Southwest Gas SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Southwest Gas combines a stable utility footprint with regulated revenue streams and strong customer retention, but faces regulatory shifts, infrastructure costs, and decarbonization pressures that could reshape margins and growth—want the full picture? Purchase the complete SWOT analysis to get a professionally written, editable report and Excel matrix with actionable insights for investors, strategists, and advisors.

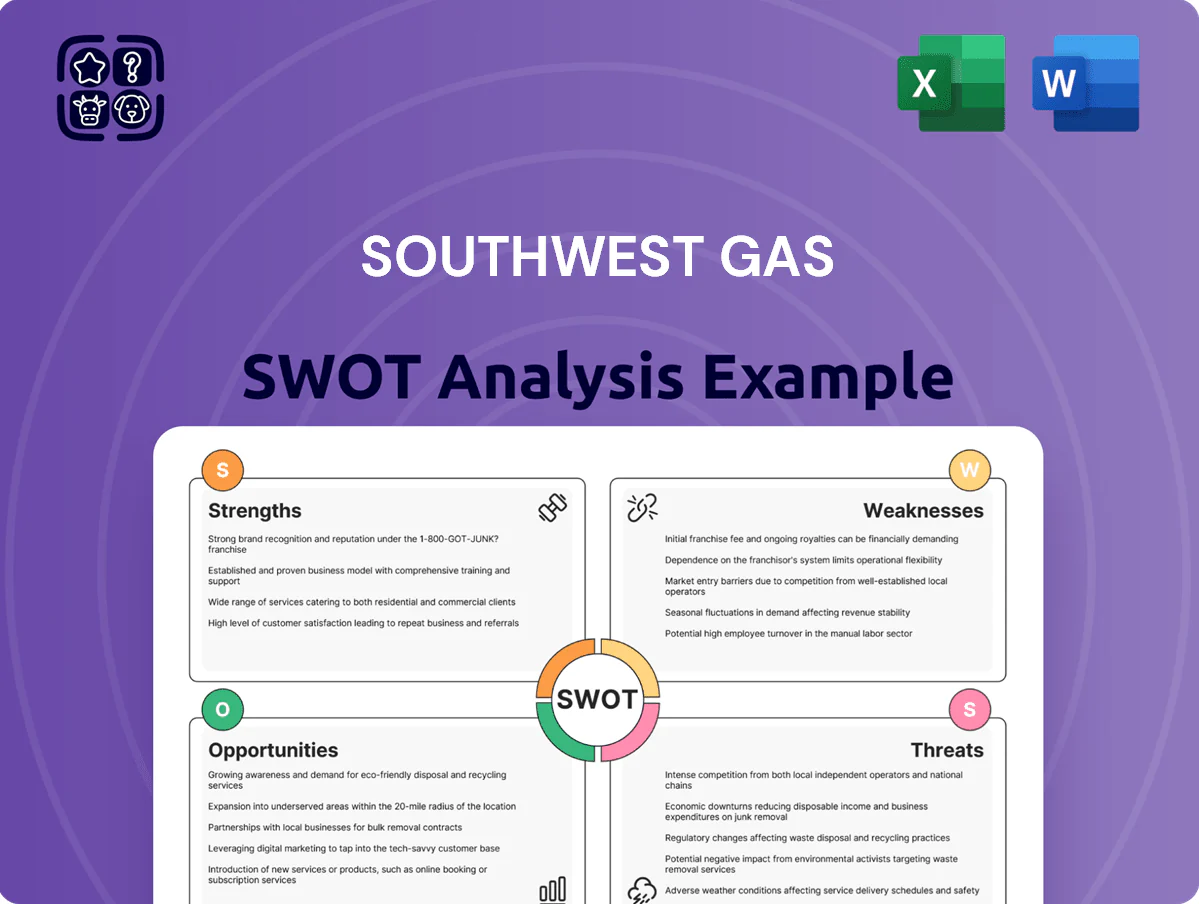

Strengths

Successful Pure-Play Transformation

By September 2025 Southwest Gas completed separation of Centuri, becoming a pure‑play regulated natural gas utility; the exit was executed via secondary offerings and private placements that raised ~1.4 billion USD, used to eliminate holding‑company debt.

The simplified structure narrows management focus to core utility operations, lowers cyclicality, and removes the construction services valuation discount, supporting a cleaner regulatory earnings profile and likely tighter P/E multiple vs pre‑2025 levels.

Robust Customer Growth in the Sun Belt

Southwest Gas benefits from a prime Sun Belt footprint, adding ~40,000 first‑time meter sets in the 12 months ending Q4 2025, equal to ~1.8% customer growth. This pace outstrips the US utility average (~0.6% in 2024), supplying steady organic revenue and rate‑base expansion. Growth is concentrated in Phoenix and Las Vegas metro areas, where rising residential and commercial connections boost long‑term gas infrastructure demand.

Strengthened Balance Sheet and Credit Profile

Following monetization of its Centuri stake, Southwest Gas strengthened its balance sheet—S&P upgraded its rating to BBB+ in late 2025—after the company fully repaid term loans and bank debt, reducing leverage and interest burden.

With over $1 billion of available liquidity as of December 2025, Southwest Gas now has a resilient capital structure capable of funding multi‑billion dollar capex for system modernization and weathering market volatility.

Constructive Regulatory Progress

Southwest Gas secured favorable regulatory outcomes: Arizona approved a System Integrity Mechanism and Nevada passed alternative ratemaking, both speeding recovery of safety and infrastructure capital and cutting regulatory lag.

Recent rate case settlements lifted allowed return on equity to about 9.8% in core territories, directly improving earnings and cash flow for upcoming capex cycles.

- Arizona: System Integrity Mechanism approved

- Nevada: alternative ratemaking enacted

- Allowed ROE: ~9.8% in key jurisdictions

- Effect: faster capex recovery, lower regulatory lag

Operational Efficiency and Safety Record

Southwest Gas has ranked in the top decile for residential customer satisfaction for six straight years through 2024 and reported a OSHA recordable incident rate 35% below the national gas-utility median in 2024.

Investments in infrared and continuous-monitoring leak detection plus ML-driven asset analytics cut O&M per customer 8% from 2019–2024 and lowered methane intensity by 22% over the same period.

This reliability and safety record creates a regulatory moat, easing rate cases and strengthening community trust across Nevada, Arizona, and California.

- 6 years top-decile satisfaction (through 2024)

- OSHA rate 35% below median (2024)

- O&M/cust down 8% (2019–2024)

- Methane intensity down 22% (2019–2024)

Pure‑play Sun Belt utility: $1.4B delever, 40k new meters, BBB+ & ~9.8% ROE

Pure‑play regulated utility after Centuri exit (Sept 2025); $1.4B proceeds paid holding‑company debt, S&P upgraded to BBB+ (late 2025).

Fast Sun Belt growth: ~40,000 net new meters in 12 months to Q4 2025 (~1.8% customer growth vs US utility 0.6% in 2024).

Regulatory wins: AZ System Integrity, NV alternative ratemaking; allowed ROE ≈9.8%.

| Metric | Value |

|---|---|

| Centuri proceeds | $1.4B |

| Net new meters (12m) | ~40,000 |

| Customer growth | ~1.8% |

| Allowed ROE | ~9.8% |

| Liquidity (Dec 2025) | >$1B |

What is included in the product

Delivers a concise SWOT overview of Southwest Gas, highlighting its operational strengths and regulatory/market weaknesses, identifying growth opportunities like infrastructure modernization and service expansion, and outlining external threats including regulatory pressure, commodity price volatility, and competition.

Delivers a clear Southwest Gas SWOT snapshot for rapid strategic alignment and executive briefings.

Weaknesses

Geographic and Sector Concentration

As a pure-play natural gas utility, Southwest Gas (ticker SWX) earns nearly 100% of revenue from gas, leaving it exposed to commodity- and demand swings; in 2024 gas operations contributed about $2.5B of consolidated revenue, concentrated in Arizona, Nevada, and California.

Unlike diversified peers, SWX lacks electric or water offsets, so regional policy shifts—like California’s aggressive decarbonization targets and Nevada’s 2024 regulatory rate reviews—create outsized earnings risk.

High Dividend Payout Ratio

Southwest Gas has run a dividend payout ratio near 90% (2024 payout ~88%), well above the 60–70% peer range, giving a strong yield but leaving little retained cash for capital projects.

With 2024 net income of $230M, the high payout limits reinvestment into pipelines and meter upgrades and raises reliance on debt or equity for capex.

Any earnings drop of 10–15% could force dividend cuts or new external financing, stressing dividend sustainability.

Exposure to Purchase Gas Price Volatility

Despite a Purchased Gas Adjustment (PGA), Southwest Gas remains exposed to natural gas price swings; the 2022–2024 Henry Hub 12-month average jumped from $4.63/MMBtu (2022) to $6.45/MMBtu (2023), causing large under-collections.

Sudden spikes create deferred regulatory assets—Southwest Gas reported $287M of gas cost deferrals at year-end 2024—straining short-term liquidity and working capital.

Recovery from customers is eventual, but timing gaps cause cash-flow volatility and risk of rate shock; political or regulatory pushback rose after 2023 tariff adjustments in Arizona and Nevada.

Historical Regulatory Lag in California

Southwest Gas faces a persistent regulatory lag in California where proceedings are more stringent and slower than in Arizona and Nevada, delaying new rates and recovery of safety investments.

These delays compressed 2024 operating margins for the California segment, with earned returns running roughly 150–300 basis points below authorized ROE in recent CPUC cases.

- California proceedings: longer, more complex

- Rate/recovery delays: compress margins

- 2024 earned returns: ~1.5–3.0% below authorized

Reliance on External Capital Markets

Southwest Gas depends on debt and equity access to fund a $4.3 billion capital plan through 2029; tighter credit or sustained high rates would raise financing costs and stress returns.

Its credit profile improved to a BBB/BBB- level in 2024, but a 1% rise in borrowing costs could add roughly $43 million annually in interest on new debt assuming $4.3 billion issuance over time.

Execution risk grows if market stress hits during peak financing needs, delaying projects or forcing more dilutive equity raises.

- Capital plan: $4.3 billion through 2029

- Credit: BBB/BBB- (2024)

- 1% rate rise ≈ $43M annual extra interest

- Risks: project delays, higher costs, equity dilution

SWX: Gas-focused, cash-strained—high capex, regulatory drag, rising funding needs

SWX is highly concentrated in natural gas (≈$2.5B revenue, 2024) and three states, exposing it to commodity and policy swings; 2024 net income was $230M with payout ~88%, limiting retained cash for a $4.3B capex plan (2025–2029) and increasing debt/equity funding need. Regulatory lag in CA cut earned returns ~150–300bp in 2024; gas-cost deferrals were $287M at year-end 2024.

| Metric | 2024 |

|---|---|

| Revenue from gas | $2.5B |

| Net income | $230M |

| Dividend payout | ~88% |

| Gas cost deferrals | $287M |

| Capex plan | $4.3B (through 2029) |

| CA earned return gap | 150–300 bp below authorized |

Preview the Actual Deliverable

Southwest Gas SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is a real excerpt from the complete, editable file. You’re viewing a live preview of the actual SWOT analysis; buy now to unlock the full, detailed report for Southwest Gas.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Southwest Gas combines a stable utility footprint with regulated revenue streams and strong customer retention, but faces regulatory shifts, infrastructure costs, and decarbonization pressures that could reshape margins and growth—want the full picture? Purchase the complete SWOT analysis to get a professionally written, editable report and Excel matrix with actionable insights for investors, strategists, and advisors.

Strengths

Successful Pure-Play Transformation

By September 2025 Southwest Gas completed separation of Centuri, becoming a pure‑play regulated natural gas utility; the exit was executed via secondary offerings and private placements that raised ~1.4 billion USD, used to eliminate holding‑company debt.

The simplified structure narrows management focus to core utility operations, lowers cyclicality, and removes the construction services valuation discount, supporting a cleaner regulatory earnings profile and likely tighter P/E multiple vs pre‑2025 levels.

Robust Customer Growth in the Sun Belt

Southwest Gas benefits from a prime Sun Belt footprint, adding ~40,000 first‑time meter sets in the 12 months ending Q4 2025, equal to ~1.8% customer growth. This pace outstrips the US utility average (~0.6% in 2024), supplying steady organic revenue and rate‑base expansion. Growth is concentrated in Phoenix and Las Vegas metro areas, where rising residential and commercial connections boost long‑term gas infrastructure demand.

Strengthened Balance Sheet and Credit Profile

Following monetization of its Centuri stake, Southwest Gas strengthened its balance sheet—S&P upgraded its rating to BBB+ in late 2025—after the company fully repaid term loans and bank debt, reducing leverage and interest burden.

With over $1 billion of available liquidity as of December 2025, Southwest Gas now has a resilient capital structure capable of funding multi‑billion dollar capex for system modernization and weathering market volatility.

Constructive Regulatory Progress

Southwest Gas secured favorable regulatory outcomes: Arizona approved a System Integrity Mechanism and Nevada passed alternative ratemaking, both speeding recovery of safety and infrastructure capital and cutting regulatory lag.

Recent rate case settlements lifted allowed return on equity to about 9.8% in core territories, directly improving earnings and cash flow for upcoming capex cycles.

- Arizona: System Integrity Mechanism approved

- Nevada: alternative ratemaking enacted

- Allowed ROE: ~9.8% in key jurisdictions

- Effect: faster capex recovery, lower regulatory lag

Operational Efficiency and Safety Record

Southwest Gas has ranked in the top decile for residential customer satisfaction for six straight years through 2024 and reported a OSHA recordable incident rate 35% below the national gas-utility median in 2024.

Investments in infrared and continuous-monitoring leak detection plus ML-driven asset analytics cut O&M per customer 8% from 2019–2024 and lowered methane intensity by 22% over the same period.

This reliability and safety record creates a regulatory moat, easing rate cases and strengthening community trust across Nevada, Arizona, and California.

- 6 years top-decile satisfaction (through 2024)

- OSHA rate 35% below median (2024)

- O&M/cust down 8% (2019–2024)

- Methane intensity down 22% (2019–2024)

Pure‑play Sun Belt utility: $1.4B delever, 40k new meters, BBB+ & ~9.8% ROE

Pure‑play regulated utility after Centuri exit (Sept 2025); $1.4B proceeds paid holding‑company debt, S&P upgraded to BBB+ (late 2025).

Fast Sun Belt growth: ~40,000 net new meters in 12 months to Q4 2025 (~1.8% customer growth vs US utility 0.6% in 2024).

Regulatory wins: AZ System Integrity, NV alternative ratemaking; allowed ROE ≈9.8%.

| Metric | Value |

|---|---|

| Centuri proceeds | $1.4B |

| Net new meters (12m) | ~40,000 |

| Customer growth | ~1.8% |

| Allowed ROE | ~9.8% |

| Liquidity (Dec 2025) | >$1B |

What is included in the product

Delivers a concise SWOT overview of Southwest Gas, highlighting its operational strengths and regulatory/market weaknesses, identifying growth opportunities like infrastructure modernization and service expansion, and outlining external threats including regulatory pressure, commodity price volatility, and competition.

Delivers a clear Southwest Gas SWOT snapshot for rapid strategic alignment and executive briefings.

Weaknesses

Geographic and Sector Concentration

As a pure-play natural gas utility, Southwest Gas (ticker SWX) earns nearly 100% of revenue from gas, leaving it exposed to commodity- and demand swings; in 2024 gas operations contributed about $2.5B of consolidated revenue, concentrated in Arizona, Nevada, and California.

Unlike diversified peers, SWX lacks electric or water offsets, so regional policy shifts—like California’s aggressive decarbonization targets and Nevada’s 2024 regulatory rate reviews—create outsized earnings risk.

High Dividend Payout Ratio

Southwest Gas has run a dividend payout ratio near 90% (2024 payout ~88%), well above the 60–70% peer range, giving a strong yield but leaving little retained cash for capital projects.

With 2024 net income of $230M, the high payout limits reinvestment into pipelines and meter upgrades and raises reliance on debt or equity for capex.

Any earnings drop of 10–15% could force dividend cuts or new external financing, stressing dividend sustainability.

Exposure to Purchase Gas Price Volatility

Despite a Purchased Gas Adjustment (PGA), Southwest Gas remains exposed to natural gas price swings; the 2022–2024 Henry Hub 12-month average jumped from $4.63/MMBtu (2022) to $6.45/MMBtu (2023), causing large under-collections.

Sudden spikes create deferred regulatory assets—Southwest Gas reported $287M of gas cost deferrals at year-end 2024—straining short-term liquidity and working capital.

Recovery from customers is eventual, but timing gaps cause cash-flow volatility and risk of rate shock; political or regulatory pushback rose after 2023 tariff adjustments in Arizona and Nevada.

Historical Regulatory Lag in California

Southwest Gas faces a persistent regulatory lag in California where proceedings are more stringent and slower than in Arizona and Nevada, delaying new rates and recovery of safety investments.

These delays compressed 2024 operating margins for the California segment, with earned returns running roughly 150–300 basis points below authorized ROE in recent CPUC cases.

- California proceedings: longer, more complex

- Rate/recovery delays: compress margins

- 2024 earned returns: ~1.5–3.0% below authorized

Reliance on External Capital Markets

Southwest Gas depends on debt and equity access to fund a $4.3 billion capital plan through 2029; tighter credit or sustained high rates would raise financing costs and stress returns.

Its credit profile improved to a BBB/BBB- level in 2024, but a 1% rise in borrowing costs could add roughly $43 million annually in interest on new debt assuming $4.3 billion issuance over time.

Execution risk grows if market stress hits during peak financing needs, delaying projects or forcing more dilutive equity raises.

- Capital plan: $4.3 billion through 2029

- Credit: BBB/BBB- (2024)

- 1% rate rise ≈ $43M annual extra interest

- Risks: project delays, higher costs, equity dilution

SWX: Gas-focused, cash-strained—high capex, regulatory drag, rising funding needs

SWX is highly concentrated in natural gas (≈$2.5B revenue, 2024) and three states, exposing it to commodity and policy swings; 2024 net income was $230M with payout ~88%, limiting retained cash for a $4.3B capex plan (2025–2029) and increasing debt/equity funding need. Regulatory lag in CA cut earned returns ~150–300bp in 2024; gas-cost deferrals were $287M at year-end 2024.

| Metric | 2024 |

|---|---|

| Revenue from gas | $2.5B |

| Net income | $230M |

| Dividend payout | ~88% |

| Gas cost deferrals | $287M |

| Capex plan | $4.3B (through 2029) |

| CA earned return gap | 150–300 bp below authorized |

Preview the Actual Deliverable

Southwest Gas SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is a real excerpt from the complete, editable file. You’re viewing a live preview of the actual SWOT analysis; buy now to unlock the full, detailed report for Southwest Gas.