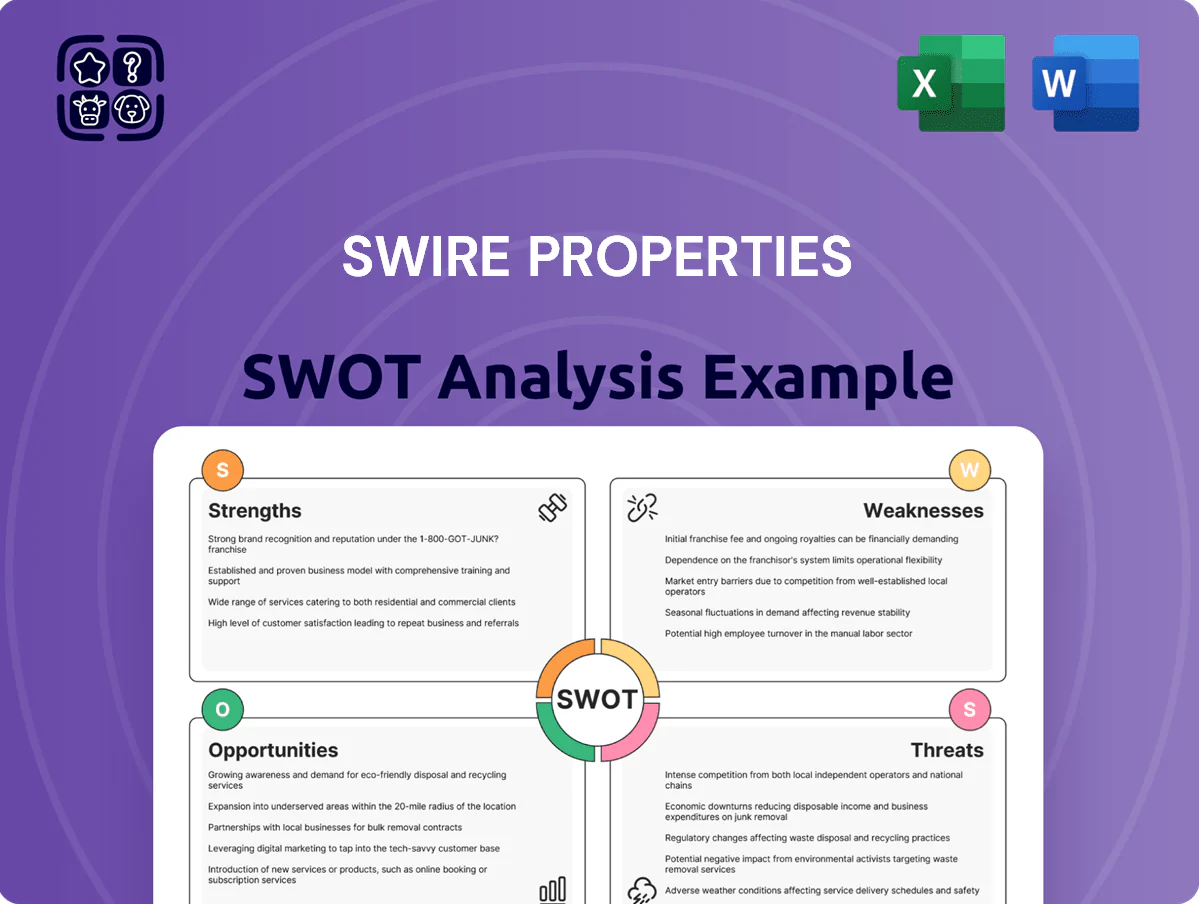

Swire Properties SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Swire Properties balances a premium mixed‑use portfolio and strong Hong Kong brand with exposure to cyclical retail and office demand; emerging markets and sustainability initiatives offer growth but geopolitical and property‑market risks loom. Discover the full SWOT analysis for actionable, research‑backed insights, editable deliverables, and strategic recommendations to support investment or planning decisions—purchase the complete report to access Word and Excel formats.

Strengths

Premium Asset Portfolio and High Occupancy

Swire Properties owns Grade-A offices and luxury retail anchored by Pacific Place and Taikoo Place, with portfolio valuation HKD 142.5 billion at end-2024 and net lettable area ~2.3 million sq ft. These assets command premium rents—office passing rent ~HKD 95/sq ft in core towers—and sustained occupancy above 94% through 2024, even in downturns. A concentrated base of multinational tenants yields stable recurring revenue, supporting dividend growth—2024 payout ratio 48%—and resilient cash flow.

Proven Placemaking and Urban Regeneration Expertise

Swire Properties transforms districts via long-term master plans, delivering mixed-use communities like Taikoo Place and Beijing Sanlitun with £8.2bn (HK$80bn) of completed and ongoing project value as of 2025, boosting footfall and rental premiums across neighborhoods.

Their integrated approach raises surrounding land values and occupancy: Taikoo Place saw office rents rise ~25% from 2018–2024, showing district-level uplift beyond single assets.

This deep placemaking expertise requires multi-decade capital, planning and stakeholder management, creating a high barrier to entry for rivals lacking experience in complex urban regeneration.

Strong Financial Position and Low Gearing

As of late 2025 Swire Properties reported a net gearing of about 10% and HKD 28 billion cash and equivalents, giving a conservative balance sheet that buffers market volatility.

That discipline funds a HKD 100 billion investment plan to 2030 without overextending capital, keeping interest coverage above 6x.

Access to diverse funding—including a HKD 5 billion green bond issued in 2024—helps lower cost of capital and matches global institutional demand.

Leadership in Sustainability and ESG Performance

Swire Properties ranks in the top 10% of the Dow Jones Sustainability World Index (2024) and has science-based targets approved by the Science Based Targets initiative, cutting scope 1–2 emissions 33% by 2023 vs 2019.

High-level green certifications (LEED/BEAM/EDGE) cover over 85% of lettable area, lowering energy costs ~15% and attracting tenants with ESG clauses, which raises terminal asset values.

- Top 10% DJSI World (2024)

- 33% cut in scope 1–2 (2023 vs 2019)

- 85% lettable area green-certified

- ~15% lower energy costs

Strategic Partnership with the Swire Group

Being a Swire Pacific subsidiary gives Swire Properties deep institutional backing and a 200+ year reputation for integrity, supporting credit strength and deal access.

This link enables preferential land sourcing, cross-group project partnerships, and shared resources—Swire Pacific reported HK$96.6 billion total assets in 2024, easing capital support.

The Swire brand boosts confidence with governments and JV partners across Greater China, aiding approvals and joint-venture formation.

- 200+ year brand history

- Swire Pacific assets HK$96.6B (2024)

- Preferential land & JV access

- Stronger govt trust in Greater China

Swire Properties: Premium HKD142.5bn portfolio, >94% occupancy, low gearing & green leader

Swire Properties owns premium Grade-A offices and retail (portfolio HKD 142.5bn end‑2024; NLA ~2.3m sq ft), high occupancy >94% and office passing rent ~HKD95/sq ft, low net gearing ~10% with HKD28bn cash (late‑2025), HKD100bn capex plan to 2030, top 10% DJSI World (2024) and 85% green‑certified lettable area.

| Metric | Value |

|---|---|

| Portfolio value | HKD142.5bn (end‑2024) |

| NLA | ~2.3m sq ft |

| Occupancy | >94% (2024) |

| Net gearing | ~10% (late‑2025) |

| Cash | HKD28bn (late‑2025) |

| Capex plan | HKD100bn to 2030 |

| DJSI | Top 10% (2024) |

| Green area | 85% lettable |

What is included in the product

Delivers a concise SWOT overview of Swire Properties, highlighting its core strengths in prime mixed‑use developments and strong balance sheet, weaknesses from geographic concentration and capital intensity, opportunities in urban redevelopment and sustainability trends, and threats from market cyclicality and regulatory shifts.

Provides a concise SWOT matrix of Swire Properties for fast strategy alignment and stakeholder-ready summaries, ideal for executives seeking a clear snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

High Geographic Concentration in Greater China

About 75% of Swire Properties revenue and over HKD 150 billion of investment properties were from Hong Kong and Mainland China in FY2024, so regional slowdowns hit income and NAV hard.

This concentration ties cash flow to Greater China cycles; the 2022–24 retail footfall slump and tighter PRC mortgage curbs show how local policy or demand shifts can compress rents and valuations.

Exposure to Structural Shifts in Office Demand

The rise of hybrid work cuts demand for large CBD floor plates; global office occupancy stayed ~80% of pre-pandemic levels in 2024 per CBRE, and Hong Kong CBD rents slipped 6% in 2024, pressuring landlords. Swire Properties’ Grade-A stock is more resilient, but sustained downsizing by multinationals could reduce long-term rental yields from current HK office yields (~3.5% in 2024).

Swire must keep investing in tech upgrades, air quality, and wellness amenities—CapEx for Hong Kong office retrofits averaged 5–8% of asset value in recent peer programs—to avoid leasing obsolescence and higher vacancy costs.

Dependency on Luxury Retail Sentiment

The retail portfolio is concentrated in luxury brands, exposing Swire Properties to swings in discretionary spending; luxury accounted for an estimated 60% of mall GFA in Hong Kong and mainland flagship malls in 2024. Tourist arrivals to Hong Kong fell 25% year-on-year in 2023 vs 2019 levels, and mainland middle-class real wage growth slowed to about 3% in 2024, raising volatility in turnover rents. Turnover-based rent structures amplified income cyclicality: retail revenue fell 18% in 2022 during downturns in luxury sales. This specialization makes retail income more cyclical than essential-goods–anchored centres.

Long Development Cycles and Capital Intensity

Swire Properties’ focus on large mixed-use projects requires massive upfront capital and multi-year development; for example, its 2024 balance sheet showed HKD 61.3 billion in property, plant and equipment tied to ongoing projects, delaying returns.

These long lead times expose cash flows to interest-rate swings (HK base rates rose ~175 basis points 2022–24) and construction inflation—Hong Kong contractor costs climbed ~8% in 2023.

Slow capital turnover limits agility versus short-cycle market shifts, reducing ability to reallocate capital quickly during demand swings or economic shocks.

- HKD 61.3bn tied in projects (2024)

- Interest rates up ~175 bps (2022–24)

- Construction costs +8% (2023)

- Multi-year payback limits flexibility

Limited Presence in High-Growth Residential Segments

Compared with peers, Swire Properties held ~5% of Hong Kong residential starts in 2024 versus >20% for major mass-market developers, reflecting a smaller footprint in volume housing.

The focus on high-end projects limits access to broad housing demand and fast, high-volume cash flows common in mass-market cycles.

Luxury bias ties sales to high-net-worth demographics; Swire reported HKD 9.2bn residential revenue in FY2024, concentrated in premium units.

- ~5% HK residential starts (2024)

- HKD 9.2bn residential revenue FY2024

- High-end sales = concentrated wealth risk

High China Concentration, Luxury Retail & Large Projects Drive NAV and Income Risk

Concentration in Greater China (≈75% revenue; HKD150bn+ investment properties FY2024) makes income and NAV sensitive to local slowdowns; retail luxury exposure (~60% GFA) and turnover rents amplify cyclicality. Large mixed-use projects tie HKD61.3bn in PP&E (2024), extend payback, and raise rate/construction-cost risk (rates +175bps 2022–24; construction +8% 2023).

| Metric | Value |

|---|---|

| Revenue concentration | ≈75% Greater China |

| Investment properties | HKD150bn+ |

| PP&E tied to projects | HKD61.3bn (2024) |

| Luxury retail GFA | ≈60% |

| Rates change | +175 bps (2022–24) |

| Construction costs | +8% (2023) |

Preview the Actual Deliverable

Swire Properties SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Swire Properties balances a premium mixed‑use portfolio and strong Hong Kong brand with exposure to cyclical retail and office demand; emerging markets and sustainability initiatives offer growth but geopolitical and property‑market risks loom. Discover the full SWOT analysis for actionable, research‑backed insights, editable deliverables, and strategic recommendations to support investment or planning decisions—purchase the complete report to access Word and Excel formats.

Strengths

Premium Asset Portfolio and High Occupancy

Swire Properties owns Grade-A offices and luxury retail anchored by Pacific Place and Taikoo Place, with portfolio valuation HKD 142.5 billion at end-2024 and net lettable area ~2.3 million sq ft. These assets command premium rents—office passing rent ~HKD 95/sq ft in core towers—and sustained occupancy above 94% through 2024, even in downturns. A concentrated base of multinational tenants yields stable recurring revenue, supporting dividend growth—2024 payout ratio 48%—and resilient cash flow.

Proven Placemaking and Urban Regeneration Expertise

Swire Properties transforms districts via long-term master plans, delivering mixed-use communities like Taikoo Place and Beijing Sanlitun with £8.2bn (HK$80bn) of completed and ongoing project value as of 2025, boosting footfall and rental premiums across neighborhoods.

Their integrated approach raises surrounding land values and occupancy: Taikoo Place saw office rents rise ~25% from 2018–2024, showing district-level uplift beyond single assets.

This deep placemaking expertise requires multi-decade capital, planning and stakeholder management, creating a high barrier to entry for rivals lacking experience in complex urban regeneration.

Strong Financial Position and Low Gearing

As of late 2025 Swire Properties reported a net gearing of about 10% and HKD 28 billion cash and equivalents, giving a conservative balance sheet that buffers market volatility.

That discipline funds a HKD 100 billion investment plan to 2030 without overextending capital, keeping interest coverage above 6x.

Access to diverse funding—including a HKD 5 billion green bond issued in 2024—helps lower cost of capital and matches global institutional demand.

Leadership in Sustainability and ESG Performance

Swire Properties ranks in the top 10% of the Dow Jones Sustainability World Index (2024) and has science-based targets approved by the Science Based Targets initiative, cutting scope 1–2 emissions 33% by 2023 vs 2019.

High-level green certifications (LEED/BEAM/EDGE) cover over 85% of lettable area, lowering energy costs ~15% and attracting tenants with ESG clauses, which raises terminal asset values.

- Top 10% DJSI World (2024)

- 33% cut in scope 1–2 (2023 vs 2019)

- 85% lettable area green-certified

- ~15% lower energy costs

Strategic Partnership with the Swire Group

Being a Swire Pacific subsidiary gives Swire Properties deep institutional backing and a 200+ year reputation for integrity, supporting credit strength and deal access.

This link enables preferential land sourcing, cross-group project partnerships, and shared resources—Swire Pacific reported HK$96.6 billion total assets in 2024, easing capital support.

The Swire brand boosts confidence with governments and JV partners across Greater China, aiding approvals and joint-venture formation.

- 200+ year brand history

- Swire Pacific assets HK$96.6B (2024)

- Preferential land & JV access

- Stronger govt trust in Greater China

Swire Properties: Premium HKD142.5bn portfolio, >94% occupancy, low gearing & green leader

Swire Properties owns premium Grade-A offices and retail (portfolio HKD 142.5bn end‑2024; NLA ~2.3m sq ft), high occupancy >94% and office passing rent ~HKD95/sq ft, low net gearing ~10% with HKD28bn cash (late‑2025), HKD100bn capex plan to 2030, top 10% DJSI World (2024) and 85% green‑certified lettable area.

| Metric | Value |

|---|---|

| Portfolio value | HKD142.5bn (end‑2024) |

| NLA | ~2.3m sq ft |

| Occupancy | >94% (2024) |

| Net gearing | ~10% (late‑2025) |

| Cash | HKD28bn (late‑2025) |

| Capex plan | HKD100bn to 2030 |

| DJSI | Top 10% (2024) |

| Green area | 85% lettable |

What is included in the product

Delivers a concise SWOT overview of Swire Properties, highlighting its core strengths in prime mixed‑use developments and strong balance sheet, weaknesses from geographic concentration and capital intensity, opportunities in urban redevelopment and sustainability trends, and threats from market cyclicality and regulatory shifts.

Provides a concise SWOT matrix of Swire Properties for fast strategy alignment and stakeholder-ready summaries, ideal for executives seeking a clear snapshot of strengths, weaknesses, opportunities, and threats.

Weaknesses

High Geographic Concentration in Greater China

About 75% of Swire Properties revenue and over HKD 150 billion of investment properties were from Hong Kong and Mainland China in FY2024, so regional slowdowns hit income and NAV hard.

This concentration ties cash flow to Greater China cycles; the 2022–24 retail footfall slump and tighter PRC mortgage curbs show how local policy or demand shifts can compress rents and valuations.

Exposure to Structural Shifts in Office Demand

The rise of hybrid work cuts demand for large CBD floor plates; global office occupancy stayed ~80% of pre-pandemic levels in 2024 per CBRE, and Hong Kong CBD rents slipped 6% in 2024, pressuring landlords. Swire Properties’ Grade-A stock is more resilient, but sustained downsizing by multinationals could reduce long-term rental yields from current HK office yields (~3.5% in 2024).

Swire must keep investing in tech upgrades, air quality, and wellness amenities—CapEx for Hong Kong office retrofits averaged 5–8% of asset value in recent peer programs—to avoid leasing obsolescence and higher vacancy costs.

Dependency on Luxury Retail Sentiment

The retail portfolio is concentrated in luxury brands, exposing Swire Properties to swings in discretionary spending; luxury accounted for an estimated 60% of mall GFA in Hong Kong and mainland flagship malls in 2024. Tourist arrivals to Hong Kong fell 25% year-on-year in 2023 vs 2019 levels, and mainland middle-class real wage growth slowed to about 3% in 2024, raising volatility in turnover rents. Turnover-based rent structures amplified income cyclicality: retail revenue fell 18% in 2022 during downturns in luxury sales. This specialization makes retail income more cyclical than essential-goods–anchored centres.

Long Development Cycles and Capital Intensity

Swire Properties’ focus on large mixed-use projects requires massive upfront capital and multi-year development; for example, its 2024 balance sheet showed HKD 61.3 billion in property, plant and equipment tied to ongoing projects, delaying returns.

These long lead times expose cash flows to interest-rate swings (HK base rates rose ~175 basis points 2022–24) and construction inflation—Hong Kong contractor costs climbed ~8% in 2023.

Slow capital turnover limits agility versus short-cycle market shifts, reducing ability to reallocate capital quickly during demand swings or economic shocks.

- HKD 61.3bn tied in projects (2024)

- Interest rates up ~175 bps (2022–24)

- Construction costs +8% (2023)

- Multi-year payback limits flexibility

Limited Presence in High-Growth Residential Segments

Compared with peers, Swire Properties held ~5% of Hong Kong residential starts in 2024 versus >20% for major mass-market developers, reflecting a smaller footprint in volume housing.

The focus on high-end projects limits access to broad housing demand and fast, high-volume cash flows common in mass-market cycles.

Luxury bias ties sales to high-net-worth demographics; Swire reported HKD 9.2bn residential revenue in FY2024, concentrated in premium units.

- ~5% HK residential starts (2024)

- HKD 9.2bn residential revenue FY2024

- High-end sales = concentrated wealth risk

High China Concentration, Luxury Retail & Large Projects Drive NAV and Income Risk

Concentration in Greater China (≈75% revenue; HKD150bn+ investment properties FY2024) makes income and NAV sensitive to local slowdowns; retail luxury exposure (~60% GFA) and turnover rents amplify cyclicality. Large mixed-use projects tie HKD61.3bn in PP&E (2024), extend payback, and raise rate/construction-cost risk (rates +175bps 2022–24; construction +8% 2023).

| Metric | Value |

|---|---|

| Revenue concentration | ≈75% Greater China |

| Investment properties | HKD150bn+ |

| PP&E tied to projects | HKD61.3bn (2024) |

| Luxury retail GFA | ≈60% |

| Rates change | +175 bps (2022–24) |

| Construction costs | +8% (2023) |

Preview the Actual Deliverable

Swire Properties SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.