Sydbank Porter's Five Forces Analysis

Don't Miss the Bigger Picture

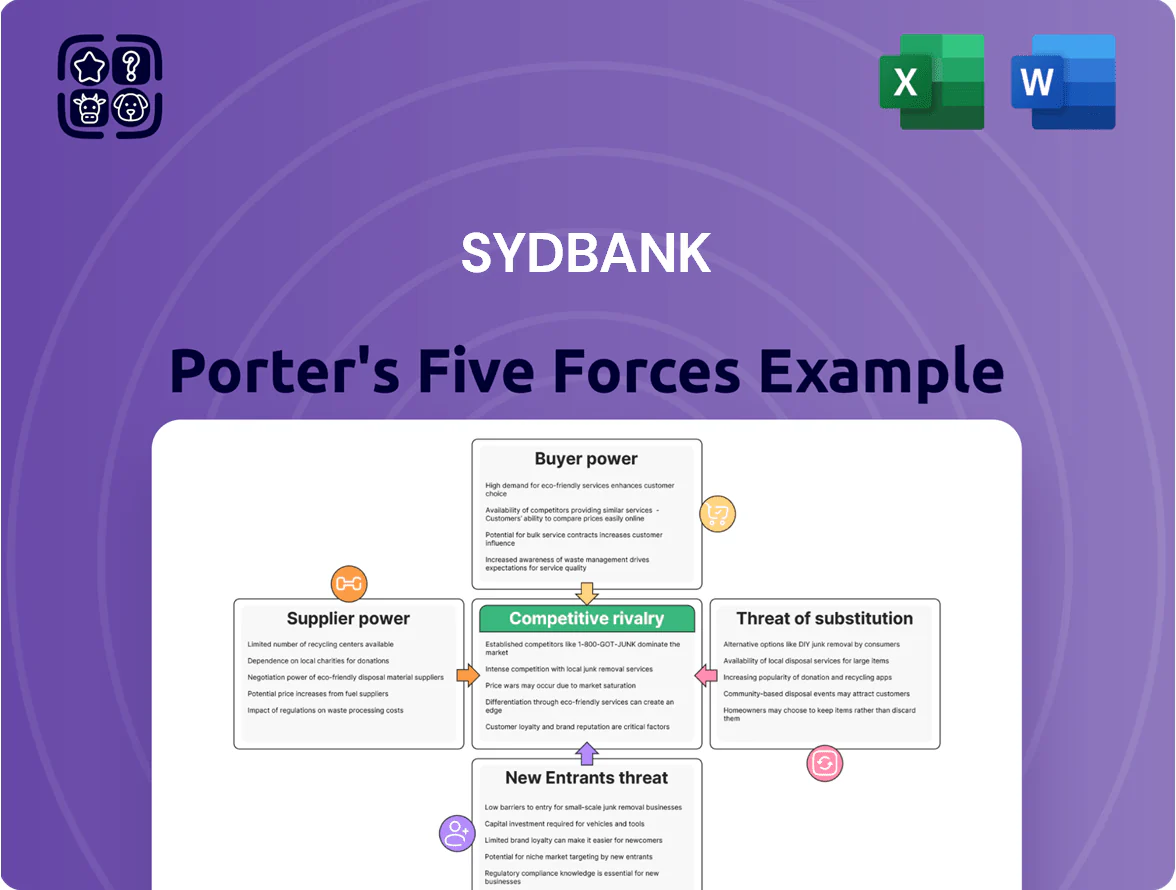

Sydbank faces moderate competitive intensity—strong local brand loyalty and scale advantages versus rising fintech rivals and margin pressure from low-rate lending; supplier power is limited but regulatory costs and digital investment elevate operational strain. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sydbank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on IT Infrastructure Providers

Sydbank depends heavily on Bankdata for core banking and digital infrastructure, creating supplier power since switching would cost an estimated DKK 200–400m and take 18–36 months for a mid-sized bank.

Technical complexity and data migration risks raise dependency, so Bankdata can demand premium terms that squeeze margins.

By late 2025, rising needs for advanced cybersecurity and AI (estimated 25–40% higher spend) further strengthen specialized vendors’ bargaining power.

Talent War for Specialized Financial Professionals

The Danish market for financial analysts and IT specialists stayed tight into 2025, with unemployment for finance grads at ~1.8% and tech vacancy rates near 4.2% (Danmarks Statistik, Q4 2024), forcing Sydbank to match offers from Danske Bank and Nordic fintechs.

To retain talent Sydbank increased average analyst pay ~6% in 2024 and flagged €10–15k sign-on packages for senior hires, raising personnel cost pressure and boosting supplier power in its service model.

Influence of Central Banks and Capital Markets

Sydbank funds itself via fragmented retail deposits and wholesale markets; at end-2024 Sydbank reported deposit funding covering ~62% of assets and wholesale debt ~18% (source: Sydbank 2024 annual report).

ECB rates and global bond yields set the baseline funding cost—ECB deposit rate rose to 4.00% in Dec 2023 and 3‑month EURIBOR averaged 3.5% through 2024—pressuring net interest margin.

Monetary policy shifts remain the main external constraint on margin management: a 100bp ECB cut would cut funding cost slowly; a 100bp hike in 2024‑style moves would have widened funding expense materially.

Regulatory Compliance and Audit Service Costs

Outsourcing of Non-Core Banking Functions

- Outsourcing spend ~DKK 450m (post-2023)

- Vendors more interchangeable than IT providers

- Higher specialization raises disruption risk

- Service delays can hit customer satisfaction

High supplier power: costly banklock, premium cyber/AI vendors & rising funding/reg costs

High supplier power: Bankdata dependency (switch cost DKK 200–400m; 18–36 months) plus specialized cyber/AI vendors (25–40% higher spend) and tight labor market (finance unemployment ~1.8%; tech vacancies 4.2%) raise costs; funding set by ECB rates (deposit rate 4.00% Dec 2023) and regulatory compliance (Sydbank regulatory costs +12% in 2024) further strengthen supplier power.

What is included in the product

Provides a concise Porter's Five Forces view of Sydbank, highlighting competitive rivalry, buyer/supplier leverage, entry barriers, and substitute threats with industry-backed insights tailored for strategic use.

Clear, one-sheet Porter's Five Forces for Sydbank—instantly spot competitive pressures and relieve strategic planning bottlenecks with a ready-to-use radar chart and editable pressure sliders.

Customers Bargaining Power

Low Switching Costs for Retail Banking

Digital platforms and open banking have cut switching time; EU-DK PSD2 adoption and Bankernes IT-Center APIs let Danish retail customers move accounts in days, not weeks.

By late 2025, automated switching services reduced friction ~40%, per Nordic Payments 2024–25 data, raising annual churn risk if fees or NPS lag peers.

Sydbank must keep service levels high and match fee reductions—median Danish checking fees fell 12% in 2024—to retain deposits and fee income.

Increased Price Transparency via Digital Tools

Online comparison tools let Danish customers check mortgage rates, loan terms and investment fees instantly; as of 2024, 68% of Danes used digital banking comparison sites when shopping financial products, raising price sensitivity. This transparency lets even novice investors demand better terms or switch: 42% report leaving a bank for cheaper fees in the past 12 months. Sydbank therefore faces continuous pressure to match market averages—mortgage spreads in Denmark averaged 0.45 percentage points in 2024—to stay competitive.

High Bargaining Power of Large Corporate Clients

Large corporates account for roughly 35% of Sydbank’s loan book (2024 annual report) and can demand bespoke pricing and covenants, raising their bargaining power.

These clients access both Danish and international lenders—Nordic banks, German commercial banks, and global syndicates—creating a buyer-favored market.

To retain them, Sydbank must offer tailored advisory, flexible credit lines, and competitive pricing; losing a single large client could cut several percent off corporate NPIs (net interest income).

Demand for Integrated Digital and Physical Services

Customers in 2025 expect seamless mobile banking plus local, in-person advice; Sydbank reported 63% of transactions via mobile in 2024 and 28% of clients still value branch meetings (Sydbank Annual Report 2024).

If Sydbank lags on tech, customers can switch to agile challengers; Nordic fintechs grew wallet share by 12% in 2023–24, raising churn risk.

This preference gives buyers power to set Sydbank’s digital roadmap and pace of investment.

- 63% mobile transactions (2024)

- 28% clients value branches (2024)

- Nordic fintech wallet +12% (2023–24)

Influence of Consumer Protection Regulations

- Forbrugerrådet Tænk drove 12% fee drop in 2023

- Danish FSA tightened disclosure in 2024

- Sydbank NIM 1.4% in 2024

- High churn risk if fees stay above peers

Customers wield power: low fees, easy switching, corporates demand bespoke terms

Customers have high bargaining power: digital switching (PSD2/APIs) cut friction ~40% (Nordic Payments 2024–25), 68% use comparison sites (2024), 42% left banks for fees (2024), large corporates = 35% loan book (Sydbank 2024) demand bespoke terms, and NIM 1.4% (2024) limits margin flexibility.

| Metric | Value |

|---|---|

| Switch friction | -40% |

| Comparison use | 68% |

| Left for fees | 42% |

| Corporate share | 35% |

| NIM | 1.4% |

Preview the Actual Deliverable

Sydbank Porter's Five Forces Analysis

This preview shows the exact Sydbank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the finished, professionally formatted report you’ll be able to download and use the moment you complete payment.

What you see is the full deliverable: a ready-to-use, comprehensive Five Forces assessment of Sydbank, available instantly after buying.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Sydbank faces moderate competitive intensity—strong local brand loyalty and scale advantages versus rising fintech rivals and margin pressure from low-rate lending; supplier power is limited but regulatory costs and digital investment elevate operational strain. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sydbank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on IT Infrastructure Providers

Sydbank depends heavily on Bankdata for core banking and digital infrastructure, creating supplier power since switching would cost an estimated DKK 200–400m and take 18–36 months for a mid-sized bank.

Technical complexity and data migration risks raise dependency, so Bankdata can demand premium terms that squeeze margins.

By late 2025, rising needs for advanced cybersecurity and AI (estimated 25–40% higher spend) further strengthen specialized vendors’ bargaining power.

Talent War for Specialized Financial Professionals

The Danish market for financial analysts and IT specialists stayed tight into 2025, with unemployment for finance grads at ~1.8% and tech vacancy rates near 4.2% (Danmarks Statistik, Q4 2024), forcing Sydbank to match offers from Danske Bank and Nordic fintechs.

To retain talent Sydbank increased average analyst pay ~6% in 2024 and flagged €10–15k sign-on packages for senior hires, raising personnel cost pressure and boosting supplier power in its service model.

Influence of Central Banks and Capital Markets

Sydbank funds itself via fragmented retail deposits and wholesale markets; at end-2024 Sydbank reported deposit funding covering ~62% of assets and wholesale debt ~18% (source: Sydbank 2024 annual report).

ECB rates and global bond yields set the baseline funding cost—ECB deposit rate rose to 4.00% in Dec 2023 and 3‑month EURIBOR averaged 3.5% through 2024—pressuring net interest margin.

Monetary policy shifts remain the main external constraint on margin management: a 100bp ECB cut would cut funding cost slowly; a 100bp hike in 2024‑style moves would have widened funding expense materially.

Regulatory Compliance and Audit Service Costs

Outsourcing of Non-Core Banking Functions

- Outsourcing spend ~DKK 450m (post-2023)

- Vendors more interchangeable than IT providers

- Higher specialization raises disruption risk

- Service delays can hit customer satisfaction

High supplier power: costly banklock, premium cyber/AI vendors & rising funding/reg costs

High supplier power: Bankdata dependency (switch cost DKK 200–400m; 18–36 months) plus specialized cyber/AI vendors (25–40% higher spend) and tight labor market (finance unemployment ~1.8%; tech vacancies 4.2%) raise costs; funding set by ECB rates (deposit rate 4.00% Dec 2023) and regulatory compliance (Sydbank regulatory costs +12% in 2024) further strengthen supplier power.

What is included in the product

Provides a concise Porter's Five Forces view of Sydbank, highlighting competitive rivalry, buyer/supplier leverage, entry barriers, and substitute threats with industry-backed insights tailored for strategic use.

Clear, one-sheet Porter's Five Forces for Sydbank—instantly spot competitive pressures and relieve strategic planning bottlenecks with a ready-to-use radar chart and editable pressure sliders.

Customers Bargaining Power

Low Switching Costs for Retail Banking

Digital platforms and open banking have cut switching time; EU-DK PSD2 adoption and Bankernes IT-Center APIs let Danish retail customers move accounts in days, not weeks.

By late 2025, automated switching services reduced friction ~40%, per Nordic Payments 2024–25 data, raising annual churn risk if fees or NPS lag peers.

Sydbank must keep service levels high and match fee reductions—median Danish checking fees fell 12% in 2024—to retain deposits and fee income.

Increased Price Transparency via Digital Tools

Online comparison tools let Danish customers check mortgage rates, loan terms and investment fees instantly; as of 2024, 68% of Danes used digital banking comparison sites when shopping financial products, raising price sensitivity. This transparency lets even novice investors demand better terms or switch: 42% report leaving a bank for cheaper fees in the past 12 months. Sydbank therefore faces continuous pressure to match market averages—mortgage spreads in Denmark averaged 0.45 percentage points in 2024—to stay competitive.

High Bargaining Power of Large Corporate Clients

Large corporates account for roughly 35% of Sydbank’s loan book (2024 annual report) and can demand bespoke pricing and covenants, raising their bargaining power.

These clients access both Danish and international lenders—Nordic banks, German commercial banks, and global syndicates—creating a buyer-favored market.

To retain them, Sydbank must offer tailored advisory, flexible credit lines, and competitive pricing; losing a single large client could cut several percent off corporate NPIs (net interest income).

Demand for Integrated Digital and Physical Services

Customers in 2025 expect seamless mobile banking plus local, in-person advice; Sydbank reported 63% of transactions via mobile in 2024 and 28% of clients still value branch meetings (Sydbank Annual Report 2024).

If Sydbank lags on tech, customers can switch to agile challengers; Nordic fintechs grew wallet share by 12% in 2023–24, raising churn risk.

This preference gives buyers power to set Sydbank’s digital roadmap and pace of investment.

- 63% mobile transactions (2024)

- 28% clients value branches (2024)

- Nordic fintech wallet +12% (2023–24)

Influence of Consumer Protection Regulations

- Forbrugerrådet Tænk drove 12% fee drop in 2023

- Danish FSA tightened disclosure in 2024

- Sydbank NIM 1.4% in 2024

- High churn risk if fees stay above peers

Customers wield power: low fees, easy switching, corporates demand bespoke terms

Customers have high bargaining power: digital switching (PSD2/APIs) cut friction ~40% (Nordic Payments 2024–25), 68% use comparison sites (2024), 42% left banks for fees (2024), large corporates = 35% loan book (Sydbank 2024) demand bespoke terms, and NIM 1.4% (2024) limits margin flexibility.

| Metric | Value |

|---|---|

| Switch friction | -40% |

| Comparison use | 68% |

| Left for fees | 42% |

| Corporate share | 35% |

| NIM | 1.4% |

Preview the Actual Deliverable

Sydbank Porter's Five Forces Analysis

This preview shows the exact Sydbank Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the finished, professionally formatted report you’ll be able to download and use the moment you complete payment.

What you see is the full deliverable: a ready-to-use, comprehensive Five Forces assessment of Sydbank, available instantly after buying.