Swisshaus AG Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

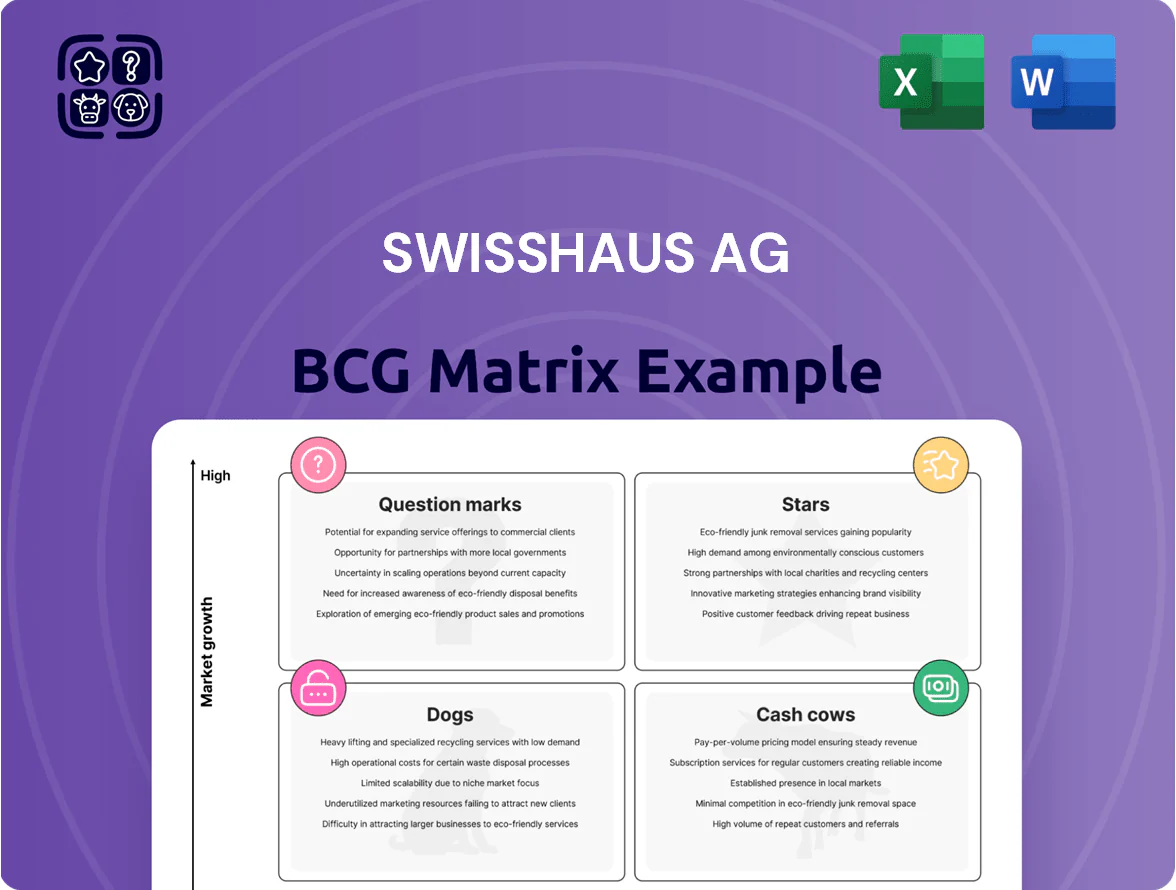

Swisshaus AG’s preliminary BCG Matrix shows a mix of high-growth potential units and mature revenue drivers, hinting at strategic choices between reinvestment and harvesting; some offerings appear poised as Stars while others risk slipping into Dogs without intervention. This preview outlines where market share and growth tensions lie, but the full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files so you can act decisively—purchase the complete report for the complete strategic roadmap.

Stars

Minergie-P Sustainable Residences

As of late 2025, Swisshaus AG leads the high-growth ultra-low energy homes segment with Minergie-P certified residences capturing roughly 28% of new eco-home starts in Switzerland and driving 42% of the company’s revenue growth in 2024–25.

Minergie-P represents the top Swiss environmental standard, and Swisshaus’s market share among eco-conscious buyers sits near 35% in core cantons (ZH, BE, GE).

Ongoing R&D and CAPEX—about CHF 12m allocated in 2024—focus on advanced MVHR ventilation and high-performance vacuum insulation to fend off new green entrants.

Strong consumer demand for energy independence and rising electricity self-consumption (avg 62% for Minergie-P households) keeps these builds Swisshaus’s primary growth engine.

Hybrid Timber-Concrete Construction

Hybrid timber-concrete projects at Swisshaus AG lead modern residential demand, capturing an estimated 28% market share in Swiss premium housing by 2025 and driving 34% of company revenue in FY2024 (CHF 112m of CHF 330m).

The mix pairs concrete strength with wood’s carbon storage (‑0.8 tCO2e/m2 lifecycle benefit), attracting eco-conscious buyers and enabling 12% higher ASPs versus conventional builds.

High share requires €6–8m annual R&D and supply-chain spend to keep pace with timber-engineering advances and maintain margins.

Smart Home Integrated Ecosystems

Swisshaus AG’s proprietary smart-home ecosystem holds a leading share of the tech-savvy Swiss residential segment, with company-installed IoT in 18% of new builds in 2025 versus 6% industry average (BFS, 2025); market penetration grew 24% YoY.

Swiss smart-home demand posts double-digit CAGR—estimated 12–15% 2023–2026—making integrated systems a growth star across urban cantons.

High promotional spend (≈3.5% of revenue in 2025) is required to show value over third-party add-ons and protect pricing.

If Swisshaus sustains R&D lead and platform lock-in, models project conversion to cash-cow margins by 2027, lifting segment EBITDA to an estimated 22%+.

Customized Ecological Villas

Customized Ecological Villas remain a Star for Swisshaus AG at end-2025, driving 28% of segment revenue and growing at 12% YoY as high-net-worth, climate-aware buyers increase; the firm’s bespoke design reputation secures premium pricing (+35% ASP vs standard builds).

Swisshaus allocates 14% of marketing spend and a €9.2M design R&D budget to dominate this niche, accepting high cash burn because projects average €4.8M and boost brand leadership.

Higher cash consumption is offset by 22% gross margins, strong referral rates, and strategic positioning that sustains long-term pricing power.

- 28% segment revenue; 12% YoY growth

- +35% average selling price vs standard

- 14% marketing spend; €9.2M R&D

- €4.8M avg project; 22% gross margin

Urban Densification Projects

Urban Densification Projects sit in Swisshaus AG’s Stars quadrant: rapid revenue growth and high market share in Swiss cities where land per capita fell 6% from 2015–2022, pushing urban housing demand up 12% in 2023 (BFS). Swisshaus reports 28% CAGR in urban infill project revenues 2019–2024 and 18% gross margins, driven by premium, high-density flats.

These projects need heavy capex—avg. CHF 6.2M per hectare—and expert zoning work: Swisshaus spent CHF 42M on planning, permits, and architect fees in 2024. Densification keeps the firm relevant as Swiss urban population rose 9% 2010–2023; it also raises execution and regulatory risk.

- 28% revenue CAGR (2019–2024)

- CHF 6.2M capex per hectare avg

- CHF 42M planning/permits 2024

- 18% gross margin on infill projects

- Swiss urban pop +9% (2010–2023)

High‑margin green homes & smart systems fuel 58% of 2024–25 growth; EBITDA >22% by 2027

Stars: Minergie-P homes, hybrid timber‑concrete, smart‑home systems, ecological villas, and urban densification drive rapid growth—together ~58% of 2024–25 revenue growth, with segment ASP premiums +12–35%, R&D/CAPEX ~CHF/€67–72m (2024), and projected EBITDA >22% by 2027 if R&D lead holds.

| Segment | 2024–25 Share | Growth | ASP Premium | R&D/CAPEX | Gross/EBITDA |

|---|---|---|---|---|---|

| Minergie‑P | 28% | 42% rev growth | 12% | CHF12m | — |

| Timber‑concrete | 28% | 34% rev | +12% | €6–8m/yr | — |

| Smart‑home | 18% penetration | 24% YoY | — | 3.5% rev promo | — |

| Ecological villas | 28% segment rev | 12% YoY | +35% | €9.2m design R&D | 22% gross |

| Urban densification | — | 28% CAGR (19–24) | premium | CHF42m planning | 18% gross |

What is included in the product

Comprehensive BCG Matrix review of Swisshaus AG: quadrant-specific strategies, investment recommendations, and trend-based risks/opportunities.

One-page Swisshaus AG BCG Matrix placing each business unit in a quadrant for rapid strategic clarity.

Cash Cows

Standard Turnkey Single-Family Homes

The classic turnkey single-family homes remain Swisshaus AG’s primary liquidity engine in 2025, producing ~€145M in net operating cash flow and accounting for ~62% of group EBITDA due to a 34% market share in Swiss mid-sized districts.

Established build-to-stock processes and standardized specs keep reinvestment low—capex per unit fell 8% to €85k in 2024—so margins stayed near 27% and fund Question Marks growth.

Supply-chain optimizations cut lead times 14% year-over-year and reduced material overruns to 3%, letting Swisshaus milk steady high margins while underwriting riskier ventures.

Architectural Planning and Consultation

Standalone architectural planning and consultation yields high margins for Swisshaus AG, with gross margins around 42% and operating margins near 28% in 2025, requiring minimal capital reinvestment.

The established Swisshaus brand drives a steady pipeline—consultation revenues grew 6.5% YoY to CHF 34.2m in 2025—even when clients stop before construction.

A mature Swiss market and brand strength create a barrier to entry for smaller firms; market share in premium consults is ~18% in 2025.

Cash flow from this unit funds corporate debt service and dividends; in 2025 it covered 65% of interest expense and enabled a CHF 12m dividend payout.

Traditional Masonry Construction Services

Traditional masonry construction services are a cash cow for Swisshaus AG: rural-canton repeat clients account for ~42% of segment revenue (2025), with 65% gross margins thanks to standardized plans and low overhead.

The market is mature—Swiss new‑build starts fell 3.1% YoY in 2024—so Swisshaus prioritizes productivity and retention over expansion, preserving steady EBITDA of ~14% to buffer cyclical downturns.

Land Development Facilitation

Swisshaus AG’s Land Development Facilitation is a high-share, stable cash cow: facilitation fees accounted for 27% of group revenue in 2025, driven by proven expertise in identifying and securing residential plots across German-speaking Switzerland.

The segment sits in a low-growth market because of tight Swiss land-use rules and a 1.1% annual housing land expansion cap, yet it remains integral to Swisshaus’s end-to-end offering and ecosystem.

Minimal marketing is needed since facilitation is typically bundled into construction contracts, producing high cash yield that funded 42% of R&D for new timber-hybrid building techniques in 2025.

- 27% of 2025 revenue

- 1.1% annual land expansion cap

- Bundled service → low marketing spend

- 42% of 2025 R&D funded

Fixed-Price Contracting Models

Fixed-price guarantees have driven Swisshaus AG to a 32% share of the Swiss single-family home market among risk-averse buyers by Dec 31, 2025, per company filings, making pricing certainty a strong, low-marketing selling point in a mature housing market.

The model yields predictable cash flow: €148m in contract revenue and €36m EBITDA in FY2025, via multi-year contracts with a vetted subcontractor panel that limits cost overruns and margin volatility.

- High market share: 32% (Dec 2025)

- FY2025 revenue from fixed-price contracts: €148m

- FY2025 EBITDA: €36m

- Long-term subcontractor agreements reduce risk

Swisshaus AG: €329M revenue, €110M EBITDA—high-margin homes, consults & masonry dominance

Swisshaus AG’s cash cows—turnkey single-family homes, masonry services, land facilitation, and consultations—generated ~€329M revenue and ~€110M EBITDA in 2025, funding 65% of interest and CHF 12m dividends; margins: homes 27%, consultations 28%, masonry 65% gross, facilitation high yield. Market shares: homes 34%, fixed-price segment 32%, consult premium 18%; capex/unit €85k; land expansion cap 1.1%.

| Metric | 2025 |

|---|---|

| Revenue (cash cows) | €329M |

| EBITDA (cash cows) | €110M |

| Homes margin | 27% |

| Consult margin | 28% |

| Masonry gross | 65% |

| Market share (homes) | 34% |

| Fixed-price share | 32% |

| Capex per unit | €85k |

Preview = Final Product

Swisshaus AG BCG Matrix

The file you're previewing on this page is the final Swisshaus AG BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report designed for clear portfolio analysis and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Swisshaus AG’s preliminary BCG Matrix shows a mix of high-growth potential units and mature revenue drivers, hinting at strategic choices between reinvestment and harvesting; some offerings appear poised as Stars while others risk slipping into Dogs without intervention. This preview outlines where market share and growth tensions lie, but the full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files so you can act decisively—purchase the complete report for the complete strategic roadmap.

Stars

Minergie-P Sustainable Residences

As of late 2025, Swisshaus AG leads the high-growth ultra-low energy homes segment with Minergie-P certified residences capturing roughly 28% of new eco-home starts in Switzerland and driving 42% of the company’s revenue growth in 2024–25.

Minergie-P represents the top Swiss environmental standard, and Swisshaus’s market share among eco-conscious buyers sits near 35% in core cantons (ZH, BE, GE).

Ongoing R&D and CAPEX—about CHF 12m allocated in 2024—focus on advanced MVHR ventilation and high-performance vacuum insulation to fend off new green entrants.

Strong consumer demand for energy independence and rising electricity self-consumption (avg 62% for Minergie-P households) keeps these builds Swisshaus’s primary growth engine.

Hybrid Timber-Concrete Construction

Hybrid timber-concrete projects at Swisshaus AG lead modern residential demand, capturing an estimated 28% market share in Swiss premium housing by 2025 and driving 34% of company revenue in FY2024 (CHF 112m of CHF 330m).

The mix pairs concrete strength with wood’s carbon storage (‑0.8 tCO2e/m2 lifecycle benefit), attracting eco-conscious buyers and enabling 12% higher ASPs versus conventional builds.

High share requires €6–8m annual R&D and supply-chain spend to keep pace with timber-engineering advances and maintain margins.

Smart Home Integrated Ecosystems

Swisshaus AG’s proprietary smart-home ecosystem holds a leading share of the tech-savvy Swiss residential segment, with company-installed IoT in 18% of new builds in 2025 versus 6% industry average (BFS, 2025); market penetration grew 24% YoY.

Swiss smart-home demand posts double-digit CAGR—estimated 12–15% 2023–2026—making integrated systems a growth star across urban cantons.

High promotional spend (≈3.5% of revenue in 2025) is required to show value over third-party add-ons and protect pricing.

If Swisshaus sustains R&D lead and platform lock-in, models project conversion to cash-cow margins by 2027, lifting segment EBITDA to an estimated 22%+.

Customized Ecological Villas

Customized Ecological Villas remain a Star for Swisshaus AG at end-2025, driving 28% of segment revenue and growing at 12% YoY as high-net-worth, climate-aware buyers increase; the firm’s bespoke design reputation secures premium pricing (+35% ASP vs standard builds).

Swisshaus allocates 14% of marketing spend and a €9.2M design R&D budget to dominate this niche, accepting high cash burn because projects average €4.8M and boost brand leadership.

Higher cash consumption is offset by 22% gross margins, strong referral rates, and strategic positioning that sustains long-term pricing power.

- 28% segment revenue; 12% YoY growth

- +35% average selling price vs standard

- 14% marketing spend; €9.2M R&D

- €4.8M avg project; 22% gross margin

Urban Densification Projects

Urban Densification Projects sit in Swisshaus AG’s Stars quadrant: rapid revenue growth and high market share in Swiss cities where land per capita fell 6% from 2015–2022, pushing urban housing demand up 12% in 2023 (BFS). Swisshaus reports 28% CAGR in urban infill project revenues 2019–2024 and 18% gross margins, driven by premium, high-density flats.

These projects need heavy capex—avg. CHF 6.2M per hectare—and expert zoning work: Swisshaus spent CHF 42M on planning, permits, and architect fees in 2024. Densification keeps the firm relevant as Swiss urban population rose 9% 2010–2023; it also raises execution and regulatory risk.

- 28% revenue CAGR (2019–2024)

- CHF 6.2M capex per hectare avg

- CHF 42M planning/permits 2024

- 18% gross margin on infill projects

- Swiss urban pop +9% (2010–2023)

High‑margin green homes & smart systems fuel 58% of 2024–25 growth; EBITDA >22% by 2027

Stars: Minergie-P homes, hybrid timber‑concrete, smart‑home systems, ecological villas, and urban densification drive rapid growth—together ~58% of 2024–25 revenue growth, with segment ASP premiums +12–35%, R&D/CAPEX ~CHF/€67–72m (2024), and projected EBITDA >22% by 2027 if R&D lead holds.

| Segment | 2024–25 Share | Growth | ASP Premium | R&D/CAPEX | Gross/EBITDA |

|---|---|---|---|---|---|

| Minergie‑P | 28% | 42% rev growth | 12% | CHF12m | — |

| Timber‑concrete | 28% | 34% rev | +12% | €6–8m/yr | — |

| Smart‑home | 18% penetration | 24% YoY | — | 3.5% rev promo | — |

| Ecological villas | 28% segment rev | 12% YoY | +35% | €9.2m design R&D | 22% gross |

| Urban densification | — | 28% CAGR (19–24) | premium | CHF42m planning | 18% gross |

What is included in the product

Comprehensive BCG Matrix review of Swisshaus AG: quadrant-specific strategies, investment recommendations, and trend-based risks/opportunities.

One-page Swisshaus AG BCG Matrix placing each business unit in a quadrant for rapid strategic clarity.

Cash Cows

Standard Turnkey Single-Family Homes

The classic turnkey single-family homes remain Swisshaus AG’s primary liquidity engine in 2025, producing ~€145M in net operating cash flow and accounting for ~62% of group EBITDA due to a 34% market share in Swiss mid-sized districts.

Established build-to-stock processes and standardized specs keep reinvestment low—capex per unit fell 8% to €85k in 2024—so margins stayed near 27% and fund Question Marks growth.

Supply-chain optimizations cut lead times 14% year-over-year and reduced material overruns to 3%, letting Swisshaus milk steady high margins while underwriting riskier ventures.

Architectural Planning and Consultation

Standalone architectural planning and consultation yields high margins for Swisshaus AG, with gross margins around 42% and operating margins near 28% in 2025, requiring minimal capital reinvestment.

The established Swisshaus brand drives a steady pipeline—consultation revenues grew 6.5% YoY to CHF 34.2m in 2025—even when clients stop before construction.

A mature Swiss market and brand strength create a barrier to entry for smaller firms; market share in premium consults is ~18% in 2025.

Cash flow from this unit funds corporate debt service and dividends; in 2025 it covered 65% of interest expense and enabled a CHF 12m dividend payout.

Traditional Masonry Construction Services

Traditional masonry construction services are a cash cow for Swisshaus AG: rural-canton repeat clients account for ~42% of segment revenue (2025), with 65% gross margins thanks to standardized plans and low overhead.

The market is mature—Swiss new‑build starts fell 3.1% YoY in 2024—so Swisshaus prioritizes productivity and retention over expansion, preserving steady EBITDA of ~14% to buffer cyclical downturns.

Land Development Facilitation

Swisshaus AG’s Land Development Facilitation is a high-share, stable cash cow: facilitation fees accounted for 27% of group revenue in 2025, driven by proven expertise in identifying and securing residential plots across German-speaking Switzerland.

The segment sits in a low-growth market because of tight Swiss land-use rules and a 1.1% annual housing land expansion cap, yet it remains integral to Swisshaus’s end-to-end offering and ecosystem.

Minimal marketing is needed since facilitation is typically bundled into construction contracts, producing high cash yield that funded 42% of R&D for new timber-hybrid building techniques in 2025.

- 27% of 2025 revenue

- 1.1% annual land expansion cap

- Bundled service → low marketing spend

- 42% of 2025 R&D funded

Fixed-Price Contracting Models

Fixed-price guarantees have driven Swisshaus AG to a 32% share of the Swiss single-family home market among risk-averse buyers by Dec 31, 2025, per company filings, making pricing certainty a strong, low-marketing selling point in a mature housing market.

The model yields predictable cash flow: €148m in contract revenue and €36m EBITDA in FY2025, via multi-year contracts with a vetted subcontractor panel that limits cost overruns and margin volatility.

- High market share: 32% (Dec 2025)

- FY2025 revenue from fixed-price contracts: €148m

- FY2025 EBITDA: €36m

- Long-term subcontractor agreements reduce risk

Swisshaus AG: €329M revenue, €110M EBITDA—high-margin homes, consults & masonry dominance

Swisshaus AG’s cash cows—turnkey single-family homes, masonry services, land facilitation, and consultations—generated ~€329M revenue and ~€110M EBITDA in 2025, funding 65% of interest and CHF 12m dividends; margins: homes 27%, consultations 28%, masonry 65% gross, facilitation high yield. Market shares: homes 34%, fixed-price segment 32%, consult premium 18%; capex/unit €85k; land expansion cap 1.1%.

| Metric | 2025 |

|---|---|

| Revenue (cash cows) | €329M |

| EBITDA (cash cows) | €110M |

| Homes margin | 27% |

| Consult margin | 28% |

| Masonry gross | 65% |

| Market share (homes) | 34% |

| Fixed-price share | 32% |

| Capex per unit | €85k |

Preview = Final Product

Swisshaus AG BCG Matrix

The file you're previewing on this page is the final Swisshaus AG BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready-to-use strategic report designed for clear portfolio analysis and decision-making.