Supremex Porter's Five Forces Analysis

Don't Miss the Bigger Picture

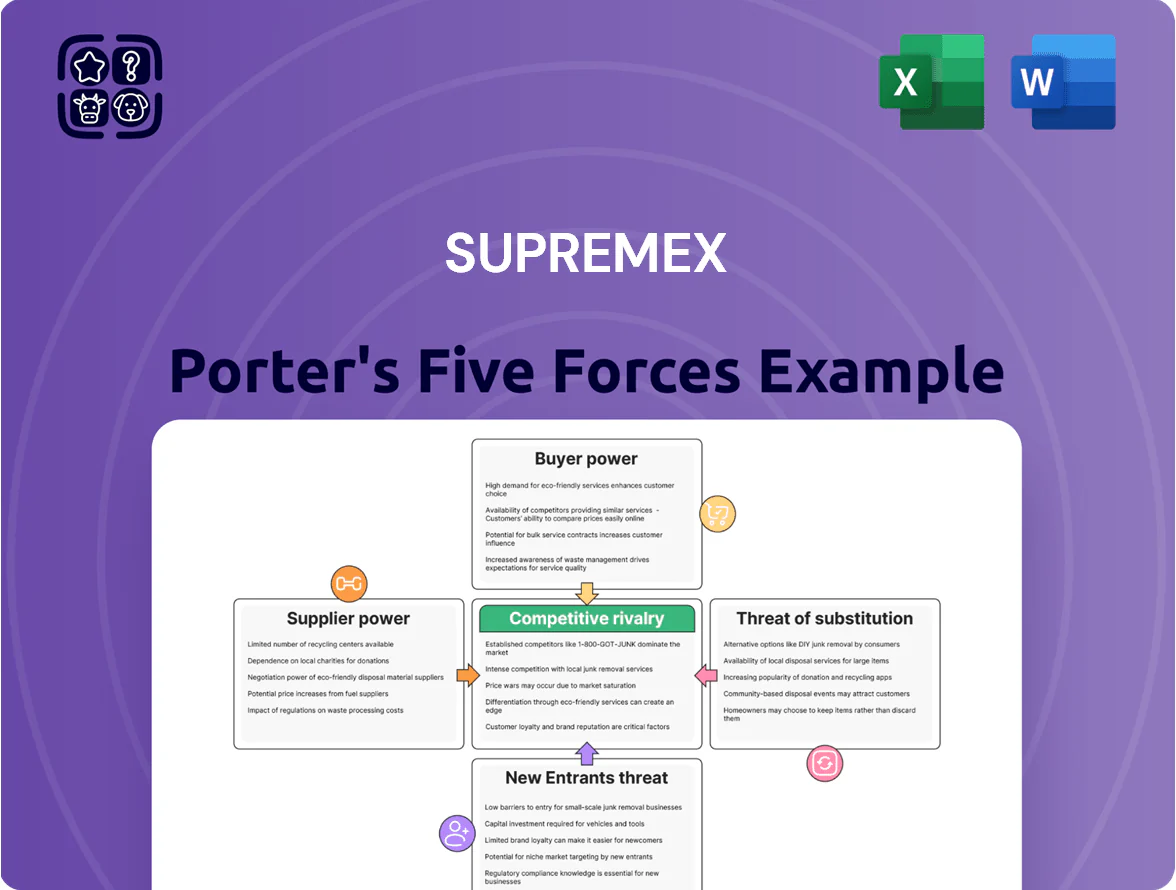

Supremex faces moderate buyer power, concentrated supplier relationships, and steady substitute threats shaped by packaging innovation and sustainability trends; competitive rivalry is high among regional converters while barriers to entry remain modest.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Supremex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Paper and Pulp Mills

The primary raw material for Supremex is paper, sourced from a handful of large North American mills; by 2025 the top 10 producers controlled about 68% of regional capacity, giving suppliers stronger pricing power.

Industry consolidation since 2018—including 2023–2024 M&A—raised supplier leverage, leading to narrower contract flexibility and higher benchmark pulp prices (bleached softwood pulp up ~22% 2022–2024).

This concentration makes vendor switching costly: replacing a major supplier can add weeks to lead times and expose Supremex to spot-market premiums that ranged 15–30% in stressed months.

Volatility in Energy and Chemical Inputs

Supremex’s envelope and packaging production depends on energy and specialty chemicals for adhesives and inks, which saw global crude and petrochemical-linked feedstock prices rise ~18% in 2022–24 and electricity costs up ~12% in North America by 2024, squeezing margins.

Suppliers pass through these increases—carbon regulation and feedstock tightness raised supplier price indices 10–25% in 2023—so Supremex has limited negotiating leverage over market-driven cost hikes.

Impact of Environmental Sustainability Standards

Supremex faces stronger supplier power as demand for FSC-certified or recycled fiber surged: global certified fiber demand rose ~18% in 2024 and corporate mandates aim for 50% sustainable packaging by 2026, letting vendors charge premiums of 6–12% for eco-grade pulp.

Logistics and Freight Dependency

Transportation providers are a critical link for moving heavy paper rolls and finished goods; in 2024 Canadian trucking wages rose ~6.5% year-over-year, pushing carrier rates up similarly and raising logistics costs for converters like Supremex.

Rising labor and volatile fuel surcharges (fuel accounted for ~18% of carrier costs in 2024) give logistics suppliers notable pricing power; Supremex often must absorb fees or face delivery delays that risk long-standing customer contracts.

- Trucking wage growth ~6.5% (2024)

- Fuel ~18% of carrier costs (2024)

- Carrier rate increases pass-through risk to Supremex

- Delivery delays threaten customer retention

Strategic Importance of Specialized Substrates

As Supremex moves into high-end packaging, demand for specialized coatings and durable substrates rises, and only about 10–15 global suppliers can meet these specs, concentrating supply power.

These niche vendors can charge 10–25% premiums over standard paper inputs; Supremex had COGS for materials of CAD 312m in FY2024, so a 10% premium could add ~CAD 31m annually.

Dependency on few suppliers raises switching costs and contract leverage, increasing supplier bargaining power and margin pressure.

- 10–15 qualified suppliers globally

- 10–25% price premium vs standard paper

- CAD 312m material COGS in FY2024

- ~CAD 31m impact at 10% premium

Supplier concentration could tack ~CAD31M onto Supremex COGS as input costs surge

Supremex faces high supplier power: concentrated North American pulp mills (top 10 ~68% capacity by 2025), niche coatings suppliers (10–15 global), and tight logistics pushed material COGS CAD 312m in FY2024; supplier-driven price moves (bleached pulp +22% 2022–24, eco-pulp premium 6–12%, niche premium 10–25%) can add ~CAD 31m at 10%

| Metric | Value |

|---|---|

| Top-10 mill share (2025) | 68% |

| Bleached pulp change (2022–24) | +22% |

| Material COGS FY2024 | CAD 312m |

| Eco-pulp premium | 6–12% |

| Niche supplier premium | 10–25% |

| Estimated impact @10% | ~CAD 31m |

What is included in the product

Concise Porter’s Five Forces analysis of Supremex identifying competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic barriers that shape its pricing and profitability.

A concise Porter's Five Forces one-sheet for Supremex—quickly spot supplier, buyer, and competitive pressures to guide strategic decisions.

Customers Bargaining Power

Concentration of Large Enterprise Clients

A large share of Supremex’s 2024 revenue—about 48% of CAD 420m total sales—comes from big banks, government agencies, and top resellers who buy in bulk, giving them strong negotiating leverage.

These customers routinely secure double-digit discounts and extended net-60 to net-90 payment terms at renewals, pressuring Supremex’s margins.

The option to shift multi-million-dollar contracts to rivals concentrates pricing power with buyers and raises supplier churn risk.

Low Switching Costs for Standardized Products

For basic commercial envelopes, products are commoditized so customers switch easily on price; industry reports show procurement-driven suppliers win with 5–15% lower bids. Because standard mailers lack technical differentiation, buyers run competitive tenders—Supremex faced 8% volume-weighted price pressure in 2024. This forces Supremex to squeeze costs: in 2024 SG&A + COGS optimization improved adjusted EBITDA margin to ~9.5% (FY2024). Operational efficiency is therefore critical to defend margins vs price-sensitive buyers.

Transition to Digital Communication Channels

Customers are shifting from physical mail to digital billing—Canada Post reported a 12% annual drop in household addressed mail in 2024—so buyers can leverage faster digital migration to pressure Supremex on pricing; if physical-mail unit costs rise above roughly CAD 0.60 (typical corporate break-even), clients may cut paper. Supremex must offer value-added services—personalized marketing inserts, hybrid mail, or printed-digital bundles—while targeting a paper-volume retention threshold to avoid churn.

High Service Level Expectations in E-commerce

E-commerce customers demand rapid lead times, custom branding, and durable materials; 2024 US e-commerce growth of 12% raised packaging spend, and 60% of retailers cite faster fulfillment as top requirement.

Buyers can choose from thousands of converters and expect flexibility and innovation; Supremex risks churn if it misses logistics needs given a >20% supplier-switch intent in packaging surveys.

Price Sensitivity in the Reseller Market

Resellers and wholesalers for flooring products run on thin margins—often 3–8% gross margin in North American distribution—so even a 2–3% price hike from Supremex can cut profitability materially and trigger channel pushback.

These intermediaries frequently play multiple manufacturers against each other to secure the lowest wholesale price, so their loyalty is to margin preservation rather than brand, limiting Supremex’s pricing power across this segment.

Supremex reported 2024 channel sales of CAD 210m; relying on resellers for ~45% of volume means broad price increases risk volume loss and margin compression.

- Reseller margins 3–8%

- 2–3% price rise risks acceptability

- 45% volume via resellers (2024 CAD 210m)

- High supplier-switching to lower cost

Buyer concentration, discounts and channel risk squeeze Supremex margins

Major buyers (banks, gov’t, resellers) drove ~48% of Supremex’s CAD 420m 2024 revenue, extracting double-digit discounts and net-60/90 terms, forcing margin pressure; commoditized envelopes and tendering caused ~8% price pressure in 2024 while channel reliance (CAD 210m, 45%) means small price moves (2–3%) risk volume loss.

| Metric | 2024 |

|---|---|

| Total sales | CAD 420m |

| Buyer concentration | 48% |

| Channel sales | CAD 210m (45%) |

| Price pressure | 8% |

Preview Before You Purchase

Supremex Porter's Five Forces Analysis

This preview shows the exact Supremex Porter’s Five Forces analysis you’ll receive immediately after purchase—fully written, formatted, and ready for use with no placeholders or drafts.

The document displayed here is the same final file available for instant download upon payment, containing supplier power, buyer power, competitive rivalry, threat of entry, and threat of substitutes analyses.

No mockups or samples—what you see is the complete, professionally prepared deliverable you’ll get after buying.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Supremex faces moderate buyer power, concentrated supplier relationships, and steady substitute threats shaped by packaging innovation and sustainability trends; competitive rivalry is high among regional converters while barriers to entry remain modest.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Supremex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Paper and Pulp Mills

The primary raw material for Supremex is paper, sourced from a handful of large North American mills; by 2025 the top 10 producers controlled about 68% of regional capacity, giving suppliers stronger pricing power.

Industry consolidation since 2018—including 2023–2024 M&A—raised supplier leverage, leading to narrower contract flexibility and higher benchmark pulp prices (bleached softwood pulp up ~22% 2022–2024).

This concentration makes vendor switching costly: replacing a major supplier can add weeks to lead times and expose Supremex to spot-market premiums that ranged 15–30% in stressed months.

Volatility in Energy and Chemical Inputs

Supremex’s envelope and packaging production depends on energy and specialty chemicals for adhesives and inks, which saw global crude and petrochemical-linked feedstock prices rise ~18% in 2022–24 and electricity costs up ~12% in North America by 2024, squeezing margins.

Suppliers pass through these increases—carbon regulation and feedstock tightness raised supplier price indices 10–25% in 2023—so Supremex has limited negotiating leverage over market-driven cost hikes.

Impact of Environmental Sustainability Standards

Supremex faces stronger supplier power as demand for FSC-certified or recycled fiber surged: global certified fiber demand rose ~18% in 2024 and corporate mandates aim for 50% sustainable packaging by 2026, letting vendors charge premiums of 6–12% for eco-grade pulp.

Logistics and Freight Dependency

Transportation providers are a critical link for moving heavy paper rolls and finished goods; in 2024 Canadian trucking wages rose ~6.5% year-over-year, pushing carrier rates up similarly and raising logistics costs for converters like Supremex.

Rising labor and volatile fuel surcharges (fuel accounted for ~18% of carrier costs in 2024) give logistics suppliers notable pricing power; Supremex often must absorb fees or face delivery delays that risk long-standing customer contracts.

- Trucking wage growth ~6.5% (2024)

- Fuel ~18% of carrier costs (2024)

- Carrier rate increases pass-through risk to Supremex

- Delivery delays threaten customer retention

Strategic Importance of Specialized Substrates

As Supremex moves into high-end packaging, demand for specialized coatings and durable substrates rises, and only about 10–15 global suppliers can meet these specs, concentrating supply power.

These niche vendors can charge 10–25% premiums over standard paper inputs; Supremex had COGS for materials of CAD 312m in FY2024, so a 10% premium could add ~CAD 31m annually.

Dependency on few suppliers raises switching costs and contract leverage, increasing supplier bargaining power and margin pressure.

- 10–15 qualified suppliers globally

- 10–25% price premium vs standard paper

- CAD 312m material COGS in FY2024

- ~CAD 31m impact at 10% premium

Supplier concentration could tack ~CAD31M onto Supremex COGS as input costs surge

Supremex faces high supplier power: concentrated North American pulp mills (top 10 ~68% capacity by 2025), niche coatings suppliers (10–15 global), and tight logistics pushed material COGS CAD 312m in FY2024; supplier-driven price moves (bleached pulp +22% 2022–24, eco-pulp premium 6–12%, niche premium 10–25%) can add ~CAD 31m at 10%

| Metric | Value |

|---|---|

| Top-10 mill share (2025) | 68% |

| Bleached pulp change (2022–24) | +22% |

| Material COGS FY2024 | CAD 312m |

| Eco-pulp premium | 6–12% |

| Niche supplier premium | 10–25% |

| Estimated impact @10% | ~CAD 31m |

What is included in the product

Concise Porter’s Five Forces analysis of Supremex identifying competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic barriers that shape its pricing and profitability.

A concise Porter's Five Forces one-sheet for Supremex—quickly spot supplier, buyer, and competitive pressures to guide strategic decisions.

Customers Bargaining Power

Concentration of Large Enterprise Clients

A large share of Supremex’s 2024 revenue—about 48% of CAD 420m total sales—comes from big banks, government agencies, and top resellers who buy in bulk, giving them strong negotiating leverage.

These customers routinely secure double-digit discounts and extended net-60 to net-90 payment terms at renewals, pressuring Supremex’s margins.

The option to shift multi-million-dollar contracts to rivals concentrates pricing power with buyers and raises supplier churn risk.

Low Switching Costs for Standardized Products

For basic commercial envelopes, products are commoditized so customers switch easily on price; industry reports show procurement-driven suppliers win with 5–15% lower bids. Because standard mailers lack technical differentiation, buyers run competitive tenders—Supremex faced 8% volume-weighted price pressure in 2024. This forces Supremex to squeeze costs: in 2024 SG&A + COGS optimization improved adjusted EBITDA margin to ~9.5% (FY2024). Operational efficiency is therefore critical to defend margins vs price-sensitive buyers.

Transition to Digital Communication Channels

Customers are shifting from physical mail to digital billing—Canada Post reported a 12% annual drop in household addressed mail in 2024—so buyers can leverage faster digital migration to pressure Supremex on pricing; if physical-mail unit costs rise above roughly CAD 0.60 (typical corporate break-even), clients may cut paper. Supremex must offer value-added services—personalized marketing inserts, hybrid mail, or printed-digital bundles—while targeting a paper-volume retention threshold to avoid churn.

High Service Level Expectations in E-commerce

E-commerce customers demand rapid lead times, custom branding, and durable materials; 2024 US e-commerce growth of 12% raised packaging spend, and 60% of retailers cite faster fulfillment as top requirement.

Buyers can choose from thousands of converters and expect flexibility and innovation; Supremex risks churn if it misses logistics needs given a >20% supplier-switch intent in packaging surveys.

Price Sensitivity in the Reseller Market

Resellers and wholesalers for flooring products run on thin margins—often 3–8% gross margin in North American distribution—so even a 2–3% price hike from Supremex can cut profitability materially and trigger channel pushback.

These intermediaries frequently play multiple manufacturers against each other to secure the lowest wholesale price, so their loyalty is to margin preservation rather than brand, limiting Supremex’s pricing power across this segment.

Supremex reported 2024 channel sales of CAD 210m; relying on resellers for ~45% of volume means broad price increases risk volume loss and margin compression.

- Reseller margins 3–8%

- 2–3% price rise risks acceptability

- 45% volume via resellers (2024 CAD 210m)

- High supplier-switching to lower cost

Buyer concentration, discounts and channel risk squeeze Supremex margins

Major buyers (banks, gov’t, resellers) drove ~48% of Supremex’s CAD 420m 2024 revenue, extracting double-digit discounts and net-60/90 terms, forcing margin pressure; commoditized envelopes and tendering caused ~8% price pressure in 2024 while channel reliance (CAD 210m, 45%) means small price moves (2–3%) risk volume loss.

| Metric | 2024 |

|---|---|

| Total sales | CAD 420m |

| Buyer concentration | 48% |

| Channel sales | CAD 210m (45%) |

| Price pressure | 8% |

Preview Before You Purchase

Supremex Porter's Five Forces Analysis

This preview shows the exact Supremex Porter’s Five Forces analysis you’ll receive immediately after purchase—fully written, formatted, and ready for use with no placeholders or drafts.

The document displayed here is the same final file available for instant download upon payment, containing supplier power, buyer power, competitive rivalry, threat of entry, and threat of substitutes analyses.

No mockups or samples—what you see is the complete, professionally prepared deliverable you’ll get after buying.