Symrise SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Symrise combines strong R&D, diversified product lines, and global reach to capitalize on premiumization and natural ingredient trends, while facing margin pressure from raw material volatility and intense competition; our full SWOT dives deeper into financials, market threats, and strategic options. Purchase the complete SWOT for a professionally formatted Word report and editable Excel matrix to support investment, strategy, or pitch work.

Strengths

Diversified Portfolio Across Taste and Scent

Symrise keeps revenue balanced between Taste, Nutrition & Health and Scent & Care, with 2024 pro forma sales about €5.7bn and roughly 50/50 segment split, which cuts exposure to shocks in luxury perfumes or food cycles.

Serving food, beverage, personal care, pharma and pet markets supports steady cash flow—2024 adjusted EBIT margin ~15%—and gives Symrise an edge versus niche ingredient peers.

Strong Leadership in Sustainable Sourcing

Symrise leads in backward integration and ethical sourcing, owning long-term contracts and plantations for vanilla and botanicals, cutting supply shocks—vanilla costs volatility down 30% for integrated firms in 2024, per industry data.

Direct access to key ingredients boosts quality control and supports global clients, while sustainability claims meet rising demand: 72% of EU consumers in 2023 prefer transparent sourcing.

This supply-chain strength helps protect margins and attracted ESG investors; Symrise reported 2024 adjusted EBITDA margin of 18.6%, up 120 bps year-on-year, reflecting operational resilience.

High Investment in Research and Development

Symrise reinvests heavily in R&D, spending about 6.1% of 2024 revenue (≈€327m of €5.36bn) to develop proprietary molecules and functional ingredients, driving ~120 new product launches in 2024 and a steady patent pipeline (over 1,100 active family patents).

Extensive Global Presence and Emerging Market Reach

Symrise operates production sites and creative centers in over 40 countries, giving it local market insights and 2024 revenues of about EUR 4.9bn that benefit from geographic diversity.

The company has grown strongly in Asia, Latin America and Africa, where sales rose roughly 7–9% CAGR 2019–2024, capturing rising middle-class demand and regional tastes.

Local operations cut logistics costs, speed delivery to beverage and cosmetic clients, and support margins—EM sales now ~35% of group revenue.

- 40+ countries footprint

- 2024 revenue ~EUR 4.9bn

- EM sales ≈35% of revenue

- Asia/LatAm/Africa CAGR ~7–9% (2019–2024)

Robust Financial Performance and Dividend Consistency

Symrise delivered 2024 sales of €5.2bn and adjusted EBITDA margin ~18%, showing steady growth versus 2021–23 despite inflation and FX headwinds.

Management pairs disciplined M&A—€0.5bn spent on strategic deals since 2022—with a progressive dividend (2024 payout €1.00/share), underpinned by long-term contracts with top FMCG clients.

Investors praise steady returns, transparent reporting, and balance-sheet strength: net debt/EBITDA ~1.8x at Dec 31, 2024.

- 2024 sales €5.2bn

- Adj. EBITDA margin ~18%

- Net debt/EBITDA ~1.8x (Dec 31, 2024)

- Dividend €1.00/share (2024)

Balanced €5.7bn portfolio: 18% EBITDA, heavy R&D, strong cash flow & low leverage

Diversified portfolio with 2024 pro forma sales ~€5.7bn and ~50/50 split between Taste, Nutrition & Health and Scent & Care; adjusted EBITDA margin ~18% and adj. EBIT ~15% support steady cash flow. Strong vertical integration (vanilla/botanicals), €327m R&D (6.1% of 2024 revenue), 1,100+ patent families, 40+ country footprint, EM sales ~35%, net debt/EBITDA ~1.8x.

| Metric | 2024 |

|---|---|

| Pro forma sales | €5.7bn |

| Reported sales | €5.2bn |

| Adj. EBITDA margin | ~18% |

| R&D spend | €327m (6.1%) |

| Patent families | 1,100+ |

| EM sales | ~35% |

| Net debt/EBITDA | ~1.8x |

What is included in the product

Delivers a concise strategic overview of Symrise by outlining its core strengths and weaknesses, mapping growth opportunities and external threats, and evaluating how internal capabilities and market dynamics shape the company’s competitive position.

Delivers a concise Symrise SWOT matrix for rapid strategic alignment and clear stakeholder communication.

Weaknesses

Exposure to Raw Material Price Volatility

As a manufacturer reliant on natural ingredients, Symrise faces sharp cost swings from climate-driven crop failures and geopolitics; essential oil and agricultural inputs rose ~18% YoY in 2023-24 in the flavors & fragrances sector, squeezing margins if prices can’t be passed to clients.

Variations in chemicals and raw materials can compress gross margin—Symrise reported a 2024 adjusted EBIT margin of ~15.4%, sensitive to input spikes—and forces complex hedging and supplier diversification.

Maintaining short-term earnings predictability is hard: hedges add cost and basis risk, and sudden input surges can still cause quarterly profit volatility despite risk programs.

Significant Debt Levels from Historical Acquisitions

Symrise’s aggressive M&A has lifted revenue and market share but pushed net debt to about €3.6bn at FY2024 year-end, raising net leverage to roughly 2.6x EBITDA; servicing costs tighten cash flow when ECB rates are elevated.

Management must pare leverage to keep its investment-grade rating (BBB range from S&P/Moody’s in 2024) or face higher borrowing costs, which would limit capacity for large bolt‑on deals.

Complex Integration of Diverse Business Units

Operating across specialized segments—pet food, cosmetic actives, fine fragrances—adds organizational complexity; Symrise’s 2024 pro forma revenue mix (53% nutrition, 47% fragrances & care) shows broad scope that complicates coordination.

Post-acquisition integration of cultures and IT (Symrise closed >10 deals 2019–2024) risks inefficiencies and delayed synergies, hurting margin targets.

Management must allocate significant resources to avoid duplicate costs; SG&A was €1.45bn in 2024, straining agility.

This internal complexity can slow decisions versus leaner rivals, risking slower go-to-market and missed fast-moving trends.

High Dependency on Key Global Accounts

- ~40% 2024 revenue from top 10 accounts

- High buyer bargaining power → margin pressure

- Loss of one major contract → mid-single-digit EBIT swing (est.)

- Requires sustained R&D and service investment

Vulnerability to Currency Exchange Fluctuations

With ~60% of 2024 sales outside the eurozone, Symrise faces material foreign-exchange risk; a 5% EUR/USD move swung reported EBIT by an estimated €40–€60m in 2024.

Translation losses from weaker euros versus emerging-market currencies and USD can dent reported earnings despite hedges; full insulation is impractical given global scale.

Currency volatility thus remains a recurring headwind that can mask true operational trends.

- ~60% 2024 sales outside eurozone

- 5% EUR/USD move ≈ €40–€60m EBIT impact (2024)

- Hedges reduce but do not eliminate risk

- Volatility can obscure organic performance

Symrise risk snapshot: input inflation, high leverage, customer concentration & FX exposure

Symrise’s weaknesses: input-cost volatility from climate/geopolitics (essential oils +18% YoY 2023–24) squeezes margins; net debt €3.6bn and leverage ~2.6x EBITDA limits deal firepower; ~40% revenue from top‑10 customers gives buyers pricing power; ~60% sales outside eurozone, where a 5% EUR/USD move affected EBIT by ~€40–€60m in 2024.

| Metric | 2024 |

|---|---|

| Essential oil input change | +18% YoY |

| Adjusted EBIT margin | ~15.4% |

| Net debt | €3.6bn |

| Leverage | ~2.6x EBITDA |

| Top‑10 customer share | ~40% |

| Sales outside eurozone | ~60% |

| 5% EUR/USD EBIT impact | €40–€60m |

What You See Is What You Get

Symrise SWOT Analysis

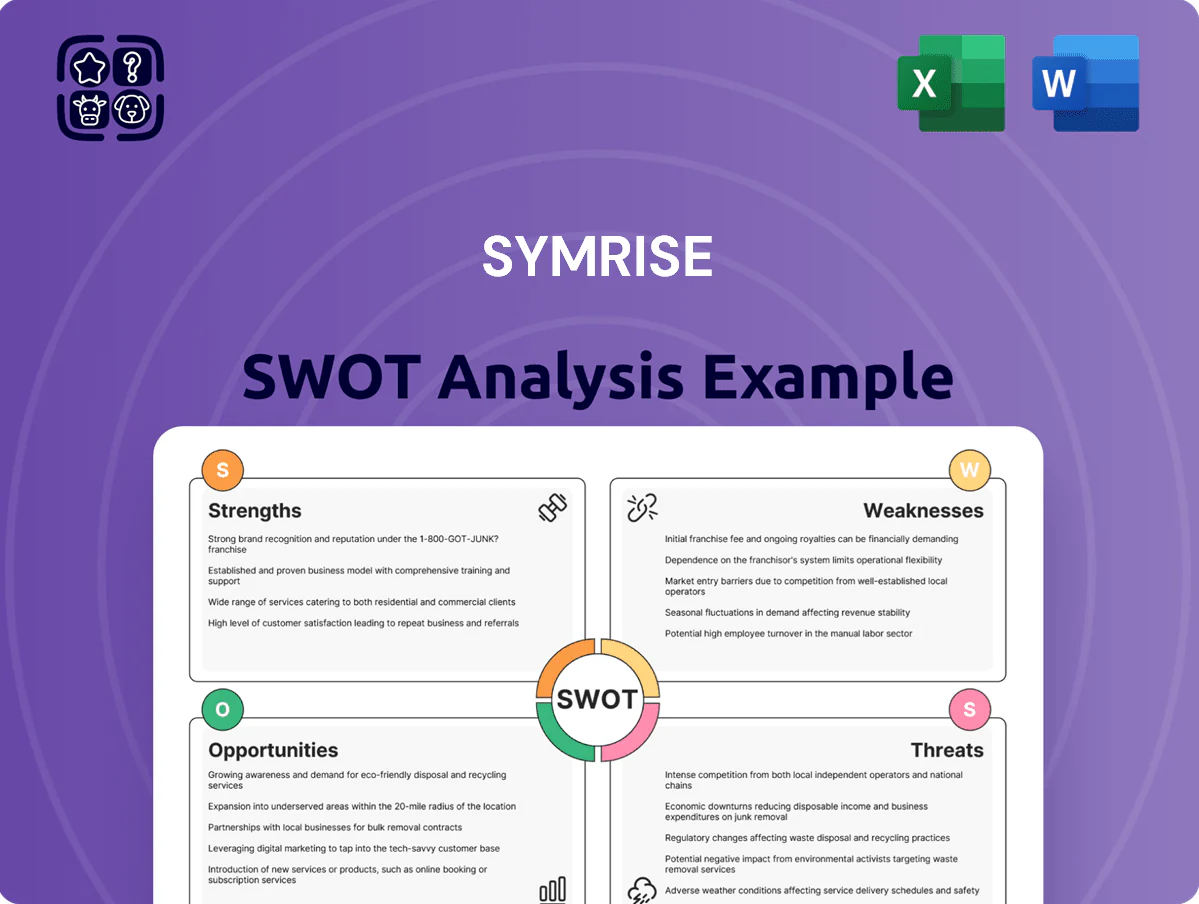

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the real, editable file included in your download. Buy now to unlock the complete, detailed version immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Symrise combines strong R&D, diversified product lines, and global reach to capitalize on premiumization and natural ingredient trends, while facing margin pressure from raw material volatility and intense competition; our full SWOT dives deeper into financials, market threats, and strategic options. Purchase the complete SWOT for a professionally formatted Word report and editable Excel matrix to support investment, strategy, or pitch work.

Strengths

Diversified Portfolio Across Taste and Scent

Symrise keeps revenue balanced between Taste, Nutrition & Health and Scent & Care, with 2024 pro forma sales about €5.7bn and roughly 50/50 segment split, which cuts exposure to shocks in luxury perfumes or food cycles.

Serving food, beverage, personal care, pharma and pet markets supports steady cash flow—2024 adjusted EBIT margin ~15%—and gives Symrise an edge versus niche ingredient peers.

Strong Leadership in Sustainable Sourcing

Symrise leads in backward integration and ethical sourcing, owning long-term contracts and plantations for vanilla and botanicals, cutting supply shocks—vanilla costs volatility down 30% for integrated firms in 2024, per industry data.

Direct access to key ingredients boosts quality control and supports global clients, while sustainability claims meet rising demand: 72% of EU consumers in 2023 prefer transparent sourcing.

This supply-chain strength helps protect margins and attracted ESG investors; Symrise reported 2024 adjusted EBITDA margin of 18.6%, up 120 bps year-on-year, reflecting operational resilience.

High Investment in Research and Development

Symrise reinvests heavily in R&D, spending about 6.1% of 2024 revenue (≈€327m of €5.36bn) to develop proprietary molecules and functional ingredients, driving ~120 new product launches in 2024 and a steady patent pipeline (over 1,100 active family patents).

Extensive Global Presence and Emerging Market Reach

Symrise operates production sites and creative centers in over 40 countries, giving it local market insights and 2024 revenues of about EUR 4.9bn that benefit from geographic diversity.

The company has grown strongly in Asia, Latin America and Africa, where sales rose roughly 7–9% CAGR 2019–2024, capturing rising middle-class demand and regional tastes.

Local operations cut logistics costs, speed delivery to beverage and cosmetic clients, and support margins—EM sales now ~35% of group revenue.

- 40+ countries footprint

- 2024 revenue ~EUR 4.9bn

- EM sales ≈35% of revenue

- Asia/LatAm/Africa CAGR ~7–9% (2019–2024)

Robust Financial Performance and Dividend Consistency

Symrise delivered 2024 sales of €5.2bn and adjusted EBITDA margin ~18%, showing steady growth versus 2021–23 despite inflation and FX headwinds.

Management pairs disciplined M&A—€0.5bn spent on strategic deals since 2022—with a progressive dividend (2024 payout €1.00/share), underpinned by long-term contracts with top FMCG clients.

Investors praise steady returns, transparent reporting, and balance-sheet strength: net debt/EBITDA ~1.8x at Dec 31, 2024.

- 2024 sales €5.2bn

- Adj. EBITDA margin ~18%

- Net debt/EBITDA ~1.8x (Dec 31, 2024)

- Dividend €1.00/share (2024)

Balanced €5.7bn portfolio: 18% EBITDA, heavy R&D, strong cash flow & low leverage

Diversified portfolio with 2024 pro forma sales ~€5.7bn and ~50/50 split between Taste, Nutrition & Health and Scent & Care; adjusted EBITDA margin ~18% and adj. EBIT ~15% support steady cash flow. Strong vertical integration (vanilla/botanicals), €327m R&D (6.1% of 2024 revenue), 1,100+ patent families, 40+ country footprint, EM sales ~35%, net debt/EBITDA ~1.8x.

| Metric | 2024 |

|---|---|

| Pro forma sales | €5.7bn |

| Reported sales | €5.2bn |

| Adj. EBITDA margin | ~18% |

| R&D spend | €327m (6.1%) |

| Patent families | 1,100+ |

| EM sales | ~35% |

| Net debt/EBITDA | ~1.8x |

What is included in the product

Delivers a concise strategic overview of Symrise by outlining its core strengths and weaknesses, mapping growth opportunities and external threats, and evaluating how internal capabilities and market dynamics shape the company’s competitive position.

Delivers a concise Symrise SWOT matrix for rapid strategic alignment and clear stakeholder communication.

Weaknesses

Exposure to Raw Material Price Volatility

As a manufacturer reliant on natural ingredients, Symrise faces sharp cost swings from climate-driven crop failures and geopolitics; essential oil and agricultural inputs rose ~18% YoY in 2023-24 in the flavors & fragrances sector, squeezing margins if prices can’t be passed to clients.

Variations in chemicals and raw materials can compress gross margin—Symrise reported a 2024 adjusted EBIT margin of ~15.4%, sensitive to input spikes—and forces complex hedging and supplier diversification.

Maintaining short-term earnings predictability is hard: hedges add cost and basis risk, and sudden input surges can still cause quarterly profit volatility despite risk programs.

Significant Debt Levels from Historical Acquisitions

Symrise’s aggressive M&A has lifted revenue and market share but pushed net debt to about €3.6bn at FY2024 year-end, raising net leverage to roughly 2.6x EBITDA; servicing costs tighten cash flow when ECB rates are elevated.

Management must pare leverage to keep its investment-grade rating (BBB range from S&P/Moody’s in 2024) or face higher borrowing costs, which would limit capacity for large bolt‑on deals.

Complex Integration of Diverse Business Units

Operating across specialized segments—pet food, cosmetic actives, fine fragrances—adds organizational complexity; Symrise’s 2024 pro forma revenue mix (53% nutrition, 47% fragrances & care) shows broad scope that complicates coordination.

Post-acquisition integration of cultures and IT (Symrise closed >10 deals 2019–2024) risks inefficiencies and delayed synergies, hurting margin targets.

Management must allocate significant resources to avoid duplicate costs; SG&A was €1.45bn in 2024, straining agility.

This internal complexity can slow decisions versus leaner rivals, risking slower go-to-market and missed fast-moving trends.

High Dependency on Key Global Accounts

- ~40% 2024 revenue from top 10 accounts

- High buyer bargaining power → margin pressure

- Loss of one major contract → mid-single-digit EBIT swing (est.)

- Requires sustained R&D and service investment

Vulnerability to Currency Exchange Fluctuations

With ~60% of 2024 sales outside the eurozone, Symrise faces material foreign-exchange risk; a 5% EUR/USD move swung reported EBIT by an estimated €40–€60m in 2024.

Translation losses from weaker euros versus emerging-market currencies and USD can dent reported earnings despite hedges; full insulation is impractical given global scale.

Currency volatility thus remains a recurring headwind that can mask true operational trends.

- ~60% 2024 sales outside eurozone

- 5% EUR/USD move ≈ €40–€60m EBIT impact (2024)

- Hedges reduce but do not eliminate risk

- Volatility can obscure organic performance

Symrise risk snapshot: input inflation, high leverage, customer concentration & FX exposure

Symrise’s weaknesses: input-cost volatility from climate/geopolitics (essential oils +18% YoY 2023–24) squeezes margins; net debt €3.6bn and leverage ~2.6x EBITDA limits deal firepower; ~40% revenue from top‑10 customers gives buyers pricing power; ~60% sales outside eurozone, where a 5% EUR/USD move affected EBIT by ~€40–€60m in 2024.

| Metric | 2024 |

|---|---|

| Essential oil input change | +18% YoY |

| Adjusted EBIT margin | ~15.4% |

| Net debt | €3.6bn |

| Leverage | ~2.6x EBITDA |

| Top‑10 customer share | ~40% |

| Sales outside eurozone | ~60% |

| 5% EUR/USD EBIT impact | €40–€60m |

What You See Is What You Get

Symrise SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the real, editable file included in your download. Buy now to unlock the complete, detailed version immediately after checkout.