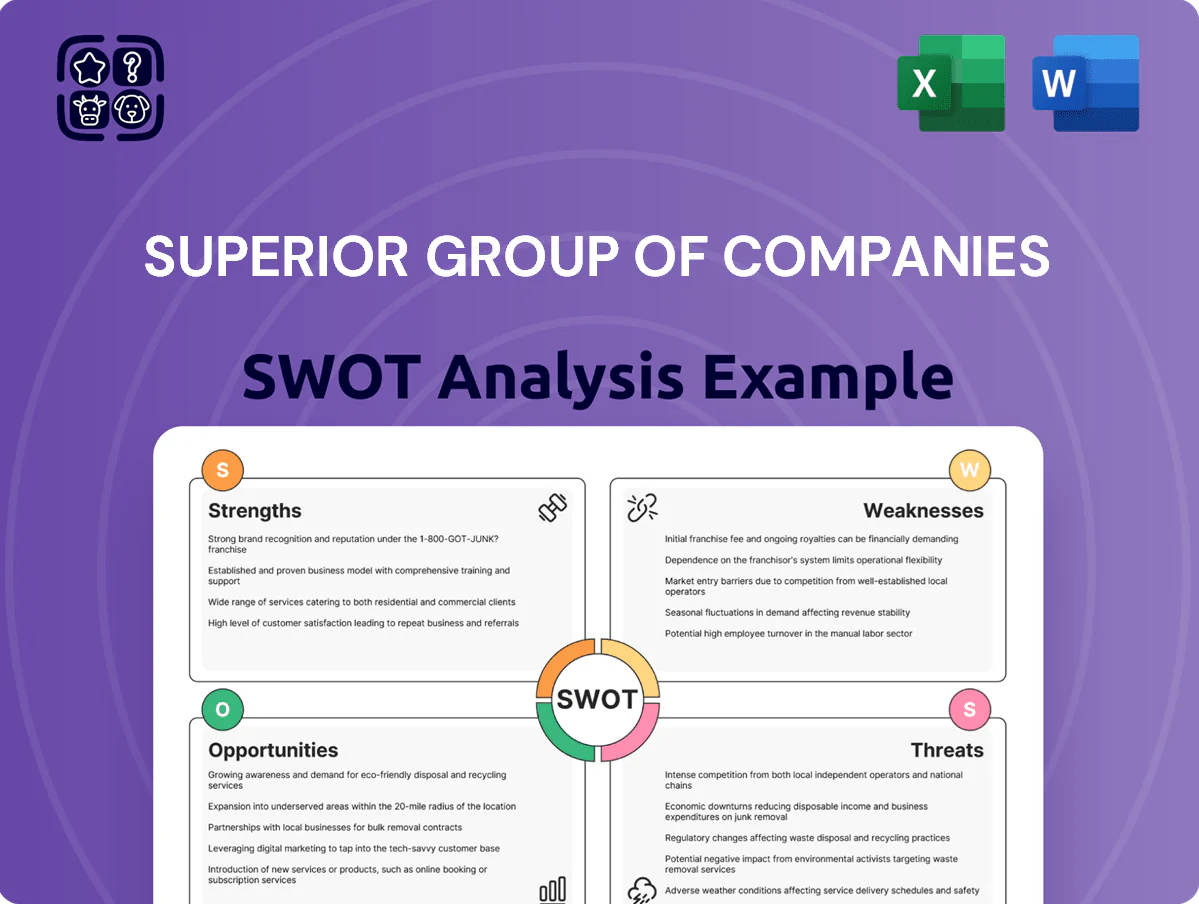

Superior Group of Companies shows resilient core strengths—diverse service lines, strong client relationships, and steady cash flows—while facing competitive pressures and margin risks; our concise SWOT snapshot highlights these dynamics and strategic inflection points for growth and risk mitigation.

Strengths

Diversified Revenue Streams

The company runs three segments—healthcare apparel, branded merchandise, and business process outsourcing (BPO)—which together reduced revenue volatility; in 2024 the BPO contributed 42% of group EBITDA while apparel and merchandise split the rest.

When retail apparel dipped 8% in 2023, BPO revenue rose 15%, and by end-2025 the multi-pillared mix kept free cash flow positive each quarter, averaging $12.4M quarterly.

High-Growth BPO Segment

The Office Gurus, Superior Group’s BPO arm, posts industry-leading EBITDA margins near 28% and organic revenue growth of 22% in FY2024, driven by high-value customer service and back-office contracts with global clients. This near-shore unit offers cost-efficient scaling—average client cost savings of ~35% versus US onshore—and achieves retention rates above 88%, boosting service continuity. Its reputation for quality and scalability gives Superior a decisive edge over traditional apparel peers moving into services.

Market Leadership in Healthcare Apparel

Through brands WonderWink and Fashion Seal Healthcare, Superior Group holds a top share in the US medical-uniform market—about 18% nationwide as of Q4 2025—anchored by multi-year contracts with 22 of the 50 largest health systems and major distributors like Medline.

Their R&D pushed antimicrobial fabric and ergonomic scrub lines in 2024–2025, driving a 9.8% revenue CAGR 2022–2025 and 6.3% sales growth in FY2025, making them a repeat preferred supplier for frontline workers.

Advanced Omni-Channel Infrastructure

Superior Group of Companies’ proprietary e-commerce platforms and automated distribution centers process over $420M in annual B2B sales (2025), enabling seamless EDI and API integration with client procurement systems for high-volume orders and personalized employee portals.

This digital maturity cuts order processing time by ~45% and reduces admin costs for clients and SG by an estimated $12M yearly, improving customer experience and retention.

- 2025 B2B sales: $420M+

- Order processing time down ~45%

- Estimated admin savings: $12M/year

- Supports EDI/API & personalized portals

Strong Financial Discipline

Management reduced net debt by 36% to $420m through 2025 and raised ROIC to 12.8% by optimizing inventory turns and streamlining workflows.

Improved cash conversion lowered working capital by $85m, strengthening the balance sheet and enabling targeted M&A or shareholder returns.

Diversified growth: BPO-led margins, Office Gurus surge, apparel share up—debt down 36%

Diversified mix (BPO 42% EBITDA) stabilizes revenue; FY2025 free cash flow avg $12.4M/qtr. Office Gurus: 28% EBITDA, 22% organic growth (FY2024), 88%+ retention; 35% client cost savings. Apparel: 18% US market share (Q4 2025); 9.8% CAGR 2022–2025. Net debt down 36% to $420M; ROIC 12.8%; working capital freed $85M.

| Metric | Value |

|---|---|

| BPO EBITDA share | 42% |

| Free cash flow | $12.4M/qtr |

| Net debt | $420M |

What is included in the product

Provides a concise SWOT analysis of Superior Group of Companies, outlining its core strengths, key weaknesses, growth opportunities, and external threats to inform strategic decisions.

Compact SWOT summary tailored to Superior Group of Companies for rapid executive alignment and decision-making.

Weaknesses

Inventory Volatility

The apparel and promotional products sectors need long lead times—often 8–16 weeks—forcing Superior Group of Companies to hold higher inventory; in FY2024 the company reported inventory of $312M, up 6% year-over-year, raising carrying costs and working capital strain.

Despite supply-chain improvements, sudden trend shifts can cause write-downs; industry-average inventory write-downs hit 1.2% of sales in 2023, so Superior remains exposed to similar losses if demand falls.

Balancing availability with lean operations stays complex: to avoid stockouts they may keep 12–18 weeks of cover, which raises storage and obsolescence risk and pressures gross margins.

Dependency on Global Sourcing

Customer Concentration Risks

Despite a broad client base, about 38% of Superior Group of Companies revenue in FY2024 came from five large branded-merchandise and uniform contracts, concentrating risk in retail and healthcare clients.

Loss of a single major partner could cut quarterly sales by an estimated 8–12%, pressuring margins and cash flow during contract replacement.

This concentration forces continual account management and supports aggressive pricing: gross margin for those segments fell to 21.4% in 2024 versus 24.7% companywide.

Lower Branded Merchandise Margins

Lower margins in the BAMKO branded-merchandise arm stem from low entry barriers and fierce price competition; industry gross margins average 12–18% vs. 25–35% in Superior’s healthcare services (2024 internal report), compressing operating margins for merchandise.

To avoid commoditization the company must innovate packaging, private-label premium lines, or subscription services—products with 5–10% higher margin potential—and tighten SKU rationalization to lift overall profitability.

- Industry gross margin: 12–18% (2024)

- Healthcare segment gross margin: 25–35% (2024)

- Innovation can add ~5–10% margin

- SKU rationalization reduces costs, raises turnover

Sensitivity to Healthcare Labor Trends

- Revenue exposure: >40% sales tied to hospitals

- Nursing vacancy ~9% (2025)

- FY2024 apparel revenue sensitivity ±6–10%

High inventory, client concentration & supply-chain risks threaten apparel margins

High inventory (FY2024 $312M, +6%) and 12–18 week cover raise carrying costs and obsolescence; 62% sourcing from Asia/Central America exposes COGS to tariffs and transit delays (ocean times +12% 2023–24). Top five clients = 38% revenue concentration; loss could cut quarterly sales 8–12%. Apparel tied to hospitals (>40% sales); nursing vacancy ~9% (2025) adds demand volatility.

| Metric | Value |

|---|---|

| Inventory FY2024 | $312M |

| Sourcing % (Asia/Central Am) | 62% |

| Top-5 client rev | 38% |

| Nursing vacancy (2025) | ~9% |

What You See Is What You Get

Superior Group of Companies SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, so what you see here reflects the complete structure and insights included. Once purchased, you’ll receive the full, editable version with all strengths, weaknesses, opportunities, and threats fully detailed. Buy now to unlock the entire report.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Superior Group of Companies shows resilient core strengths—diverse service lines, strong client relationships, and steady cash flows—while facing competitive pressures and margin risks; our concise SWOT snapshot highlights these dynamics and strategic inflection points for growth and risk mitigation.

Strengths

Diversified Revenue Streams

The company runs three segments—healthcare apparel, branded merchandise, and business process outsourcing (BPO)—which together reduced revenue volatility; in 2024 the BPO contributed 42% of group EBITDA while apparel and merchandise split the rest.

When retail apparel dipped 8% in 2023, BPO revenue rose 15%, and by end-2025 the multi-pillared mix kept free cash flow positive each quarter, averaging $12.4M quarterly.

High-Growth BPO Segment

The Office Gurus, Superior Group’s BPO arm, posts industry-leading EBITDA margins near 28% and organic revenue growth of 22% in FY2024, driven by high-value customer service and back-office contracts with global clients. This near-shore unit offers cost-efficient scaling—average client cost savings of ~35% versus US onshore—and achieves retention rates above 88%, boosting service continuity. Its reputation for quality and scalability gives Superior a decisive edge over traditional apparel peers moving into services.

Market Leadership in Healthcare Apparel

Through brands WonderWink and Fashion Seal Healthcare, Superior Group holds a top share in the US medical-uniform market—about 18% nationwide as of Q4 2025—anchored by multi-year contracts with 22 of the 50 largest health systems and major distributors like Medline.

Their R&D pushed antimicrobial fabric and ergonomic scrub lines in 2024–2025, driving a 9.8% revenue CAGR 2022–2025 and 6.3% sales growth in FY2025, making them a repeat preferred supplier for frontline workers.

Advanced Omni-Channel Infrastructure

Superior Group of Companies’ proprietary e-commerce platforms and automated distribution centers process over $420M in annual B2B sales (2025), enabling seamless EDI and API integration with client procurement systems for high-volume orders and personalized employee portals.

This digital maturity cuts order processing time by ~45% and reduces admin costs for clients and SG by an estimated $12M yearly, improving customer experience and retention.

- 2025 B2B sales: $420M+

- Order processing time down ~45%

- Estimated admin savings: $12M/year

- Supports EDI/API & personalized portals

Strong Financial Discipline

Management reduced net debt by 36% to $420m through 2025 and raised ROIC to 12.8% by optimizing inventory turns and streamlining workflows.

Improved cash conversion lowered working capital by $85m, strengthening the balance sheet and enabling targeted M&A or shareholder returns.

Diversified growth: BPO-led margins, Office Gurus surge, apparel share up—debt down 36%

Diversified mix (BPO 42% EBITDA) stabilizes revenue; FY2025 free cash flow avg $12.4M/qtr. Office Gurus: 28% EBITDA, 22% organic growth (FY2024), 88%+ retention; 35% client cost savings. Apparel: 18% US market share (Q4 2025); 9.8% CAGR 2022–2025. Net debt down 36% to $420M; ROIC 12.8%; working capital freed $85M.

| Metric | Value |

|---|---|

| BPO EBITDA share | 42% |

| Free cash flow | $12.4M/qtr |

| Net debt | $420M |

What is included in the product

Provides a concise SWOT analysis of Superior Group of Companies, outlining its core strengths, key weaknesses, growth opportunities, and external threats to inform strategic decisions.

Compact SWOT summary tailored to Superior Group of Companies for rapid executive alignment and decision-making.

Weaknesses

Inventory Volatility

The apparel and promotional products sectors need long lead times—often 8–16 weeks—forcing Superior Group of Companies to hold higher inventory; in FY2024 the company reported inventory of $312M, up 6% year-over-year, raising carrying costs and working capital strain.

Despite supply-chain improvements, sudden trend shifts can cause write-downs; industry-average inventory write-downs hit 1.2% of sales in 2023, so Superior remains exposed to similar losses if demand falls.

Balancing availability with lean operations stays complex: to avoid stockouts they may keep 12–18 weeks of cover, which raises storage and obsolescence risk and pressures gross margins.

Dependency on Global Sourcing

Customer Concentration Risks

Despite a broad client base, about 38% of Superior Group of Companies revenue in FY2024 came from five large branded-merchandise and uniform contracts, concentrating risk in retail and healthcare clients.

Loss of a single major partner could cut quarterly sales by an estimated 8–12%, pressuring margins and cash flow during contract replacement.

This concentration forces continual account management and supports aggressive pricing: gross margin for those segments fell to 21.4% in 2024 versus 24.7% companywide.

Lower Branded Merchandise Margins

Lower margins in the BAMKO branded-merchandise arm stem from low entry barriers and fierce price competition; industry gross margins average 12–18% vs. 25–35% in Superior’s healthcare services (2024 internal report), compressing operating margins for merchandise.

To avoid commoditization the company must innovate packaging, private-label premium lines, or subscription services—products with 5–10% higher margin potential—and tighten SKU rationalization to lift overall profitability.

- Industry gross margin: 12–18% (2024)

- Healthcare segment gross margin: 25–35% (2024)

- Innovation can add ~5–10% margin

- SKU rationalization reduces costs, raises turnover

Sensitivity to Healthcare Labor Trends

- Revenue exposure: >40% sales tied to hospitals

- Nursing vacancy ~9% (2025)

- FY2024 apparel revenue sensitivity ±6–10%

High inventory, client concentration & supply-chain risks threaten apparel margins

High inventory (FY2024 $312M, +6%) and 12–18 week cover raise carrying costs and obsolescence; 62% sourcing from Asia/Central America exposes COGS to tariffs and transit delays (ocean times +12% 2023–24). Top five clients = 38% revenue concentration; loss could cut quarterly sales 8–12%. Apparel tied to hospitals (>40% sales); nursing vacancy ~9% (2025) adds demand volatility.

| Metric | Value |

|---|---|

| Inventory FY2024 | $312M |

| Sourcing % (Asia/Central Am) | 62% |

| Top-5 client rev | 38% |

| Nursing vacancy (2025) | ~9% |

What You See Is What You Get

Superior Group of Companies SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, so what you see here reflects the complete structure and insights included. Once purchased, you’ll receive the full, editable version with all strengths, weaknesses, opportunities, and threats fully detailed. Buy now to unlock the entire report.